Meeting of the

Finance Audit & Risk Sub-committee

Date: 2 March 2022

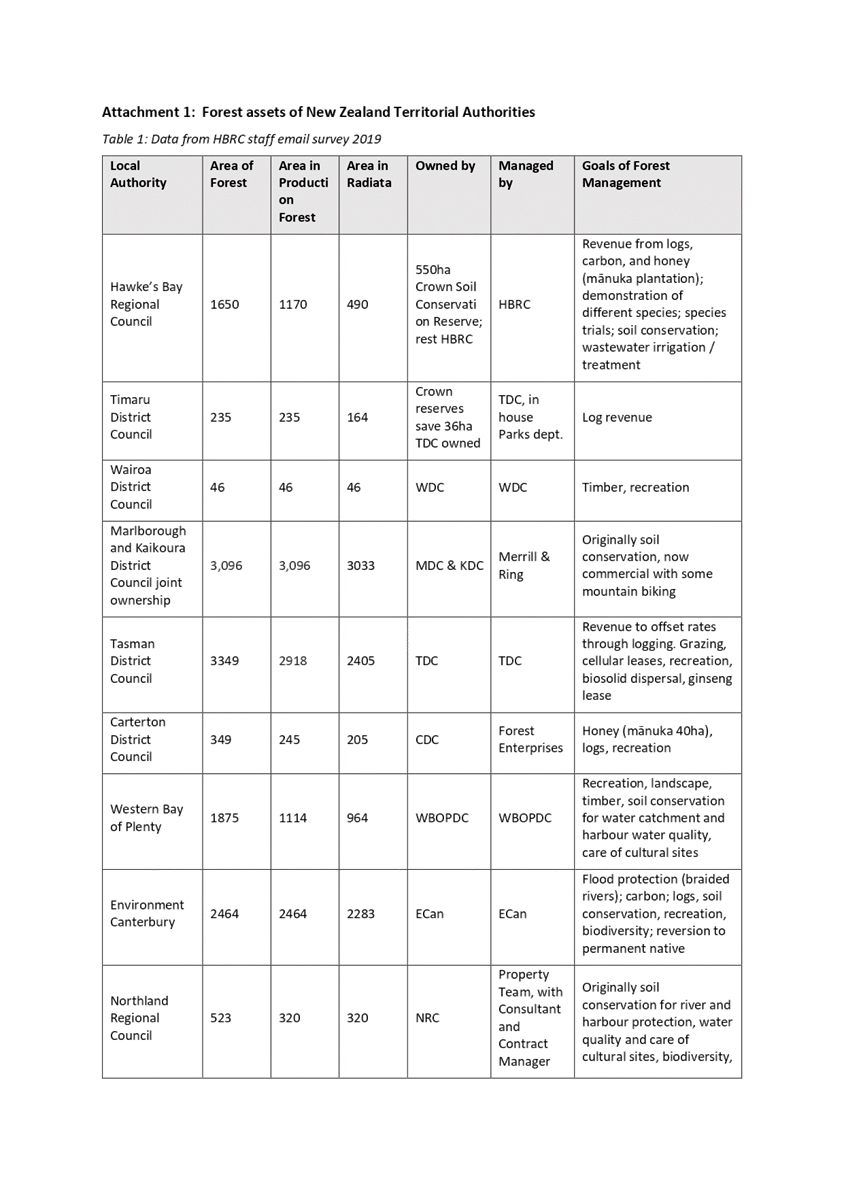

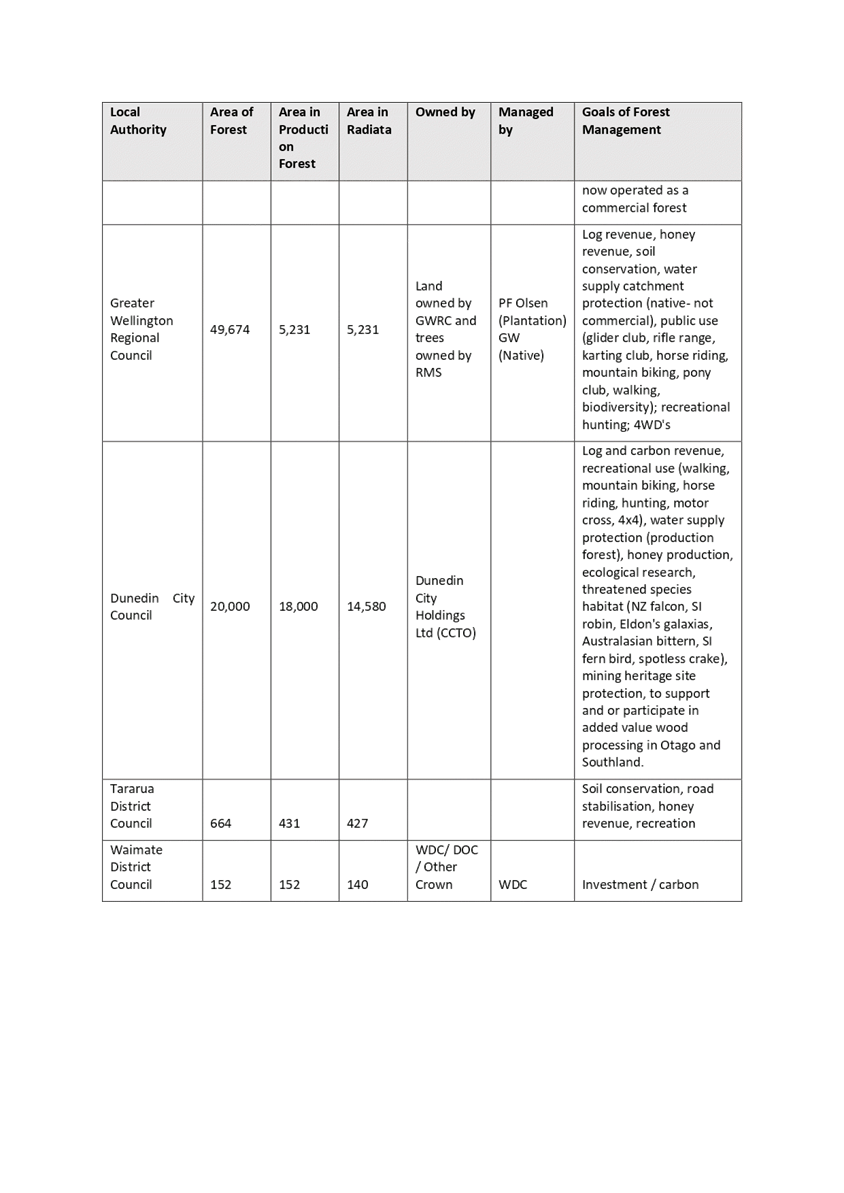

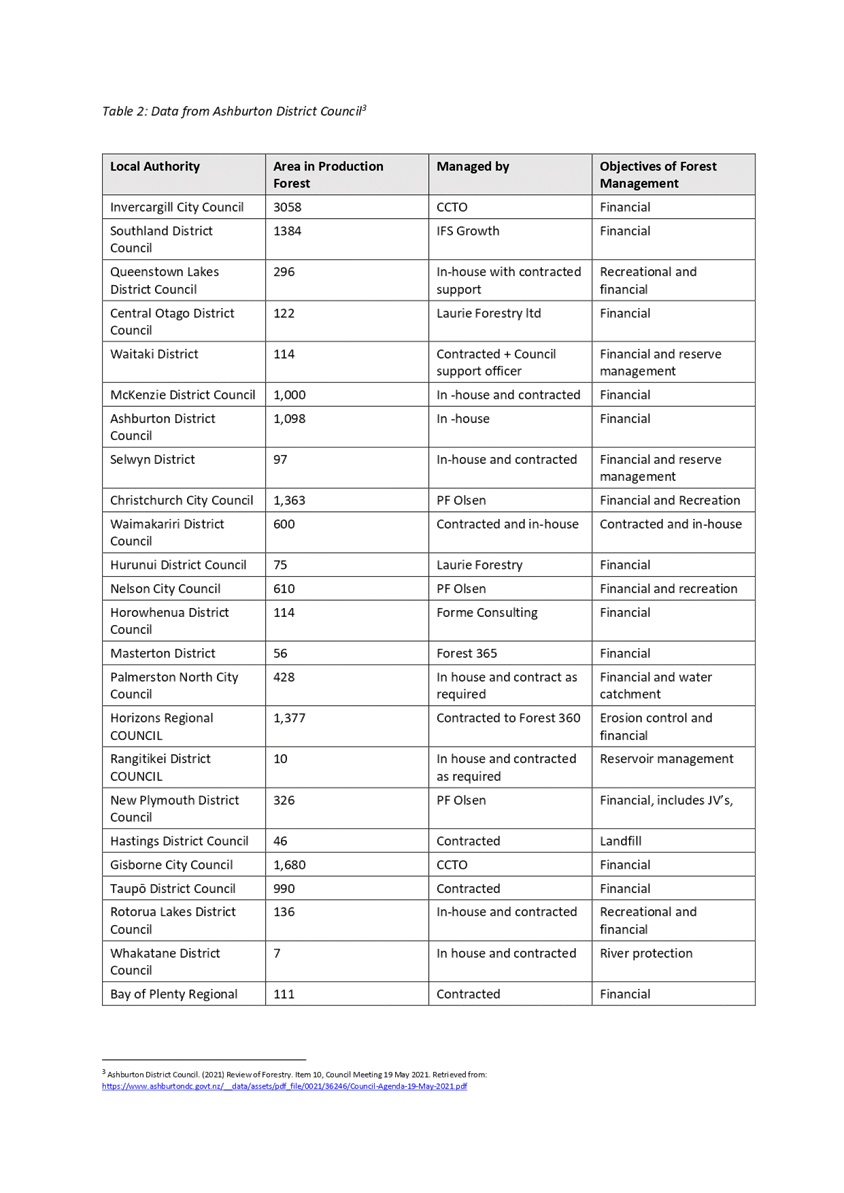

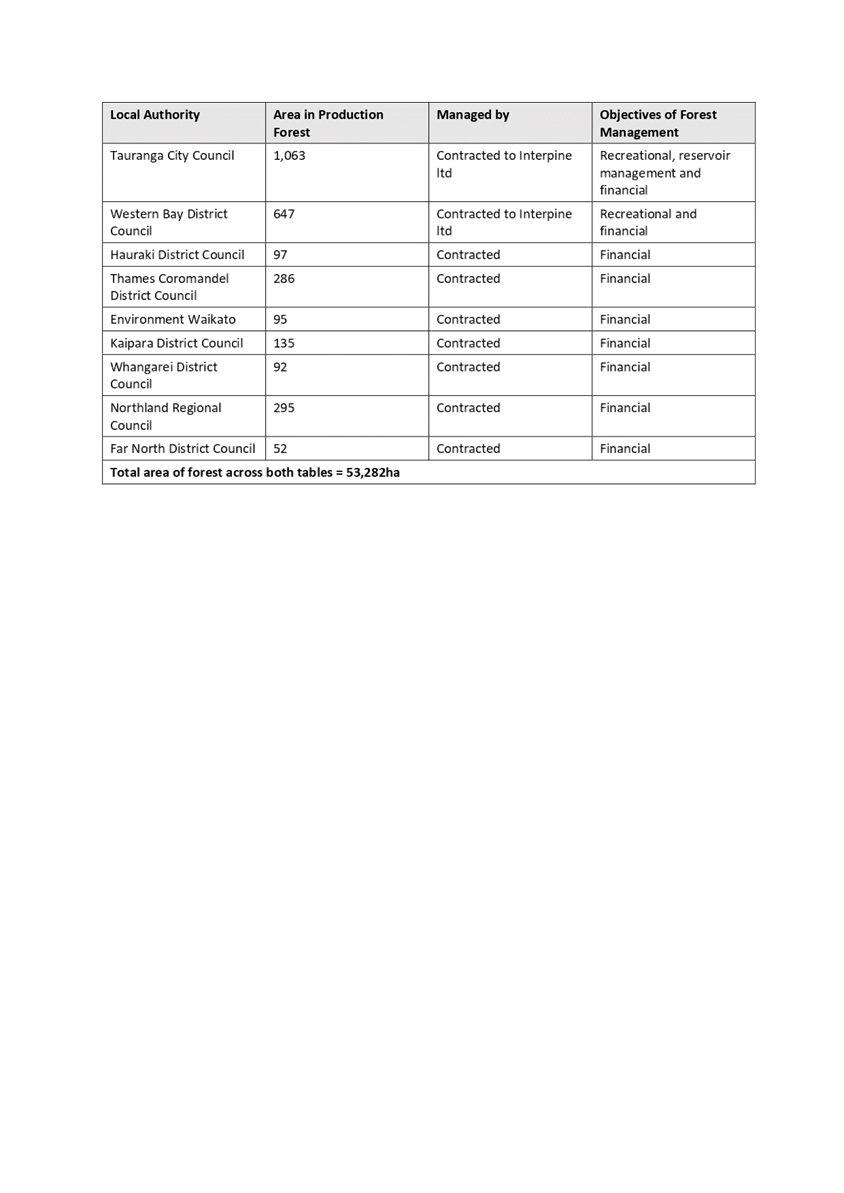

Time: 9.00am

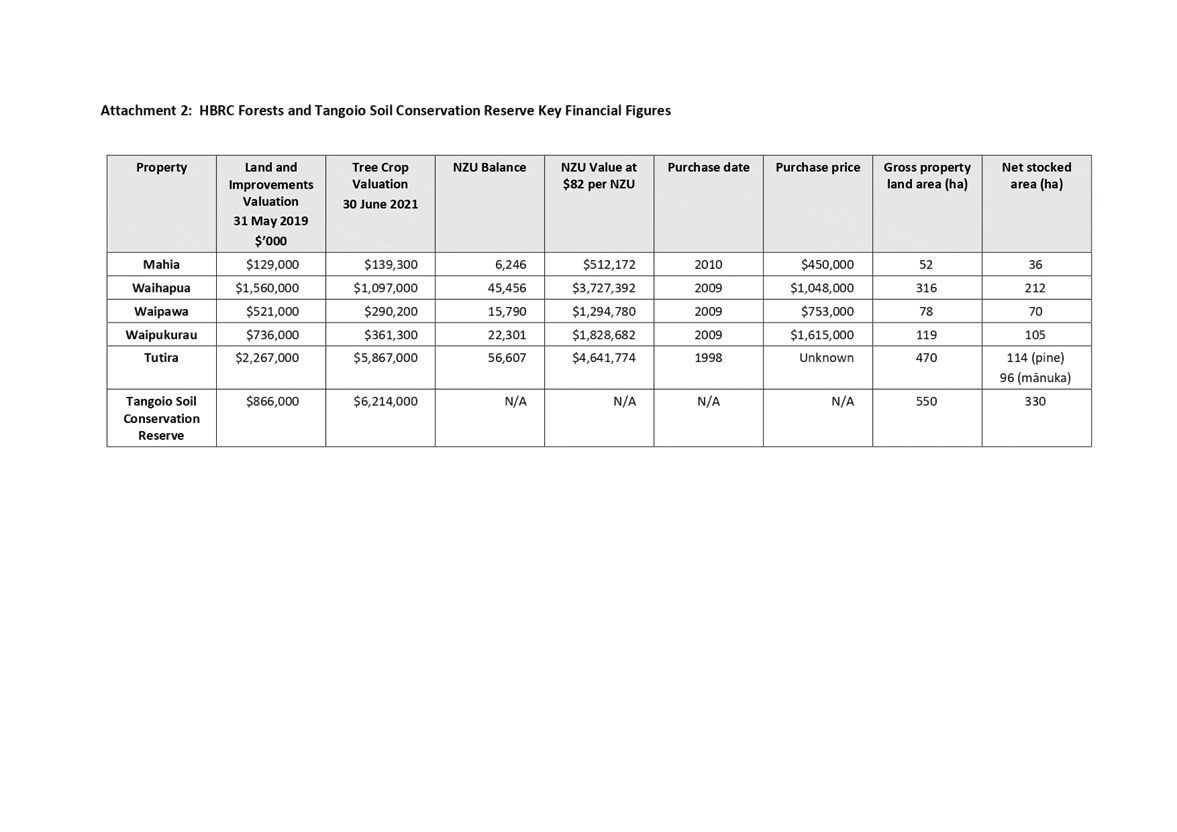

|

Venue:

