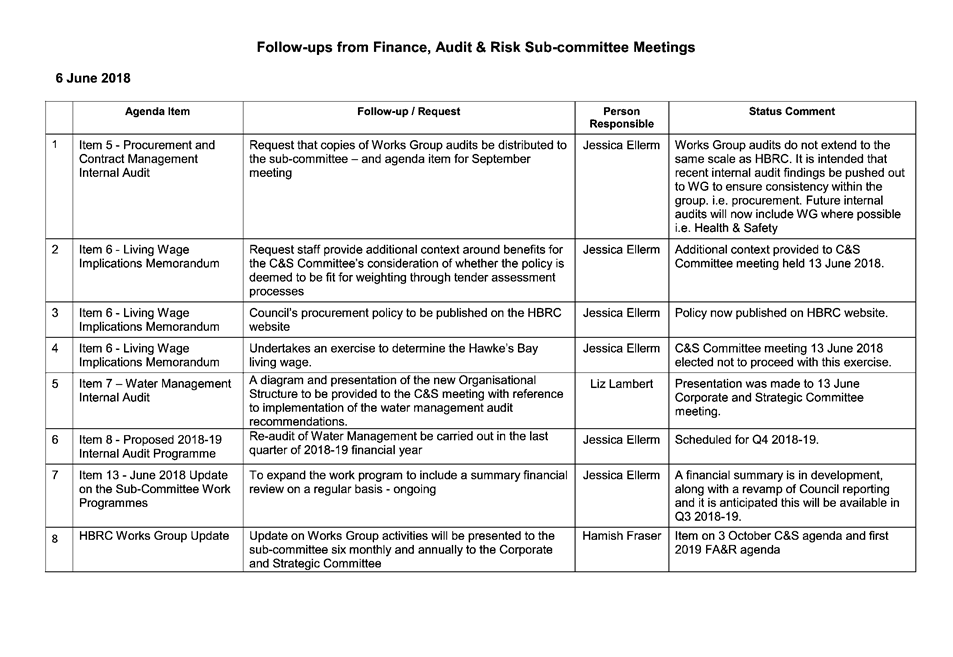

Meeting of the Finance Audit & Risk Sub-committee

Date: Wednesday 21 November 2018

Time: 9.00am

|

Venue:

|

Council Chamber

Hawke's Bay Regional Council

159 Dalton Street

NAPIER

|

Agenda

Item Subject Page

1. Welcome/Notices/Apologies

2. Conflict

of Interest Declarations

3. Confirmation of

Minutes of the Finance Audit & Risk Sub-committee meeting held on 19

September 2018

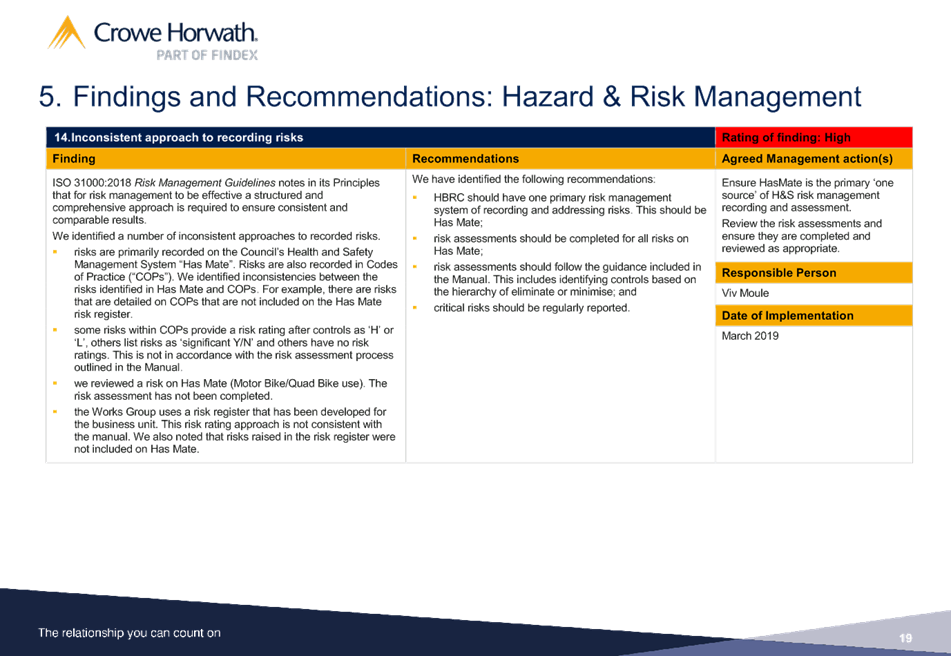

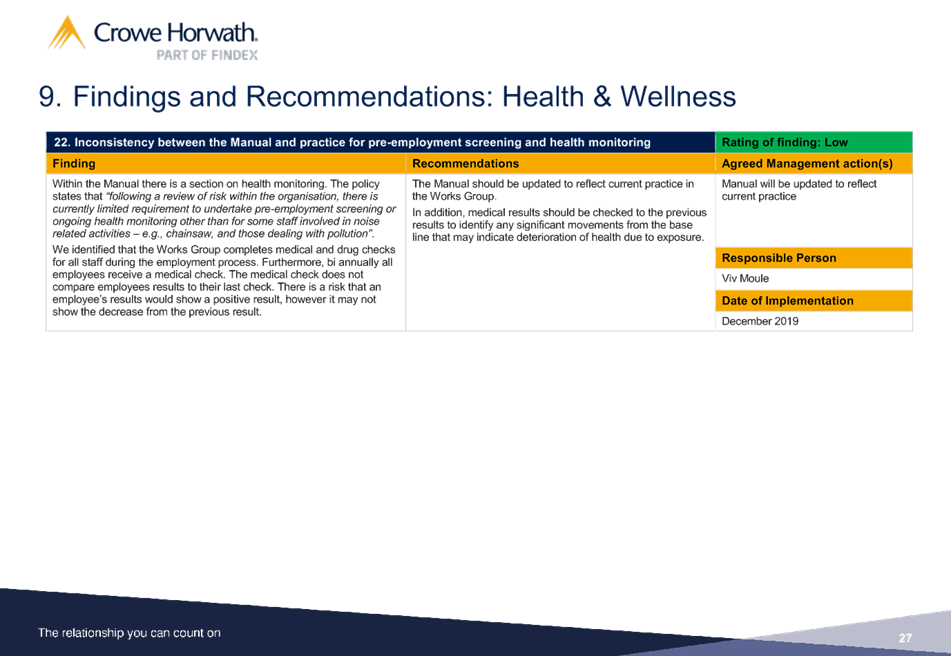

4. Follow-ups from

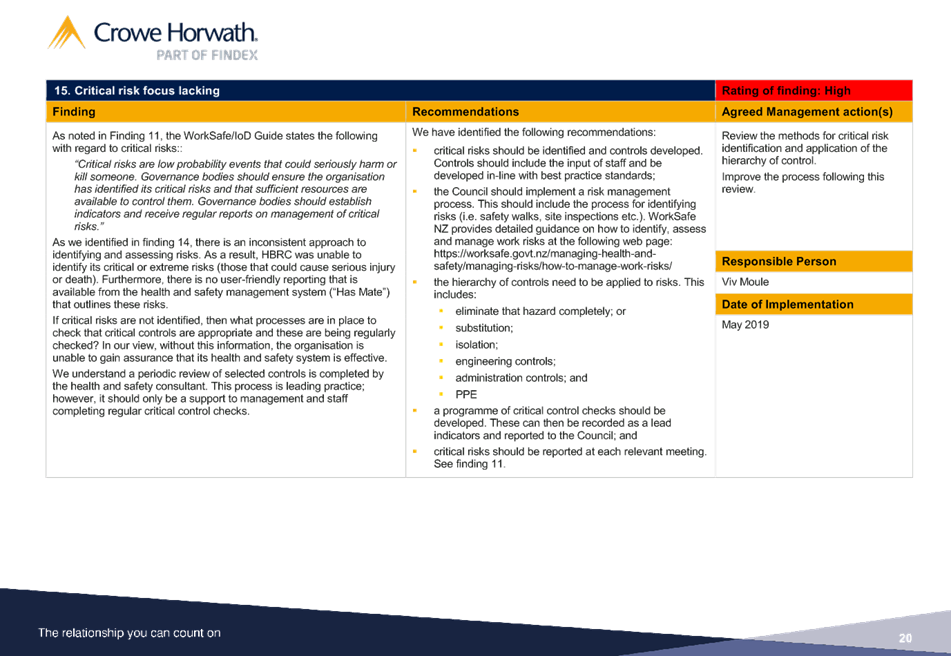

Previous Finance Audit & Risk Sub-committee Meetings 3

Decision Items

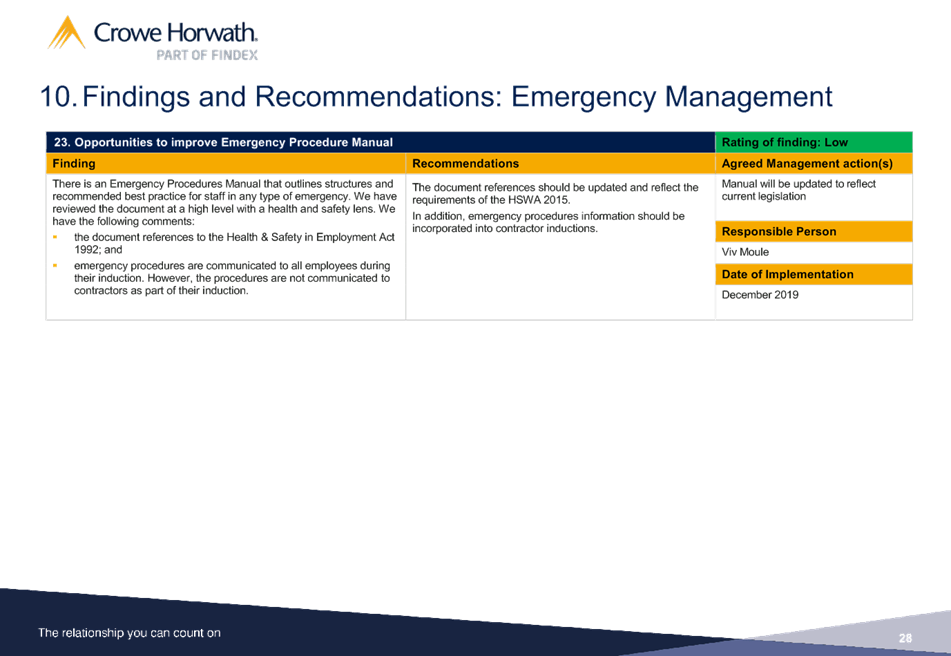

5. Local Government

Funding Agency Accession 7

Information or Performance Monitoring

6. Health &

Safety Internal Audit Report 9

7. Internal Audit

Update 51

8. Treasury Update 53

9. November 2018

Sub-committee Work Programme Update 67

Decision Items (Public Excluded)

