Meeting of the Finance Audit & Risk Sub-committee

Date: Tuesday 12 February 2019

Time: 9.00am

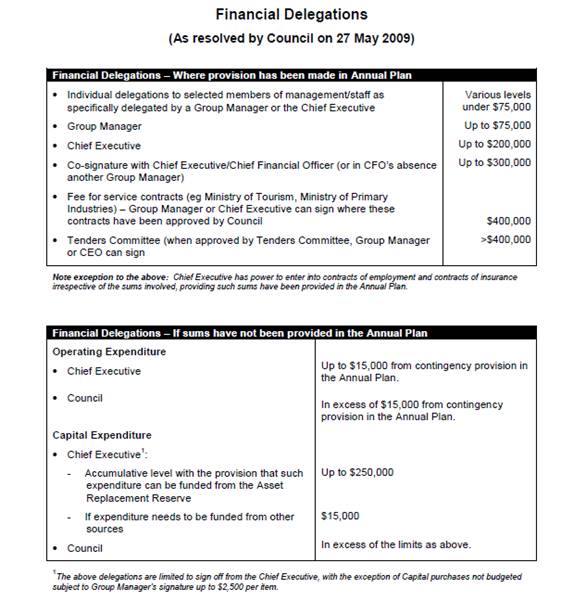

|

Venue:

|

Council Chamber

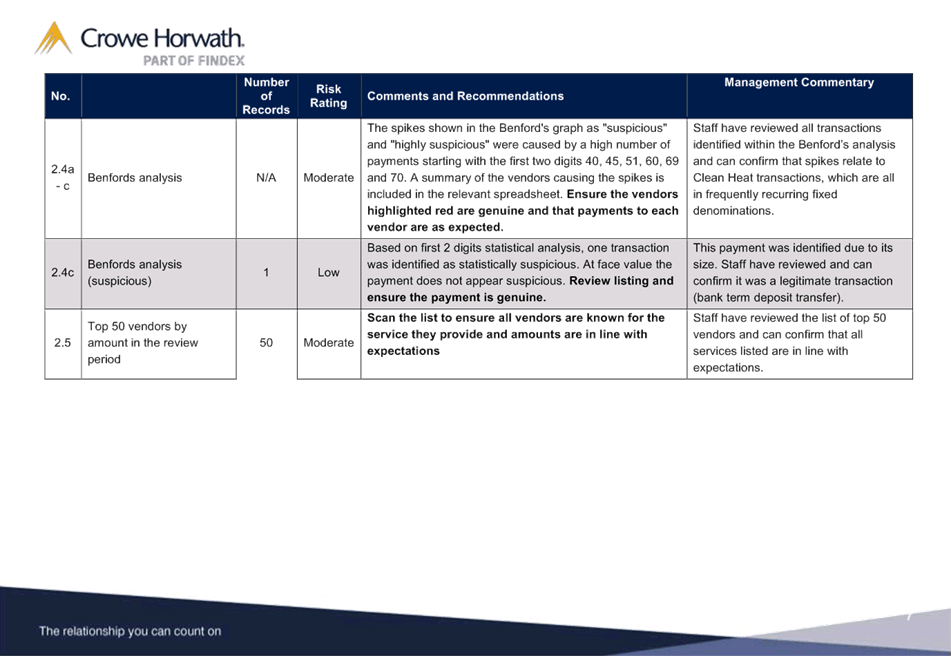

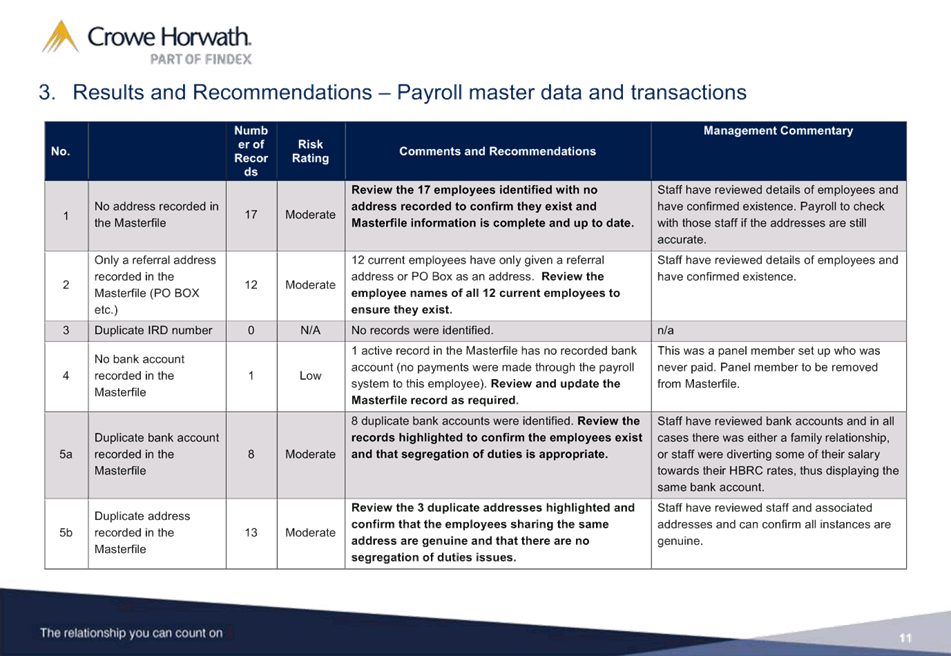

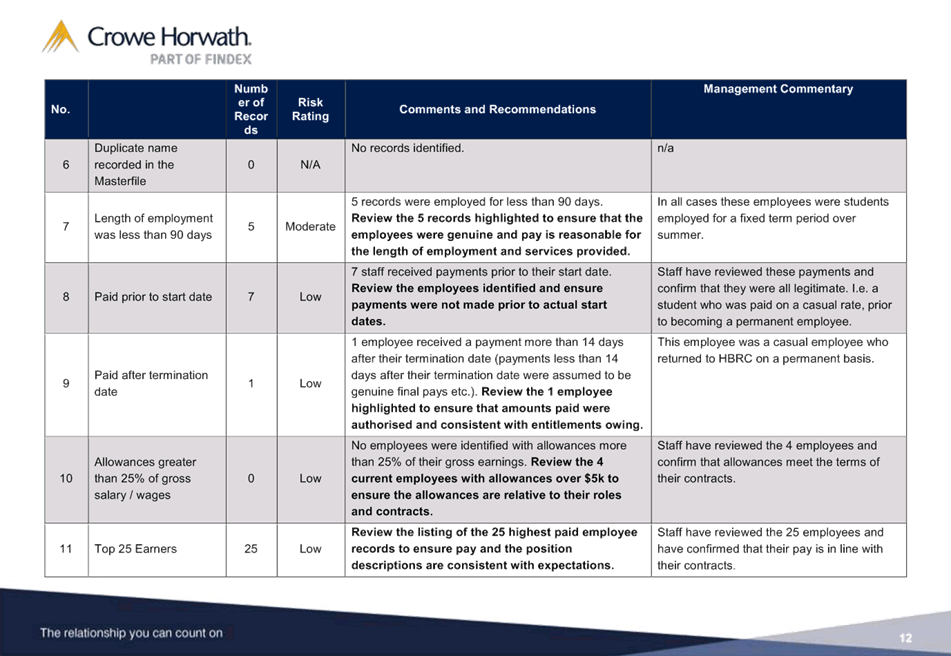

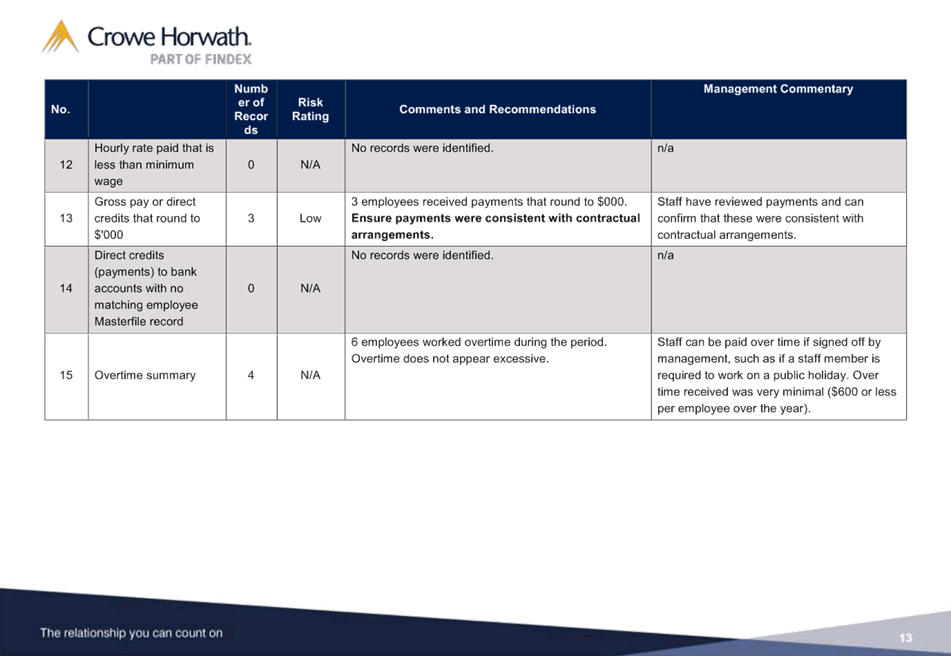

Hawke's Bay Regional Council

159 Dalton Street

NAPIER

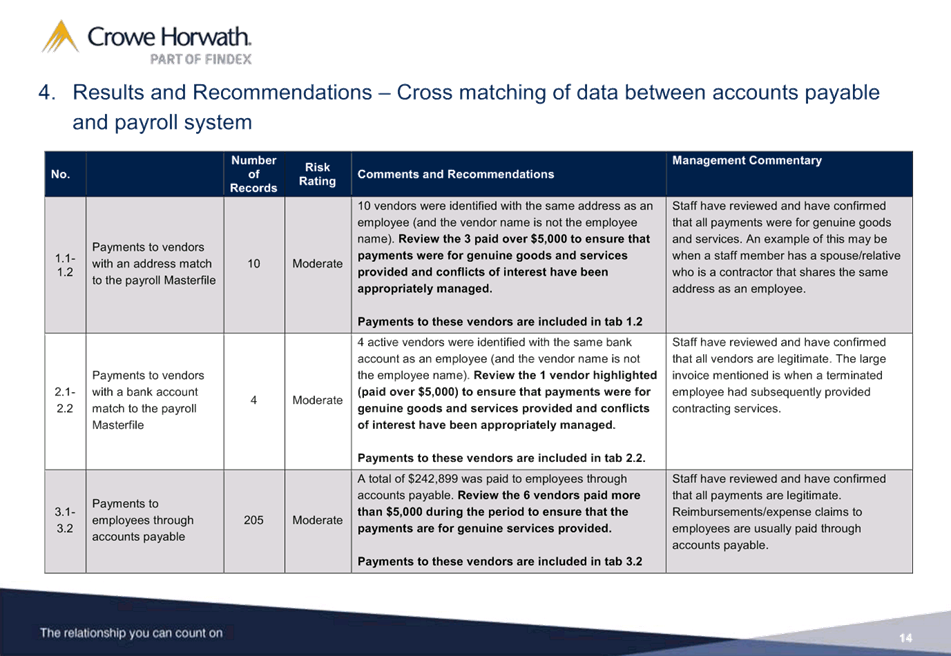

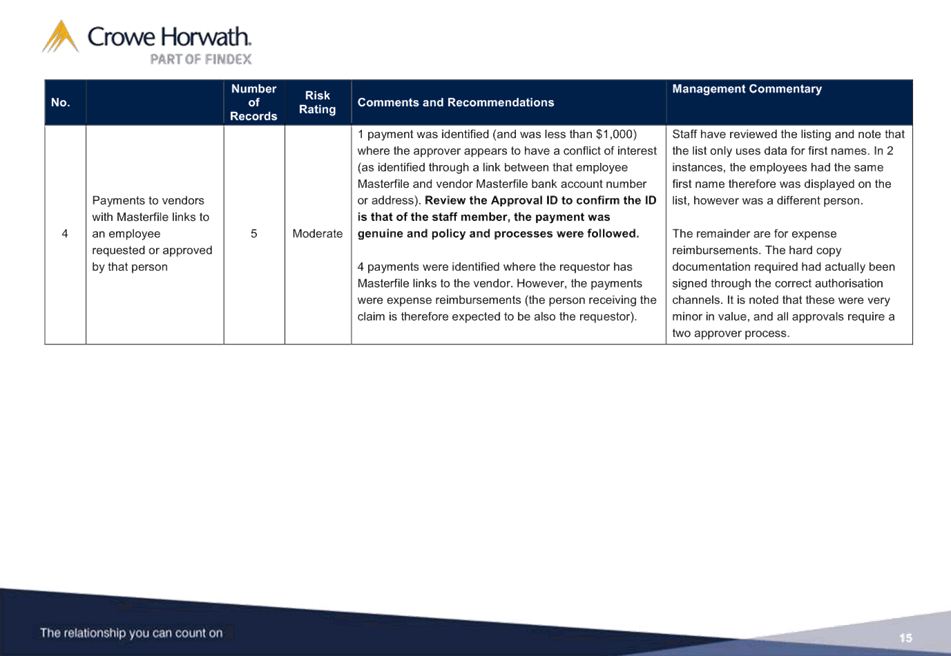

|

Agenda

Item Subject Page

1. Welcome/Notices/Apologies

2. Conflict

of Interest Declarations

3. Confirmation of

Minutes of the Finance Audit & Risk Sub-committee meeting held on 21

November 2018

4. Follow-ups from

Previous Finance Audit & Risk Sub-committee Meetings 3

Decision Items

5. Six Monthly Report

on Risk Assessment and Management 7

6. Proposed Scope for

Follow-up Water Management Internal Audit 15

7. Data Analytics

Internal Audit Report 23

8. Financial

Delegations 45

9. 2017-18 Audit NZ

Management Report 49

Information or Performance Monitoring

10. Treasury Report 85

11. Resource Management

Information System (IRIS) Implementation Update 99

12. February 2019 Sub-committee

Work Programme Update 101

Decision Items (Public Excluded)