|

Council

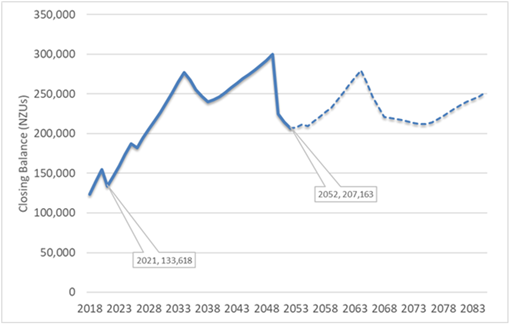

Chamber

Hawke's

Bay Regional Council

159

Dalton Street

NAPIER

|

Agenda

Item Title Page

1. Welcome/Notices/Apologies

2. Conflict

of Interest Declarations

3. Confirmation of Minutes of

the Finance Audit & Risk Sub-committee meeting held on 15 December 2021

4. Six

Monthly Enterprise Risk Report 3

5. Risk

Maturity Update 35

6. Internal

Audit Annual Plan Status Update FY2021-2022 39

7. Annual

Internal Assurance Plan 2022-2023 41

8. 2020-2021

Annual Report Audit Update 45

9. Quarterly

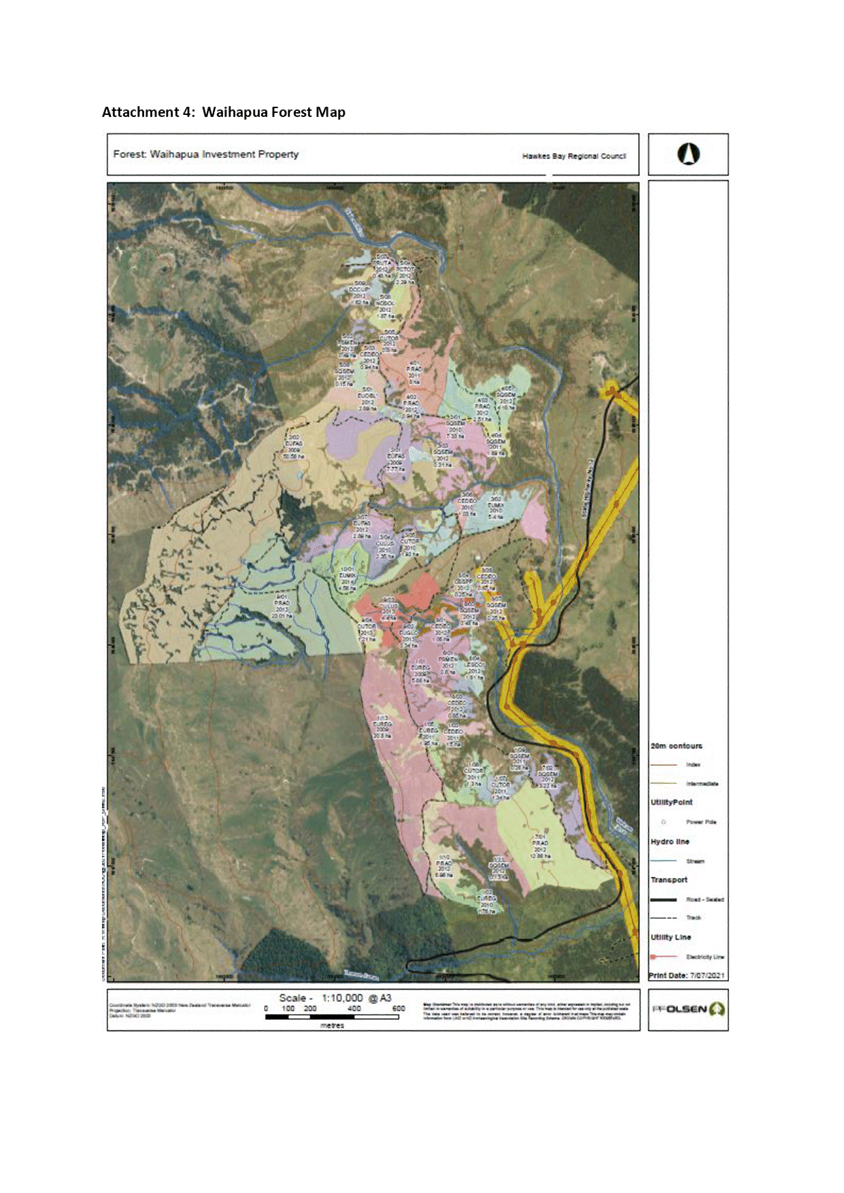

Treasury Report for 1 October – 31 December 2021 49

10. HBRC

Forestry Update 79

11. Tūtira

Mānuka Plantation Update 103

12. Internal

Assurance Dashboard - Corrective Actions Status Update 117

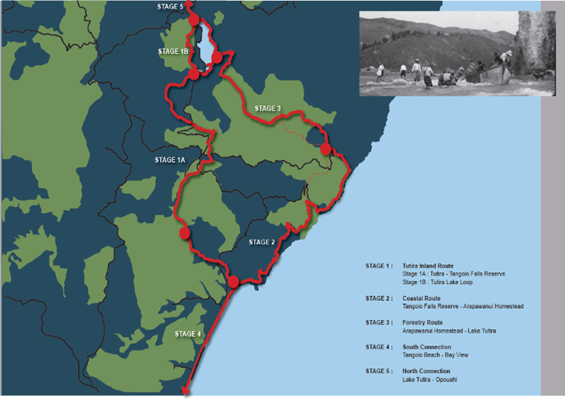

13. Talent

Management Internal Audit Update 129

15. Scope

for Fund Manager Review (late item to come)

Public

Excluded

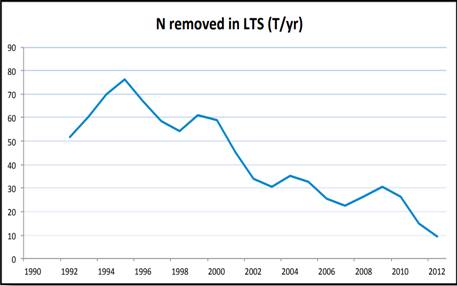

14. Internal

Assurance Dashboard - Cyber Security Corrective Actions Status Update 133

HAWKE’S BAY REGIONAL

COUNCIL

Finance

Audit & Risk Sub-committee

02 March

2022

Subject: Six Monthly Enterprise Risk

Report

Reason for Report

1. This item and the accompanying

enterprise risk report provide the Finance Audit and Risk Sub-committee (FARS)

with the six-monthly update of Council’s enterprise risk profile. The

update in the report includes the review of:

1.1. The enterprise risks and

risk descriptions

1.2. The inherent and residual

risk ratings for each enterprise risk

1.3. The overall control

assessment and control corrective actions for each enterprise risk

1.4. Supporting risk information

that may impact Council’s risk profile, including a regulatory/legal

update, business incidents, internal audits, material internal change projects,

and emerging issues or uncertainties.

Officers’

Recommendations

2. Council Officers recommend

that the Sub-committee notes the revised enterprise risks, control corrective

actions, and supporting risk information.

Background/Discussion

3. At the Regional Council

meeting held on 30 September 2020 the Risk Management Framework was approved by

Council. The Framework requires that the FARS receives and reviews the

enterprise risk report at least six monthly. Therefore, this paper presents to

the FARS the Council’s enterprise risk report as of February 2022.

4. In assessing the overall

residual risk ratings, the external emerging issues considered were:

4.1. Magnitude, broadness and

complexity of regulatory change that is likely to impact Council, including:

climate change national adaption plan, emissions reduction plan, resource

management reform, national standards for management of human drinking water

resources, national standards for freshwater amendments, and national standards

for air quality amendments

4.2. Covid-19 variant mutations

including New Zealand’s current Omicron outbreak and the impact of the

government lead response through the phased traffic light system, including

isolation and testing requirements, and the impact on supply chains

4.3. Economic outlook and

forecasts for interest and inflation rates

4.4. The competitive New Zealand

labour market and the labour market post border restrictions

4.5. Heightened geo-political

tensions with far reaching impacts on global financial markets e.g.

Ukraine/Russia

4.6. Climate change and global

climate action delays as the world responds to the immediate risks of: Covid-19

pandemic, economic instability (including asset bubbles), and geopolitical

tensions and the impact these global and national distractions may have on

Council’s strategy for climate change.

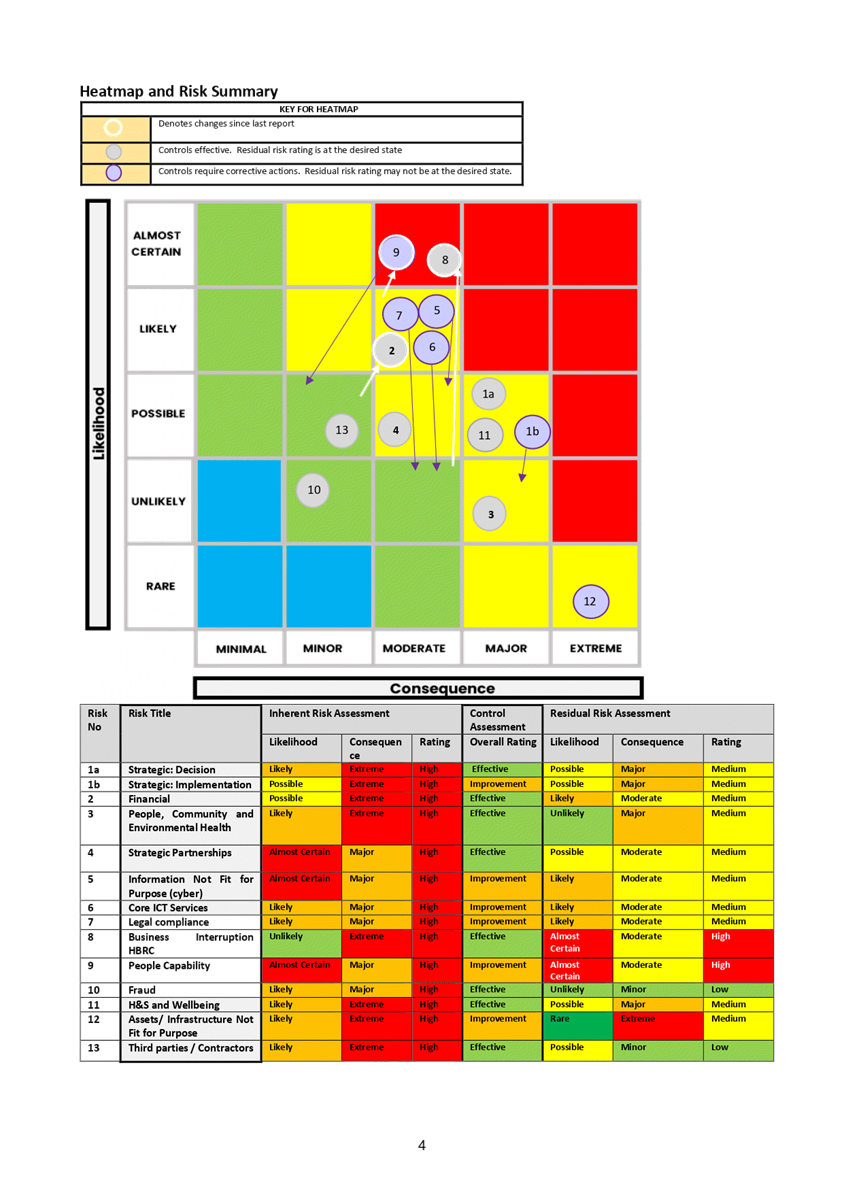

5. The following material

changes are noted in the February 2022 Enterprise Risk Report when compared to

the enterprise risk report presented to the FARS at the July 2021 meeting.

Risk

2 – Financial

5.1. The emerging issues noted

under bullet point four above are creating global and domestic uncertainties

within the financial markets. While Council’s financial

controls are effective at managing its financial position. The high

levels of uncertainties and current levels of volatility within the financial

markets has increased the residual likelihood assessment to

‘Likely’ and the overall financial impact to

‘Moderate’. With the overall residual risk rating increasing

to ‘Medium’. This risk is

being closely monitored by the Finance Team and constantly reviewed by the

Leadership team.