10. Appointment of an Independent

Member of the Finance, Audit & Risk Sub-Committee 69

HAWKE’S BAY REGIONAL COUNCIL

Finance

Audit & Risk Sub-committee

Wednesday 21 November 2018

SUBJECT: Follow-ups from Previous Finance Audit

& Risk Sub-committee Meetings

Reason for Report

1. In order to track items raised at previous meetings that require

follow-up, a list of outstanding items is prepared for each meeting. All

follow-up items indicate who is responsible for each, when it is expected to be

completed and a brief status comment. Once the items have been completed and

reported to the Committee they will be removed from the list.

Decision

Making Process

2. Council is required to make every decision in

accordance with the Local Government Act 2002 (the Act). Staff have assessed

the in relation to this item and have concluded that as this report is for

information only and no decision is required, the decision making procedures

set out in the Act do not apply.

|

Recommendation

That the Finance, Audit and Risk Sub-committee receives

and notes the report “Follow-ups from Previous Finance Audit and

Risk Sub-committee Meetings”.

|

Authored by:

|

Melissa des

Landes

Corporate Accountant

|

|

Approved by:

|

Jessica

Ellerm

Group Manager Corporate Services

|

|

Attachment/s

|

⇩1

|

Follow-ups from

Previous FA&RS meetings

|

|

|

|

Follow-ups

from previous FA&RS meeting

|

Attachment 1

|

HAWKE’S BAY REGIONAL COUNCIL

Finance

Audit & Risk Sub-committee

Wednesday 21 November 2018

Subject: Local Government

Funding Agency Accession

Reason for Report

1. This report

seeks to authorise the taking of all necessary steps to give effect to

Council’s accession to Local Government Funding Agency (LGFA) as an

unrated guaranteeing Local Authority.

Background

2. As part of its

2018-2028 Long Term Plan consultation, Council resolved to join LGFA as an

unrated guaranteeing Local Authority.

3. In order to

accede to LGFA, Council must make a formal resolution to join and execute the

following legal documents.

3.1. Deed of

Amendment and Restatement of Debenture Trust Deed

3.2. Section 118

Chief Executive Certificate in relation to the abovementioned document

3.3. Letter from

Council to Computershare Investor Services Limited (to amend and restate

Council’s 21 October 2009 Registrar and Paying Agent Services Agreement);

3.4. Accession

Deed to Multi-Issuer Deed

3.5. Accession

Deed to Notes Subscription Agreement

3.6. Accession

Deed to Equity Commitment Deed

3.7. Accession

Deed to Guarantee and Indemnity

3.8. Security

Stock Certificate (in relation to the Multi-Issuer Deed)

3.9. Security

Stock Certificate (in relation to the Equity Commitment Deed)

3.10. Security Stock

Certificate (in relation to the Guarantee)

3.11. Stock Issuance

Certificate (in relation to the documents noted at 3.8. – 3.10.)

3.12. Section 118 Chief

Executive Certificate (in relation to the documents noted at 3.4. –

3.11.), and

3.13. Officer’s

Certificate.

4. The documents

at 3.1. – 3.3. and 3.8. – 3.12. are being drafted by

Council’s solicitors, Simpson Grierson, and the documents at 3.4. –

3.7. and 3.13. will be reviewed and approved by Council’s solicitors

prior to their execution. Simpson Grierson has extensive LGFA accession

experience with other Local Authorities.

5. Council staff

are requesting that authority for signing the abovementioned documents be

delegated to (as relevant) two elected members of Council and the Chief

Executive.

Decision Making

Process

6. Council and its committees are required to make every decision in

accordance with the requirements of the Local Government Act 2002 (the Act).

Staff have assessed the requirements in relation to this item and have

concluded:

6.1. The decision does not significantly alter the service provision or

affect a strategic asset.

6.2. The use of the special consultative procedure is not prescribed by

legislation.

6.3. The decision does not fall within the definition of Council’s

policy on significance.

6.4. The decision is not inconsistent with an existing policy or plan.

6.5. Given the nature and significance of the issue to be considered and

decided, and also the persons likely to be affected by, or have an interest in

the decisions made, Council can exercise its discretion and make a decision

without consulting directly with the community or others having an

interest in the decision.

|

Recommendations

1. That the Finance, Audit and Risk Sub-committee:

1.1. receives

the Local Government Funding Agency (LGFA) Accession staff report, and

1.2. notes the

contents of that report.

2. The Finance, Audit and Risk Sub-committee

recommends that Hawke’s Bay Regional Council:

2.1. Confirms

Council’s intention to join the Local Government Funding Agency as an

unrated guaranteeing Local Authority.

2.2. Delegates

authority to the Chief Executive to execute the following documents for the

purposes of recommendation 2.1. above:

2.2.1. Letter

from Council to Computershare Investor Services Limited (to amend and restate

Council’s 21 October 2009 Registrar and Paying Agent Services

Agreement)

2.2.2. Security

Stock Certificate (in relation to the Multi-Issuer Deed)

2.2.3. Security

Stock Certificate (in relation to the Equity Commitment Deed)

2.2.4. Security

Stock Certificate (in relation to the Guarantee); and

2.2.5. Stock

Issuance Certificate (in relation to the documents noted at recommendation 2.2.2. – 2.2.4.).

2.3. Authorises

Council’s elected members, Chairman Rex Graham and Deputy Chairman Rick

Barker, to execute the following deeds for the purposes of recommendation 2.1

above:

2.3.1. Deed of

Amendment and Restatement of Debenture Trust Deed

2.3.2. Accession

Deed to Multi-Issuer Deed

2.3.3. Accession

Deed to Notes Subscription Agreement

2.3.4. Accession

Deed to Equity Commitment Deed, and

2.3.5. Accession

Deed to Guarantee and Indemnity.

2.4. Delegates

authority to the Chief Executive to execute such other documents and take

such other steps on behalf of Council as the Chief Executive considers it is

necessary or desirable to execute or take to give effect to recommendation

2.1 above.

|

Authored by: Approved

by:

|

Melissa des

Landes

Corporate Accountant

|

Jessica

Ellerm

Group

Manager Corporate Services

|

Attachment/s

There are no

attachments for this report.

HAWKE’S BAY REGIONAL COUNCIL

Finance

Audit & Risk Sub-committee

Wednesday 21 November 2018

Subject: Health & Safety

Internal Audit Report

Purpose of Report

1. To present the internal audit report and proposed work programme for

Health & Safety (H&S) within Council.

Background

2. The Finance, Audit and Risk Sub-committee (FARS) included Health

& Safety as part of the internal audit work programme for 2018-19 and

agreed to the scope (attached) on 6 June 2018.

3. It is important to note that the scope of the review was process

based in nature, and as such, findings were conducted primarily through

interviews with staff, review of policies and relevant systems and

documentation. Field work was not part of the agreed scope of the review.

4. The report was originally planned to be presented at a previous FARS

meeting, however due to the HR Manager’s absence, this report was

deferred until this meeting.

5. Staff have reviewed the findings in detail, and have proposed a work

programme to enact findings from the review. These findings have also been

presented and discussed at two Executive Leadership Team (ELT) meetings due to

the critical importance of this review.