13. Confirmation of the Public

Excluded Minutes of the Finance, Audit and Risk Sub-committee Meeting held on

21 November 2018 103

HAWKE’S BAY REGIONAL COUNCIL

Finance

Audit & Risk Sub-committee

Tuesday 12 February 2019

SUBJECT: Follow-ups from Previous Finance

Audit & Risk Sub-committee Meetings

Reason for Report

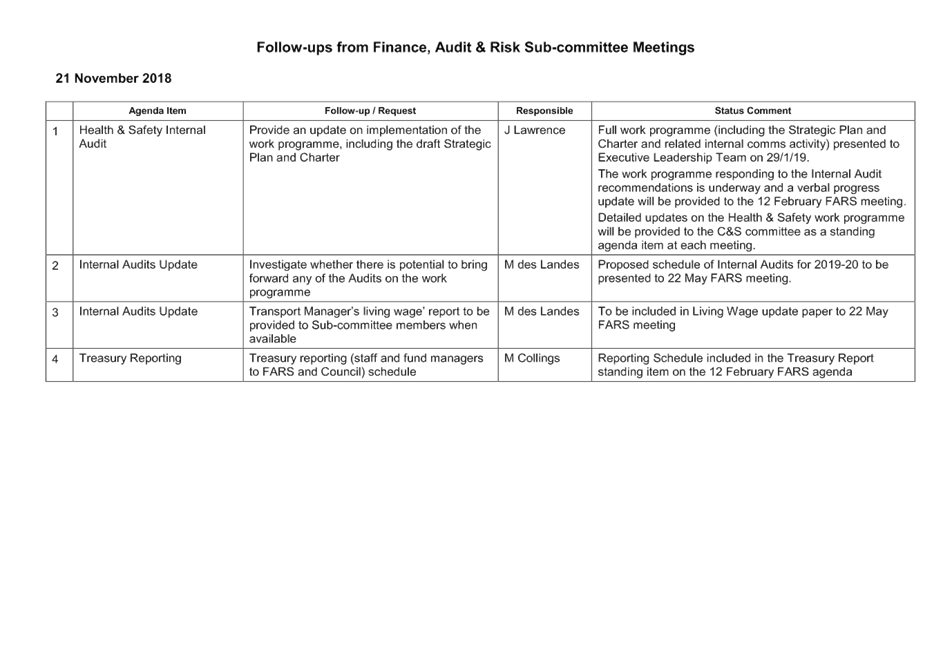

1. In order to track items raised at previous meetings that require

follow-up, a list of outstanding items is prepared for each meeting. All

follow-up items indicate who is responsible for each, when it is expected to be

completed and a brief status comment. Once the items have been completed and

reported to the Committee they will be removed from the list.

Decision

Making Process

2. Council is required to make every decision in

accordance with the Local Government Act 2002 (the Act). Staff have assessed

the in relation to this item and have concluded that as this report is for

information only and no decision is required, the decision making procedures

set out in the Act do not apply.

|

Recommendation

That the Finance, Audit and Risk Sub-committee receives

and notes the report “Follow-ups from Previous Finance Audit and

Risk Sub-committee Meetings”.

|

Authored by:

|

Leeanne

Hooper

Principal Advisor Governance

|

|

Approved by:

|

Jessica

Ellerm

Group Manager

Corporate Services

|

|

Attachment/s

|

⇩1

|

Followups for

Feb 2019 FARS meeting

|

|

|

|

Followups

for Feb 2019 FARS meeting

|

Attachment 1

|

HAWKE’S BAY REGIONAL COUNCIL

Finance

Audit & Risk Sub-committee

Tuesday 12 February 2019

Subject: Six Monthly Report on

Risk Assessment and Management

Reason

for Report

1. To provide the Sub-committee with the six monthly review of the

risks that Council is exposed to and the mitigation actions in place to manage

Council’s risk profile.

Background

2. The

Sub-committee last considered the risk management report at its meeting held

19 September 2018.

3. Subsequent

to this meeting, Executive were briefed and then committed to further risk

management discussion at Executive meetings. Executive also met with Corporate

Accountant individually to commit to delivering on one or more mitigation

strategies within the register. Staff will feedback at future Finance, Audit

& Risk sub-Committee (FARS) meetings as to progress on actions - which

would also be reflected by an update in the risk register.

4. Following

on from a series of six monthly risk management workshops held in January 2019

and examination of findings at several Executive meetings, attached is

the latest risk management update for councillors’ review.

5. At the

September 2018 meeting, the sub-committee was advised of the update to risks

and risk owners as a reflection of the recent LTP restructure. As part of the

risk management maturity process, each risk has had a risk owner commit to an

action(s) in order to further mitigate their risks. This is in addition to the

reassessment of current risks and their impacts within Council.

6. The sub-committee

also requested feedback from the Group Manager – Office of the Chief

Executive & Chair. This commentary is provided in the “Summary of

Risk Management” section following, along with further detail around

other aspects of Risk Management at Council and future plans including a

proposed review of internal processes.

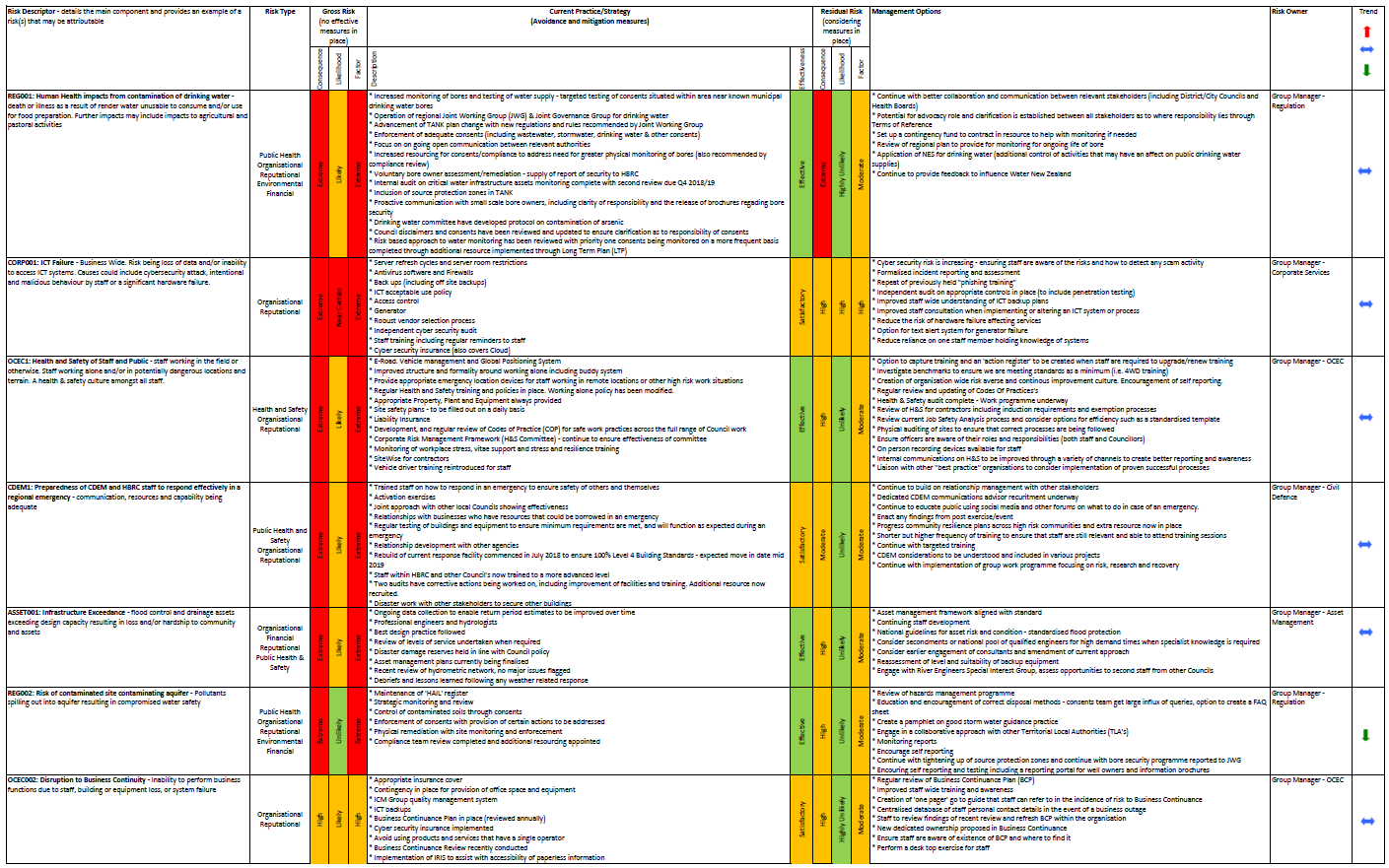

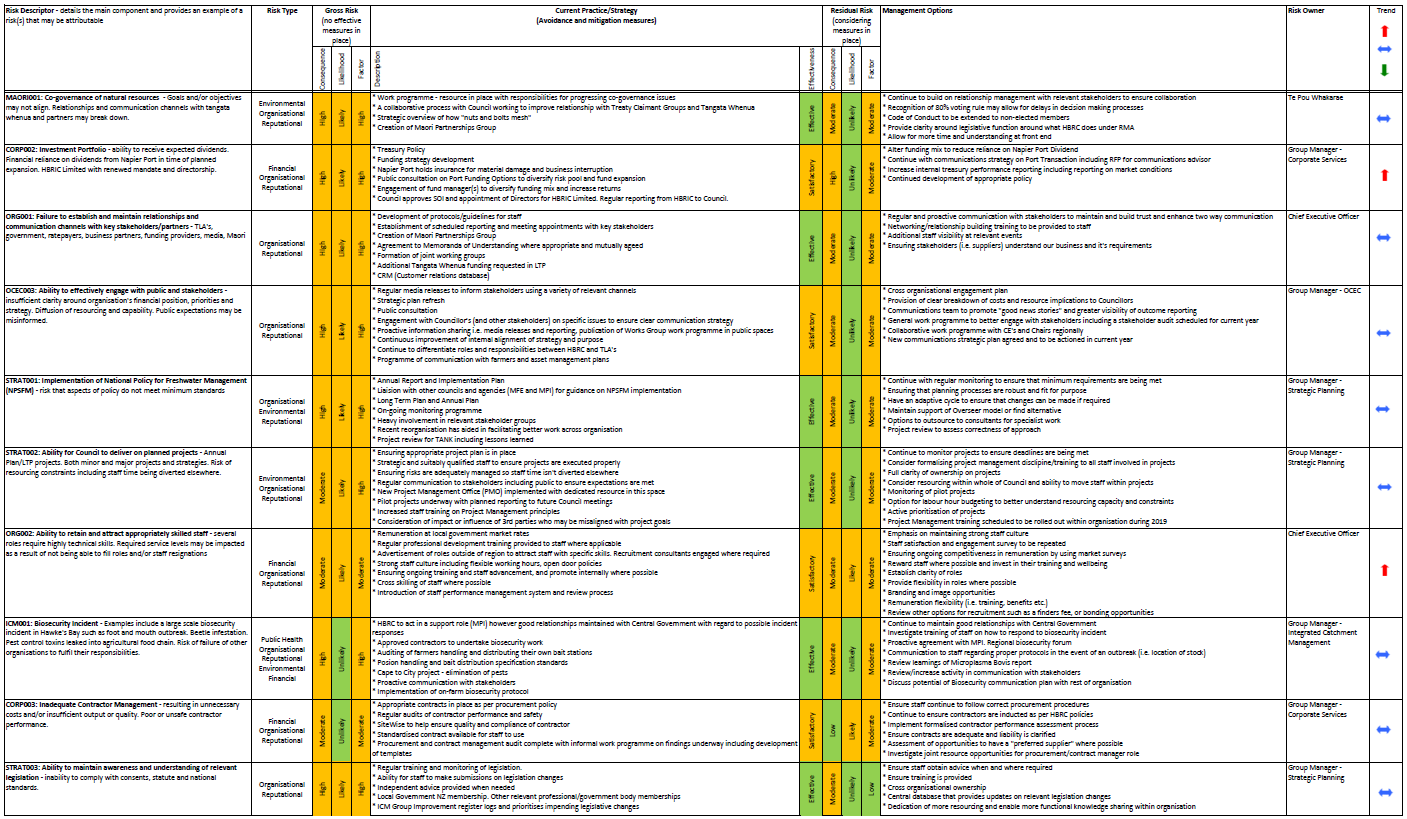

Risk Management Progress

7. Overall

there has been a series of tangible mitigation strategies employed as Council

evolves its risk management process. This has been assisted by the recent LTP

process whereby additional resource has been added and has enabled Council to

be more proactive.