Risk

8 – Business Interruption

5.2. In response to the recent

Omicron Covid-19 outbreak and associated isolation mandates, Council’s pandemic plan was updated

to include:

5.2.1. mandating of vaccinations

for Council employees

5.2.2. work bubbles for all

critical roles

5.2.3. surgical masks for all

staff

5.2.4. Covid-19 passport

verification and sign in for Dalton Street and Station Street

‘private’ areas

5.2.5. Covid-19 sign-in and

physical distancing for meetings in the Council Chamber

5.2.6. access to rapid antigen

tests (RATS). It is noted the pandemic plan remains fluid and is continually

reviewed and updated by management to ensure that it remains relevant to the

evolving situation.

5.3. However, due to the Omicron

outbreak and associated

isolation rules the business interruption likelihood assess has been elevated

to ‘almost certain’. While additional measures in the pandemic plan

limit the extent of isolation requirements for Council staff. Council

needs to engage with strategic partners such as landowners and others in the

community to deliver on strategic activities. Therefore, it is almost certain

execution of some strategic objectives for FY2022 will be impacted, however,

the extent of that impact remains unchanged as ‘moderate. The overall

residual risk rating for this risk has therefore increased from

‘medium’ to ‘high’.

5.4. It is noted that the tight

labour market and risks associated work pressures on staff to cover vacant

positions, is being monitored under risk nine ‘People Capability’.

The convergence of the tight labour market coupled with alternate working

arrangements due to the Omicron outbreak could potentially elevate this

business interruption risk impact. Therefore, staff vacancies are being closely

monitored through the Omicron outbreak.

5.5. It is also noted that, late

2021 in response to the growing Covid threat from emerging mutations and border

containment breaches, a review of Council’s resilience to supply chain

disruption was undertaken. Council’s suppliers of business-critical

goods/services were proactively contacted and where necessary additional stocks

were procured to ensure that the Hawke’s Bay Regional Council (HBRC)

could operate independently and uninterrupted for a period of at least three

months. The review also considered the level of critical stock and spares

required should HBRC be required to respond to a regional crisis in addition to

Covid-19. New processes have also been established so that if key supply chains

become disrupted a review of supplies will be undertaken two months before supplies

are depleted.

Risk

9 – People Capability

5.6. Three aspects where

consider when assessing the overall residual rating of this risk covering

short-, medium- and longer-term uncertainties. The short-term uncertainties

(immediate risks) are driving the overall residual risk rating of

‘high’.

Medium

Term

5.7. The overall residual risk

rating for this risk was reported in the last risk report as

‘medium’ which was an elevated assessment. The elevated assessment

reflected the internal

audit of Council’s talent management framework/system which determined a

low level of maturity. And, while the talent management (P&C) strategy is

drafted implementation of the elements required to mature the framework will

take time. Maturity of Council’s talent management framework will help to

manage Council’s people capability risk, both day to day and in more

challenging times. However, it is recognised that maturity of the talent

management framework alone will not necessarily be enough to ensure a positive

staff experience. The corporate plan is designed to look more holistically at

Council’s culture, processes, frameworks and systems to ensure these are

effective in design to enable staff to work ‘smarter’ and execute

on strategy (see the longer-term update below).

Longer Term

5.8. A Corporate Plan has been

developed and is continually being refined and improved. The plan is currently

being reviewed to ensure that as the organisation grows and matures its key

management frameworks/systems the subsequent maturity activities are

prioritised to ensure foundational elements that help the operational business

work ‘smarter’ are addressed first. Also, that as these maturity

activities are rolled out and embedded into the business-related changes to the

way the business operates are effectively managed and sustained within

Council’s operating rhythm. The management of change also ensures that

potential disruption and impacts to staff due to the maturity of key management

frameworks are anticipated and minimised.

Short

Term (immediate risk)

5.9. An outcome of NZ’s

response to Covid-19 and the prolonged closures of borders has meant

unemployment has fallen and the employment market is highly competitive.

Without a mature talent management framework there is real pressure on

responding to the immediate people risk and minimise the convergence this risk

has on Council’s business interruption risk. Therefore, due to the

immediate employment market pressures the likelihood of this risk has now been

elevated to ‘almost certain’ while the impact assessment has

remained unchanged as ‘moderate’. The overall residual risk rating

has increased to ‘high’. The People and Capability (P&C) team,

together with management, are working through short term mitigations for this

risk which includes reviewing all strategic and smaller team projects them

applying a risk-based lens to determine which of these projects or project

milestones maybe paused without significantly disrupting delivery of key

strategic objectives. Where practical ‘people’ resources assigned

these projects can then be redeployed to areas with an immediate need.

6. Lastly, given

Council’s mandate for visibility and aesthetics consideration was given

to including climate change as a separate risk on the enterprise risk report.

Climate change is currently weaved through all relevant enterprise risks and

documented in those risks as either a risk cause or impact and therefore

explicitly considered in each of those risk assessments. Consequently, climate

change has not been added as a standalone risk. However, the Climate Change

Ambassador recently started at Council. A formal review of climate change will

be undertaken with the Ambassador’s to leverage off her technical

expertise. Therefore, inclusion of a separate enterprise climate changes will

be reconsidered then.

Strategic Fit

7. The six-monthly risk report

facilitates discussions to ensure that any emerging matters within the

Council’s internal and external environment are being managed. And,

therefore unlikely to impact on the Council’s ability to deliver on its

strategy. In addition, the maturity of the Council’s risk management

system contributes towards achieving excellence in execution of strategy. A

mature risk system provides consistent risk intelligent decision making

enabling the efficient prioritisation of finite organisational resources to

deliver on strategy.

Financial

and Resource Implications

8. There are no additional or

significant budgetary requirements resulting from control corrective actions

noted within the risk report that have not already been accounted for through

the LTP or BAU activities.

Decision Making Process

9. Council and its committees

are required to make every decision in accordance with the requirements of the

Local Government Act 2002 (the Act). Staff have assessed the requirements in

relation to this item and have concluded:

9.1. The decision of the

Sub-committee is in accordance with the Terms of Reference and decision-making

delegations adopted by Hawke’s Bay Regional Council on 25 March

2020, specifically the Finance, Audit and Risk Sub-committee shall have

responsibility and authority to:

9.1.1. Review whether Council

management has a current and comprehensive risk management framework and

associated procedures for effective identification and management of the

council’s significant risks in place

9.1.2. Undertake periodic

monitoring of corporate risk assessment, and the internal controls instituted

in response to such risks

9.1.3. report on the robustness of

risk management systems, processes and practices to the Corporate and Strategic

Committee to fulfil its responsibilities.

Recommendations

That the Finance, Audit and Risk

Sub-committee:

1. Receives and considers the

“Six Monthly Enterprise Risk” staff report.

2. Reports to the Corporate

and Strategic Committee, the Sub-committee’s satisfaction that the Six-Monthly

Enterprise Risk Report provides adequate evidence of the robustness of

Council’s risk management policy and framework and progress to implement

the maturing risk management system.

Authored by:

|

Helen Marsden

Risk & Corporate Compliance

Manager

|

|

Approved by:

|

Jessica Ellerm

Group Manager Corporate Services

|

|

Attachmen

|

1⇩

|

February 2022 Enterprise Risk Report

|

|

|

|

February

2022 Enterprise Risk Report

|

Attachment 1

|

HAWKE’S BAY REGIONAL

COUNCIL

Finance

Audit & Risk Sub-committee

02 March

2022

Subject: Risk Maturity Update

Reason for Report

1. This item provides the

Finance, Audit and Risk Sub-committee (FARS) with an update on Council’s Risk Management Maturity.

Background

2. At the Corporate and

Strategic (C&S) Committee meeting on 10 June 2020 Council’s risk

maturity roadmap was endorsed. At that meeting it was agreed that the

FARS would take responsibility for overseeing the implementation of the risk

maturity roadmap. Therefore, this item provides a summary of risk

maturity actions completed since last reported to FARS on 13 October 2021

and risk maturity actions scheduled for the next FARS reporting period.

Discussion

3. The last update to the

Sub-committee was in October 2021. Since October 2021 the following risk

maturity actions have been completed:

3.1. Appointment of a Risk

Champion within each Group – the Risk Champion will coordinate the

development of risk profiles for each Group and influence risk attitudes to

ensure alignment across the business

3.2. Inclusion of Risk Champions

in a ‘light touch’ risk aggregation session to provide bottom-up

challenge to the current enterprise risk profile

3.3. Completion of risk bowties

for each enterprise risk

3.4. A session with the Strategy

and Governance Team to identify risk processes to formalise within strategy and

governance e.g., inclusion of a formal risk sign-off in concept documents

(business cases), decision papers, and project scope variations.

4. For the next FARS reporting

period the risk maturity plan had intended to target formal training of the

Risk Champions and the development of a risk profiles for each Group.

Developing a risk profile for each Group would help to upskill Managers and key

subject matter experts in risk-based thinking and systematically embed risk

methodologies into the business. However, currently the business is

facing significant disruption with responding to immediate high impact risks of

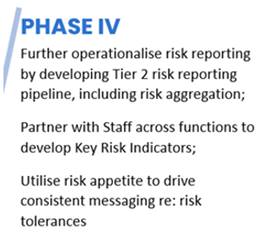

Covid19 and a tight employment market. Therefore, phase IV of the roadmap

(see image below) has been re-evaluated to identify a less resource intensive

approach to embedding risk.

5. It is agreed that the focus

for the next reporting period will be on partnering with staff across functions

to develop Key Risk Indicators (KRI’s) and utilise the draft risk

appetite to drive consistent messaging and risk tolerances for identified

indicators. The Strategy and Performance team have already developed

financial and non-financial performance reporting via the Quarterly

Organisational Performance Report that includes several KRI metrics.

Therefore, the intention is to work collaboratively with the Strategy and

Performance team and KRI metric owners to determine tolerance levels bringing

risk monitoring and corrective actions closer to performance outcomes. In

addition, strengthening the risk bowties and identified critical controls for

each enterprise risk may enable new KRI metrics to be identified that could

further strengthen the non-financial performance part of the report.

6. Therefore, the following

actions are now scheduled to be delivered as part of the risk maturity roadmap

over the next FARS reporting period:

6.1. External validation on the

completeness and accuracy of the enterprise bowties including identifying

opportunities to enhance critical controls.

6.2. Using validated bowties to

identify new KRI metrics to enhance the Organisational Performance Report.

6.3. Working collaboratively

with the Strategy and Performance team to identify key KRI’s in the

current Organisational Performance Report, upskill metric owners in risk based

thinking to improve qualitative reporting (i.e. commentary provided) and establish

risk tolerance levels (triggers) as guided by Council’s risk appetite

statement.

6.4. Continue with informal risk

aggregation sessions (light touch meetings) with Risk Champions.

6.5. Progress the formulation of

Council’s risk appetite statement including reviewing the Risk Management

Framework and Policy with particular attention on the quantitative scale in the

risk matrix.

Strategic Fit

7. Maturity of the

Council’s risk management system contributes towards achieving all

strategic goals/vision by protecting the organisation. A mature risk system

provides consistent risk intelligent decision making enabling the efficient

prioritisation of finite organisational resources to deliver on strategy.

Financial and Resource Implications

8. Maturity of the risk

management system is phased to minimise budgetary implications. Some

facilitated risk training workshops maybe need to be provided to targeted

staff. The 0.1 Risk Champion FTE from each Group will be managed through

current resourcing.

Next Steps

9. Refer to section six of

this report for the next steps for maturity of the Council’s risk

management system.

Decision Making Process

10. Council and its committees

are required to make every decision in accordance with the requirements of the

Local Government Act 2002 (the Act). Staff have assessed the requirements in

relation to this item and have concluded:

10.1. The decision of the

sub-committee is in accordance with the Terms of Reference and decision-making

delegations adopted by Hawke’s Bay Regional Council 25 March 2020,

specifically the Finance, Audit and Risk Sub-committee shall have

responsibility and authority to:

10.1.1. Review whether Council

management has a current and comprehensive risk management framework and

associated procedures for effective identification and management of the

council’s significant risks in place.

10.1.2. Undertake periodic

monitoring of corporate risk assessment, and the internal controls instituted

in response to such risks.

10.1.3. Report on the

robustness of risk management systems, processes and practices to the Corporate

and Strategic Committee to fulfil its responsibilities.

10.2. As this

report is for information only, the decision-making provisions do not apply.

Recommendations

1. That the Finance, Audit and

Risk Sub-committee receives and considers the “Risk Maturity Update” staff report.

2. The Finance, Audit and Risk

Sub-committee reports

to the Corporate and Strategic Committee that:

2.1. Delivery of phase IV of the

roadmap was re-evaluated to identify a less resource intensive approach for

embedding risk-based thinking into the business due to the level of business

disruption from Covid19 and the tight labour market, and

2.2. The revised delivery plan

for phase IV of the roadmap still aligns to Council’s overall risk

maturity strategy of embedding risk-based thinking into the business.

Authored by:

|

Helen Marsden

Risk & Corporate Compliance

Manager

|

Desiree Cull

Strategy & Governance Manager

|

Approved by:

|

Jessica Ellerm

Group Manager Corporate Services

|

|

Attachment/s

There are no attachments for this

report.

HAWKE’S

BAY REGIONAL COUNCIL

Finance

Audit & Risk Sub-committee

02 March

2022

Subject: Internal Audit Annual Plan

Status Update FY2021-2022

Reason for Report

1. This item provides the

Finance Audit and Risk Sub-committee (FARS) with the Internal

Audit Annual Plan FY21-22 status update.

Officers’

Recommendations

2. Council officers recommend

that the FARS members consider and note the Internal Audit Annual Plan FY21-22

status update below.

2.1. The Fraud Management audit

carried out by Crowe commenced in mid-February, interviews with a range of

staff have been held. The full report will be submitted to FARS in May

2022.

|

Approved Audit FY2021-22

|

Provider

|

Quarter Due

|

Date Commenced

|

Management Comments

|

Reported to FARS

|

|

Fraud Management

|

Crowe

|

Q3

|

February 2022

|

|

|

|

Data Analytics

|

Crowe

|

Q4

|

|

Due to commence in May 2022

|

|

|

Retained Audit Capacity – 40 hrs

|

|

|

|

|

|

3. The purpose of the annual

internal audit plan status update dashboard is to provide the FARS with

oversight and progress of individual internal audits that form part of the

Corporate and Strategic Committee (C&S) approved annual internal audit

plan.

