Meeting of the Finance Audit & Risk Sub-committee

Date: Wednesday 10 May 2017

Time: 9.00am

|

Venue:

|

Council Chamber

Hawke's Bay Regional Council

159 Dalton Street

NAPIER

|

Agenda

Item Subject Page

1. Welcome/Notices/Apologies

2. Conflict

of Interest Declarations

3. Confirmation of

Minutes of the Finance Audit & Risk Sub-committee held on 31 January 2017

4. Follow-ups from

Previous Finance Audit & Risk Sub-committee Meetings 3

5. Progress on HB

LASS Tender for Internal Audit Provision 7

6. Operational

Efficiency Review 13

7. Capital Structure

Review 17

8. 2017 Sub-committee

Work Programme 23

Public Excluded Items

9. Proposed 2017-18

Council Insurance Programme 25

10. Internal Audit Report -

Taxation Compliance Review 27

HAWKE’S BAY REGIONAL COUNCIL

Finance

Audit & Risk Sub-committee

Wednesday 10 May 2017

SUBJECT: Follow-ups from Previous Finance

Audit & Risk Sub-committee Meetings

Reason for Report

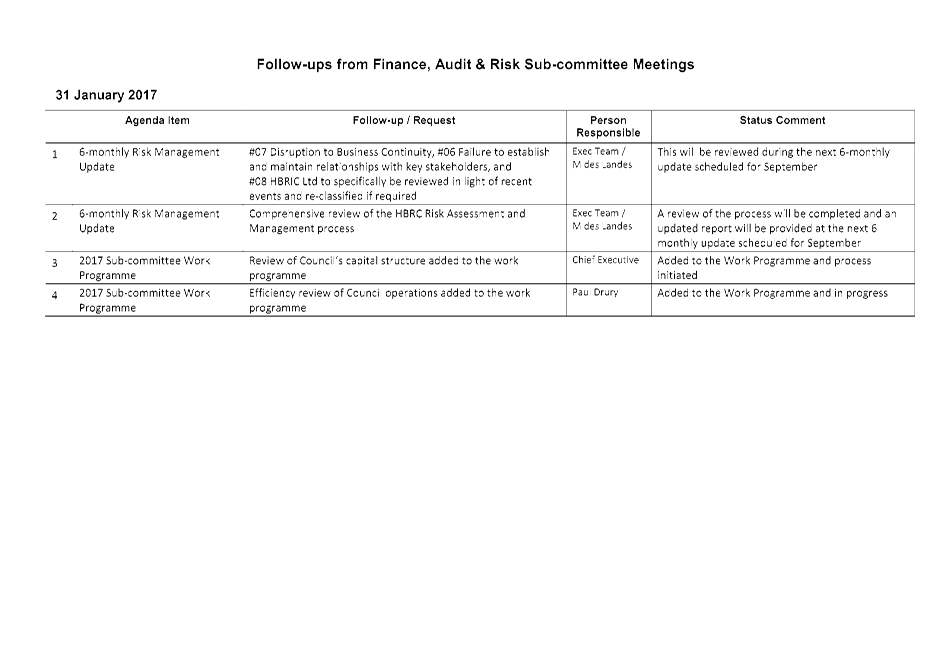

1. In order to track items raised at previous meetings that require

follow-up, a list of outstanding items is prepared for each meeting. All

follow-up items indicate who is responsible for each, when it is expected to be

completed and a brief status comment. Once the items have been completed and

reported to the Committee they will be removed from the list.

Decision

Making Process

2. Council is required to make every decision in

accordance with the Local Government Act 2002 (the Act). Staff have assessed

the in relation to this item and have concluded that as this report is for

information only and no decision is required, the decision making procedures

set out in the Act do not apply.

|

Recommendation

That the Finance, Audit and Risk Sub-committee receives

and notes the report “Follow-ups from Previous Finance Audit and

Risk Sub-committee Meetings”.