8. A key

example of this is within the Contamination of Drinking Water risk, a series of

proposed “management options” have now become current practice for

this risk. This is due to the additional resource added to the Compliance team

which has enabled Council to do more testing after Priority One consents have

been identified.

9. In

addition, there has been better communication with stakeholders which has been

aided by streamlined Council communication, additional clarity provided in the

form of brochures and review of disclaimers, and the Joint Drinking Water

committees which are now up and running.

10. There is a programme

in place for improving Health & Safety within Council which is driven out

of a recent Health & Safety audit which was presented to this Sub-Committee

on 21 November last year. Feedback from the risk workshops has been positive,

with other additional suggestions made to improve Health & Safety, with a

focus on physical competence to complete a job, such as operation of a Land Use

Vehicle.

11. It is noted that in

this example (and others) some of the mitigation options will never necessarily

be “complete” as some will require regular monitoring and progress,

as such the narrative within the register has been updated to reflect that

Council should continue to drive its risk mitigation strategies.

12. In addition, the level

of engagement across the organisation has increased generally around risk

management, with additional executive meetings, and further staff engagement on

risks and communication. There is an improved culture of understanding and

engagement with senior staff which Council will continue to progress.

13. Key changes to the

matrix are outlined further below. These changes are in addition to

reassessment of current practices and treatment options which have also been

updated in the register. Risk descriptors have also been updated to better

reflect the actual risk to Council.

Key

Changes to the Risk Matrix

14. Three previous risks

have been renamed to better reflect the actual risk to Council.

|

Previous Risk Title

|

Amended Risk Title

|

Commentary

|

|

Failure

to meet unrealistic public expectations

|

Ability

to effectively engage with public and stakeholders

|

Recognition that the risk is not so much in

Council’s ability to meet expectations, but the ability to effectively

educate and communicate with stakeholders

|

|

Infrastructure Failure

|

Infrastructure

Exceedance

|

Recognition that flood and drainage systems are

designed to meet minimum standards and the risk is that systems exceed such

standards

|

|

Risk

of staff providing incorrect or sensitive information to stakeholders

|

Risk

of Council providing incorrect or sensitive information to stakeholders

|

Recognition

that the risk of providing incorrect or sensitive information extends to

beyond staff.

|

15. Risk trend ratings

have been amended as follows.

|

Risk

|

Previous Trend Rating

|

New Trend Rating

|

Commentary

|

|

Risk of Contaminated

Site contaminating Aquifer

|

|

|

Recognition of

additional resourcing within this space including improvement monitoring

capacity and better information programmes

|

|

Implementation of

National Policy for Freshwater Management

|

|

|

TANK implementation

lessons learned

|

|

Ability for Council to

deliver on Planned Projects

|

|

|

Recognition of Project

Management Office up and running with dedicated resource to ensure project

service delivery.

|

16. Residual Risk

assessments have been amended as follows.

|

Risk

|

Previous Assessment

|

New Assessment

|

Commentary

|

|

Inadequate Contractor

Management

|

Effectiveness:

Effective

Likelihood:

Unlikely

Risk Factor:

Low

|

Effectiveness:

Satisfactory

Likelihood:

Likely

Risk Factor:

Moderate

|

Recognition of recent

procurement and contract management audit which identified a number of

inconsistencies in approach between groups.

Staff are working

through this internally and with other agencies to improve contract

management within Council.

|

Summary of Risk Management

External

Review

17. As proposed at its

previous meeting, a risk management review is proposed for the 2019-20

financial year. This review will form part of the agreed Crowe Horwath internal

audit programme included in existing internal audit budgets. A timeline and

scope will be presented at the 22 May 2019 sub-committee meeting. The scope

will include an assessment of the effectiveness of current risk management

policies and practices within Council.

Council

Collaboration

18. Council staff have

been meeting with Hastings District Council risk managers on an informal basis.

Initial meetings indicated that there was a lot of overlap with risks within

the two councils’ registers. As a result it was decided to invite

representatives of all five councils to the meetings, which have proven to be

insightful in terms of risk management information sharing and discussion of

emerging risks within our region.

Hawke’s

Bay Forums

19. In addition to the

above, it was recognised that risk mitigation can benefit from sharing

collective expertise with other agencies within Hawke’s Bay. As a result

a Hawke’s Bay Risk Management Forum was created which includes

representatives from local Councils, local government departments, and local

industries.

20. Its first official meeting was held in December 2018,

facilitated by Price Waterhouse Coopers, and a Terms of Reference is being

drafted. Future meetings are intended to be scheduled on a quarterly basis,

with the purpose of these meetings being to discuss topical risks within our

region, along with shared best practice for risk management.

Project Risks

21. Reporting on

Council’s project risks has been incorporated into the Project Management

Office (PMO). The PMO has created a reporting format for project risks that is

in line with the current risk management reporting framework.

22. The PMO and Risk

Management team meet on at least a quarterly basis to discuss any Project risk

trends that may need to be incorporated into the Council wide strategic risk

register.

23. To date, the key risks

arising throughout the PMO process are aligned with the current risk register

and are focused mainly around staff resourcing and ability to prioritise

projects based on capacity and demands.

Risk

Management Group Manager Commentary

24. Group Manager –

Office of the Chief Executive and Chair is unable to attend this meeting due to

previously booked leave, however notes that in the previous six months, risk

management capacity within Council has increased with further resource

assisting with the risk management process. The process has also extended from

its original recording and awareness nature, to increased utilisation of the

register as a tool to drive change and progress in the risk management space.

Specifically, risk owners have each committed to actions which will be

monitored by risk staff to allow for increased visibility and accountability on

mitigation strategies.

25. Risk management is

also on the Executive Leadership Team (ELT) meeting agenda once a month, on

average, to ensure that the risks have full and regular executive oversight,

along with frequent updates on progress.

26. Whilst the risk

management process has gained traction and maturity over the recent two years

with regular and frequent Executive interrogation of all strategic level risks,

it is recognised that there is still work to be done to filter risk management

understanding and awareness throughout the rest of the organisation. Staff will

report back on progress on this at the next risk management update to FARS.

Decision

Making Process

27. Council

and its committees are required to make every decision in accordance with the

requirements of the Local Government Act 2002 (the Act). Staff have assessed

the requirements in relation to this item and have concluded:

27.1. The

decision does not significantly alter the service provision or affect a

strategic asset, and is not inconsistent with an existing policy or plan.

27.2. The use

of the special consultative procedure is not prescribed by legislation.

27.3. The

decision does not fall within the definition of Council’s policy on

significance.

27.4. The

decision of the sub-committee is in accordance with the Terms of Reference and

decision making delegations adopted by Hawke’s Bay Regional Council

9 November 2016, specifically:

27.4.1. The

Finance, Audit and Risk Sub-committee shall have responsibility and authority

to review whether Council management has a current and comprehensive risk

management framework and associated procedures for effective identification and

management of the council’s significant risks in place, and

27.4.2. undertake

periodic monitoring of corporate risk assessment, and the internal controls

instituted in response to such risks

27.4.3. report on

Council’s risk management systems, processes and practices to the

Corporate and Strategic Committee to fulfil its responsibilities.

|

Recommendations

That the Finance, Audit and Risk Sub-committee:

1. receives and considers the “Six Monthly Risk

Assessment and Management” staff report

AND

2. confirms the Sub-committee’s confidence that Council management has a current and comprehensive risk management

framework and associated procedures for effective identification and

management of the Council’s significant risks

3. recommends that the Corporate and Strategic Committee receives and

notes the resolutions of the sub-committee, confirming the robustness of Council’s risk management systems,

processes and practices.

OR

4. advises staff of the specific risks (following) that require

reassessment to confirm the level of risk is accurate and internal controls

are adequate, for reporting back to the 22 May 2019 Sub-committee

meeting.

4.1. …

4.2. …

5. recommends that the Corporate and Strategic Committee receives and

notes the resolutions of the sub-committee, including the specific risks that

require reassessment.

|

Authored by: Approved

by:

|

Melissa des

Landes

Corporate Accountant

|

Jessica

Ellerm

Group

Manager Corporate Services

|

Attachment/s

|

⇩1

|

Risk Management Register Feb 2019

|

|

|

|

Risk Management Register Feb 2019

|

Attachment 1

|

|

Risk

Management Register Feb 2019

|

Attachment 1

|

|

Risk

Management Register Feb 2019

|

Attachment 1

|

HAWKE’S BAY REGIONAL

COUNCIL

Finance

Audit & Risk Sub-committee

Tuesday 12 February 2019

Subject: Proposed Scope for

Follow-up Water Management Internal Audit

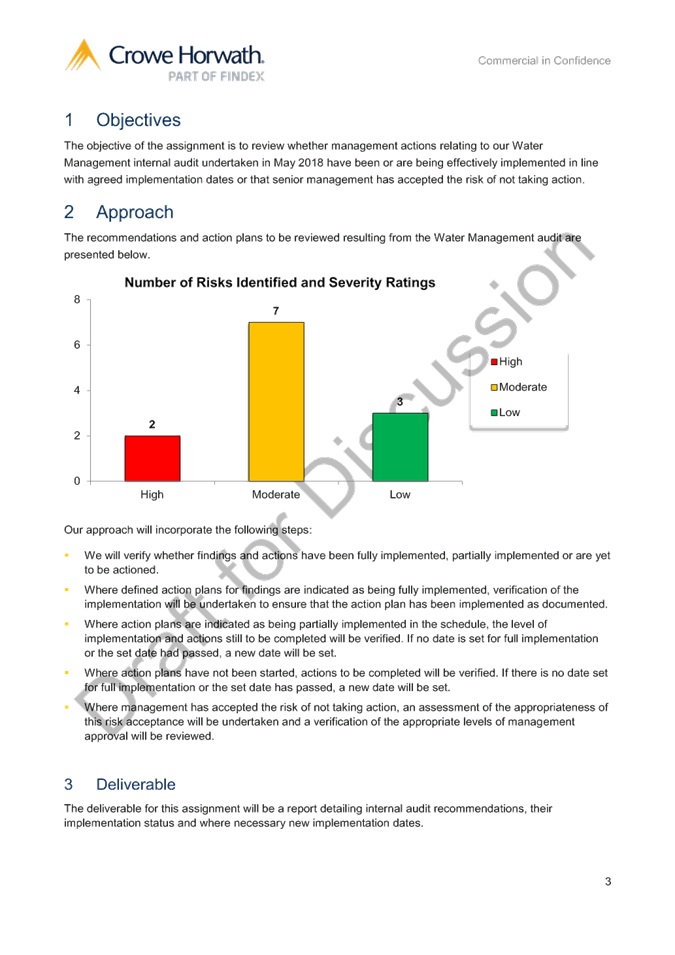

Reason for Report

1. To present a

proposed scope for a Water Management Follow-up Internal Audit for the

sub-committee’s review and feedback.

Background

2. At its meeting

6 June 2018, an internal audit report on HBRC’s Water Management

processes was presented to the sub-committee. This report contained a series of

findings, recommendations, and management’s responses to each finding.

3. At the same

meeting, the sub-committee was presented with a proposed internal audit

programme for the 2018-19 financial year. Councillors requested at that meeting

that a Water Management “Follow up” audit be included within the

2019-20 work programme.