Decision Making Process

4. Council and its committees

are required to make every decision in accordance with the requirements of the

Local Government Act 2002 (the Act). Staff have assessed the requirements in

relation to this item and have concluded:

4.1. This agenda item is in

accordance with the Sub-committee’s Terms of Reference, specifically:

4.1.1. The purpose of the Finance,

Audit and Risk Sub-committee is to report to the Corporate and Strategic

Committee to fulfil its responsibilities for (1.3) the independence and

adequacy of internal and external audit functions

4.1.2. The Finance, Audit and Risk

Sub-committee shall have responsibility and authority to (2.6) receive the

internal and external audit report(s) and review actions to be taken by

management on significant issues and recommendations raised within the

report(s)

4.1.3. The Finance, Audit and Risk

Sub-committee is delegated by Council to (3.6) review the objectives and scope

of the internal audit function, and ensure those objectives are aligned with

Council’s overall risk management framework; and (3.7) assess the

performance of the internal audit function, and ensure that the function is

adequately resourced and has appropriate authority and standing within Council.

Recommendations

That the Finance, Audit and Risk

Sub-committee:

1. Receives and considers the

“Internal Audit Annual Plan Status Update FY2021-2022” staff

report.

2. Reports to the Corporate

and Strategic Committee, the Sub-committee’s satisfaction that the Internal

Assurance Programme Update provides adequate evidence of the adequacy of

Council’s internal assurance functions and management actions undertaken

or planned respond to findings and recommendations from completed internal

audits.

Authored by:

|

Olivia Giraud-Burrell

Quality & Assurance Advisor

|

Helen Marsden

Risk & Corporate Compliance

Manager

|

Approved by:

|

Jessica Ellerm

Group Manager Corporate Services

|

|

Attachment/s

There are no attachments for this

report.

HAWKE’S

BAY REGIONAL COUNCIL

Finance

Audit & Risk Sub-committee

02 March

2022

Subject: Annual Internal Assurance

Plan 2022-2023

Reason for Report

1. This item provides the

Finance Audit and Risk Sub-committee (FARS) with a draft proposed Annual

Internal Assurance Plan 2022-2023 for consideration as requested at FARS

October 2021.

Background/Discussion

2. Council officers recommend

that the Sub-committee considers the proposed Plan. An outline of current

trends is provided below by our current internal auditors (Crowe) which is aligned

to the Office of the Auditor- General’s areas of focus. A detailed report

will be provided at the 4 May 2022 FARS meeting and seek the

Sub-committee’s approval of the 2022-2023 Plan.

2.1. Business continuity

planning

2.2. Integrity and Ethics (covered

by the planned Fraud Risk Management and Analytics assignments)

2.3. Infrastructure and asset

management (although limited to an extent by the 3 waters reforms)

2.4. Capital works programme

management

2.5. Information/Cybersecurity

2.6. People and Capability

(completed last year)

2.7. Climate change and

sustainability in service delivery.

Financial and Resource Implications

3. There are no financial

implications or additional resource requirements resulting from this internal

assurance programme update.

Decision Making Process

4. Council and its committees

are required to make every decision in accordance with the requirements of the

Local Government Act 2002 (the Act). Staff have assessed the requirements in

relation to this item and have concluded:

4.1. The agenda item is in

accordance with the Sub-committee’s Terms of Reference, specifically:

4.1.1. The purpose of the Finance,

Audit and Risk Sub-committee is to report to the Corporate and Strategic

Committee to fulfil its responsibilities for (1.3) the independence and

adequacy of internal and external audit functions

4.1.2. The Finance, Audit and Risk

Sub-committee shall have responsibility and authority to (2.6) receive the

internal and external audit report(s) and review actions to be taken by

management on significant issues and recommendations raised within the

report(s)

4.1.3. The Finance, Audit and Risk

Sub-committee is delegated by Council to (3.6) review the objectives and scope

of the internal audit function, and ensure those objectives are aligned with

Council’s overall risk management framework; and (3.7) assess the

performance of the internal audit function, and ensure that the function is

adequately resourced and has appropriate authority and standing within Council.

4.2. As this item is for

information only, the decision making provisions do not apply.

Recommendations

That

the Finance, Audit and Risk Sub-committee receives and considers the draft

“Annual

Internal Assurance Plan 2022-2023” staff report.

Authored by:

|

Olivia Giraud-Burrell

Quality & Assurance Advisor

|

Helen Marsden

Risk & Corporate Compliance

Manager

|

Approved by:

|

Tom Skerman

Regional Water Security Programme

Director

|

Jessica Ellerm

Group Manager Corporate Services

|

Attachment/s

|

1⇩

|

Annual Internal Assurance Plan

(universe)

|

|

|

|

Annual

Internal Assurance Plan (universe)

|

Attachment 1

|

HAWKE’S

BAY REGIONAL COUNCIL

Finance

Audit & Risk Sub-committee

02 March

2022

Subject: 2020-2021 Annual Report Audit

Update

Reason for Report

1. This item provides an

update on the audit of Council’s 2020-2021 Annual Report and timing for

Council adoption.

Background

2. Staff presented the

Hawke’s Bay Regional Council Annual Report for the 2020-2021 financial

year to the Finance, Audit and Risk Sub-committee on 15 December 2021, noting

the final audit report was yet to be received and adjustments might be

required.

3. The sub-committee

recommended that Hawke’s Bay Regional Council adopt the 2020-2021 Annual

Report, pending receipt of Audit New Zealand’s final audit report and

subject to any minor adjustments.

Audit

update

4. Council staff had

anticipated bringing the Annual Report to Council for adoption in January 2022,

however due to delays with Audit NZ completing their audit, expect to now bring

it to Council at its meeting in March.

5. The delay is due to Audit

NZ’s technical team working through the best treatment for the Accident

Compensation Corporation adjustment.

Feedback incorporated since last FARS meeting

6. At the December

sub-committee meeting, a member raised an issue with how leave entitlements and

liabilities were presented. Finance staff responded directly to the member to

explain that it was to do with the difference between how information is

presented by HBRC and the Port (which is consolidated into HBRIC and the HBRC

Group accounts). No change was required. .

7. A number of small

adjustments to the Annual Report and Summary have been made. These were either

as a result of audit feedback or improvement/corrections made by staff.

8. As stated in December,

staff would bring revised financial statements back to the sub-committee for

further review only if they were considered significant in nature.

Implication of Late Adoption

9. Under the Local Government

Act 2020 (the Act), the Annual Report and Summary are statutory requirements

and required to be audited by an independent auditor.

10. Legislation[1] was passed in July

2021 to extend the statutory deadline for adoption of both the 2020-2021 and

2021-2022 Annual Reports (with 30 June balance dates) by two months due to a

severe shortage of auditors. That means that those annual reports must be

adopted no later than 31 December in their respective year.

11. As we will be adopting

after that date, we are required to include a self-disclosure note in our

financial statements. The Regional Council will be included in the audit

statistics reported to central government.

12. A late adoption does not

affect our Level of Service Measure in our Long Term Plan 2021-2031 related to

a clear audited opinion.

13. Interim non-financial and

financial results, prior to being audited, have been in the public arena

multiple times via committee agendas.

Audit

NZ

14. Karen Young, Director of

Audit NZ, will be joining this meeting as per the FARS terms of reference, to

discuss any matters that the auditors wish to bring to the

Sub-committee’s attention. This can be a members-only session if required.

15. Should the sub-committee

wish to discuss matters with the Auditor in private, with the public excluded,

the following resolution must be passed.

15.1. That the Finance, Audit and

Risk Sub-committee excludes the public from this section of the meeting being

Discussion with Director of Audit NZ with the general subject of the item to be

considered while the public is excluded; the reasons for passing the resolution

and the specific grounds under Section 48 (1) of the Local Government Official Information

and Meetings Act 1987 for the passing of this resolution being:

|

General

Subject of the Item to be Considered

|

Reason

for Passing This Resolution

|

Grounds

Under Section 48(1) for the Passing of the Resolution

|

|

2020-2021 HBRC Annual Report Audit

|

7(2)(c)(i) The exclusion of the public from this

discussion is necessary to protect information which is subject to an

obligation of confidence and to ensure the supply of similar information from

the same source is not prejudiced; it is in the public interest that such

information should continue to be supplied

|

The Council is specified, in the First

Schedule to this Act, as a body to which the Act applies.

|

|

2020-2021 HBRC Annual Report Audit

|

7(2)(f)(ii) The exclusion of the public from this

discussion is necessary to maintain the effective conduct of public affairs

through the protection of such members, officers, employees, and persons from

improper pressure or harassment

|

The Council is specified, in the First

Schedule to this Act, as a body to which the Act applies.

|

Decision Making Process

16. The Regional Council and

its committees are required to make every decision in accordance with the

requirements of the Local Government Act 2002 (the Act). Staff have assessed

the requirements in relation to this item and have concluded:

16.1. The decisions are in

accordance with the Finance, Audit and Risk Sub-committee Terms of Reference,

specifically to:

16.1.1. Satisfy itself that the

financial statements and statements of service performance are supported by

adequate management signoff and adequate internal controls and recommend

adoption of the Annual Report by Council

16.1.2. Enquire of internal and

external auditors for any information that affects the quality and clarity of

the Council’s financial statements and statements of service performance,

and assess whether appropriate action has been taken by management in response

to this

16.1.3. Conduct a sub-committee

members-only session with Audit NZ to discuss any matters that the auditors

wish to bring to the Sub-committee’s attention and/or any issues of

independence

16.2. as this report is for

information only, the decision-making provisions do not apply.

Recommendations

1. That the Finance, Audit and

Risk Sub-committee receives and notes the “2020-21 Annual Report Audit Update” staff report.

And if required

2. That the Finance, Audit and

Risk Sub-committee excludes the public from this section

of the meeting being Discussion with Director of Audit NZ with the general

subject of the item to be considered while the public is excluded; the reasons

for passing the resolution and the specific grounds under Section 48 (1) of the

Local Government Official Information and Meetings Act 1987 for the passing of

this resolution being:

|

General

Subject of the Item to be Considered

|

Reason

for Passing This Resolution

|

Grounds

Under Section 48(1) for the Passing of the Resolution

|

|

2020-2021 HBRC Annual Report Audit

|

7(2)(c)(i) The exclusion of the public from this

discussion is necessary to protect information which is subject to an

obligation of confidence and to ensure the supply of similar information from

the same source is not prejudiced; it is in the public interest that such information

should continue to be supplied

|

The Council is specified, in the First

Schedule to this Act, as a body to which the Act applies.

|

|

2020-2021 HBRC Annual Report Audit

|

7(2)(f)(ii) The exclusion of the public from this

discussion is necessary to maintain the effective conduct of public affairs

through the protection of such members, officers, employees, and persons from

improper pressure or harassment

|

The Council is specified, in the First

Schedule to this Act, as a body to which the Act applies.

|

Authored by:

|

Tim Chaplin

Senior Group Accountant

|

Mandy Sharpe

Project Manager

|

|

Desiree Cull

Strategy & Governance Manager

|

Christopher Comber

Chief Financial Officer

|

Approved by:

|

Jessica Ellerm

Group Manager Corporate Services

|

|

Attachment/s

There are no attachments for this

report.

HAWKE’S

BAY REGIONAL COUNCIL

Finance

Audit & Risk Sub-committee

2 March

2022

Subject: Quarterly Treasury Report for

1 October – 31 December 2021

Reason for Report

1. This item provides

compliance monitoring of Hawke’s Bay Regional Council (HBRC) treasury

activity and reports the performance of Council’s investment portfolio

for the quarter ended 31 December 2021.