|

Authored by:

|

Leeanne

Hooper

Governance Manager

|

|

Approved by:

|

Paul Drury

Group Manager

Corporate Services

|

|

Attachment/s

|

⇩1

|

Follow-ups

from Previous Finance Audit & Risk Sub-committee Meetings

|

|

|

|

Follow-ups

from Previous Finance Audit & Risk Sub-committee Meetings

|

Attachment 1

|

HAWKE’S BAY REGIONAL COUNCIL

Finance

Audit & Risk Sub-committee

Wednesday 10 May 2017

Subject: Progress on HB LASS

Tender for Internal Audit Provision

Reason for Report

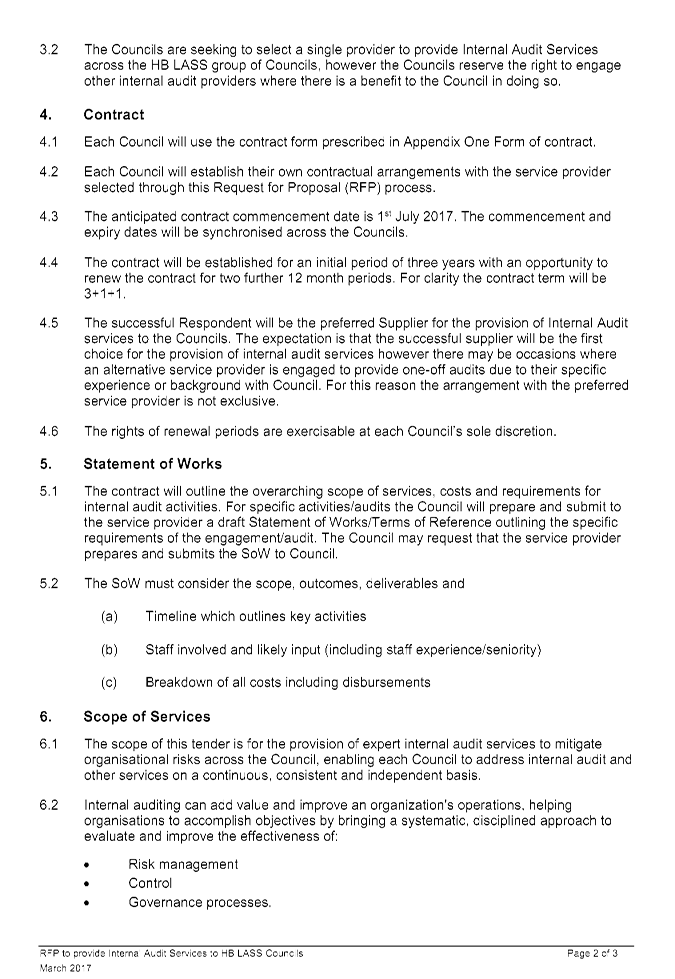

1. To provide the

Sub-committee with an update of the progress of the HB LASS (Hawke’s Bay

Local Authority Shared Services) tender for internal audit provision.

Background

2. This

Sub-committee resolved on 20 September 2016 that a joint internal audit

services approach with other local Council’s should be undertaken. This

would allow for financial efficiencies, better knowledge sharing and improved

access to skills.

Comment

3. A request for

proposal (RFP) for internal audit services for three years (with possibility

for up to two year extension) was advertised on 29 March 2017 using the

Government Electronic Tenders Service (GETS). The RFP overview is Attachment

1.

4. The tender

closed on 19 April 2017 with responses from six organisations.

5. These responses

are in the final stages of being evaluated based on price/non-price

information, with an evaluation meeting to be held on 5 May 2017 between all

HBLASS Councils. The current provider of internal audit services to HBRC is

PricewaterhouseCoopers.

6. Due diligence

checks with shortlisted suppliers are about to commence with a final

recommendation report scheduled for later in the month. Contract negotiation

and execution is scheduled for mid-late June. All five participating Councils

will need to be in a position to execute this contract. The service is expected

to commence for the 2017/18 financial year. HBRC have provided $30,000 in that

year for internal audit services.

Decision Making

Process

7. Staff have

assessed the requirements of the Local Government Act 2002 in relation to this

item and have concluded that, as this report is for information only, the

decision making provisions do not apply.

|

Recommendations

That the

Finance, Audit and Risk Sub-committee:

1. Receives and

notes the “Progress on HB LASS Tender for Internal Audit

Provision” report

2. Notes that

the Hawke’s Bay Regional Council Chief Executive has delegation to

enter into agreements as a member of HB LASS Ltd on behalf of Hawke’s

Bay Regional Council, including the provision of internal audit services.