6. The audit report, with management commentary provided against

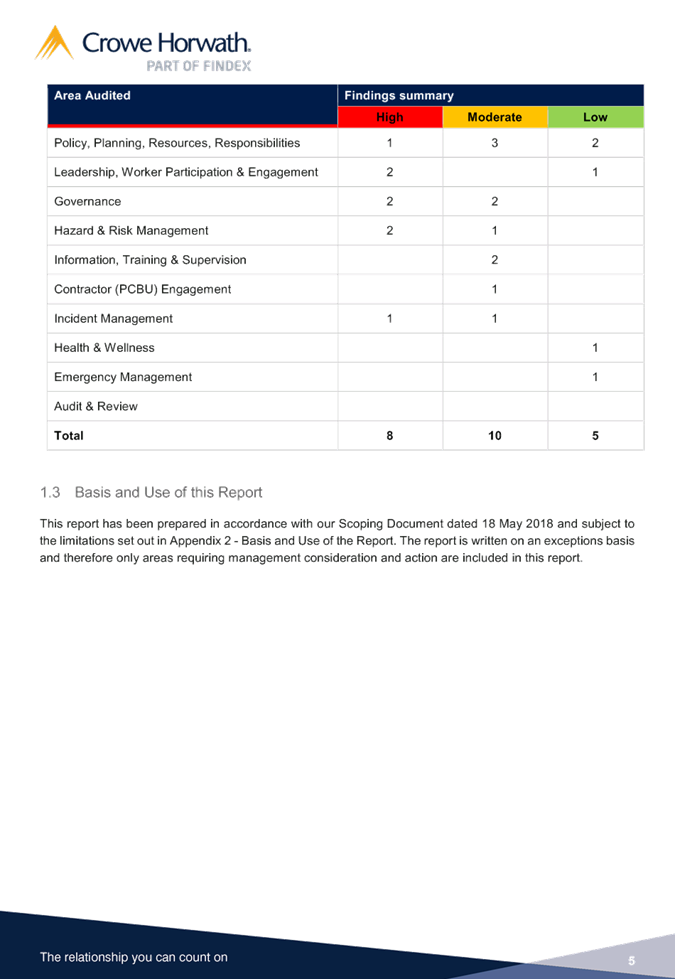

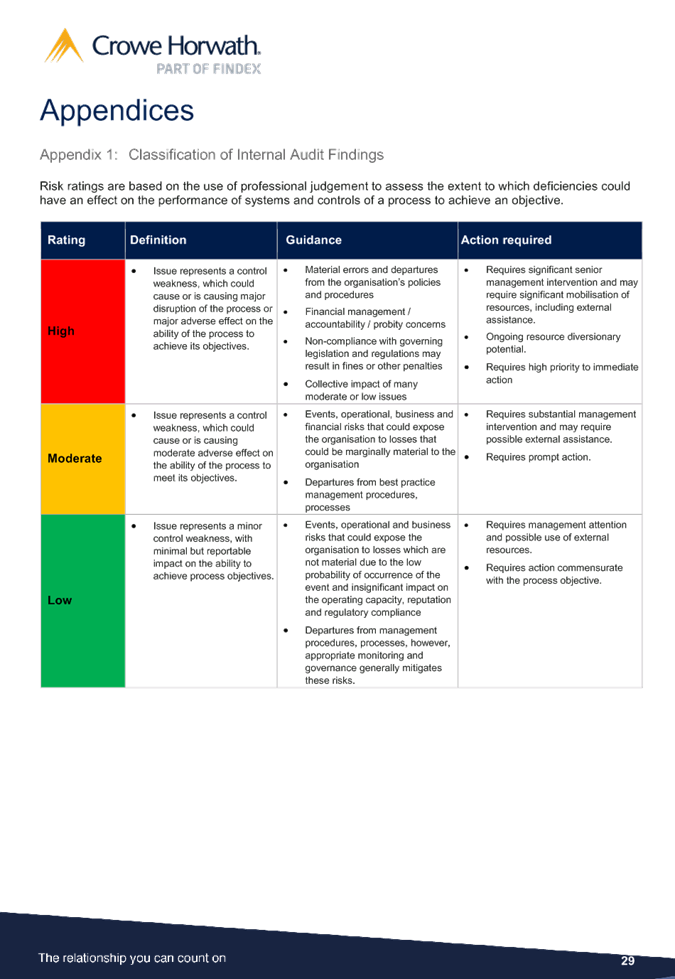

recommendations, is attached. For ease of reference, an analysis of high risk

findings is also outlined in ‘Report Analysis’ section below.

7. Jeffrey Broughton, Audit Manager for Crowe Horwath will attend the

FARS meeting to answer any relevant questions on the review.

Report Analysis

8. To provide context for the report it is important to acknowledge

comments made in the Executive Summary of the report under

‘Findings’.

9. The report indicates that, “It is important to note that

our findings are written on an exception basis, there were many examples of

good practice within the Council” and further,

9.1. “Throughout our review, it was clear that staff were engaged

in health and safety and truly understood its importance. This is often the

hardest pieces of the puzzle to develop and provides a strong foundation to

implement the findings in our report. The Council has also engaged an external

health and safety consultant which has resulted in several good practice documents

being in place.”

10. To assist

Councillors with a summary of the review’s key findings rated

‘high’, a brief outline is provided below.

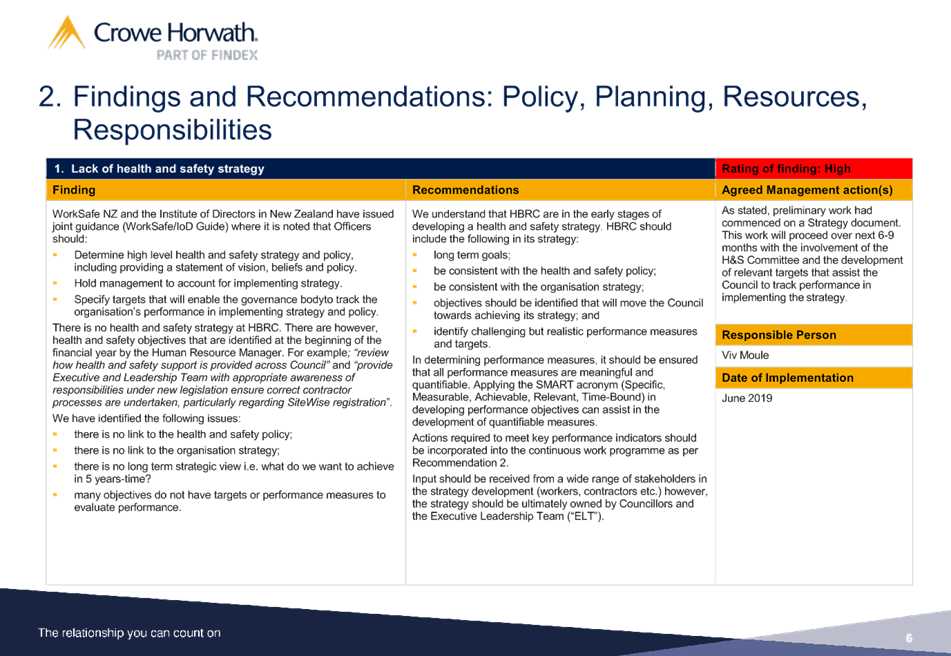

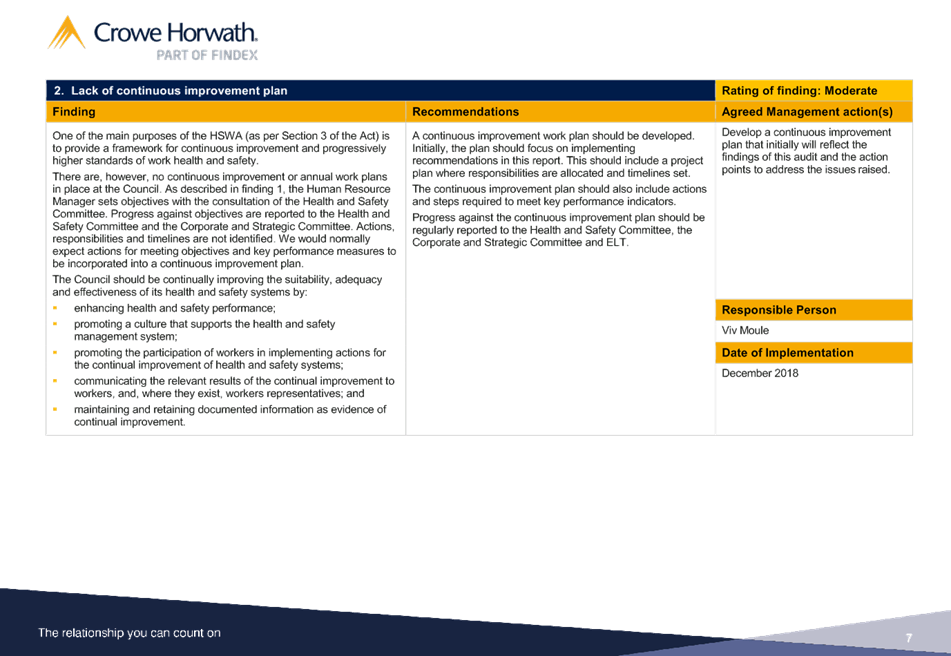

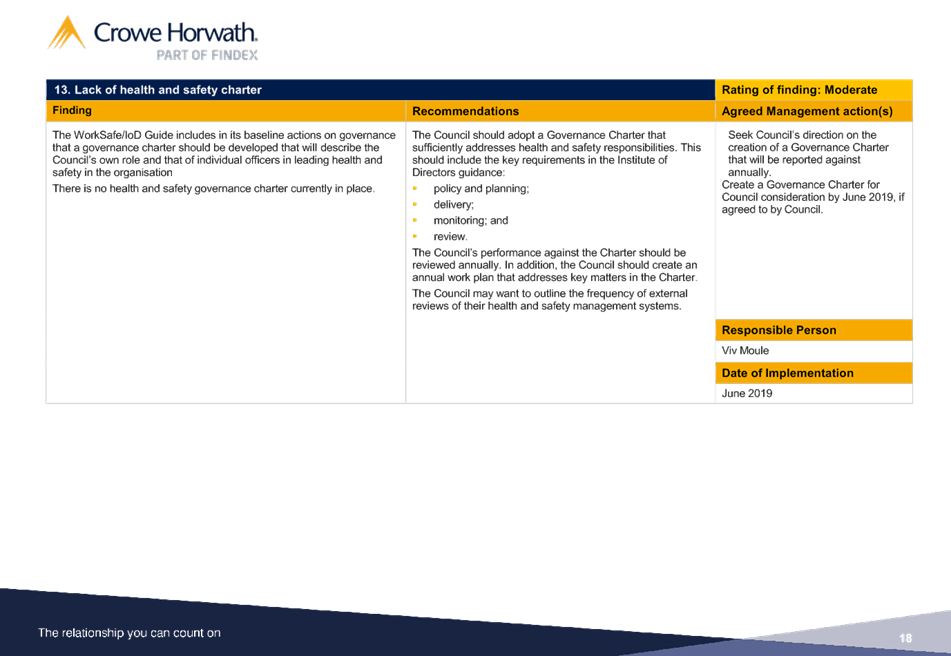

Lack of Health

and Safety Strategy (Report

page 6/ and Finding clause number 1)