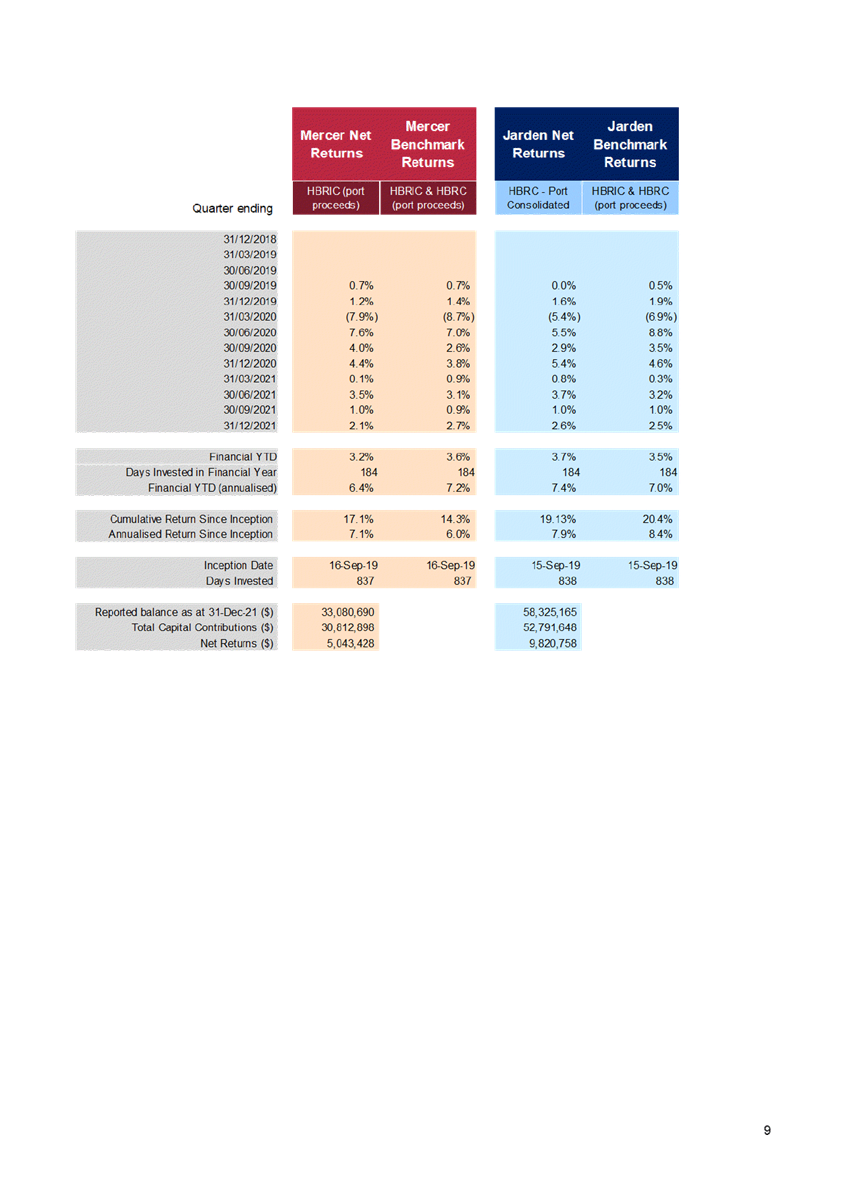

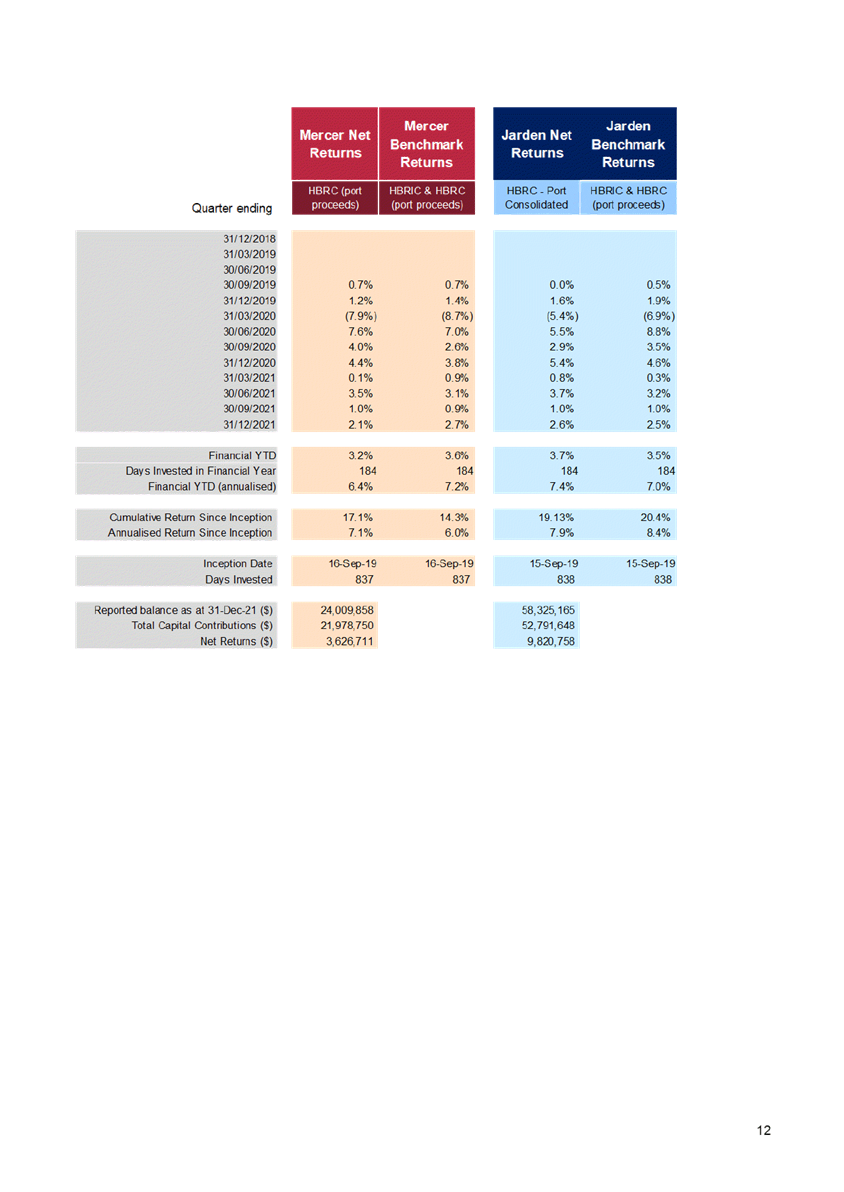

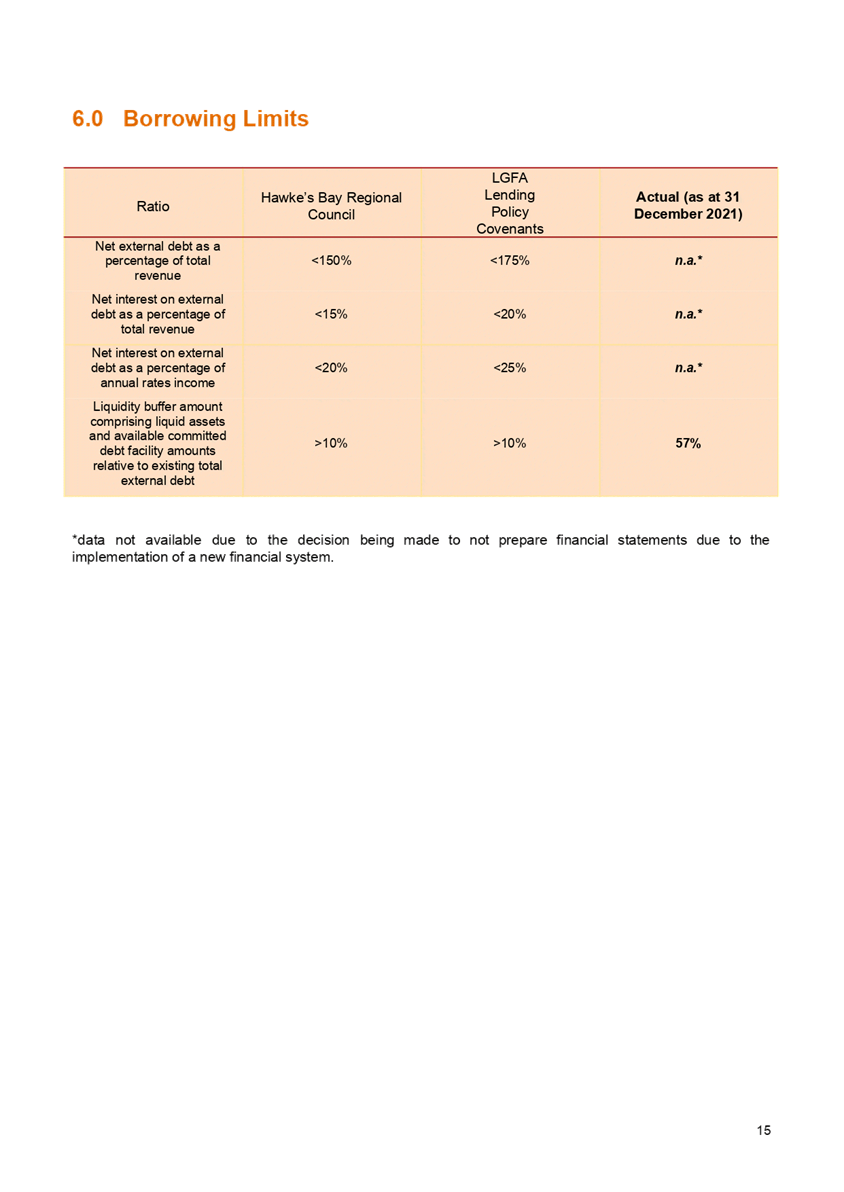

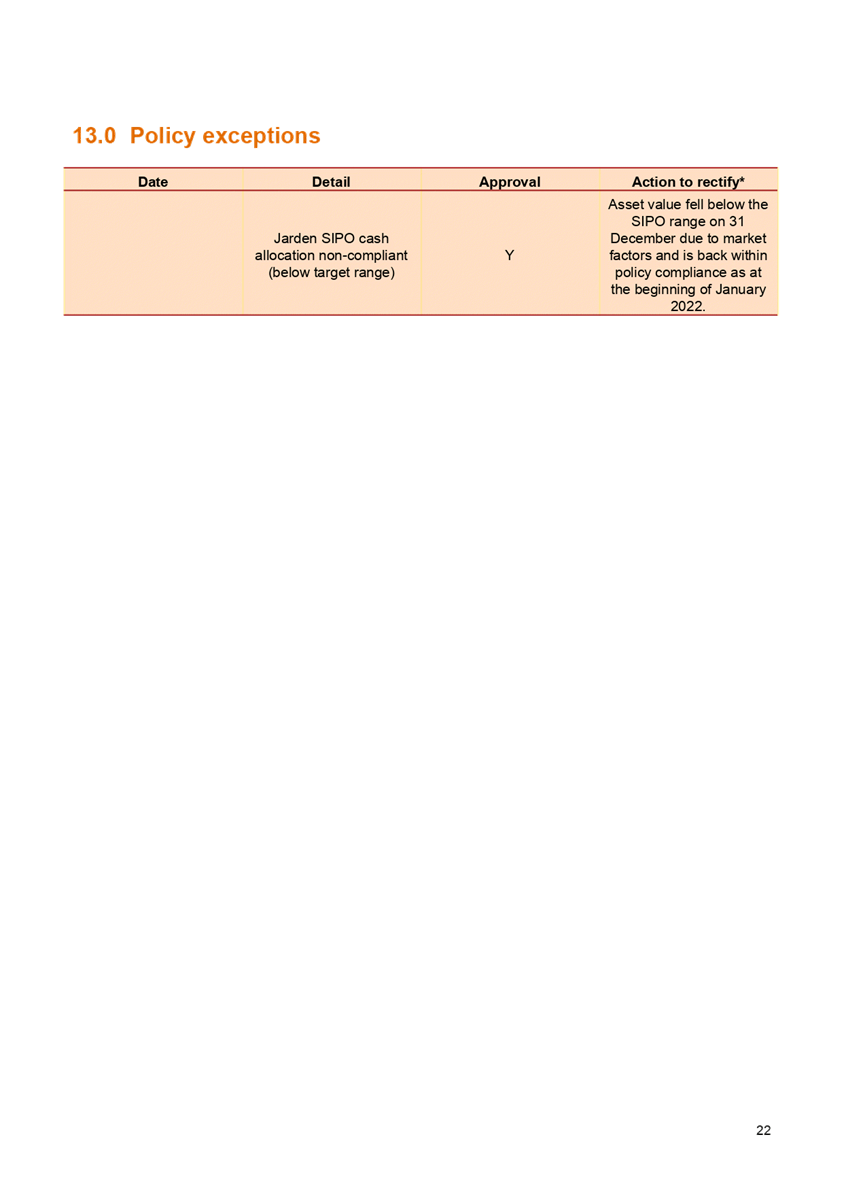

Overview of the Quarter – ending 31 December 2021

2. At the end of the quarter

to 31 December 2021, HBRC was compliant with all measures in its Treasury

policy except for the Mercer SIPO investment allocation, which has since been

corrected.

3. Investment returns for the

first 6 months met budget expectations, however, due to market volatility and a

significant financial market adjustment in January 2022, it is too early to

predict the returns for the full financial year. The fluctuation in January

erased most of the gains of the first 6 months so a recovery in the markets is

required to deliver target returns for the year.

4. Financial markets,

particularly international markets, continue to move around considerably and a

bounce back to forecast returns within the financial year is not out of the

question. Staff advice is to watch and wait at this point in time, corrective

action is not required, and the portfolio is well balanced for the long term.

5. Cash balances are good and

borrowing requirements low for the first 6 months. As Council progresses

further into the financial year additional borrowing will be required.

Financial Impact of Covid-19 / Omicron on Current and Future

Financial Year

6. The sub-committee requested

that a financial assessment, including commentary regarding any corrective

actions required, of the financial impact of the current Omicron outbreak on

FY21-22 be incorporated within this Treasury report. However, given the 6-month

financials to 31 December 2021 will be presented to the Corporate and

Strategic Committee alongside the organisation performance reporting on 16

March 2022, the financial impact commentary is best placed to accompany that

reporting.

7. Financial impacts of

Covid/Omicron are both direct and indirect and include adjustments or impacts

to budget assumptions for inflation, interest costs. Additional expenses may be

incurred in relation to business continuity/resilience planning, (working from

home equipment/cleaning/masks etc), direct staff costs where there is a

requirement to add resourcing for critical stand-alone roles. There may,

however, be costs savings or deferral of spend where capital work programmes

are not being delivered within planned timeframes because of the

disruption/distraction. The most significant financial impact will likely be to

investment income, where impact to financial markets can be immediate and high

impact.

8. All of the above will be

incorporated into the financial reporting for the 16 March 2022 Corporate and

Strategic Committee meeting.

Background

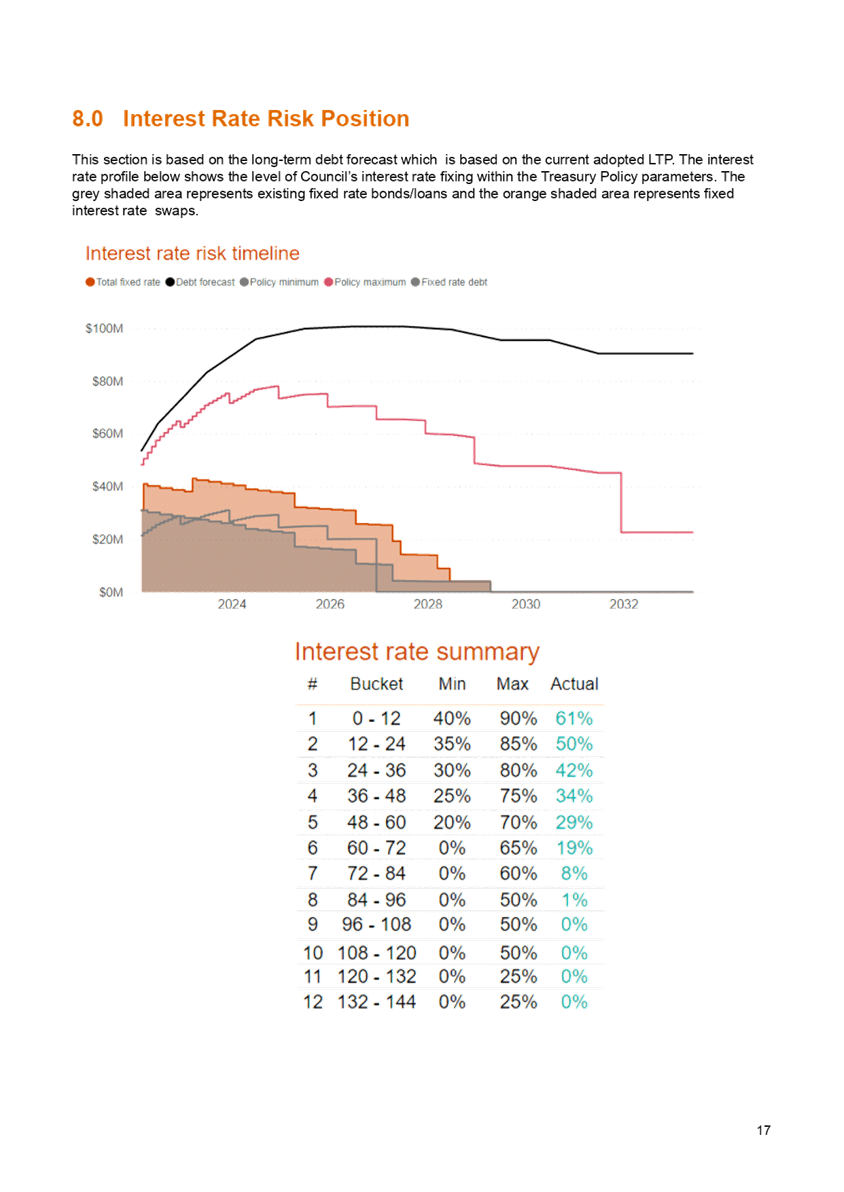

9. Council’s Treasury

Policy requires a quarterly Treasury Report to be presented to the Finance

Audit and Risk Sub-committee. The policy states that the Treasury Report is to

include:

9.1. Treasury Exceptions report

9.2. Policy compliance

9.3. Borrowing Limit report

9.4. Funding and liquidity

report

9.5. Debt maturity profile

Interest rate report

9.6. Investment management

report**

9.7. Treasury investments

9.8. Cost of funds report Cash

flow and debt forecast report

9.9. Debt and interest rate

strategy and commentary

9.10. Counterparty credit report

9.11. Loan advances.

10. The Investment Management

report** has specific requirements outlined in the Treasury Policy. This

requires quarterly reporting on all treasury investments plus annual reporting

on all equities and property investments.