|

Authored by:

|

Melissa des

Landes

Management Accountant

|

|

Approved by:

|

Paul Drury

Group Manager

Corporate Services

|

|

Attachment/s

|

⇩1

|

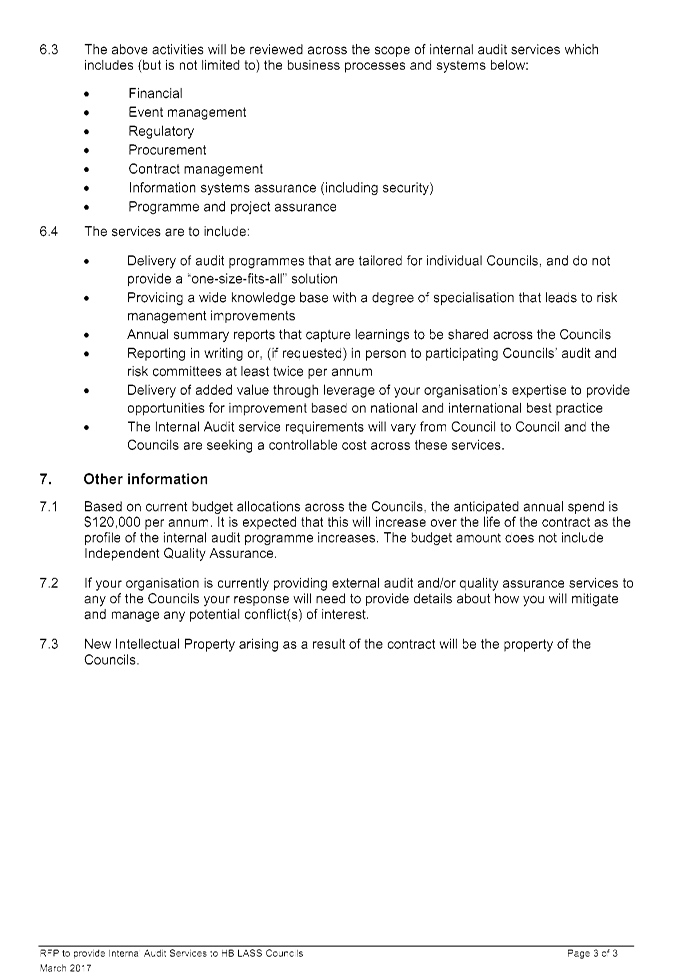

HB LASS

Request for Proposals for Internal Audit Services

|

|

|

|

HB

LASS Request for Proposals for Internal Audit Services

|

Attachment 1

|

HAWKE’S BAY REGIONAL COUNCIL

Finance

Audit & Risk Sub-committee

Wednesday 10 May 2017

Subject: Operational Efficiency

Review

Reason for Report

1. This report

sets out the programme of work for the operational efficiency review currently

being undertaken within Council and provides an update on the status of this

review.

Background

2. Council has

established that it intends to undertake an efficiency review to potentially

secure costs savings within the Council’s operational structure.

Reference to this review has been made in a number of documents including the

Consultation Document for the Annual Plan 2017-18.

3. The intention

is to undertake this efficiency review in advance of the upcoming LTP round

where there will be extra pressure for increasing expenditure in additional

environmental work and there could also well be pressure in the LTP on regional

income levels.

4. This review

will focus on cost efficiency opportunities including assessing whether or not

there are sensible levels of service adjustments within the current Council

operation. In particular:

4.1. A detailed

assessment of the income flow and expenditure across Council activities; and

4.2. Further areas

of discretionary/non-essential costs.