4. The primary

purpose of this audit is for Crowe Horwath to independently investigate

Council’s progress on implementing and maintaining agreed action points

that were stated as a response to the original audit, and the proposed scope is

attached.

5. Staff note that

there are less hours allocated to this follow-up audit than the original audit,

due to the groundwork already having been completed. The number of hours

allocated are within Council’s agreed internal audit budget for the year.

Decision Making

Process

6. Council and its committees are required to make every decision in

accordance with the requirements of the Local Government Act 2002 (the Act).

Staff have assessed the requirements in relation to this item and have

concluded:

6.1. The decision does not significantly alter the service provision or

affect a strategic asset, and is not inconsistent with an existing policy or

plan.

6.2. The use of the special consultative procedure is not prescribed by

legislation.

6.3. The decision does not fall within the definition of Council’s

policy on significance.

6.4. The decision of the sub-committee is in accordance with the Terms of

Reference and decision making delegations adopted by Hawke’s Bay Regional

Council 9 November 2016, specifically:

6.4.1. The Finance, Audit and Risk Sub-committee shall have responsibility

and authority to confirm the terms of appointment and engagement of external

auditors, including the nature and scope of the audit, timetable, and fees.

|

Recommendations

That the Finance, Audit and Risk Sub-committee:

1. Receives and notes the “Proposed Scope for the

Follow-up Water Management Internal Audit” staff report.

2. Confirms the proposed Scope for the Follow-up Water Management

Internal Audit including amendments agreed 12 February 2019.

|

Authored by:

|

Melissa des

Landes

Corporate Accountant

|

|

Approved by:

|

Jessica

Ellerm

Group Manager

Corporate Services

|

|

Attachment/s

|

⇩1

|

HBRC Internal

Audit Scoping document - follow-up Water Management Audit

|

|

|

|

HBRC

Internal Audit Scoping document - follow-up Water Management Audit

|

Attachment 1

|

HAWKE’S BAY REGIONAL COUNCIL

Finance

Audit & Risk Sub-committee

Tuesday 12 February 2019

Subject: Data Analytics Internal

Audit Report

Purpose of Report

1. To present the internal audit report (attached) for the Data

Analytics audit undertaken by Crowe Horwath in late 2018.

Background

2. The Finance, Audit and Risk Sub-committee (FARS) agreed at its

meeting on 6 June 2018, as part of the internal audit work programme, to engage

Crowe Horwath to conduct an internal audit of Council’s Data Analytics.

3. The agreed scope and purpose of the audit was to review payables and

payroll, and master and transactional data for the financial year ended 30 June

2018. This data was then analysed independently by Crowe Horwath for any

potential anomalies or suspicious transactions.

4. The report was then provided to staff, along with a separate spreadsheet

listing the transactions that required review. This report was initially

analysed by the Corporate Accountant and then reviewed by the Chief Financial

Officer. Any findings requiring further interrogation were actioned where

deemed necessary. The process included questioning the Payroll officer and the

Accounts Payable officer and examination of relevant invoices and

authorisations.

5. Following the review of findings, commentary has been provided

alongside each finding within the report. For ease of reference, a key findings

analysis is provided in the “Report Analysis” section following.

6. As a reminder, this is the second Data Analytics audit conducted by

Crowe Horwath, having reported the findings of the 2016-17 audit to the

sub-committee on 4 December 2017. A comparison to previous findings is also

provided in separate analysis following.