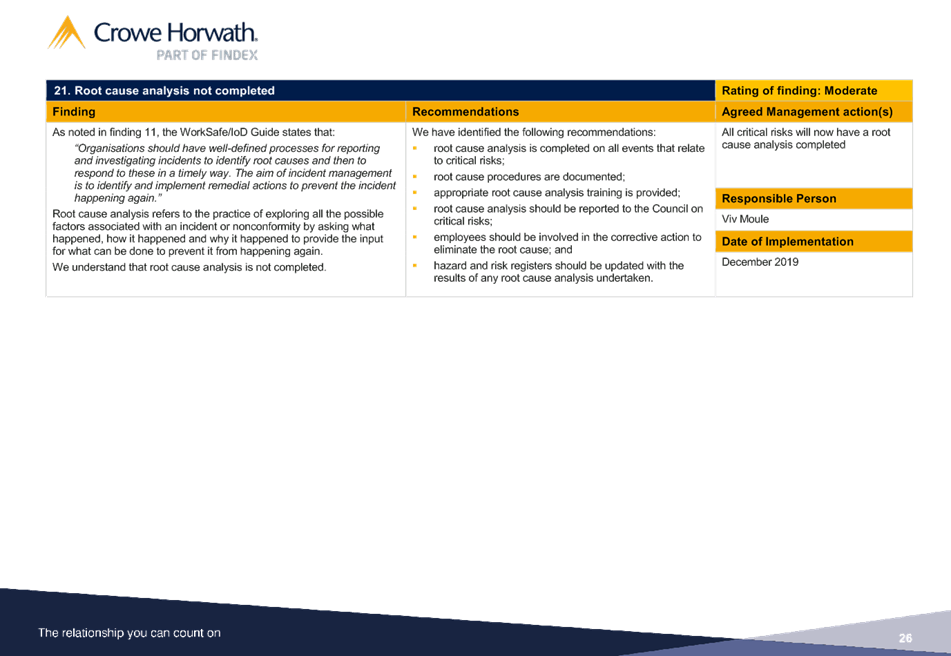

11. The

report advocates the development of a Strategic Plan that outlines the longer

term goals the Council wants to achieve over the next 3-5 years. This should be

linked to the H&S policy and the Council’s overall strategic

objectives. Development of the plan should involve a range of stakeholders, but

is ultimately ‘owned’ by the ELT and Councillors.

12. The

report acknowledged that work had commenced on developing a Strategic Plan.

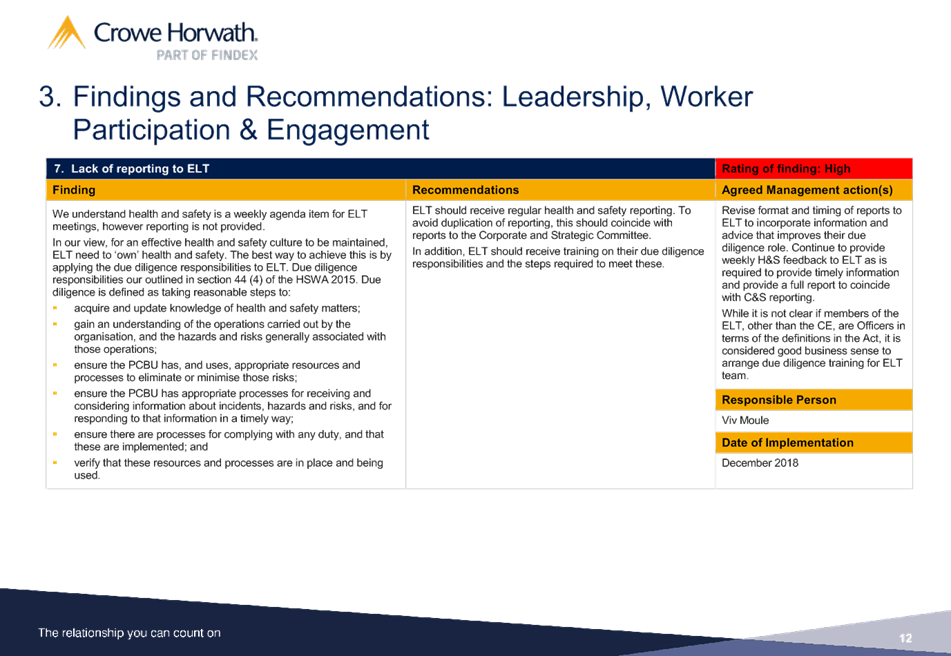

Lack of

reporting to ELT (pg

12/ cl 7)

13. The

report recommends better reporting of issues presented to, and/or discussed by,

the ELT and ensuring this meets the due diligence requirements of the ELT. The

report advocates regular reports to the ELT and documentation of discussions

and decisions resulting from the reports. The audit report suggests that an H&S

report to the ELT could coincide with the H&S report to the Council

Corporate & Strategic Committee, notwithstanding other H&S discussions

that happen at ELT meetings as the need arises.

14. The

report also recommends that the ELT undertakes due diligence training to

reinforce their responsibilities under the legislation.

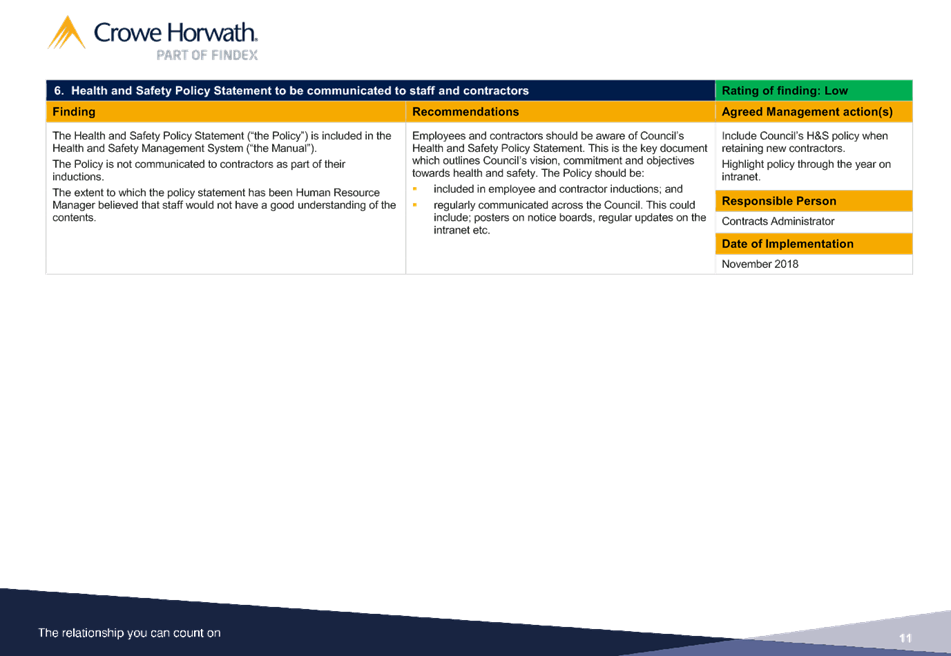

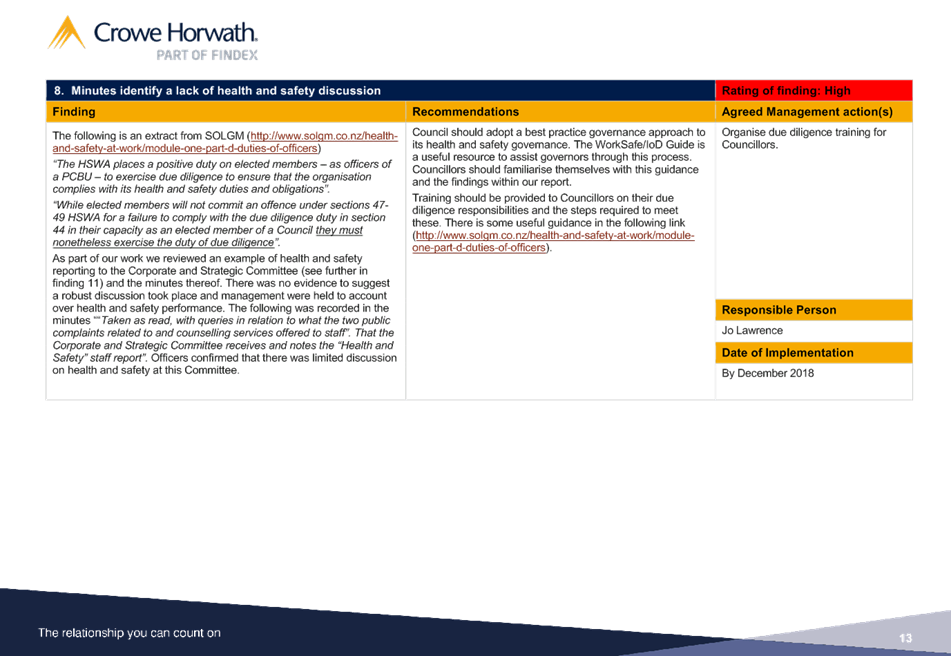

Minutes identify

a lack of health and safety discussion (pg 13/ cl 8)

15. The

report also identified that in Council meetings, “that there was no

evidence to suggest a robust discussion took place and management were held to

account over health and safety performance.” The audit felt that

Councillor due diligence training would be beneficial and lead to improved

debate and reporting.