5. On 20 February

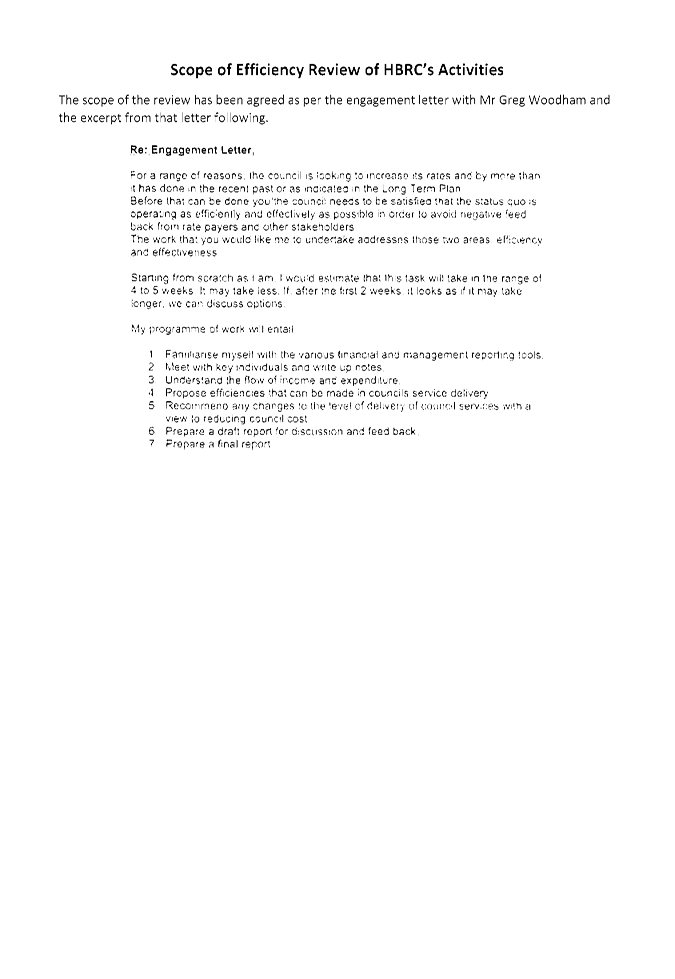

2017, the first stage of the review was contracted to Greg Woodham of Three

Roads Consulting, entailing the following work (as stated in the Engagement

Letter excerpt attached).

5.1. Familiarise

with the various financial and management reporting tools.

5.2. Meet with

individuals and write up notes.

5.3. Understand

the flow of incoming expenditure.

5.4. Propose

efficiencies that can be made in Council’s service delivery.

5.5. Recommend any

changes to the level of delivery of Council services with a view to reducing

Council costs.

5.6. Prepare a

draft report for discussion and feedback.

5.7. Prepare a

final report.

6. The draft

report has been distributed by Mr Woodham to the Executive and Councillors for

comment and feedback, and he has indicated that he will be preparing his final

report for Council’s consideration at the Corporate and Strategic

Committee meeting on 24 May 2017.

Decision Making

Process

7. Staff have

assessed the requirements of the Local Government Act 2002 in relation to this

item and have concluded that, as this report is for information only, the

decision making provisions do not apply.

|

Recommendations

That the Finance

Audit and Risk Sub-committee receives and notes the “Operational

Efficiency Review” staff report, and specifically notes the

agreed Scope of the review as attached.

|

Authored by:

|

Leeanne

Hooper

Governance Manager

|

|

Approved by:

|

Paul Drury

Group Manager

Corporate Services

|

|

Attachment/s

|

⇩1

|

Scope of

Efficiency Review

|

|

|

|

Scope

of Efficiency Review

|

Attachment 1

|

HAWKE’S BAY REGIONAL COUNCIL

Finance

Audit & Risk Sub-committee

Wednesday 10 May 2017

Subject: Capital Structure

Review

Reason for Report

1. To provide an

update on the Capital Structure Review as this review is included on this

Sub-committee’s work programme.