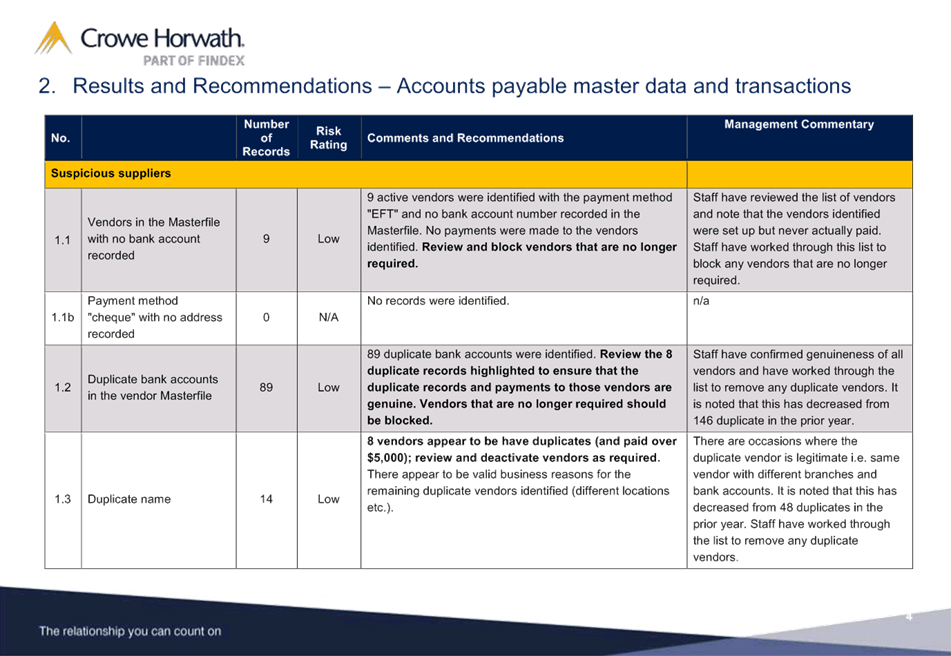

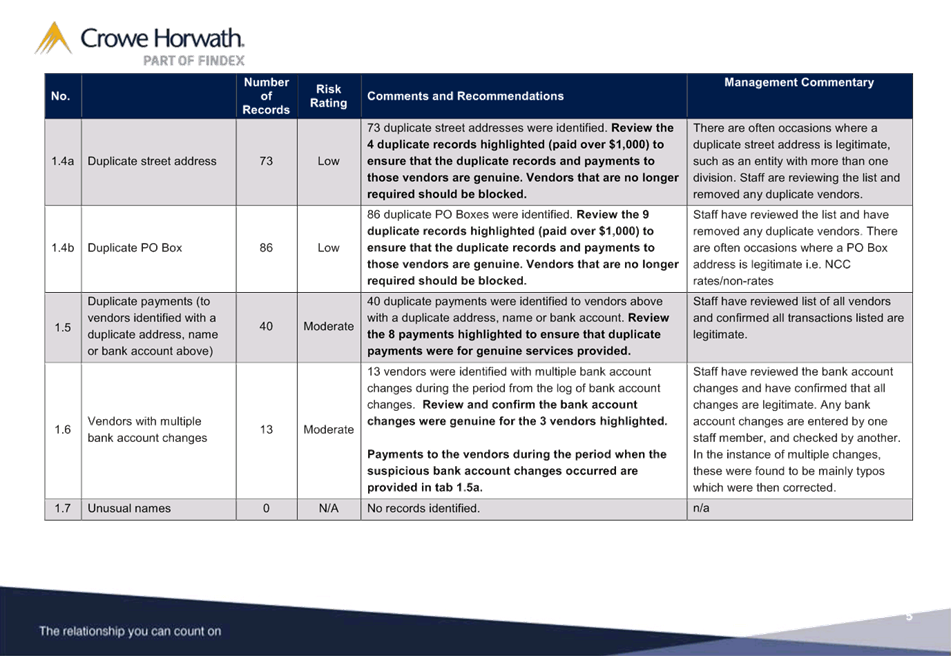

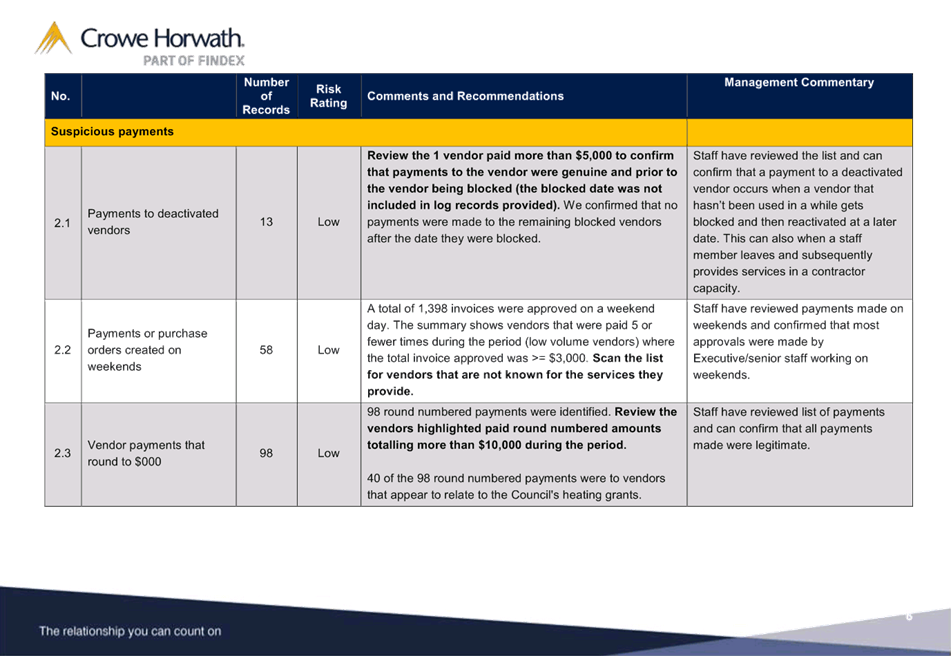

Report Analysis

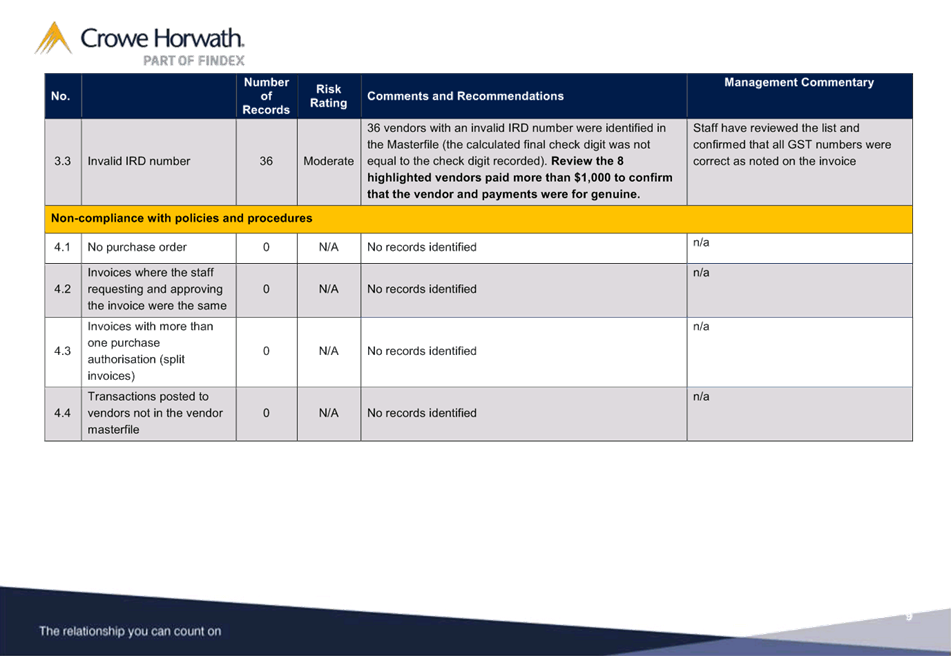

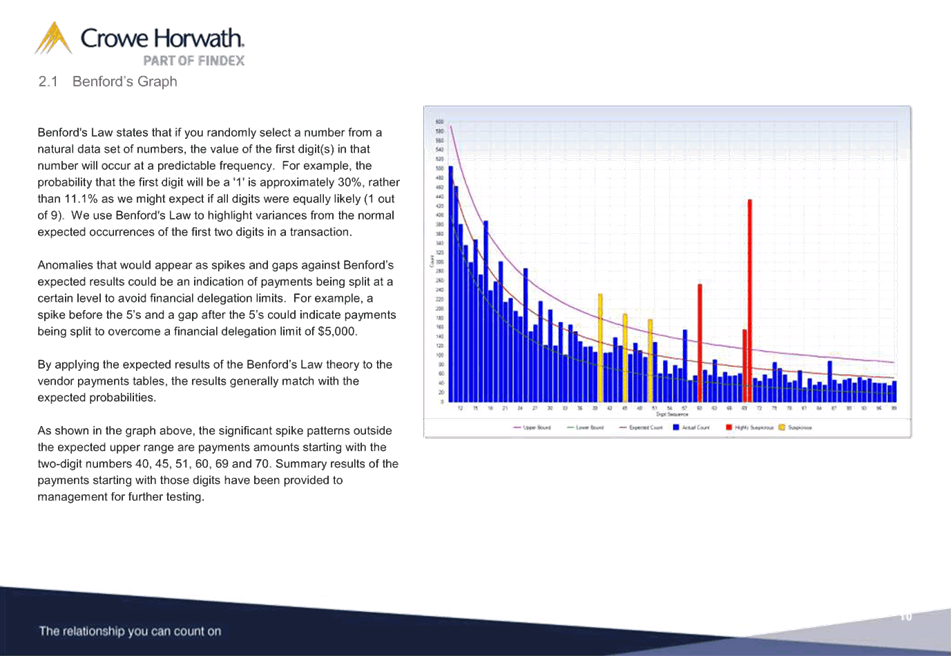

7. It is important to note that when a transaction is identified; it

does not necessarily indicate that there is anything suspicious. There are

often legitimate business reasons for a transaction being identified, such as

different types of payments to a Council (rates credits versus payment for

services) by way of pure example. These types of transactions may display in

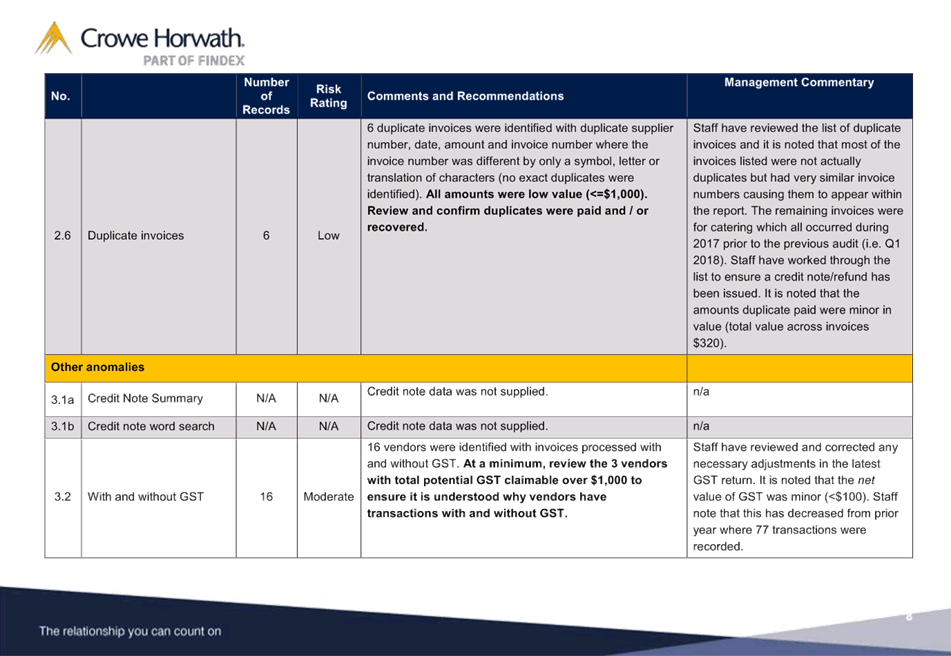

areas such as “duplicate address”, “GST/non-GST

transactions”, or “duplicate IRD number” for example.

8. In addition, some transactions are listed purely for review purposes

due to their higher risk nature, such as “review of top 50 vendors”

as a further example. This in itself allows staff to easily assess that vendors

are in line with expectations and would highlight any vendors that may appear

erroneous.

9. As a result, only transactions that require further attention are

outlined following. A full commentary of each finding, however, is provided in

the attachment.

10. Given the

small size of Hawke’s Bay, there are often times when an employee may

share the same address as a vendor, usually a spouse. Accounts processing staff

ensure that employee approvals are not allowed where any conflicts exist

between an employee and a vendor.

11. There

were a selection of payments to some vendors that had a combination of GST and

non-GST applied to the transactions. There were two instances where the

incorrect GST treatment was applied and staff have since corrected this in the

latest GST return.

12. There was

a small number of invoices paid twice. This is often due to a supplier

providing several small value invoices which staff have approved a second time

without realising. It is noted that this occurred within Q1 of the 2017-18

financial year, prior to staff receiving findings of the initial data analytics

audit discussed further following. Staff have worked through with vendors to

receive a refund/credit note where applicable. The financial implication of

these is low in value.

13. In terms

of the payroll master file and transactional data, there were fewer records

identified during this year, with no major issues to note. There were some

records that require tidying up however, such as 17 employees that did not yet

have addresses recorded in their master file. Payroll is working on following

up with those employees.

2016-17 Comparison

14. There are

several notable improvements since the initial 2016-17 audit was presented to

FARS.

15. The list

of duplicates within the supplier master file has decreased substantially. For

example, duplicate bank accounts have decreased from 146 to 89. Of these 89,

some will be legitimate duplicates, such as when a vendor has more than one

business function i.e. Hastings District Council. Duplicate named vendors have

decreased from 48 to 8.

16. While

there were a small number of minor duplicate payments, these all occurred

within the first quarter of the 2017-18 financial year and there have not been

any duplicate payments made to vendors since the 2016-17 audit was presented in

December 2017.

17. There are

also significantly fewer GST/non-GST transactions paid to the same vendor. This

has decreased from 77 transactions, to 16. It is noted that 14 of these

transactions had correct GST treatment, with only two minor adjustments being

required, with a net value of less than $100.

18. Overall

improvement in internal processes is noticeable since the prior data analytics

assignment was performed, with additional checks reducing the number of

transactions arising within the review. Staff recognize, however, that there is

still further work to be done to further reduce errors.

19. A

proposed 2019-20 internal audit schedule will be presented at the 22 May

2019 FARS meeting. Staff are seeking feedback as to whether this Sub-committee

would like to see another data analytics assignment included in that proposal,

as Auditors recommend completing a data analytics audit every year.

Decision Making

Process

20. Council and

its committees are required to make every decision in accordance with the

requirements of the Local Government Act 2002 (the Act). Staff have assessed

the requirements in relation to this item and have concluded:

20.1. The

decision does not significantly alter the service provision or affect a

strategic asset, and is not inconsistent with an existing policy or plan.

20.2. The use

of the special consultative procedure is not prescribed by legislation.

20.3. The

decision does not fall within the definition of Council’s policy on

significance.

20.4. The

decision of the sub-committee is in accordance with the Terms of Reference and

decision making delegations adopted by Hawke’s Bay Regional Council

9 November 2016, specifically:

20.4.1. The Finance, Audit and

Risk Sub-committee shall have responsibility and authority to receive the

internal and external audit report(s) and review actions to be taken by

management on significant issues and audit recommendations raised within the

report(s)

20.4.2. Report to the Corporate

and Strategic Committee, on whether appropriate action has been taken by

management in response to the Data Analytics Internal Audit recommendations.

|

Recommendations

That the Finance, Audit and Risk

Sub-committee:

1. receives and notes the “Data Analytics Internal Audit

Report”

AND

2. confirms its confidence that appropriate

action has been taken by management in response to the Data Analytics

Internal Audit recommendations

3. recommends that the Corporate and Strategic Committee receives and

notes the resolutions of the sub-committee, confirming that appropriate action has been taken by

management in response to the Data Analytics Internal Audit recommendations.

OR

4. advises staff of the specific action required in response to the Data Analytics Internal Audit recommendation stated following, as agreed, for reporting back to the 22 May 2019

Sub-committee meeting.

4.1 …

…

4.2 …

…

5. recommends that the Corporate and Strategic Committee receives and

notes the resolutions of the sub-committee, including the specific actions required in response to the Data

Analytics Internal Audit recommendations.

|

Authored by:

|

Melissa des

Landes

Corporate Accountant

|

|

Approved by:

|

Jessica

Ellerm

Group Manager

Corporate Services

|

|

Attachment/s

|

⇩1

|

Data

Analytics Internal Audit Report

|

|

|

|

Data

Analytics Internal Audit Report

|

Attachment 1

|

|

Data

Analytics Internal Audit Report

|

Attachment 1

|

|

Data

Analytics Internal Audit Report

|

Attachment 1

|

HAWKE’S BAY REGIONAL

COUNCIL

Finance

Audit & Risk Sub-committee

Tuesday 12 February 2019

Subject: Financial Delegations

Reason for Report

1. To provide the

Finance, Audit and Risk Sub-committee with the opportunity to discuss the

current financial delegations for the Chief Executive (CE) and Group Managers.

2. Any changes to

financial delegations need to be approved by Council, so this item enables

debate thought the sub-committee, the Corporate and Strategic Committee and

then recommendations to Council.

Background

3. Council last

changed the financial delegations for the CE and Group Managers in 2009, and

the levels decided then are still current as below.

4. Since 2009

Council’s annual expenditure has increased from $32 million to $45

million but the delegation limits have remained the same. Staff believe that an

update of the financial delegations is well overdue and should be updated to

allow for efficient operation, especially to implement the ambitious workload

of the 2018-28 long term plan.

5. Staff have

investigated the delegation limits of other regional councils whose delegations

were online, with the results shown below.

|

Council

|

Role

|

Delegation

|

|

Greater Wellington

|

CE

|

Authority to

implement the Annual Plan

|

|

Group

Managers

|

$200,000

|

|

Environment Canterbury

|

CE &

Group Manager (Jointly)

|

Authority to

implement the Annual Plan

|

|

CE

|

$250,000

|

|

Group

Manager

|

$250,000

|

|

Bay of Plenty

|

CE

|

$2,000,000

|

|

Group

Manager

|

Delegated by

CE

|

Proposal

6. Staff propose

that the financial delegation levels for the CE and Group Managers be increased

to levels that reflect the organisational growth over the last 10 years, align

more closely to other regional councils and allow for the organisation to

operate efficiently.

7. The following

recommendations are based on simplifying the current system and allowing for

practical governance.

|

Financial Delegations – Where provision is

made in the LTP / Annual Plan

|

|

CE

|

Authority to

implement the LTP/Annual Plan as approved by Council – with a tolerance

of up to the higher of $100,000 or 5%

|

|

Group Managers

|

Up to

$150,000

|

|

Staff

|

Delegations

provided by their Group Manager up to a level of $100,000

|

8. The Tenders

Committee is only used for competitive procurement processes over $400,000.

Financial Delegations – Where no provision is

made in the LTP / Annual Plan

|

|

Operating

Expenditure

|

|

Council

|

In excess of

$100,000

|

|

CE

|

Up to

$100,000

|

|

Capital

Expenditure

|

|

Council

|

In excess of

the limits below

|

|

CE

|

Up to $50,000

per asset if funded via asset replacement reserve

Up to

$20,000 if funded elsewhere

|

|

Group

Managers

|

Up to

$20,000 per asset if funded via asset replacement reserve

Up to $5,000

if funded elsewhere

|

Decision Making

Process

9. Council and its

committees are required to make every decision in accordance with the

requirements of the Local Government Act 2002 (the Act). Staff have assessed

the requirements in relation to this item and have concluded:

9.1. The decision

does not significantly alter the service provision or affect a strategic asset,

and is not inconsistent with an existing policy or plan.

9.2. The use of

the special consultative procedure is not prescribed by legislation.

9.3. The decision

does not fall within the definition of Council’s policy on significance.

9.4. The decision

of the sub-committee is in accordance with the Terms of Reference and decision

making delegations adopted by Hawke’s Bay Regional Council

9 November 2016, specifically:

9.4.1. The purpose of the Audit and Risk Sub-committee is to report to the

Corporate and Strategic Committee to fulfil its responsibilities for the

provision of appropriate controls to safeguard the Council’s financial

and non-financial assets, the integrity of internal and external reporting and

accountability arrangements.

|

Recommendations

1. That the Finance, Audit and Risk Sub-committee receives and notes

the “Financial Delegations” staff report.

2. That the Finance, Audit and Risk Sub-committee provides feedback

on the “Financial Delegations” levels proposed.

3. The Finance, Audit and Risk Sub-committee recommends that the

Corporate and Strategic Committee:

3.1. Agrees that the decisions to be made are not significant under the

criteria contained in Council’s adopted Significance and Engagement

Policy, and that the Committee can exercise its discretion and make decisions

on this issue without conferring directly with the community or persons

likely to be affected by or have an interest in the decision.

3.2. Reviews and considers the proposed Financial

Delegations and provides feedback for recommendations to Council for

decision.

|

Authored by:

|

Manton

Collings

Chief Financial Officer

|

|

Approved by:

|

Jessica

Ellerm

Group Manager

Corporate Services

|

|

Attachment/s

There are no

attachments for this report.