Gaps in

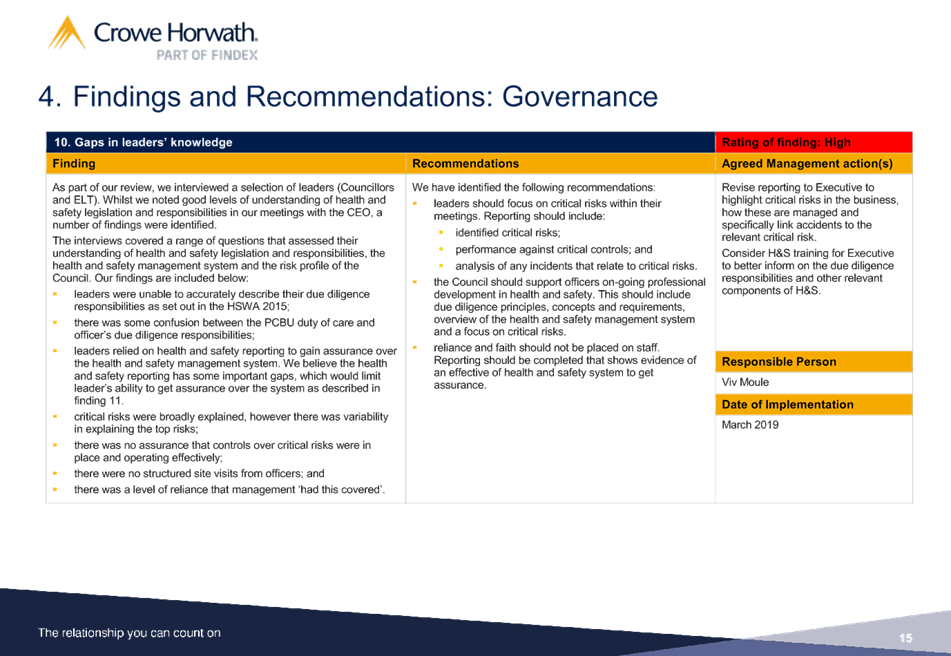

leader’s knowledge (pg

15/ cl 10)

16. Following

interviews with several senior staff and councillors, the report concluded that

the ELT should focus on critical risks and H&S performance associated with

the controls for those risks. Incidents should be investigated in terms of the

critical risk they are associated with to further improve the controls in

place. The report recommended training for the ELT to improve their knowledge

of due diligence and ways to clearly identify an effective H&S system.

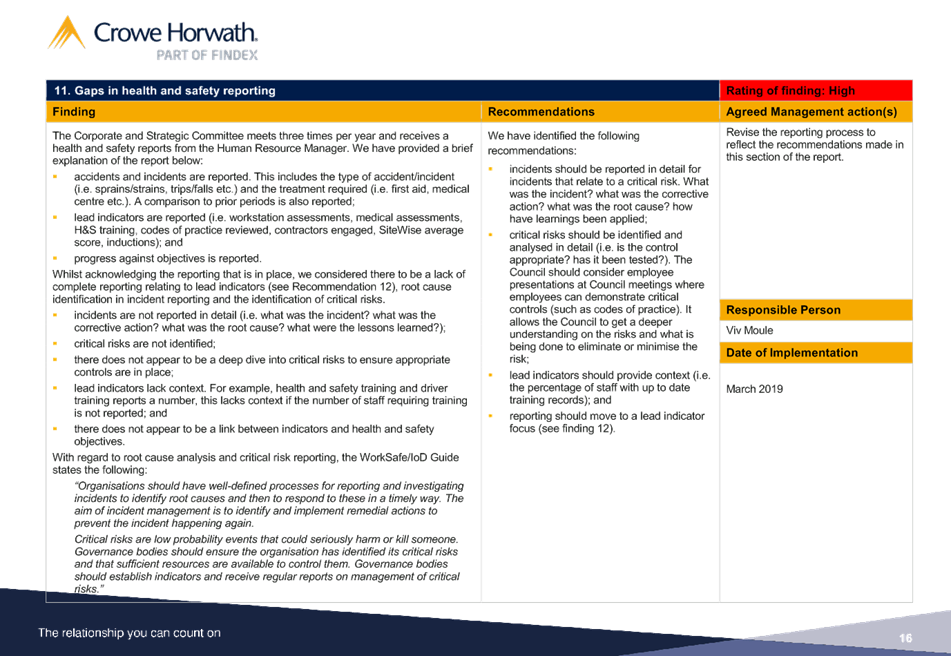

Gaps in H&S

reporting (pg 16/ cl 11)

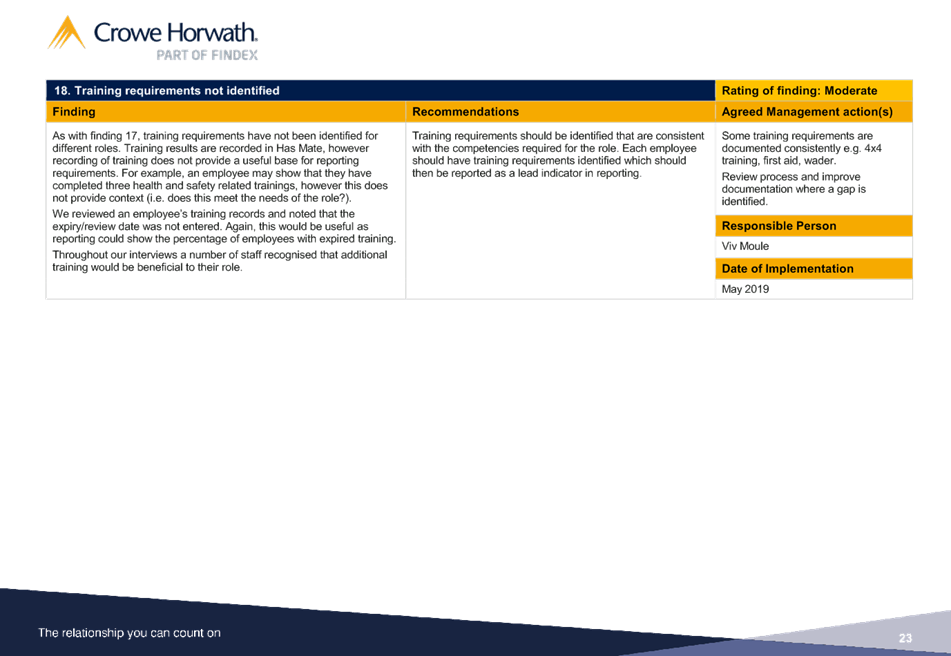

17. This

section reinforces the need to identify critical risk and ensure incident

reporting relates to those critical risks in more detail e.g. what happened, is

the control appropriate, what Code of Practice is in place, is it relevant and

being followed etc. This helps the ELT develop a deeper understanding of the

critical risks.

18. The

report also advocates the development of ‘lead’ indicators to

assist with more effective reporting.

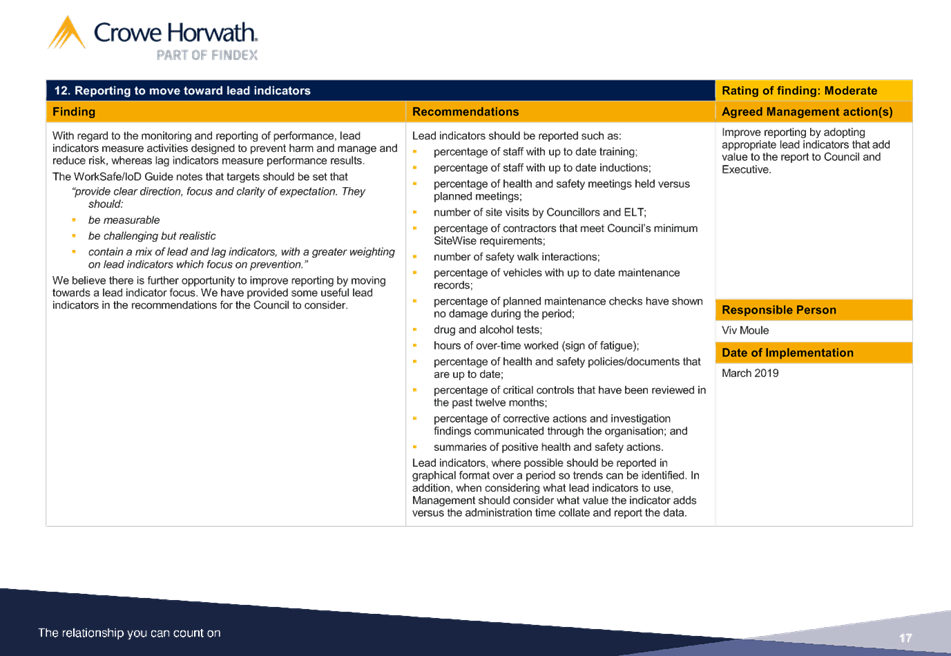

Inconsistent

approach to recording risks (pg 20/ cl 14)

19. This

recommendation related to all risks being recorded in Hasmate (Council’s

workplace health and safety management system), across Council and having risk

assessments completed that are consistent with the process outlined in the

H&S Manual.

Critical risk

focus lacking (pg 21/

cl 15)

20. This

relates to the above recommendation. It reinforces the recommendation to

identify critical risk and develop appropriate controls that address the need

to implement the hierarchy of control as outlined in the Act. It advocates a

programme of critical control checks to improve relevant reporting.

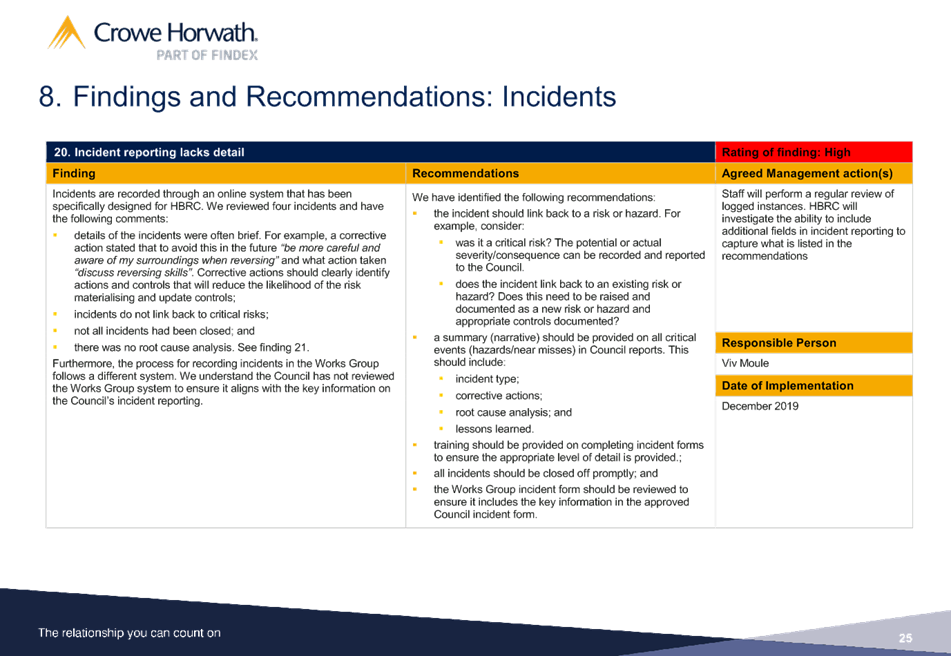

Incident

reporting lacks detail (page

26/ cl 20)

21. This

recommendation relates to the need for more detail when reporting/recording

incidents. This will include any association with a critical risk, potential

consequences, what corrective action is proposed, what lessons have been learnt

and what further training might be required.