Background

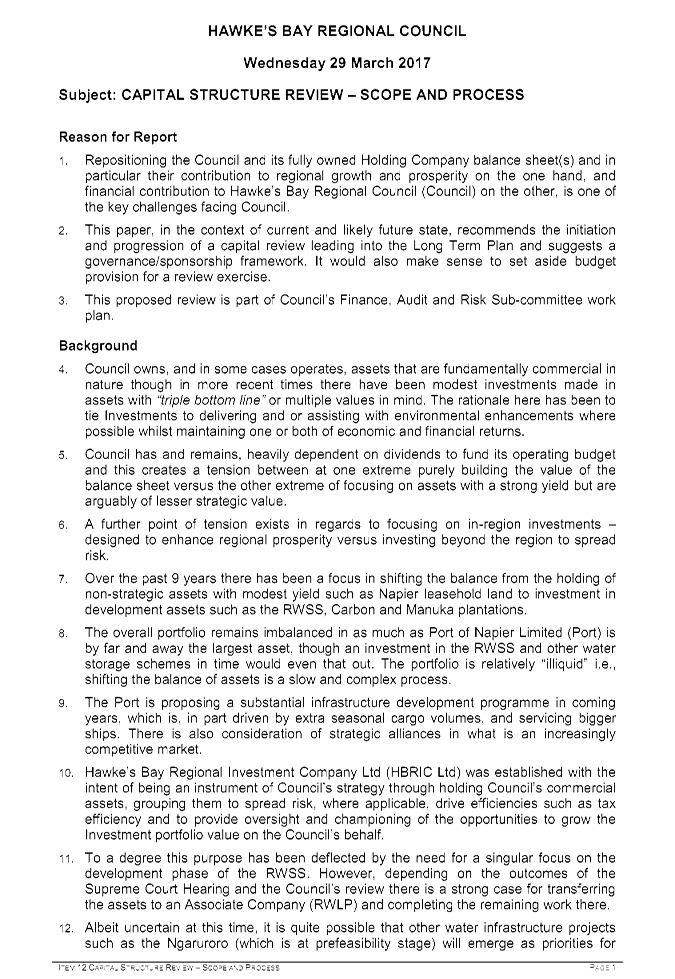

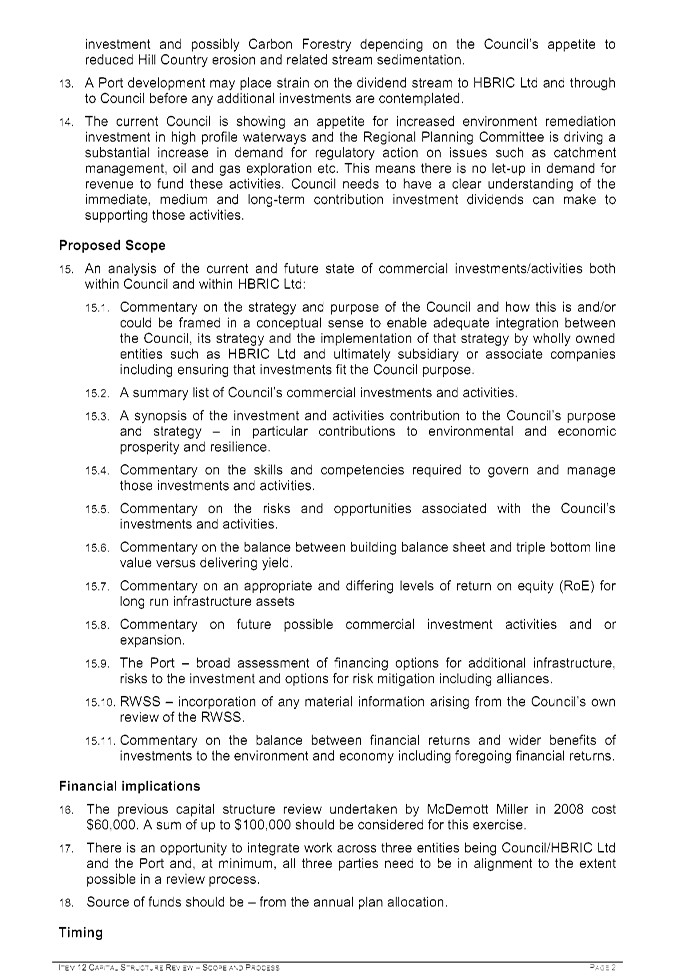

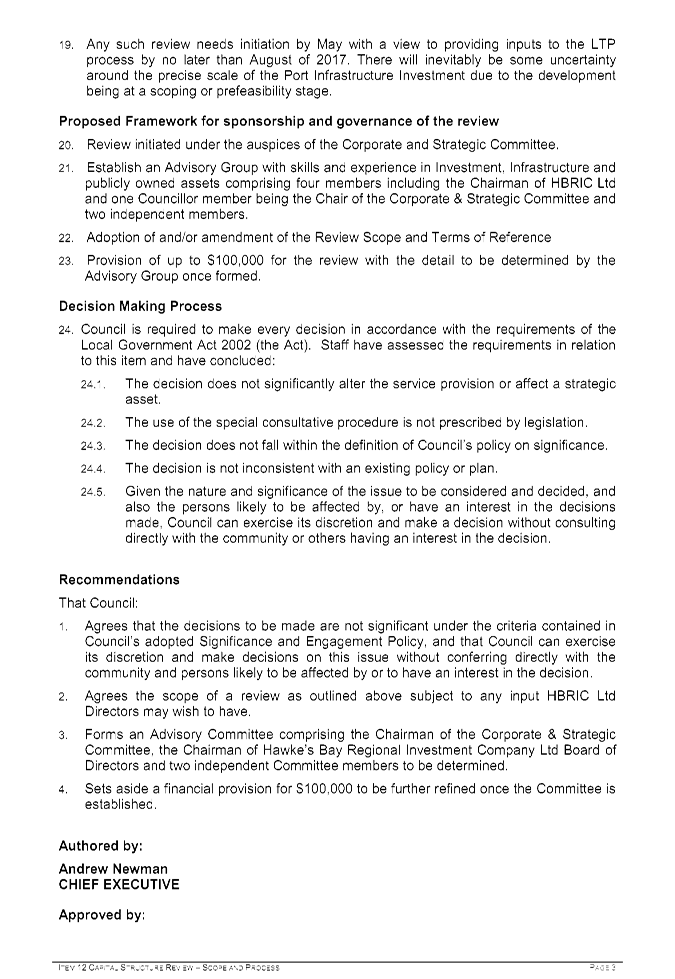

2. On 29 March

2017 Council approved the scope and process for the Capital Structure Review as

set out in Attachment 1; this approval being subject to any input

Hawke’s Bay Regional Investment Company Ltd (HBRIC Ltd) directors may

wish to have.

3. At that meeting

Council also resolved the membership of the Capital Structure Review

Advisory Committee, being:

3.1. Forms a Capital

Structure Review Advisory Committee comprising the HBRC Chairman, Rex

Graham, Chairman of the HBRC Corporate & Strategic Committee, Neil Kirton,

the Chairman of Hawke’s Bay Regional Investment Company Ltd Board of

Directors, the Chairman of the Napier Port Board of Directors and two suitably

qualified independent members to be confirmed by Council at its 26 April

meeting.

4. The appointment

of two independent committee members was the subject of a paper submitted to

Council on 26 April 2017, however the item was left to lie on the table as nominations

for the independent members had not been finalised.

5. At the Council

meeting on 26 April 2017 there was also discussion, arising from discussion on

the HBRIC Ltd 2017-18 Statement of Intent item, about a proposal to:

5.1. Amend the

HBRC Capital Structure – Scope and Process document to include a clause

that specifically states that the review will examine the arguments for and

against retaining ownership of Napier Port in HBRIC Ltd or moving to direct

ownership, with such arguments to include but not be limited to tax

considerations.

6. This amendment

was also ‘left to lie’ by Council resolution on 26 April 2017.

Outstanding Matters

7. The two matters

to be resolved prior to the Review commencing are:

7.1. recommendation

of suitably qualified candidates for appointment as the two independent members

on the Capital Structure Review Advisory Committee

7.2. Addition of