HAWKE’S BAY REGIONAL

COUNCIL

Finance

Audit & Risk Sub-committee

Tuesday 12 February 2019

Subject: 2017-18 Audit NZ

Management Report

Reason for Report

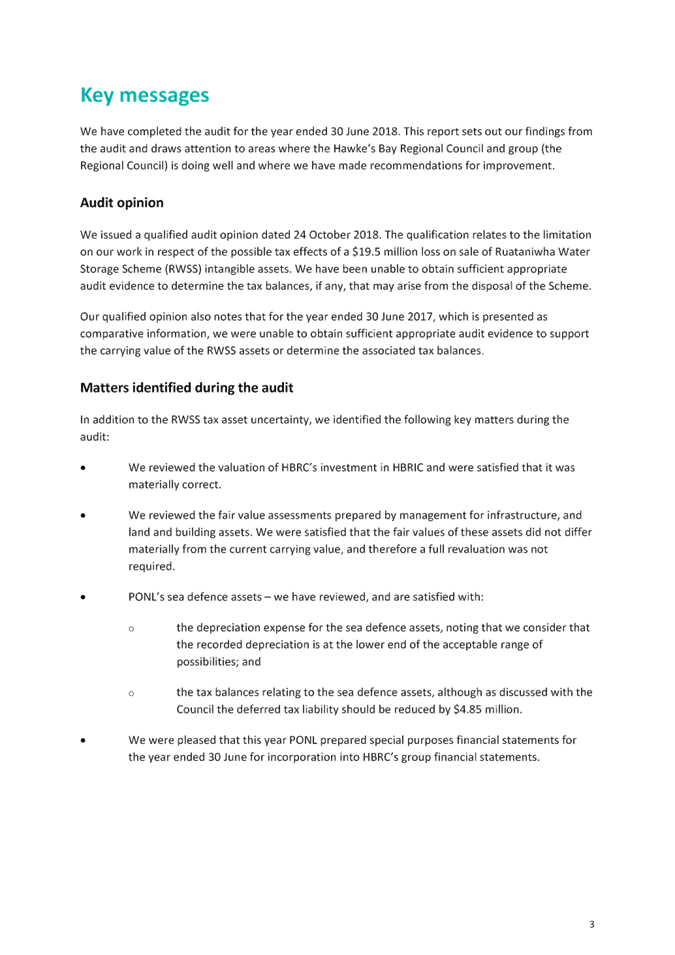

1. To provide the opportunity for the sub-committee to review and

discuss the Report to the Council on the Audit of Hawke’s Bay Regional

Council for the year ended 30 June 2018.

Background

2. Each year Audit NZ provides Council with a report on how the audit

went for the previous year. This includes any significant matters and

recommendations that came out of the audit process.

3. Review of these reports provides the sub-committee with the chance

to ask further questions and gain comfort from the audit process. It also gives

an indication of any changes that might be occurring in the next financial

year.

4. Unfortunately our Audit NZ director, Stephen Lucy cannot be at the

meeting but had previously talked with the sub-committee on a number of these

matters and will continue to do so over the 2019/20 audit.

Decision Making

Process

5. Council and its committees are required to make every decision in

accordance with the requirements of the Local Government Act 2002 (the Act).

Staff have assessed the requirements in relation to this item and have

concluded:

5.1. The decision does not significantly alter the service provision or

affect a strategic asset, and is not inconsistent with an existing policy or

plan.

5.2. The use of the special consultative procedure is not prescribed by

legislation.

5.3. The decision does not fall within the definition of Council’s

policy on significance.

5.4. The decision of the sub-committee is in accordance with the Terms of

Reference and decision making delegations adopted by Hawke’s Bay Regional

Council 9 November 2016, specifically:

5.4.1. The purpose

of the Audit and Risk Sub-committee is to report to the Corporate and Strategic

Committee to fulfil its responsibilities for the independence and adequacy of

internal and external audit functions.

5.4.2. The Finance,

Audit and Risk Sub-committee shall have responsibility and authority to receive

the internal and external audit report(s) and review actions to be taken by

management on significant issues and audit recommendations raised within the

report(s)

5.4.3. The Finance,

Audit and Risk Sub-committee shall have responsibility and authority to conduct

a sub-committee members-only session with Audit NZ to discuss any matters that

the auditors wish to bring to the Sub-committee’s attention and/or any

issues of independence.

|

Recommendation

1. That the Finance, Audit and Risk

Sub-committee receives and notes the “2017-18

Audit NZ Management Report”.

2. The Finance, Audit and Risk Sub-committee recommends that the

Corporate and Strategic Committee:

2.1. Agrees that the decisions to be made are not significant under the

criteria contained in Council’s adopted Significance and Engagement

Policy, and that the Committee can exercise its discretion and make decisions

on this issue without conferring directly with the community or persons

likely to be affected by or have an interest in the decision.

2.2. Confirms the Finance, Audit and Risk Sub-committee’s

satisfaction that the “2017-18 Audit NZ

Management Report” is sufficient and

that there are no outstanding issues of concern.

|

Authored by:

|

Manton

Collings

Chief Financial Officer

|

|

Approved by:

|

Jessica

Ellerm

Group Manager

Corporate Services

|

|

Attachment/s

|

⇩1

|

Report to the

Council on the audit of HBRC for the year ended 30 June 2018

|

|

|

|

Report

to the Council on the audit of HBRC for the year ended 30 June 2018

|

Attachment 1

|

HAWKE’S BAY REGIONAL COUNCIL

Finance

Audit & Risk Sub-committee

Tuesday 12 February 2019

Subject: Treasury Report

Reason for Report

1. This

item provides an update on the development of Council’s diversified

investment portfolio and application to join the Local Government Funding

Agency (LGFA).

Background

2. On 26

September 2018 Council resolved to appoint dual fund managers, being Mercer and

First New Zealand Capital. Since that time staff have been working with

both fund managers to get all of the paperwork and signing-on process completed

before funds could be transferred.

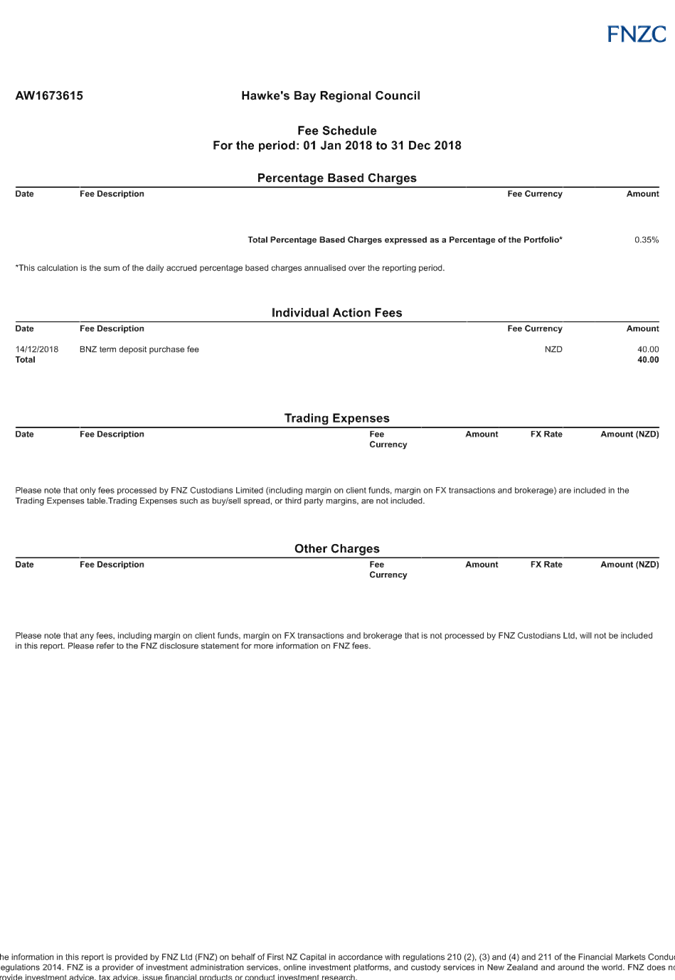

3. First NZ

Capital was the first to finalise and the first transfer of $5,000,000 was made

on 5 December 2018.

4. Mercer

had some suggested minor amendments to the Statement of Investment Policy

Objectives (SIPO) and Treasury Policy to allow for more practical

implementation of the portfolio. These amendments included making reference to

having two investment fund managers, allowing some infrastructure assets in the

growth asset mix and allowing some unhedged equities. The changes did not

impact the overall asset mix or risk profile and had been reviewed by

Council’s Treasury advisors who provided a view that the changes are

consistent with the previous SIPO and minor in nature.

5. These changes

agreed by the Corporate and Strategic Committee on 12 December 2018 and

recommended to Council for adoption on 19 December 2018. Once these

changes were adopted the final sign on documents for Mercer were completed

mid-January. The first transfer of $5,000,000 to Mercer was made on 18

January 2019.

6. Due to

the delays getting the amendments to the SIPO and Treasury Policy adopted, the

distribution of funds to the investment managers drifted out with the

anticipation that the full allocation will take place by the end of February

2019. The table below sets out the anticipated movement of funds.

|

Completed

|

|

|

|

|

Date

|

Mercer

|

First NZ Capital

|

Total

|

|

05/12/18

|

-

|

$5 million

|

$5 million

|

|

18/01/19

|

$5 million

|

$5 million

|

$10 million

|

|

|

|

|

|

|

Proposed

|

|

|

|

|

Date

|

Mercer

|

First NZ Capital

|

Total

|

|

11/02/19

|

$10 million

|

$10 million

|

$20 million

|

|

21/02/19

|

$5 million

|

-

|

$5 million

|

|

|

|

|

|

|

TOTAL

|

$20 million

|

$20 million

|

$40 million

|

7. Forecast

returns could be unfavourably affected by the delays and staff will continue to

update the Sub-committee and full Council on any effects on investment income

and any mitigation that may be required. A full finance report will be

provided to Council on 27 February 2019.

Treasury Reports

8. At the

last sub-committee a draft treasury report was presented for review.

9. Due to

the fact that there were minimal funds invested by the end of the

31 December 2018 quarter, staff have decided to delay the first full

treasury report until meaningful data is available. This will come to the

sub-committee at the next meeting on 22 May 2019.