22. The

report questioned whether the Works Group should retain a separate reporting

form or adopt the incident reporting form the rest of Council uses.

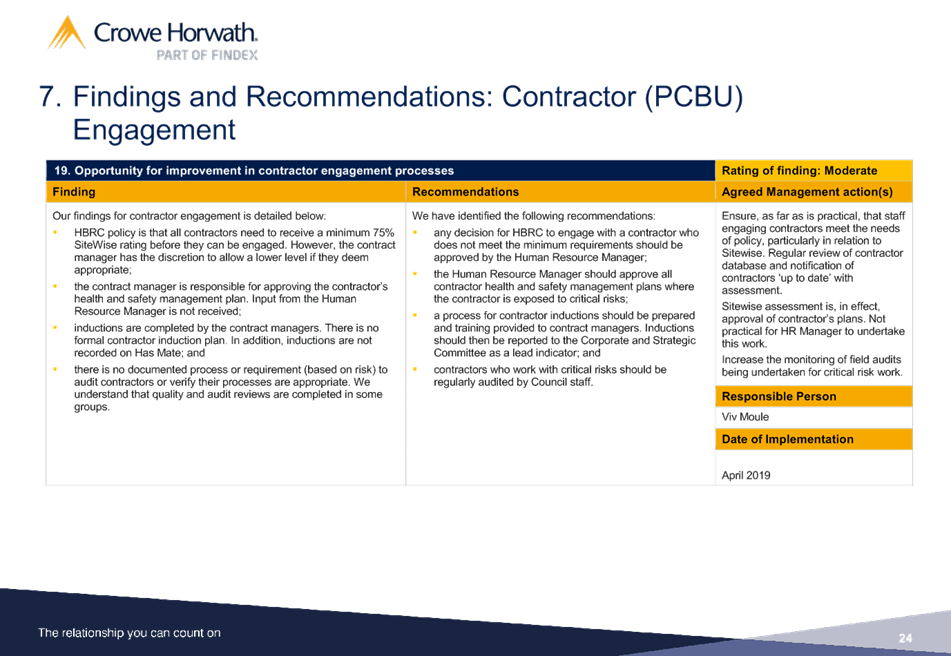

Contractor

Engagement

23. While not

classified as ‘high’ in terms of the audit report rating, the

recommendations on contractor induction are considered a key aspect of the

report that should have priority focus and are included in this section

accordingly.

24. A key

finding, which is considered vital for effective contractor H&S delivery,

is that contractors who work with critical risks should be regularly audited by

Council staff and that auditing should be documented. Improved processes to

ensure this happens, need to be developed.

25. The

report also advocates improved induction of contractors to ensure they are

aware of Council’s H&S requirements, have adequate H&S

documentation and meet the Council’s requirements for Sitewise

registration and assessment.

26. This list

focuses on the high risk and priority areas for Council to action.

Next Steps

27. As a

result of a combination of review recommendations and feedback from the

Executive team, a work programme has been created whereby our external H&S

advisor, Franz Assenmacher, will be responsible for enacting the initial

findings. Franz has been utilised by Council for a considerable number of years

and has vast experience in Health & Safety and associated legislation.

28. The work

programme will have a priority focus on urgent and high risk findings as noted

in Report Analysis section above. Franz is currently contracted on a day a week

basis, it is proposed this his current programme be temporarily increased to

focus on implementation of the findings while maintaining priority areas of his

current work programme.

29. In order

to drive the findings, it is likely that Franz’s time will need to be

utilised at a higher frequency than it is currently. Franz has been provided

with a copy of the draft report and spoken to in anticipation of these

additional requirements and has informally agreed to increase his hours

available to Council. It is anticipated this will take approximately one

month’s work to implement on a part time basis and is likely to cost an

additional estimated $2,000-$3,000 in total.

30. Once high

risk findings have been adhered to, it is proposed that the other lower risk

items and maintenance of findings form part of Franz’s usual work

agreement and will be part of current budgets. This will form part of a

continuous work programme, which is one of the recommendations within the

review.

31. In

conjunction with the above work programme, there will be active engagement with

staff to ensure that Health & Safety is well understood, fully embedded and

fit for purpose. This will include development of internal communications to

staff to support a prevention approach to Health & Safety.

32. Regular

updates on the progress of the Health & Safety work programme will also be provided

to the Executive team and an update will be given to the Corporate &

Strategic Committee in six months’ time.

33. Once the

initial work programme has been implemented and embedded, it is proposed that a

follow up audit be conducted as independent assurance that Council has

responded to the recommendations adequately. This is proposed further in the

“Internal Audit Update” paper at this same meeting.

Decision

Making Process

34. Staff have assessed the

requirements of the Local Government Act 2002 in relation to this item and have

concluded that, as this report is for information only, the decision making

provisions do not apply.

|

Recommendation

That the Finance, Audit and Risk

Sub-committee receives and notes the “Health & Safety

Internal Audit Report”.

|

Authored by:

|

Melissa des

Landes

Corporate Accountant

|

Viv Moule

Human Resources Manager

|

Approved by:

|

Joanne

Lawrence

Group Manager Office of the Chief Executive

and Chair

|

|

Attachment/s

|

⇩1

|

Crowe Horwath

Health & Safety Internal Audit Proposal

|

|

|

|

⇩2

|

Crowe Horwath

Health and Safety Internal Audit Report

|

|

|

|

Crowe

Horwath Health & Safety Internal Audit Proposal

|

Attachment 1

|

|

Crowe Horwath Health and

Safety Internal Audit Report

|

Attachment 2

|

|

Crowe

Horwath Health and Safety Internal Audit Report

|

Attachment 2

|

|

Crowe

Horwath Health and Safety Internal Audit Report

|

Attachment 2

|

HAWKE’S BAY REGIONAL

COUNCIL

Finance

Audit & Risk Sub-committee

Wednesday 21 November 2018

Subject: Internal Audit Update

Reason for Report

1. To provide the Sub-committee with an update on the status of

previous and pending internal audits conducted by internal audit provider,

Crowe Horwath.

Background

2. At its meeting on 6 June 2018, the Sub-committee agreed that the

internal audit work programme for the 2018-19 financial year would include

Health & Safety, Data Analytics, Business Continuance and Water Management

(revisited).

3. The Health & Safety internal audit is presented at this Finance

Audit and Risk Sub-committee (FARS) meeting.

4. The Data Analytics internal audit is near completion and will be

presented at the 12 February 2019 FARS meeting.

Future Internal Audits

5. As outlined above, Business Continuance was agreed to form part of

the current work programme however it should be noted that Council recently

engaged a specialised Business Continuance agency for an initial review of the

current plan. This is currently being assimilated internally prior to being

presented to FARS.

6. Initial findings of the review indicate that the Business

Continuance Plan (BCP) requires a refresh, staff believe it not be an efficient

use of funds to perform a full internal audit review while the current BCP

requires work.

7. As a result, staff are requesting that the Business Continuance

internal audit be pushed out to a future financial year.

8. If FARS resolves for the Business Continuance internal audit to be

postponed, it is recognised that there will be available scope within the

internal audit budget. As a result staff recommend that an “Internal

Audit Follow Up” review be completed.

9. This Follow Up review would involve the internal auditors following

up on previously conducted internal audits and providing feedback as to how

effectively Council is progressing with implementing agreed recommendations.

10. There is

the option for the review to focusing on one or two select audits thoroughly,

or alternatively, an examination of all internal audits conducted over the last

two years. Staff are seeking feedback from Councillors on this matter.

11. Hastings

District Council engaged Crowe Horwath to perform such a review and found it to

be useful in terms of both accountability and providing comfort for their

governors.

Previous Internal Audits

12. The Crowe

Horwath internal audit programme is proving successful within Council, with

some solid feedback and recommendations received from our internal audits.

13. As a

reminder, under the new internal audit programme, Council has completed Data

Analytics (2016-17), Water Management, Procurement/Contract Management with

Living Wage extension.

Water Management

14. Group

Manager – Regulation, has provided a Water Management update at a

previous Corporate & Strategic Committee (C&S) meetings and is

scheduled to provide another update to the C&S Committee on 5 December 2018

with regard to how the recommendations and action points are progressing.

Procurement/Contract

Management

15. The

Procurement/Contract Management Audit provided some insightful review points. A

joint internal audit meeting between all five TLA’s identified that

procurement was a common theme amongst all Council’s and the proposal of

a joint approach was initiated.

16. Three meetings between councils have been held to agree a common way

forward as audits for each council are delivering the following similar

opportunities for improvement: S17a - review of contracts over $500k; Policy

review; Common Templates; Need for a central point of advice and support

centre.

17. At HBRC

level, work has started on the following 5 priority areas: Review of

Procurement strategy; Procurement and Contract management plan template;

Consistent use of contract central; Exec overview of contracts reporting;

Supplier review and close off (cleaning the existing 750 contracts in our

data base).

18. The

intention is to design a road map for the development of a hub and spoke model

for strategic and shared procurement by the end of this financial year, scoping

capacity, capability and resource requirements.

GoBus Living

Wage

19. The

Living Wage extension saw C&S agree to await the results of the Public

Transport Operating Model (PTOM review) being conducted at a national level.

Staff were expecting an initial report to be available around this time,

however Transport Minister Phil Twyford has indicated that there was further

work required with the interim draft as it “needed to dig more into the

detail to be useful”.

20. As a

result, further research is expected to be completed by the end of December,

with a public release date still to be determined. Staff will continue to

comply with the review and provide information when requested.