Napier Port ownership examination (as above) to the Scope and Process document

for the review.

Decision Making

Process

8. Staff have

assessed the requirements of the Local Government Act 2002 in relation to this

item and have concluded that, as this report is for information only, the

decision making provisions do not apply.

|

Recommendations

That the

Finance Audit and Risk Subcommittee receives and notes the “Capital

Structure Review” staff report.

|

Authored by:

|

Leeanne

Hooper

Governance Manager

|

|

Approved by:

|

Paul Drury

Group Manager

Corporate Services

|

|

Attachment/s

|

⇩1

|

Capital

Structure Review - Council Paper from 29 March 2017 Meeting

|

|

|

|

Capital

Structure Review - Council Paper from 29 March 2017 Meeting

|

Attachment 1

|

HAWKE’S BAY REGIONAL COUNCIL

Finance

Audit & Risk Sub-committee

Wednesday 10 May 2017

Subject: 2017 Sub-committee Work

Programme

Reason for Report

1. In order to ensure the sub-committee’s ability to effectively

and efficiently fulfill its role and responsibilities, an overall suggested

work programme is provided following.

|

Task

|

Item

|

Scheduled / Status

|

|

Internal Audits

|

Fraud

Detection and Prevention Review Report

|

completed

|

|

Event

Response Review

|

September

FA&R meeting

|

|

Taxation Review

|

May FA&R

meeting

|

|

Decide on

Internal Audit Programme for 2017-18

|

September

FA&R meeting

|

|

Risk Assessment & Management

|

Reporting on

risks (6-monthly) affecting Council

|

January

& September FA&R meetings

|

|

|

Review

previous 6-month Risk Assessment to note changes / improvements / areas that

require attention

|

|

|

Sub-committee

to carry out detailed review of individual Group’s Risk Management (as

part of the programmed reviews of activities)

|

|

Insurance

|

Council’s

proposed 2017-18 Insurance programme

|

Council’s

insurance broker to present at May FA&R meeting

|

|

Annual Report

|

Discussion

on the major issues (if any) in the audit report.