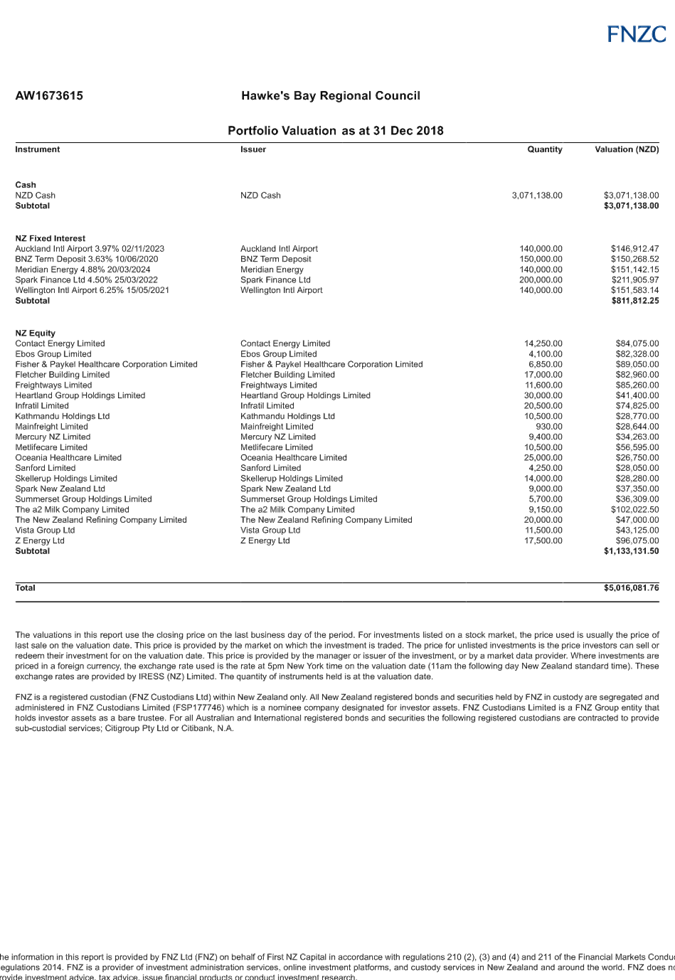

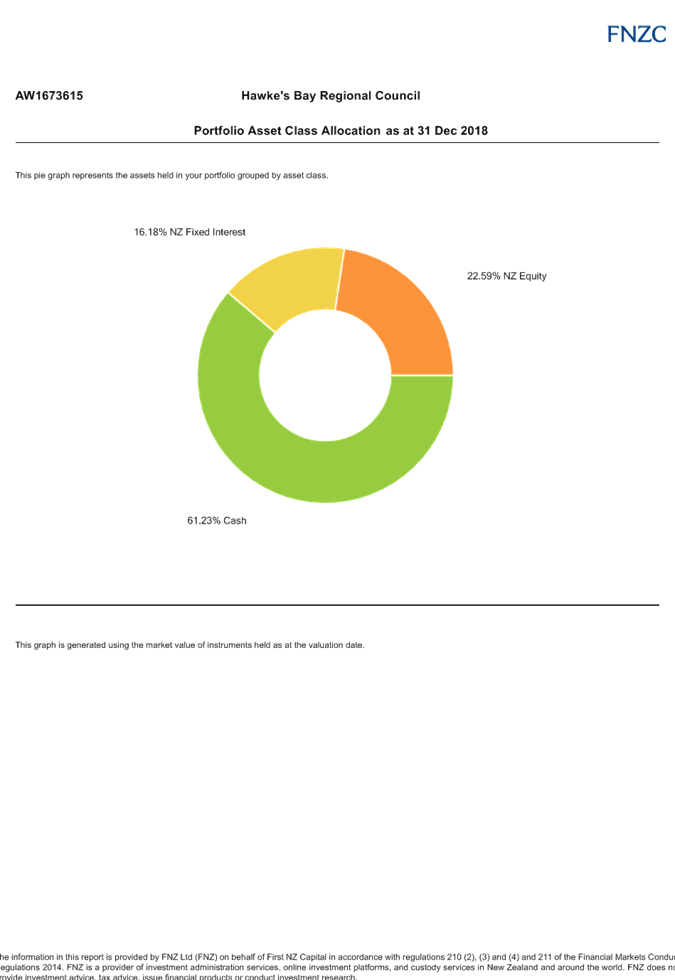

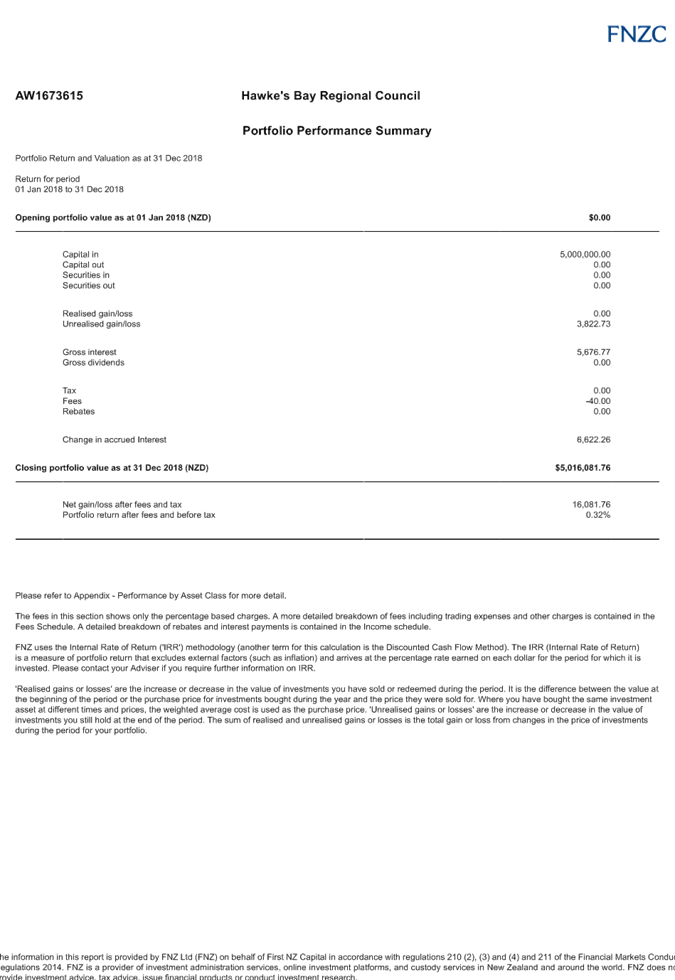

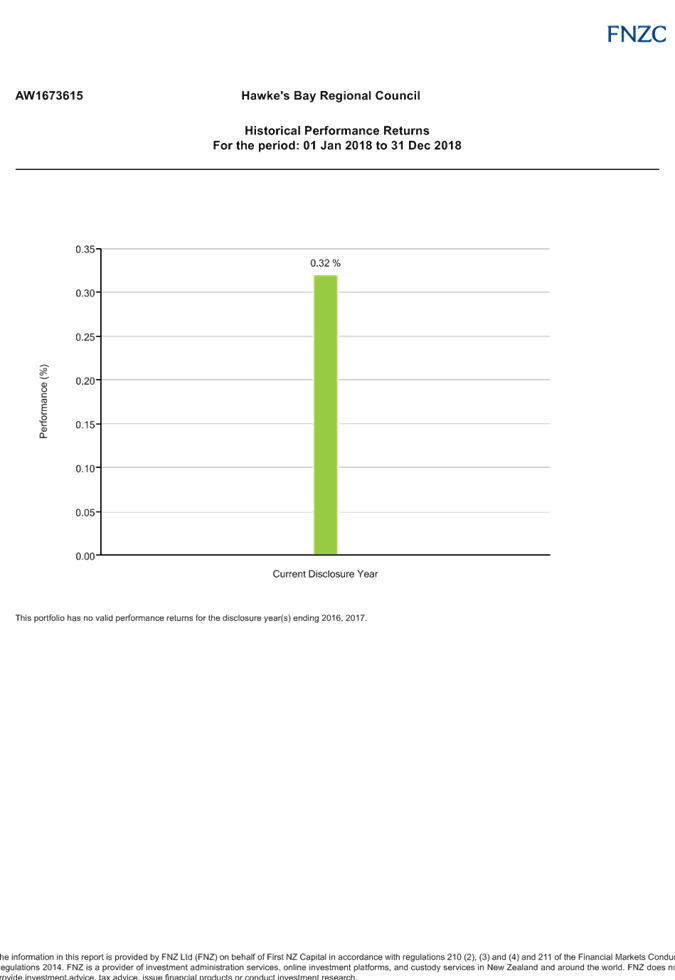

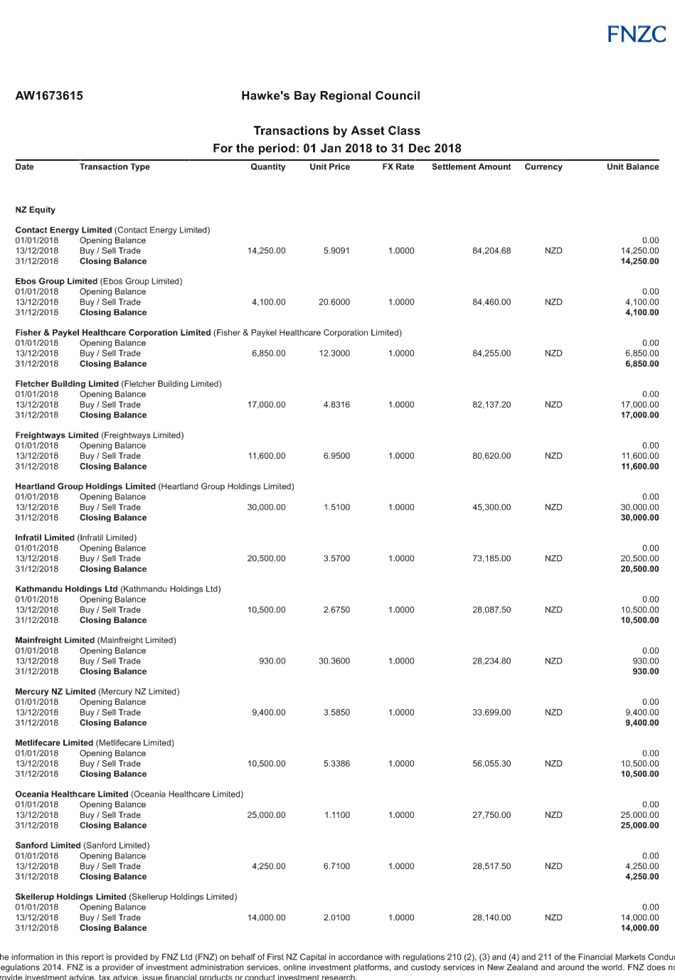

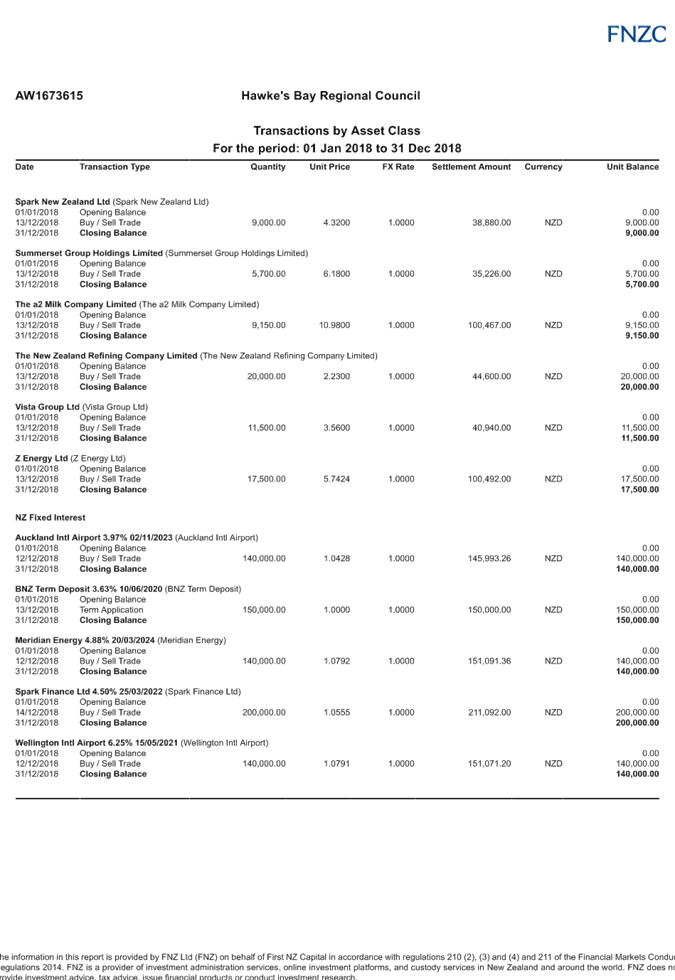

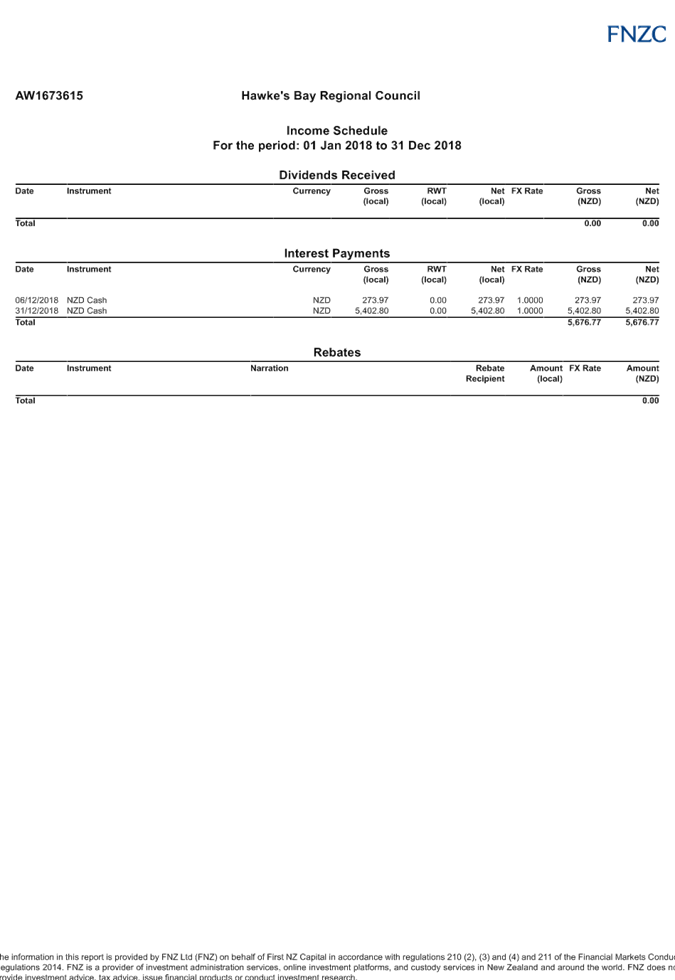

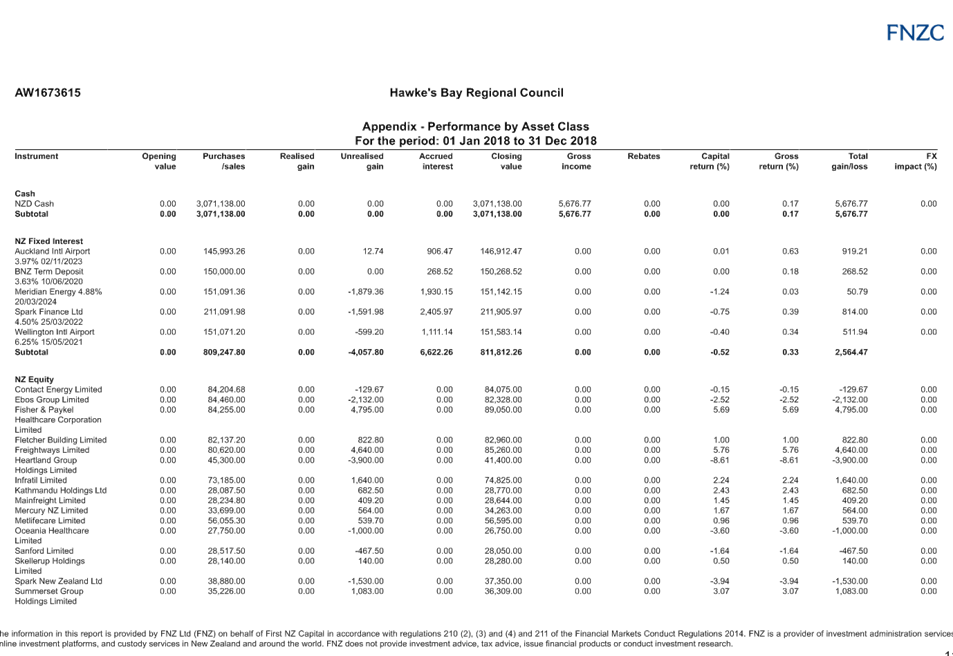

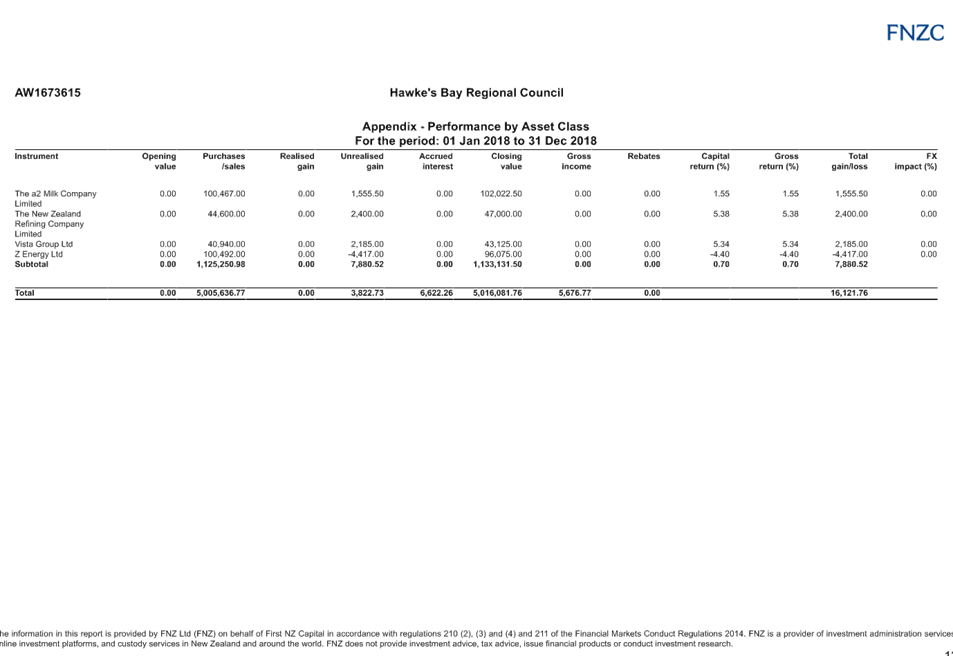

10. Attached is a

detailed quarterly report from First NZ Capital for the $5,000,000 invested

since 5 December 2018. Once full reporting is implemented, future reports will

be wrapped up into a summary version.

Joining LGFA

11. Authority to

execute all of the documentation for joining the LGFA was resolved by Council

on 19 December 2018 and staff are working alongside Council’s solicitors

to complete all of the documentation. It is anticipated that this transaction

will be completed by the end of February 2019.

Decision Making

Process

12. Staff

have assessed the requirements of the Local Government Act 2002 in relation to

this item and have concluded that as this report is for information only, the

decision making provisions do not apply.

|

Recommendation

That the Finance Audit and Risk

Sub-committee receives and notes the “Treasury Report”.

|

Authored by:

|

Manton

Collings

Chief Financial Officer

|

|

Approved by:

|

Jessica

Ellerm

Group Manager

Corporate Services

|

|

Attachment/s

|

⇩1

|

FNZC report

dated 31 December 2018

|

|

|

|

FNZC

report dated 31 December 2018

|

Attachment 1

|

|

FNZC

report dated 31 December 2018

|

Attachment 1

|

HAWKE’S BAY REGIONAL

COUNCIL

Finance

Audit & Risk Sub-committee

Tuesday 12 February 2019

Subject: Resource Management

Information System (IRIS) Implementation Update

Reason for Report

1. To provide an update on progress with the implementation of the new

Resource Management Information System software (IRIS).

Milestones and Progress Update

2. The Business Case for the system implementation was approved on 28

June 2017 and expenditure was confirmed in the LTP.

3. Phase 1 of the project is on schedule and will close on 31 March

2019.

3.1. Consents and Compliance modules went live on 26 November 2018, in

line with the revised forecasts received by this committee on 6 June 2018

3.2. Incidents and Enforcements modules are on schedule, and will

‘go live’ on 11 February 2019

3.3. The Water Information Services module has been deferred to Phase 2.

This was to avoid potential disruption to services over the high risk weather

period (November – April)

3.4. A lessons learnt workshop will be held in mid-February and learnings

from this phase will be used in the planning and implementation of Phase 2.

Next Steps

4. Phase 2 of the project will soon be initiated. This will deliver

modules for Biosecurity, Integrated Catchment Management and Water Information

Systems (moved from Phase 1). The LTP includes the following provisions for

Phase 2.

4.1. 2018-19: $650,000

4.2. 2019-20: $350,000

4.3. $600,000 of the cost is the capitalisation of internal labour, the

remaining $400,000 is for external implementation services.

5. The following steps will be undertaken to validate the budget

figures.

5.1. Review the business requirements in light of the changes to the

organisation structure, especially the Integrated Catchment Management

functions

5.2. Finalise the scope of engagement with external suppliers

5.3. Confirm internal resourcing requirements

5.4. Identify any improvements arising from Phase 1 that need to be

addressed

5.5. Any significant budget variation brought back to Council for

approval.

6. Staff are confident that there is no need to revisit our sourcing

approach, because:

6.1. The initial RMIS selection explicitly included the Phase 2 functions

and capabilities (Biosecurity and Land Management). The IRIS product was rated

favourably in these areas compared to others.

6.2. IRIS has been specifically developed for Regional Council functions

by a consortium of other regional councils. HBRC has similar needs to the other

regional councils, so should be able to leverage the base functionality

available.

6.3. Introducing alternative products or solutions for the Phase 2

functions would increase the complexity and cost of IT support and

integrations.

Decision Making Process

7. Staff have assessed the requirements of the Local Government Act

2002 in relation to this item and have concluded that, as this report is for

information only, the decision making provisions do not apply.

|

Recommendation

That the

Finance, Audit & Risk Sub-committee receives and notes the “Resource

Management Information System Implementation Update” report.

|

Authored by:

|

Andrew

Siddles

Acting ICT Manager

|

|

Approved by:

|

Jessica

Ellerm

Group Manager

Corporate Services

|

|

Attachment/s

There are no

attachments for this report.

HAWKE’S BAY REGIONAL

COUNCIL

Finance

Audit & Risk Sub-committee

Tuesday 12 February 2019

Subject: February 2019

Sub-committee Work Programme Update

Reason for Report

1. In order to ensure the sub-committee’s ability to effectively