Decision Making

Process

21. Staff have assessed the

requirements of the Local Government Act 2002 in relation to this item and have

concluded that, as this report is for information only, the decision making

provisions do not apply.

|

Recommendation

That the Finance, Audit and Risk

Sub-committee receives and notes the “Internal

Audit Update” staff report.

|

Authored by:

|

Melissa des

Landes

Corporate Accountant

|

|

Approved by:

|

Jessica

Ellerm

Group Manager

Corporate Services

|

|

Attachment/s

There are no

attachments for this report.

HAWKE’S BAY REGIONAL

COUNCIL

Finance

Audit & Risk Sub-committee

Wednesday 21 November 2018

Subject: Treasury Update

Purpose of Report

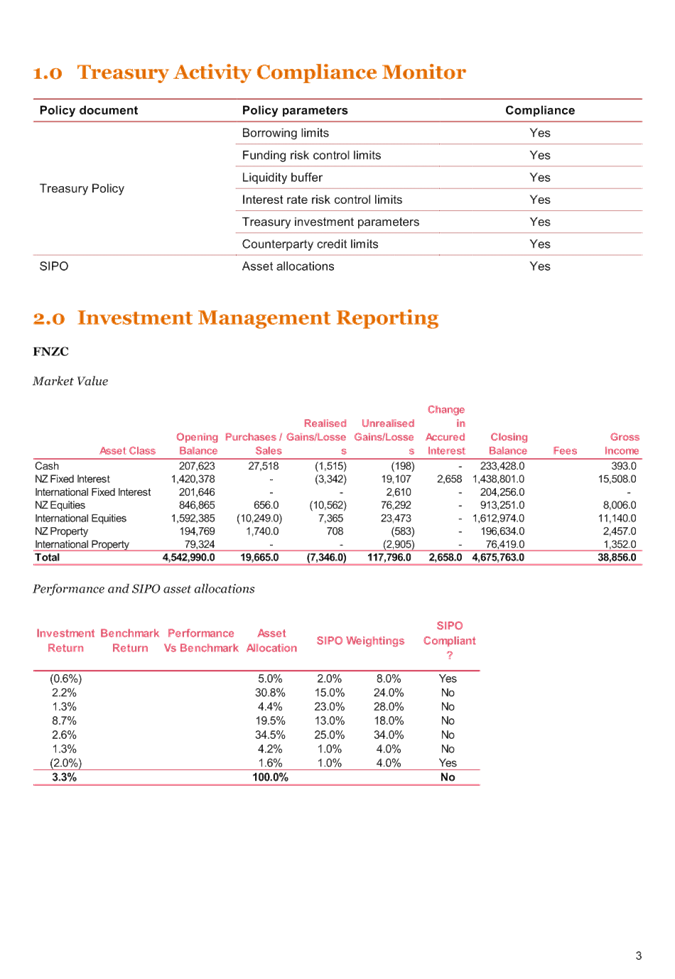

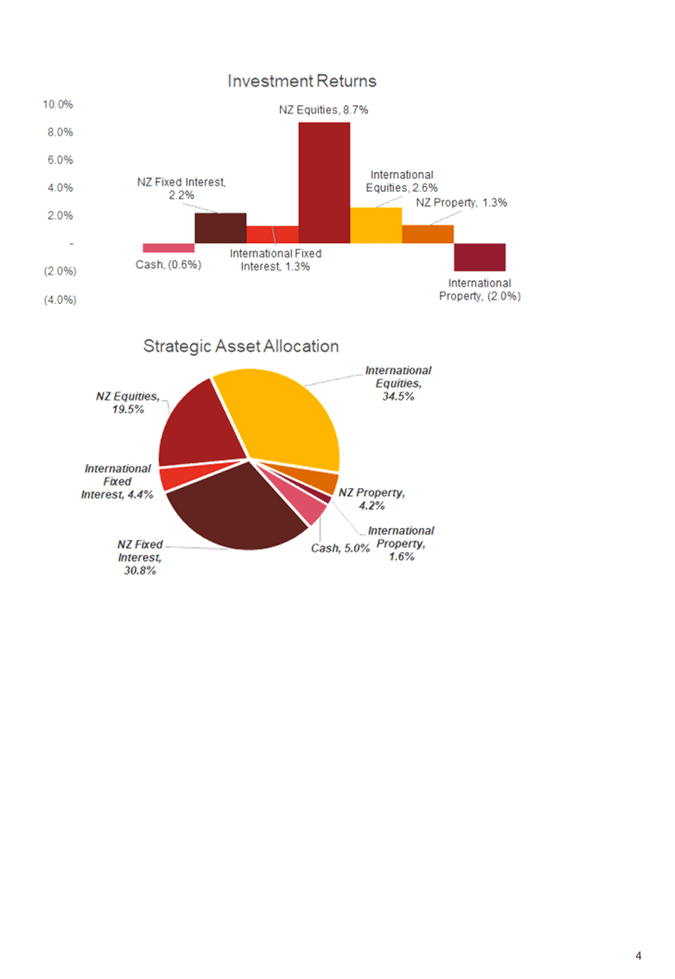

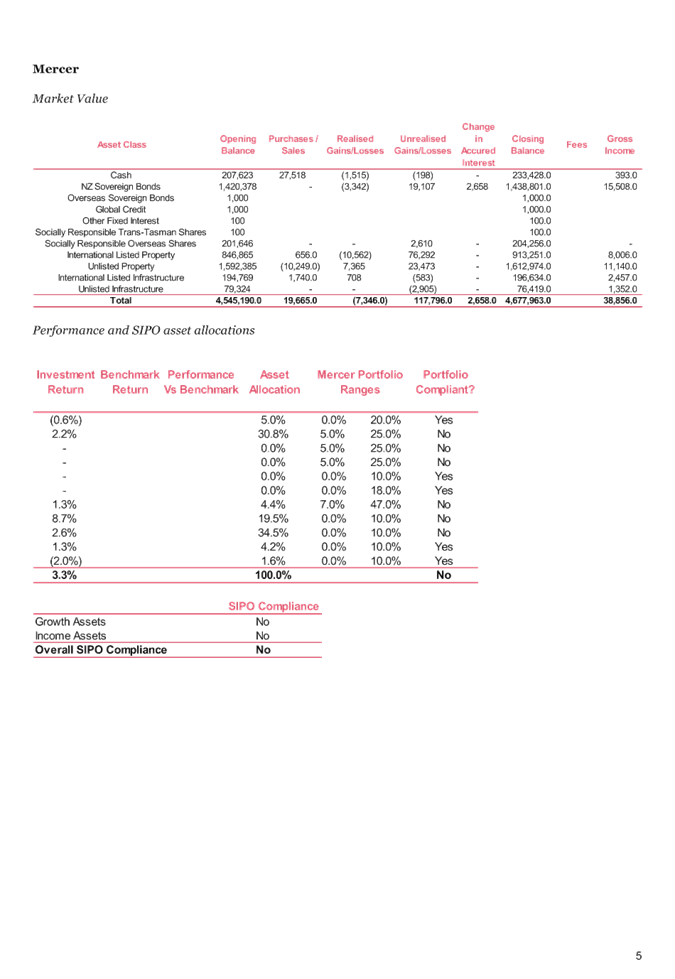

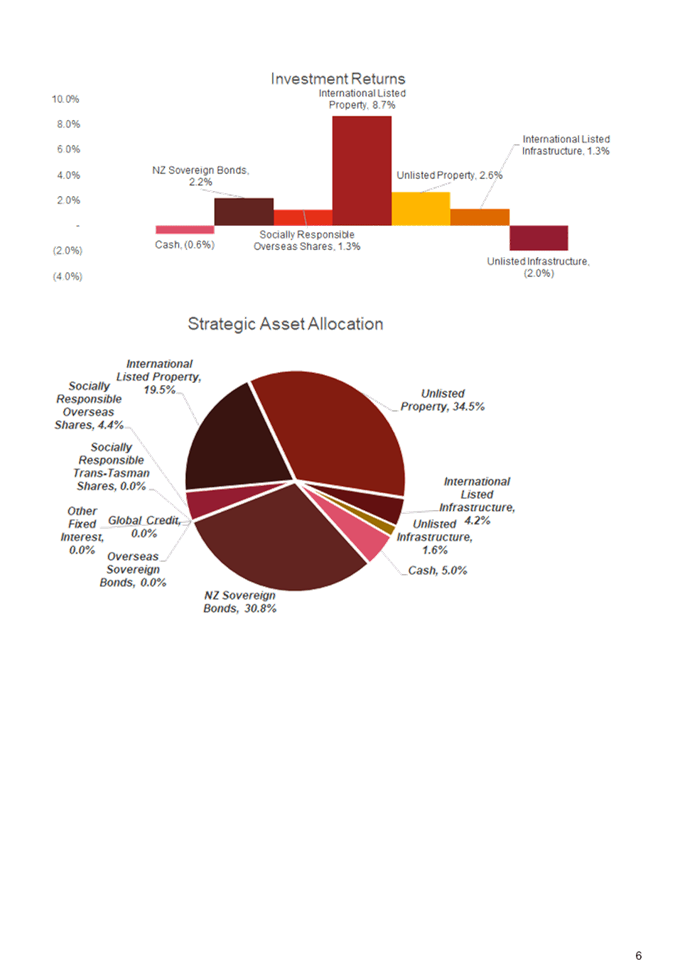

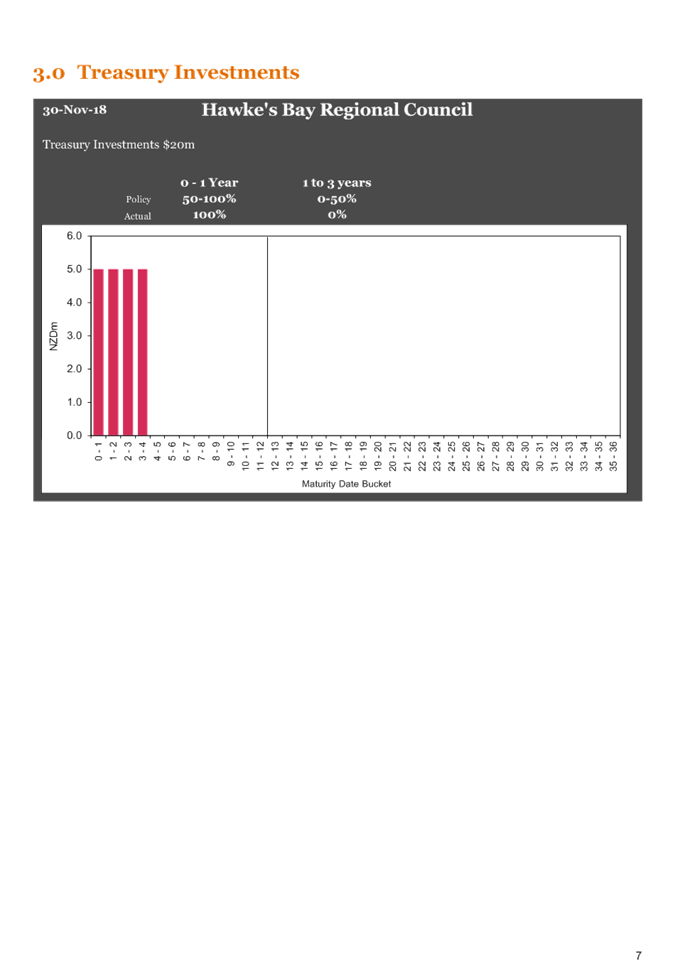

1. This item provides an update to the Sub-committee on the development

of Council’s diversified investment portfolio and a draft treasury report

for review, intended to form the basis of future reports to the Sub-committee.

Background

2. As part of the 2018-28 Long Term Plan (LTP) Council decided that the

$50 million previously set aside for the Ruataniwha Water Storage Scheme (RWSS)

would be preserved and grown to provide investment income to help fund the

increase in Council’s operating activities. These funds had

previously been on term deposit and the LTP proposed through its financial

strategy that these funds be allocated to diversified managed investment funds

in order to make these assets work harder and achieve better returns.

3. At the 27 June 2018 Council meeting it was also resolved to allow a

debt facility of $10 million to Hawkes Bay Regional Investment Company

(HBRIC). This was seen as a short term facility and would allow HBRIC the

flexibility for any funding required regarding the pending Napier Port

transaction. The $10 million would be deducted from the initial $50

million, however the interest rate charged to HBRIC would at least match the

forecast returns from the managed funds. On repayment of this loan

facility, the funds will be allocated to the diversified managed funds.

4. Since adoption of the Long Term Plan, staff have run a robust

procurement process for the appointment of Fund Managers. Requests for

proposals were issued to the open market, seventeen proposals were received and

shortlisted with four chosen to present to a Council workshop on 22 August

2018.

5. PwC treasury advisors were used as a third party to verify the

process and provide expertise on the merits of each investment manager.

PwC prepared a report for a Council workshop on 5 September 2018.

6. As a result of the process Council resolved at the meeting on 26

September 2018 to proceed with duel fund managers being Mercer and First New

Zealand Capital. The $40 million remaining would be split evenly over the two

funds.

7. Staff have since been working with fund managers and lawyers to get

all of the paper work and signing on process completed. It is expected

funds will start to be transferred to the fund managers to start investing

within the next two weeks.

8. The timing of the cash transfers match the maturity dates of

existing term deposits and the cash flow needs of the business. The

anticipated transfer of funds is below.

|

Date

|

Mercer

|

First NZ Capital

|

Total

|

|

November 18

|

$5 million

|

$5 million

|

$10 million

|

|

December 18

|

$2.5 million

|

$2.5 million

|

$5 million

|

|

January 19

|

$12.5 million

|

12.5 million

|

$25 million

|

|

TOTAL

|

$20 million

|

$20 million

|

$40 million

|

9. Staff note the process has taken longer than initially

expected. The budgeted returns of 4.5% in the first year of the LTP were

lower than the 5% expected for the rest of the LTP which accounts for the

timing involved of the creation of the fund and the allocation of funds out of

term deposit.

10. Forecast

returns could be unfavourably affected by the delay. Staff will continue

to update the Sub-committee and full Council on the effects on investment

income and any mitigation that maybe needed.

11. It is

anticipated that funds will be fully allocated by the next Sub-committee

meeting in February 2019, and formal treasury reporting will then commence.

Draft Treasury Report

12. Due to

the added complexity of having two fund managers we have commissioned PwC to

draft a Treasury report (attached) which will incorporate both reports into a

meaningful and easily comparable report.

13. Any

feedback from the Sub-committee would be appreciated, to enable presentation of

a complete report that meets the Sub-committee’s needs at the February

meeting.

Decision Making

Process

14. Staff have assessed the

requirements of the Local Government Act 2002 in relation to this item and have

concluded that, as this report is for information only, the decision making

provisions do not apply.

|

Recommendation

That the Finance, Audit and Risk