11. In addition to the Treasury

Policy, Council has a Statement of Investment Policy and Objectives (SIPO)

document setting out the parameters required for funds under management for the

HBRC Long Term Investment Fund.

12. Treasury Investments to be

reported on consist of:

12.1. Liquidity

12.1.1. Cash and Cash Equivalents

12.1.2. Debt Management

12.2. Externally Managed

Investment Funds

12.2.1. Long-Term Investment Fund

(LTIF)

12.2.2. Future Investment Fund

(FIF)

12.3. Investment properties

12.4. HBRIC Ltd

12.5. 2021-22 Performance

Summary.

13. Since 2018, HBRC has

procured treasury advice and services from PriceWaterhouseCoopers (PwC) and

their quarterly compliance report is attached.

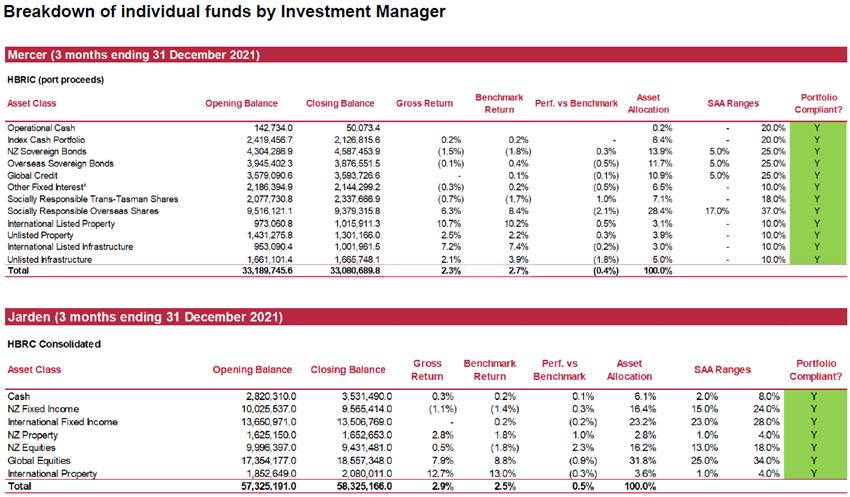

Discussion

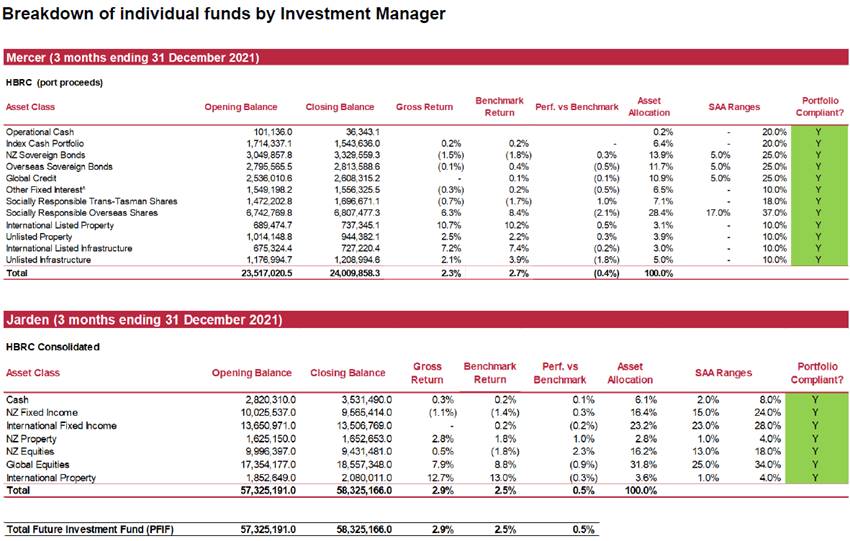

14. A separate treasury report

is prepared by Council’s advisors, PwC to report on compliance with the

policy parameters and investment performance. The PwC report is attached. This

report gives a high-level summary of the data in the PwC report.

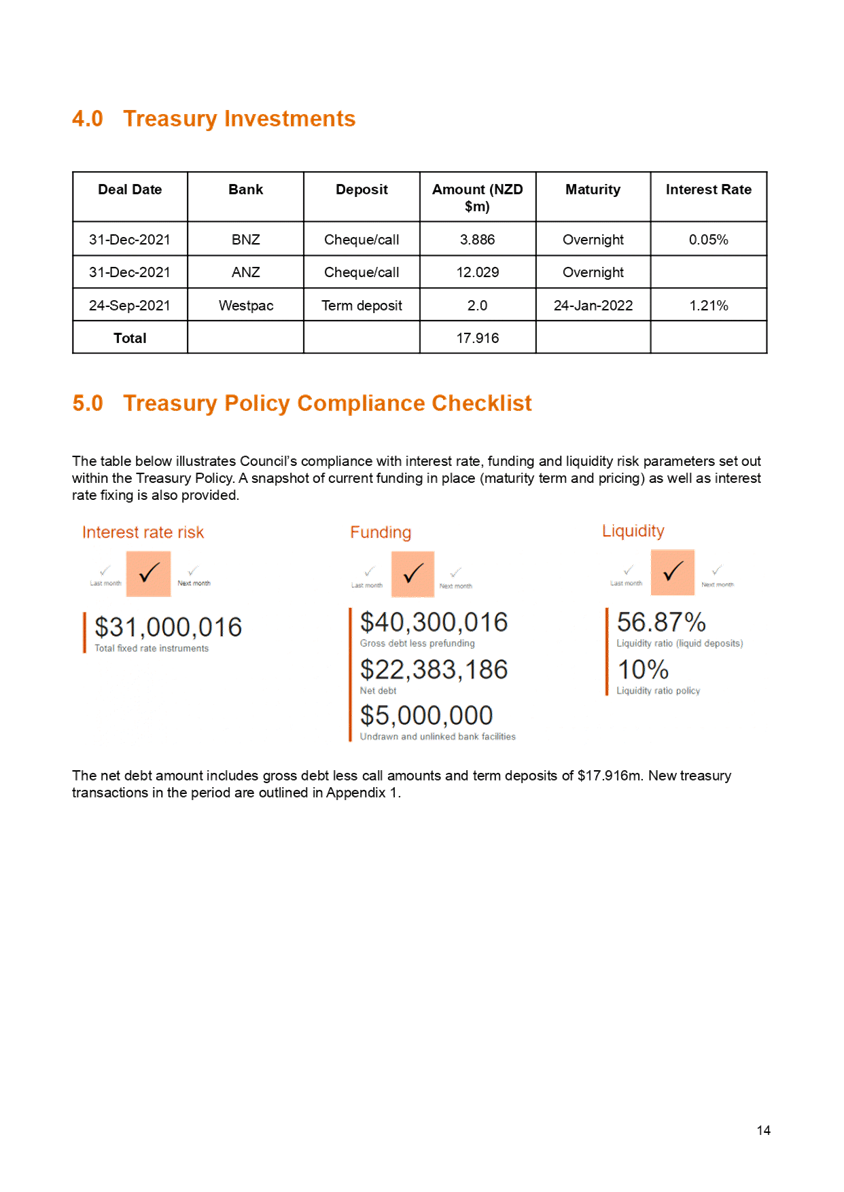

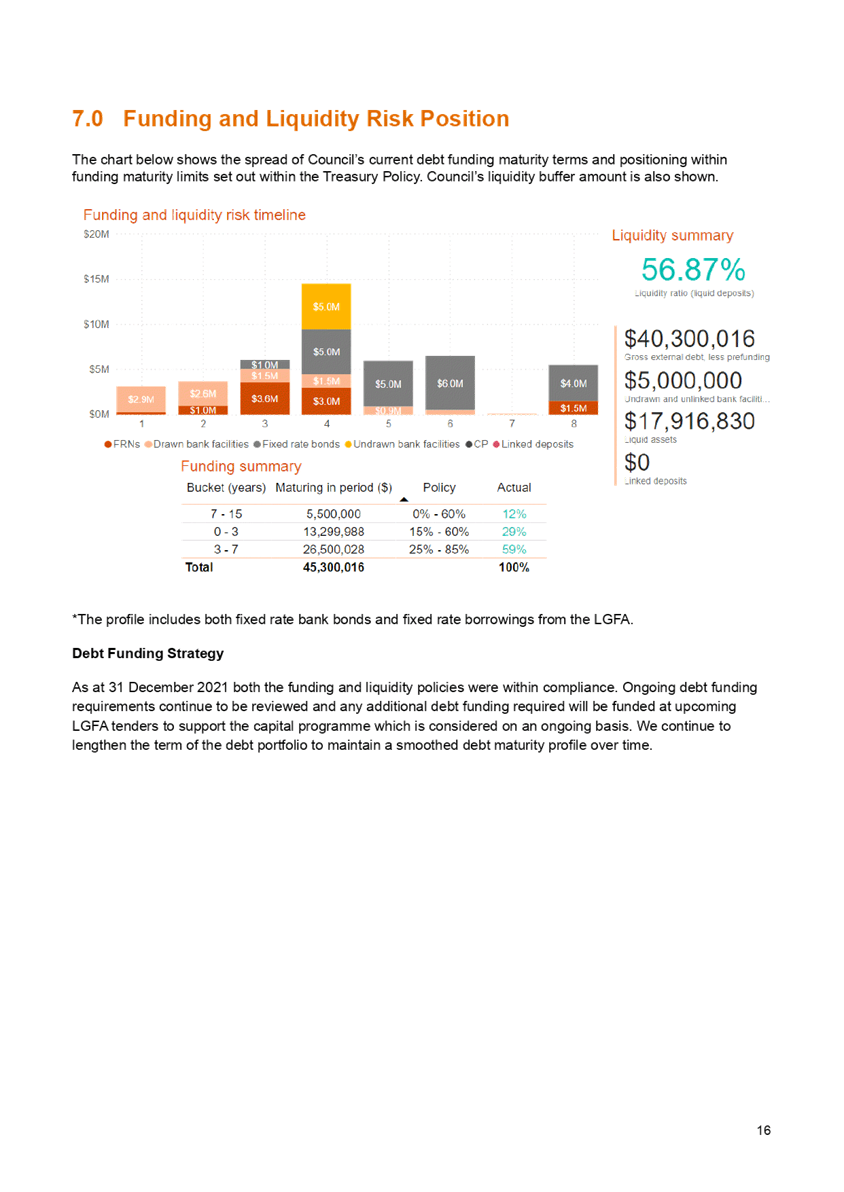

Liquidity

15. To ensure HBRC has the

ability to adequately fund its operations, current policy requires HBRC to

maintain a liquid balance of $3.0m.

16. The following table reports

the cash and cash equivalents on 31 December 2021.

|

31 December 2021

|

$000

|

|

Cash on Call

|

15,915

|

|

Short-term bank deposits

|

2,000

|

|

Total Cash & and Deposits

|

17,916

|

17. Council’s balance of

cash and deposits compares favourably with the December 2020 balance of $13.5m.

18. To manage HBRC liquidity

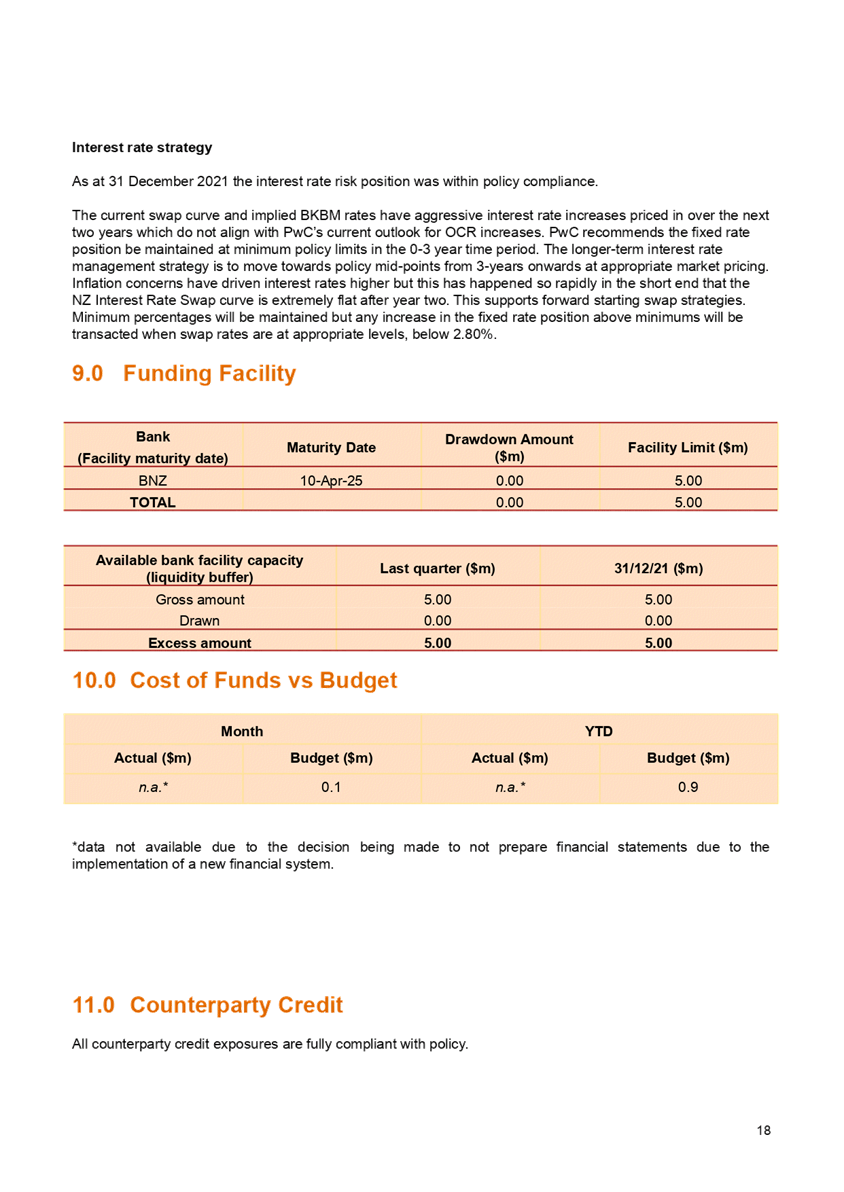

risk, HBRC also retains a Standby Facility with BNZ.