and efficiently fulfill its role and responsibilities, an overall update on its

work programme is provided following.

2. It should be noted that some non-urgent items in the work programme

have been deferred due to current staff resourcing and capacity restraints. We

have now successfully recruited for and appointed a Financial Accountant who

commenced employment on 19 November 2018. This additional senior resource

will provide much needed capacity to make good progress on a substantive work

programme for this team.

|

Task

|

Item

|

Scheduled / Status

|

|

Internal

Audits

|

Health &

Safety

|

Presented to

21 November 2018 FARS meeting.

|

|

Data

Analytics

|

Presented to

12 February FARS meeting.

|

|

Business

Continuance

|

Deferred to

future 2019-20 programme.

|

|

Water

Management

|

Scope to be

agreed at 12 February FARS meeting to be presented to 22 May FARS meeting.

|

|

Risk

Assessment & Management

|

Reporting on risks

(6-monthly) affecting Council plus noting changes / improvements / areas that

require attention from last report (3-monthly).

|

Presented to

19 September 2018 and 12 February meeting.

Risk

management now a monthly item on Executive agenda and action register now

implemented.

|

|

Insurance

|

Council’s

proposed 2018-19 Insurance programme.

|

Reported to

6 June 2018 FARS meeting next update to 22 May FARS meeting subject to

timing.

|

|

Annual

Report

|

Discussion on Audit

Management Letter.

Discussion

on the major issues (if any) in the audit report on the Annual Report.

|

Audit

Director attended 21 November 2018 FARS meeting to discuss Annual Report

process.

|

|

S17a Efficiency

Reviews (Section 17a Local Government Act)

|

Update on progress and

findings of Section 17a Efficiency Reviews.

|

No reviews

scheduled in Q1&2 of Year 1 of LTP (Long Term Plan).

Q3 has Open

Spaces and Surface Water Science reviews planned. Q4 has Fleet review

planned.

Staff member

regularly attends Hawke’s Bay Council wide S17a Review collaboration

meetings where opportunities for cost sharing are discussed.

|

|

Investment

Returns & Treasury Monitoring

|

Update on progress in

obtaining required level of dividend from PONL (Port of Napier Limited).

Update on Treasury function within Council.

|

HBRIC Ltd

2018-19 SoI (Statement of Intent) adopted at 27 June 2018 Council

meeting.

SIPO

(Statement of Investment Policy & Objectives) adopted at 27 June 2018

Council meeting. Amendment made to SIPO and Treasury Policy 19 December 2018

Council meeting.

Fund

managers appointed at 26 September Council meeting, updates now captured

within treasury report.

Application

to join LGFA (Local Government Funding Agency) underway.

|

|

Living Wage

|

Procurement and

Contract Management

|

Staff are

currently undertaking a review of supplier contracts and will perform an

exercise to quantify the financial impact of enforcing a procurement policy

which requires suppliers to pay the Living Wage.

The findings

of this will be presented at 22 May FARS meeting, alongside an update on the

PTOM (Public Transport Operating Model) review.

|

Decision Making

Process

3. Staff have assessed the requirements of the Local Government Act

2002 in relation to this item and have concluded that, as this report is for

information only, the decision making provisions do not apply.

|

Recommendation

That the Finance, Audit and Risk

Sub-committee receives and notes the “February 2019 Sub-committee

Work Programme Update” staff report.

|

Authored by:

|

Melissa des

Landes

Corporate Accountant

|

|

Approved by:

|

Jessica

Ellerm

Group Manager

Corporate Services

|

|

Attachment/s

There are no

attachments for this report.

HAWKE’S BAY REGIONAL COUNCIL

Finance

Audit & Risk Sub-committee

Tuesday 12 February 2019

SUBJECT: Confirmation

of the Public Excluded Minutes of the Finance, Audit and Risk Sub-committee

Meeting held on 21 November 2018

That the Council excludes the public

from this section of the meeting being Confirmation of Public Excluded Minutes

Agenda Item 13 with the general subject of the item to be considered while the public

is excluded; the reasons for passing the resolution and the specific grounds

under Section 48 (1) of the Local Government Official Information and Meetings

Act 1987 for the passing of this resolution being:

|

|

GENERAL SUBJECT OF THE ITEM TO BE

CONSIDERED

|

REASON FOR PASSING THIS RESOLUTION

|

GROUNDS UNDER SECTION 48(1) FOR THE

PASSING OF THE RESOLUTION

|

|

Appointment of an Independent Member of

the Finance, Audit & Risk Sub-Committee

|

7(2)(a) That the public conduct of this

agenda item would be likely to result in the disclosure of information

where the withholding of the information is necessary to protect the

privacy of natural persons

|

The Council is specified, in the First

Schedule to this Act, as a body to which the Act applies.

|

|

Authored by:

|

Leeanne

Hooper

Principal Advisor Governance

|

|

Approved by:

|

James Palmer

Chief Executive

|

|