Sub-committee receives and notes the “Treasury Update” staff

report.

|

Authored by:

|

Manton

Collings

Chief Financial Officer

|

|

Approved by:

|

Jessica

Ellerm

Group Manager

Corporate Services

|

|

Attachment/s

|

⇩1

|

PWC Draft

Combined Treasury Report

|

|

|

|

PWC

Draft Combined Treasury Report

|

Attachment 1

|

HAWKE’S BAY REGIONAL COUNCIL

Finance

Audit & Risk Sub-committee

Wednesday 21 November 2018

Subject: November 2018

Sub-committee Work Programme Update

Reason for Report

1. In order to ensure the sub-committee’s ability to effectively

and efficiently fulfill its role and responsibilities, an overall update on its

work programme is provided following.

2. It should be noted that some non-urgent items in the work programme

have been deferred due to current staff resourcing and capacity restraints. We

have now successfully recruited for and appointed a Financial Accountant who

commences employment on 19 November 2018. This additional senior resource

will provide much needed capacity to make good progress on a substantive work

programme for this team.

|

Task

|

Item

|

Scheduled / Status

|

|

Internal

Audits

|

Health &

Safety

|

19 September

2018 FARS (Finance, Audit & Risk sub-committee) meeting now deferred to

21 November 2018 meeting

|

|

Data

Analytics

|

Q3 2018-19

FARS meeting

|

|

Business

Continuance

|

Q3 2018-19

FARS meeting

|

|

Water Management

|

Q4 2018-19

FARS meeting

|

|

Risk

Assessment & Management

|

Reporting on risks

(6-monthly) affecting Council plus noting changes / improvements / areas that

require attention from last report (3-monthly)

|

19 September

2018 and Q3 2018-19 FARS meetings.

Risk

management discussions and follow ups now being documented at each monthly

Exec meeting.

|

|

Insurance

|

Council’s

proposed 2018-19 Insurance programme

|

Reported to

6 June 2018 FARS meeting

|

|

Annual

Report

|

Discussion on Audit

Management Letter

|

Auditor

scheduled to attend November 2018 FARS meeting

|

|

Discussion

on the major issues (if any) in the audit report on the Annual Report.

|

Aligned with

Audit NZ & legislative requirements Sept-Nov each year. Update paper was

provided at 19 September meeting.

|

|

S17a Efficiency

Reviews (Section 17a Local Government Act)

|

Update on progress and

findings of Section 17a Efficiency Reviews

|

No reviews

scheduled in Q1&2 of Year 1 of LTP (Long Term Plan).

Staff member

attended Hawke’s Bay Council wide S17a Review collaboration meeting in

Wairoa held on 2 August 2018 where opportunities for cost sharing were

discussed.

|

|

Investment

Returns & Treasury Monitoring

|

Update on progress in

obtaining required level of dividend from PONL (Port of Napier Limited).

Update on Treasury function within Council.

|

HBRIC Ltd

2018-19 SoI (Statement of Intent) adopted at 27 June 2018 Council

meeting.

SIPO

(Statement of Investment Policy & Objectives) adopted at 27 June 2018

Council meeting.

Fund

managers appointed at 26 September Council meeting, thereafter quarterly

updates are to be presented at future FARS meetings.

Application

to join LGFA (Local Government Funding Agency) underway.

|

Decision Making

Process

3. Staff have assessed the requirements of the Local Government Act

2002 in relation to this item and have concluded that, as this report is for

information only, the decision making provisions do not apply.

|

Recommendation

That the Finance, Audit and Risk

Sub-committee receives and notes the “November 2018 Sub-committee

Work Programme Update” staff report.

|

Authored by:

|

Melissa des

Landes

Corporate Accountant

|

|

Approved by:

|

Jessica

Ellerm

Group Manager

Corporate Services

|

|

Attachment/s

There are no

attachments for this report.

HAWKE’S BAY REGIONAL COUNCIL

Finance

Audit & Risk Sub-committee

Wednesday 21 November 2018

Subject: Appointment of an

Independent Member of the Finance, Audit & Risk Sub-Committee

That the Finance Audit & Risk

Sub-committee excludes the public from this section of the meeting, being

Agenda Item 10 Appointment of an Independent Member of the Finance, Audit &

Risk Sub-committee with the general subject of the item to be considered while

the public is excluded; the reasons for passing the resolution and the specific

grounds under Section 48 (1) of the Local Government Official Information and

Meetings Act 1987 for the passing of this resolution being:

|

GENERAL SUBJECT OF THE ITEM TO BE

CONSIDERED

|

REASON FOR PASSING THIS RESOLUTION

|

GROUNDS UNDER SECTION 48(1) FOR THE

PASSING OF THE RESOLUTION

|

|

Appointment of an Independent Member of the Finance, Audit

& Risk Sub-Committee

|

7(2)(a) That the public conduct of this agenda item would

be likely to result in the disclosure of information where the withholding of

the information is necessary to protect the privacy of natural persons.

|

The Council is specified, in the First Schedule to this

Act, as a body to which the Act applies.

|

Authored and

Approved by:

|

Jessica

Ellerm

Group Manager

Corporate Services

|

|