This facility provides HBRC with a same day draw down option, to any amount

between $0.3-$5.0m, and with a 7-day minimum draw period.

Debt

Management

19. On 31 December 2021 the

current external debt for the Council group was $40.3m ($56.96m including the

loan from HBRIC).

20. Following the $11m raised

in the September quarter no further funds were borrowed in the December

quarter. This was as anticipated given Council’s cash position is at its

best in the December quarter (due to rates being due in September).

21. Further borrowing will be

required in the second half of the financial year (first half of calendar year

2022) as the requirements of the proposed 2021-2022 borrowing programme of

$27.5m ramps up.

22. The following summarises

the Year-to-date movements in Council’s debt position.

Summary of HBRC Debt

|

|

HBRC only

|

HBRC Group

|

|

Opening Debt – 1 July 2021 – excl HBRIC

Loan

|

30,875,014

|

30,875,014

|

|

New Loans raised

|

11,000,000

|

11,000,000

|

|

Less amounts repaid

|

(1,574,998)

|

(1,574,998)

|

|

Closing Debt 31 December 2021 (excluding

HBRIC loan)

|

40,300,016

|

40,300,016

|

|

Plus opening balance - loan from HBRIC

|

16,663,036

|

-

|

|

Total Borrowing as at 31 December

|

56,963,052

|

40,300,016

|

Managed

Funds

23. The LTP budgets an annual

return of 5.16% from managed funds. Of this 3.16% is used to fund activities

with 2.0% retained to grow the capital base to enable the future earnings to

protect the capital base for future generations.

24. Council budgets separately

for revenue from directly held managed funds and those held by HBRIC. HBRIC is

required to deliver an overall portfolio return by way of an agreed annual

dividend agreed through an annual Statement of Intent. The composition (between

revenues from managed funds and other sources such as port dividends is up to

the HBRIC board). Council has budgeted to receive $10.1 in dividends from HBRIC

within the FY21-22.

25. The FY21-22 budget

expectation for managed funds to be withdrawn to support Council operations is

$3.7m. Based on the December funds result and the value above the protected

amount the funds held sufficient returns to meet Council’s requirements.

Unfortunately, since 31 December the markets dropped eroding in excess of

$2m of these gains. A recovery of the market is now required to deliver on

budget expectations.

26. The Fund performances for

the first 6 months have been lower than we have experienced recently. Financial

markets have not performed as strongly as prior year with the YTP results for

the two providers being 0.9% and 1% so far. This follows on from annualized

returns of 12.5% and 14.5% for the 2020-21 financial year.

27. Given the nature of the

investments some volatility is to be expected. It is too early to predict

likely returns for the full year, however, if the remaining quarters deliver

similar results the annualised return would be approximately 4% which is below

the LTP budget of 5.16% p.a.

28. However, the performance of

the managed funds since placement demonstrate market recovery can occur within

relatively short timeframes, and a watch and wait approach is prudent. The

portfolio construct is intentionally conservatively balanced for the long-term.

29. The presentation of table

below has been changed from previous reports to show the combined view of funds

and the value available above the capital protected sum. As at June 2021

Council had an additional $3.36m available due to the stronger investment

returns in FY20-21. Some of this could be used to supplement any shortfall if

the current lower returns continue to the end of the financial year.

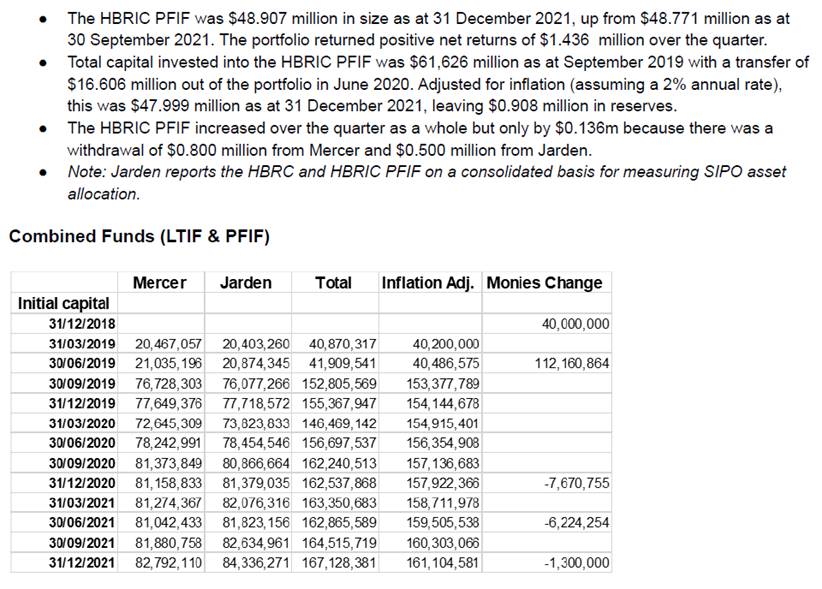

30. The following table summarises the fund balances at the

end of each quarter.

31. The view for the June,

September and December 2021 quarters has been expanded to show the total group

balance of managed funds (including HBRIC) and the amount by which the current

funds balance exceeds the capital protected amount.

|

|

31 Dec 2020

|

31 Mar 2021

|

30 Jun 2021

|

30 Sep 2021

|

31 Dec 2021

|

|

|

$000

|

$000

|

$000

|

$000

|

$000

|

|

Total funds before withdrawals

|

121,404

|

114,625

|

118,563

|

115,745

|

118,221

|

|

Funds withdrawn

|

(6,500)

|

|

(4,200)

|

|

|

|

Fund Balance HBRC

|

114,904

|

114,625

|

114,363

|

115,745

|

118,221

|

|

Capital Protected Amount HBRC (2% compounded)

|

|

|

111,983

|

112,543

|

113,105

|

|

Current HBRC value above protected amount

|

|

|

2,380

|

3,202

|

5,116

|

|

|

|

Funds Balances (Group – HBRC + HBRIC)

|

|

Long-Term Investment Fund

|

49,925 *

|

50,206

|

49,883**

|

50,484

|

51,712

|

|

Future Investment Fund

|

64,300 *

|

64,418

|

64,370**

|

65,261

|

66,508

|

|

Total HBRC

|

114,904

|

114,625

|

114,363**

|

115,745

|

118,220

|

|

Plus HBRIC

|

|

|

48,503

|

48,771

|

48,907***

|

|

Total Group Managed Funds

|

|

|

162,866

|

164,516

|

167,127

|

|

Capital Protected Amount (2% compound inflation)

|

|

|

159,506

|

160,303

|

161,104

|

|

Current group value above protected amount

|

|

|

3,360

|

4,213

|

6,023

|

31.1. * December 2020 saw $6.5m

(LTIF $4.5m & FIF $2.0m) Funds being divested for the first time, which

explains the reduced fund balance

31.2. ** Additional funds totalling

$4.2m (LTIF $2.0m & FIF $2.2m) were withdrawn from the funds during the June

2021 quarter

31.3. *** HBRIC withdrew $1.3m

during the December quarter. The Capital Protected amount of HBRIC on

31December is $47.999m. ($0.907m available).

Investment

Property – Napier Leasehold Portfolio

32. Napier Leasehold properties

represent the balance of ex Harbour Board residential leasehold properties. The

HBRC returns from this portfolio are limited as following the sale of future

revenues in 2013 to ACC, HBRC retains one third of any excess rentals and one

third of any surplus when a property is freeholded.

33. For the first 6 months

$546,466 in rent was collected and Council’s share of excess rents for

the period was $54,000.

34. In the first 6 months, six

Napier Endowment Leasehold Properties were freeholded totalling $0.6m. $0.43m

of this has been subsequently paid to ACC as settlement for the remaining

42 years rent for these properties. The HBRC share of $213,641 for the

first 6 months has been paid into the sale of land reserve.

35. During the first 6 months

one property (3 units) has had its 21year rent review applied and a further 5

properties (13 units) have been notified of their proposed new rental. Only one

(5 units) has the new rental commencing prior to 30 June. With the 21-year

renewal cycle, and the movement in the market values in recent years, lessees

are seeing substantial increases in the annual rental. Those rentals currently

under review are increasing by between 5.6 and 7.3 times what the existing rent

is.

36. The size of the rent increases

proposed is generating an increased number of enquiries about Council’s

rent deferral scheme.

Investment

Property – Wellington Leasehold Portfolio

37. The Wellington leasehold

portfolio comprises 12 properties in central Wellington. The lessees are a mix

of Commercial and residential entities.

38. Most of the properties (11)

have the rental reviewed every 14 years and one has a 7-year review period. No

rent reviews were conducted over the first 6 months and one property is due for

a review in June 2022.

39. The portfolio value has

grown considerably for the initial cost of $6.5m in 2002 to $20.8m at

30 June 2021. Valuation advise is that we can expect another significant

increase in the portfolio value when it is revalued as at 30 June 2022.

40. Council budgets to utilise

the annual rentals of $841k to offset rates each year.

HBRIC

Ltd

41. In accordance with Council

Policy, HBRIC provides separate quarterly updates to the Corporate and

Strategic Committee.

Decision Making Process

42. Council and its committees

are required to make every decision in accordance with the requirements of the

Local Government Act 2002 (the Act). Staff have assessed the requirements in

relation to this item and have concluded:

42.1. This agenda item is in

accordance with the Finance, Audit and Risk Sub-committee Terms of Reference,

specifically “The Finance, Audit and Risk

Sub-committee shall have responsibility and authority to (2.4) monitor the performance of Council’s investment

portfolio”.

42.2. As this report is for

information only, the decision making provisions do not apply.

Recommendations

That the Finance, Audit and Risk

Sub-committee:

1. Receives and notes the

“Quarterly Treasury Report for 1 October – 31 December 2021”.

2. Confirms that the

performance of Council’s investment portfolio has been reported to the

Sub-committee’s satisfaction.

Authored by:

|

Ross Franklin

Finance Consultant

|

Christopher Comber

Chief Financial Officer

|

Approved by:

|

Jessica Ellerm

Group Manager Corporate Services

|

|

Attachment/s

|

1⇩

|

PwC Treasury report for period ended

31 December 2021

|

|

|

|

PwC

Treasury report for period ended 31 December 2021

|

Attachment 1

|

HAWKE’S BAY REGIONAL

COUNCIL

Finance

Audit & Risk Sub-committee

02 March

2022

Subject: HBRC Forestry Update

Reason for Report

1. This paper provides a

summary of Hawke’s Bay Regional Council’s (HBRC) forestry assets as

requested by Finance, Audit and Risk Sub-committee (FARS) on 15 December

2021.

2. The last comprehensive

update on HBRC’s forest assets was presented to Corporate and Strategic

Committee, 23 September 2015 after request by the Committee for a paper “…establishing

values other than commercial that demonstrate the justification for Council

maintaining this investment and projecting the ongoing forest management

programme beyond 10 years to cover the rotation period of the range of

species.”

Executive Summary

3. Local authorities own or

manage 53,282 hectares (ha) of forest land in New Zealand (Attached).

4. HBRC manages the 550ha

Crown-owned Tangoio Soil Conservation Reserve as required by section 16 of the

Soil Conservation and Rivers Control Act (1941). 58% (320ha) of the Reserve is

currently in commercial forestry and the remainder in native forest at varying

stages of regeneration. Commercial forest in the Reserve has a 30 June 2021

valuation of $6,214,000 (Attached).

5. In addition, there are

529ha of commercial forestry across five HBRC-owned properties of a combined

area of 1029ha. These properties have a range of objectives as will be

described in this item and which include wastewater irrigation, carbon

sequestration, recreation, and trialling and demonstrating alternative timber

species. Commercial forest in the HBRC properties has a 30 June 2021 valuation

of $7,754,800.

6. Around 24ha of commercial

forest has been established on river land controlled by HBRC. This is currently

unvalued.

7. HBRC is a minor partner in

190ha of erosion-control forests across the region. These are expected to

return in the realm of $500,000 to HBRC over the coming 10 years.

8. HBRC has a

significant carbon portfolio of 146,400 post 89 NZU and 14,907 pre 1990 NZU,

currently worth $13 million at the current price of $82.

9. Detailed

management plans are in place for the Tangoio Soil Conservation Reserve and the

HBRC Forest Estate and have been approved by two trained foresters, one a

member of the New Zealand Institute of Forestry. The Maungaharuru Tangitū

Trust has approved the management plan for the Tangoio Soil Conservation

Reserve as is required by the Mana Enhancing Agreement signed with HBRC in

2016. Objectives and policies from the plans have been provided in this item

and full plans will be provided to Councillors on request.

Strategic Fit

Water quality safety and

certainty

10. All of the forests provide

erosion control and sediment reduction benefits to some extent, but in the

Waipukurau and Waipawa Forests this is negligible as the land is very stable

anyway. In the erosion-prone soils of Tūtira,

Waihapua and Tangoio, the benefits are significant. Having replaced the network of aging

septic tanks with a more sustainable option, the Mahia Forest plays an

important role in improving water quality and safety in that area.