|

Auditor

scheduled to attend September FA&R meeting

|

|

Discussion

on Audit Management Letter

|

Auditor

scheduled to attend December FA&R meeting

|

|

Reviews

|

Review of

Council expenditure on delivery of functions with a view to ensuring and or

enhancing efficiency

|

Initiated 27

February 2017

|

|

|

Review of

the Council’s capital structure, taking into account the values of

dividends in supporting Council operations

|

Scope and

process for the review, and membership of the Capital Structure Review

Advisory Committee to lead the review were agreed by Council 29 March

2017 and

|

|

|

Comprehensive

review of the HBRC Risk Assessment and Management process to ensure major

strategic risks to the public and environment are appropriately managed

|

Review in

progress and an updated report will be provided with the next scheduled

update in September

|

Decision Making Process

2. As this report

is for information only and no decision is to be made, the decision making

provisions of the Local Government Act 2002 do not apply.

|

Recommendation

That the Finance, Audit and Risk

Sub-committee receives and notes the “2017 Sub-committee Work

Programme” report.

|

Authored by:

|

Leeanne

Hooper

Governance Manager

|

|

Approved by:

|

Paul Drury

Group Manager

Corporate Services

|

|

Attachment/s

There are no

attachments for this report.

HAWKE’S BAY REGIONAL COUNCIL

Finance

Audit & Risk Sub-committee

Wednesday 10 May 2017

Subject: Proposed 2017-18

Council Insurance Programme

Recommendations

1.

That the Finance, Audit and

Risk Sub-committee excludes the public from this section of the meeting, being

Agenda Item 9 Proposed 2017-18 Council Insurance Programme with the general

subject of the item to be considered while the public is excluded; the reasons

for passing the resolution and the specific grounds under Section 48 (1) of the

Local Government Official Information and Meetings Act 1987 for the passing of

this resolution being:

|

GENERAL SUBJECT OF THE ITEM TO BE

CONSIDERED

|

REASON FOR PASSING THIS RESOLUTION

|

GROUNDS UNDER SECTION 48(1) FOR THE

PASSING OF THE RESOLUTION

|

|

Proposed 2017-18 Council Insurance Programme

|

7(2)(i) That the public conduct of this agenda item would

be likely to result in the disclosure of information where the withholding of

the information is necessary to enable the local authority holding the

information to carry out, without prejudice or disadvantage, negotiations

(including commercial and industrial negotiations).

|

The Council is specified, in the First Schedule to this

Act, as a body to which the Act applies.

|

2.

That Matt Meacham,

representing JLT insurance brokers, is in attendance for this item to enable

provision of detailed responses to Committee queries.

Authored by:

|

Trudy

Kilkolly

Financial Accountant

|

|

Approved by:

|

Paul Drury

Group Manager

Corporate Services

|

|

HAWKE’S BAY REGIONAL

COUNCIL

Finance

Audit & Risk Sub-committee

Wednesday 10 May 2017

Subject: Internal Audit Report -

Taxation Compliance Review

Recommendation

That the Finance, Audit & Risk

Sub-committee excludes the public from this section of the meeting, being

Agenda Item 10 Internal Audit Report - Taxation Compliance Review with the

general subject of the item to be considered while the public is excluded; the

reasons for passing the resolution and the specific grounds under Section 48

(1) of the Local Government Official Information and Meetings Act 1987 for the

passing of this resolution being:

|

GENERAL SUBJECT OF THE ITEM TO BE CONSIDERED

|

REASON FOR PASSING THIS RESOLUTION

|

GROUNDS UNDER SECTION 48(1) FOR THE

PASSING OF THE RESOLUTION

|

|

Internal Audit Report - Taxation Compliance Review

|

7(2)(a) That the public conduct of this agenda item would

be likely to result in the disclosure of information where the withholding of

the information is necessary to protect the privacy of natural persons.

|

The Council is specified, in the First Schedule to this

Act, as a body to which the Act applies.

|

Authored by:

|

Manton

Collings

Corporate Accountant

|

|

Approved by:

|

Paul Drury

Group Manager

Corporate Services

|

|