Smart sustainable landuse

11. The HBRC Forests are all

multi-use properties. As well as the financial returns they generate via carbon

sequestration and log sales, they play important roles in the communities in

which they are situated.

Healthy and functioning biodiversity

12. The Tangoio Soil

Conservation Reserve and Mahia Forest contain areas classified by HBRC’s

ecologists as ecosystem prioritisation sites. Significant areas of native are

being planted and regenerated in the Tūtira and Waipukurau Forests, and

the Tangoio Soil Conservation Reserve over the coming years.

Sustainable

services and infrastructure.

13. The Mahia

Forest provides an important wastewater treatment function to the Mahia

Community, and the Waipukurau Forest (also known as Gum Trees Mountain Bike

Park) is a popular recreational venue and attraction to the town. Management of

the Tangoio Soil Conservation Reserve is very important in ensuring the ongoing

integrity of the section of State Highway 2 that runs through it. Due to access

limitations, the Waihapua Forest Park has not yet been developed, but there is

strong support for this in the surrounding Tūtira Community as represented by the now

disbanded ‘Tūtira Visionary Group’.

Background

Tangoio Soil Conservation Reserve

14. The Tangoio Soil

Conservation Reserve comprises 550ha adjacent to State Highway 2 between

Tangoio and Tūtira, acquired by the Crown in 1946 for the protection of

the Highway, following ongoing closures due to slips, most notably the

‘Anzac Storm’ of 1938 which caused the Highway to be closed for a

period of months.

15. The Reserve was managed in

turn by a series of Government departments, before this responsibility passed

to the Hawke’s Bay Catchment Board and then its successor HBRC in 1989 as

required by Section 16 of the Act:

15.1. “Every

soil conservation reserve shall be under the control and management of the Board within

whose district it is situated, and the Board

shall manage and control the reserve in such manner as in its opinion will best

conserve the soil of the reserve and prevent injury to other land.”

16. Currently, 58% of the

Reserve’s area (320ha) is in commercial forestry and the remainder in

varying stages of reversion to native forest. Returns from the commercial

forestry are held in a Reserve Fund, which is used to entirely fund the

management of the Reserve - no ratepayer funds are used in the management of

the Reserve.

17. Budgets are reviewed every

3 years and cashflows modelled over 40 years to ensure the ongoing

sustainability of the Reserve Fund. As required by Sections 21-23 of the

Maungaharuru Tangitū Hapū Claims Settlement Act (2014), surplus funds

not required for Reserve management are transferred to a ‘Catchments

Fund’ where they available for carrying out soil conservation projects in

the surrounding catchments in partnership with the Maungaharuru Tangitū

Trust (MTT).

18. To date, $320,000 of

Reserve Funds have helped leverage some $6 million in funding for the MTT-led

projects Tūtira

Mai Ngā Iwi, Te

Waiū o Tūtira, and Kia eke Te Ngārue, Kia eke Arapawanui.

19. A Mana Enhancing Agreement

signed with MTT in 2016 requires HBRC to maximise training and employment

opportunities for MTT in the Reserve, and for HBRC and MTT to agree the

Reserve’s three-yearly management plans.

20. As the forests on the

Reserve were established prior to 1990, they are not eligible for entry in the

Emissions Trading Scheme and earning NZU.

Forests

owned by HBRC

River Berms

21. Around 24ha of forest is

planted on river berms around the region. Generally, soils are very stony and

conditions for tree growth are poor in these sites. River berms are also

invariably weed hot spots and control of these in newly established plantings

can be challenging.

22. Despite these challenges,

forests are a good use for the many unused hectares of river berm land

controlled by HBRC. As well as the revenue from carbon and logs, tree canopies

assist in shading out the various weeds over time and negate the need for

grazing and the associated risks of nutrient loss in the free-draining gravel

soils. The flat terrain ensures low logging costs with no tracking and

subsequently low risk of sediment loss.

23. 6ha of the river berm

forests are radiata pine established in the mid to late 1990’s. The other

18ha is a 2021 planting of radiata pine (14ha) and eucalyptus bosistoana (4ha)

on the left bank of the Waipawa River off Walker Road.

24. While the Walker Road

planting is too newly established for registration in the emissions trading

scheme, HBRC’s extensive willow plantings received a one-off allocation

of 14,907 pre-1990 NZU in 2008.

Joint

Venture Forests

25. Between 1994 and 2000, HBRC

entered into 10 joint ventures with landowners across the region to establish

radiata pine plantations on some 190 hectares of erosion-prone land. The joint

venture contracts expire on harvest of the trees or expiry of the 35-year term.

|

Owner

|

YOE

|

Logging Date (at 30yrs)

|

Ha

|

Estimated Ha Harvestable

|

HBRC share

|

Estimated HBRC revenue

|

|

Netherton Station

|

1995

|

2025

|

29

|

14

|

14%

|

$35,000

|

|

McRae Trust

|

1995

|

2025

|

9.5

|

9.5

|

13%

|

$30,875

|

|

Roy Stoddart

|

1995

|

2025

|

40

|

4

|

15%

|

$

-

|

|

Parsons Estate

|

1996

|

2026

|

22.6

|

22.6

|

22.6%

|

$127,690

|

|

Beamish

|

1996

|

-

|

5.4

|

0

|

18%

|

$

-

|

|

Waipari Station (Kairākau)

|

1997

|

2027

|

20

|

20

|

16.6%

|

$83,000

|

|

Lloyd and Virginia Cave

|

1997

|

2027

|

30

|

30

|

13%

|

$97,500

|

|

Bruce Goldstone

|

2000

|

2030

|

4.5

|

4.5

|

13%

|

$14,625

|

|

Waipari Station (Glengarry)

|

2000

|

2030

|

20

|

20

|

14%

|

$70,000

|

|

Haupouri Station

|

2000

|

_

|

8.4

|

0

|

18%

|

$

-

|

|

Totals

|

189.4

|

124.6

|

|

$535,385

|

Table

1: HBRC Joint Venture Erosion Control Forests

26. Though erosion control was

HBRC’s primary objective, the agreements anticipated the forests would

eventually be harvested and generate a financial return. The objective of the

joint venture contracts is stated in Clause 1.1 of each:

26.1. “The goal of the

parties hereto is the establishment and management of the Erosion Control

Plantation, which is to be planted with rapidly growing exotic timber species,

for a rotation period to ensure that the land within the Erosion Control

Plantation is managed and harvested in a manner which will minimise the erosion

impacts”.

27. More recently, staff have

agreed with landowners that approximately 64ha of the joint ventures will not

be harvested as the environmental impacts would be too great. Staff are looking

into ways to use some of the revenue from harvesting the better joint venture

forests to help revert the unharvested forests to native over time.

28. Management objectives for

the joint venture forests are listed in the HBRC Forest Estate

2021-2031 Management Plan as:

28.1. To ensure where harvest is

environmentally and economically feasible, it is carried out with minimal soil

conservation or environmental impacts

28.2. To assist landowners in

transitioning harvested sites to a sustainable post-harvest landuse

28.3. To assist landowners to

transition to permanent native forest where harvest is not environmentally or

economically feasible

28.4. To maximise financial

returns from the forests without compromising the above objectives.

Tūtira

Regional Park

29. 78ha of pine forest was

established on the Tūtira Regional Park between 1991-1993, prior to HBRC

purchasing the property, and a further 36ha immediately after. All were

established primarily for soil conservation following the devastation wreaked

by Cyclone Bola (Attached), with eventual financial returns from harvest being

an important secondary objective.

30. The forest is currently in

the process of being harvested and afterwards approximately 50% will be

converted to native forest for permanent retirement. Council papers relating to

the harvest procurement process were presented to EICC on 19 June 2019 and

regarding the replanting on 3 February 2021.

31. The Tūtira mānuka

plantation is not considered in this item and is described fully as a separate

item in this agenda.

32. Management objectives for

the Tūtira Forest are listed in the 2021-2031

HBRC Forest Estate Management Plan as:

32.1. To manage the forest and

plantation in a way that best supports the soil conservation, biodiversity,

recreational, cultural and aesthetic values of the Regional Park

32.2. To maximise soil

conservation and minimise sediment loss to waterways and Lakes Tūtira and

Waikōpiro

32.3. To facilitate reversion to

native forest over time

32.4. To enhance biodiversity

values on the property and create connections to other habitat in the District.

32.5. To maximise financial

returns from the Forest while not compromising any of the above.

Waihapua Forest Park

33. The Waihapua property had

been of interest to HBRC for many years before the opportunity to purchase it

arose in 2009. The reasons were summarised by a sub-committee of Council

charged with forming a strategy statement for the property in the same year:

33.1. “It’s

significant open space and strategic value given its location adjacent to key

amenity areas and Tangoio Soil Conservation Reserve; its potential to

demonstrate land use options relating to soil conservation and waterways; its

severely eroded nature (Attached); and its commercial advantages associated

with timber and carbon trading.”

34. Following purchase, Council

developed the following Goal for the property:

34.1. “A profitable

working example of integrated and multi-functional land use centred on sequestration

and soil conservation forestry consistent with wider social, amenity,

environmental and economic values and opportunities within the Tutira

area.”

35. Council also identified key

functions for the property as:

35.1. ‘social engagement,

amenity values, recreation, the improvement of water quality, soil

conservation, biodiversity and indigenous ecological values, research, and

demonstration.”

36. Council was advised at the

time an internal rate of return of 6-7% was likely.

37. The name ‘Waihapua

Forest Park’ was formally adopted by Council on 27 April 2011 after

advice from Maungaharuru Tangitū Trust, endorsed by the Tūtira

Visionary Group- a group formed around that time to encourage the development

of tourism and other opportunities for the Tūtira District. The name is

derived from a deep spring with special qualities found on the property.

38. Planting was planned in

conjunction with the Hawke’s Bay Branch of the New Zealand Farm Forestry

Association and carried out between 2009 and 2013. More than twenty-five timber

species on a range of management regimes were established (Attached). There are

two dedicated trial sites on the property, one of eucalyptus fastigata, and the

other of mixed ground durable eucalyptus species. The site-specific planting

resulted in many small compartments, useful for trial and demonstration

purposes, but significantly increasing the difficulty of logging economically

using conventional methods.

39. Approximately 30ha of the

property was deemed to be too steep and erosion-prone to establish in

production forestry or was already in the early stages of reversion to native

forest and not planted with production species on that basis.

40. As well as being envisaged

as a future recreational and educational venue in its own right, Waihapua was

seen as a key addition to a potential walkway over the corridor of public lands

stretching almost uninterrupted for some 16km from the bottom of the Tangoio

Soil Conservation Reserve In the south to the top of the Tūtira Regional

Park in the north (figure 1 below).

Figure 1: Concept Plan,

Tūtira Trails

41. Due to a lack of safe

access to the property, it has not yet been developed and opened to the public.

The main access is through private property, but the easement only provides for

HBRC and its contractors. Other options are possible, but difficult to form

tracks in given the steep and eroding nature of the land. Access from State

Highway 2 is hazardous and would require investment before opening to the

public.

42. Management objectives are

listed in the HBRC Forest Estate 2021-2031 Management Plan as:

42.1. To maintain soil

conservation on the property and minimise sediment loss to the Waikoau River

and erosion impacts on State Highway 2

42.2. To establish and maintain

secure access to the property for recreational use

42.3. To establish and maintain

links from the property to Guthrie-Smith Arboretum and Education Trust and

Tūtira Regional Park

42.4. To enhance biodiversity

values on the property, creating connections to other habitat in the District

42.5. To demonstrate alternative

commercial forest species and support the development of their genetics and

markets

42.6. To maximise financial

returns from the Forest while not compromising any of the above.

Mahia

Forest

43. The Mahia Forest property

was purchased in 2009 primarily as a receiving environment for Mahia

township’s treated wastewater, but also as a carbon and timber investment

property.

44. Unlike the Central

Hawke’s Bay Wastewater Forests, Wairoa District Council (WDC) did proceed

with irrigating treated wastewater into the Mahia Forest.

45. After being pumped over the

hill from the township, the wastewater passes through a series of three

settlement ponds, before being screened and pumped to irrigation fields in the

forest. Irrigation in the different fields is alternated to allow them to fully

dry out between applications and maintain the treatment capacity of the soils.

Of the total 50ha land area, and 35ha forested area, approximately 11ha are

used to treat wastewater.

46. A key risk in

wastewater-irrigated forests is exceeding the treatment capacity of the soil.

This was a major reason for the dissolution of Rotorua’s Whakarewarewa

Forest wastewater irrigation scheme after 28 years of operation. This risk is

managed in the Mahia Forest through ongoing monitoring of tree health,

application volumes and soil moisture levels. The risk to the environment

is managed by monitoring water quality parameters in the stream leaving the

forest.

Figure 2: Nitrogen removed from

Wastewater in the Whakarewarewa Land Treatment System Over Time[2]

47. Management objectives are

listed in the HBRC Forest Estate 2021-2031 Management Plan as:

47.1. To maintain the ability of

the Land to receive and effectively treat wastewater from the Mahia Township

for the foreseeable future

47.2. To protect cultural values

within the Forest, and in particular the registered archaeological sites

47.3. To enhance biodiversity

values in the Forest, building on the work of the Predator Free Mahia Project

47.4. To maximise financial

returns from the Forest while not compromising any of the above.

Central

Hawke’s Bay Forests: Waipukurau and Waipawa

48. The two Central

Hawke’s Bay properties were purchased between 2009 – 2010 and, as

with the Mahia Forest, were established in forest for the purpose of safely

disposing of treated wastewater from the townships while earning revenue from

carbon sequestration and ‘high value hardwood timber’.

49. Central Hawke’s Bay

District Council opted for another option to deal with their wastewater, and

the forests have never been used for this purpose.

50. In 2009 HBRC signed an MOU

with the Rotary Rivers Pathway Trust, allowing the Trust use of the Waipukurau

Forest for mountain biking for a term of 30 years. Since that time, the Trust

has established approximately 15km of mountain bike tracks in the forest, with

a further 5km scheduled for completion in the coming months. The Park is ridden

an estimated 10,000 times annually.

51. Currently, the Waipawa

Forest has only a commercial purpose, though two requests from the community

have been made for its use. The Central Hawkes Bay District Council has

requested the use of the forest for disposing of sludge remaining after their

sewerage treatment, and the Hawkes Bay Riders’ Club has requested its use

for horse rides and potentially grazing.

52. Management objectives for

the Central Hawkes Bay Forests are listed in the HBRC Forest Estate 2021-2031