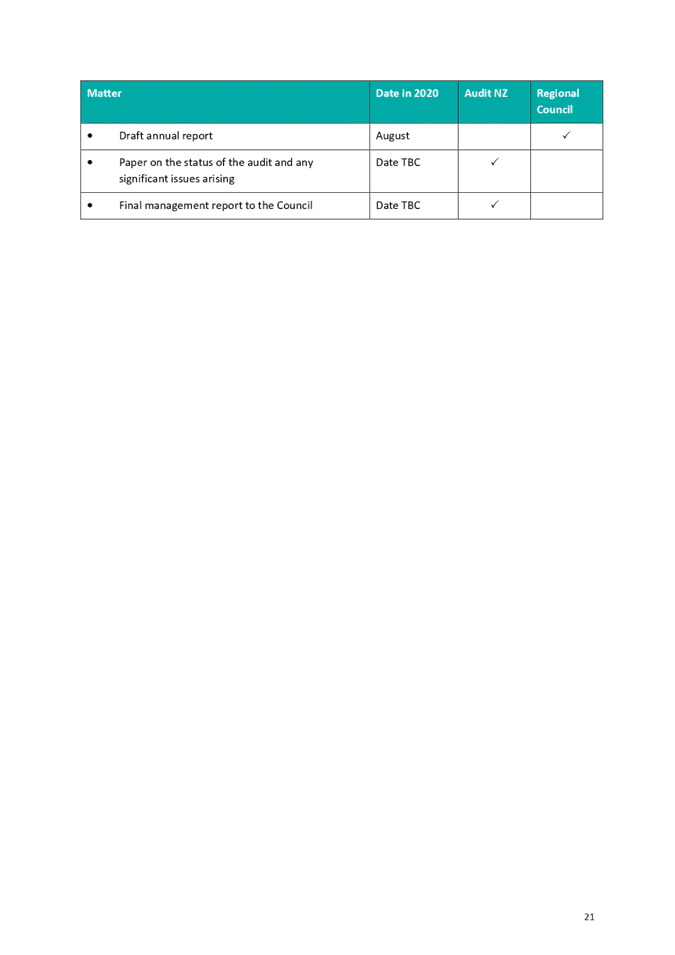

Meeting of the Finance Audit & Risk Sub-committee

Date: Wednesday 12 August 2020

Time: 9.00am

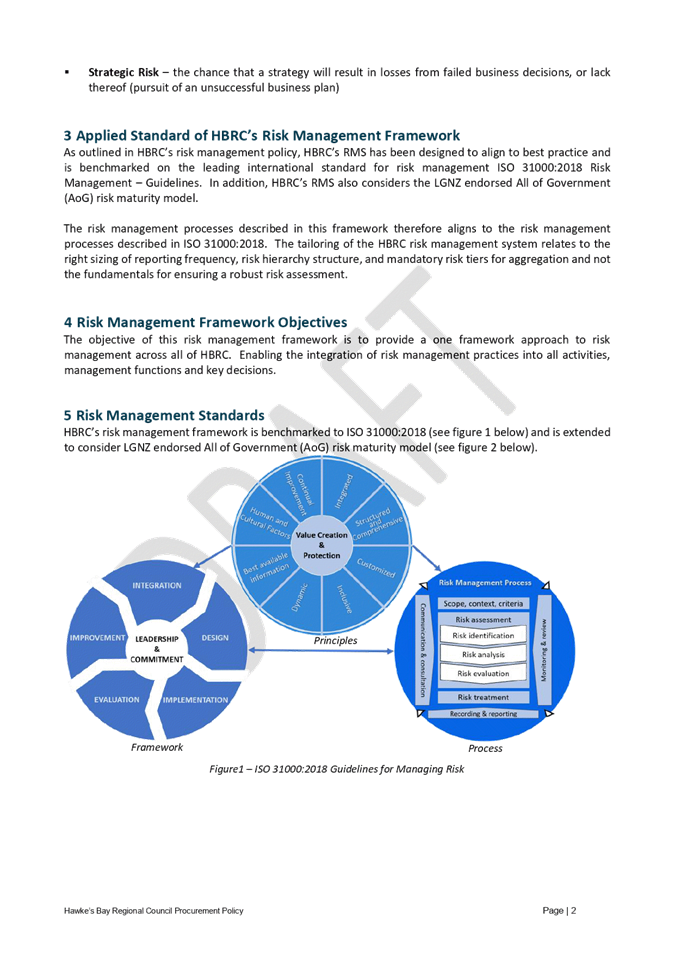

|

Venue:

|

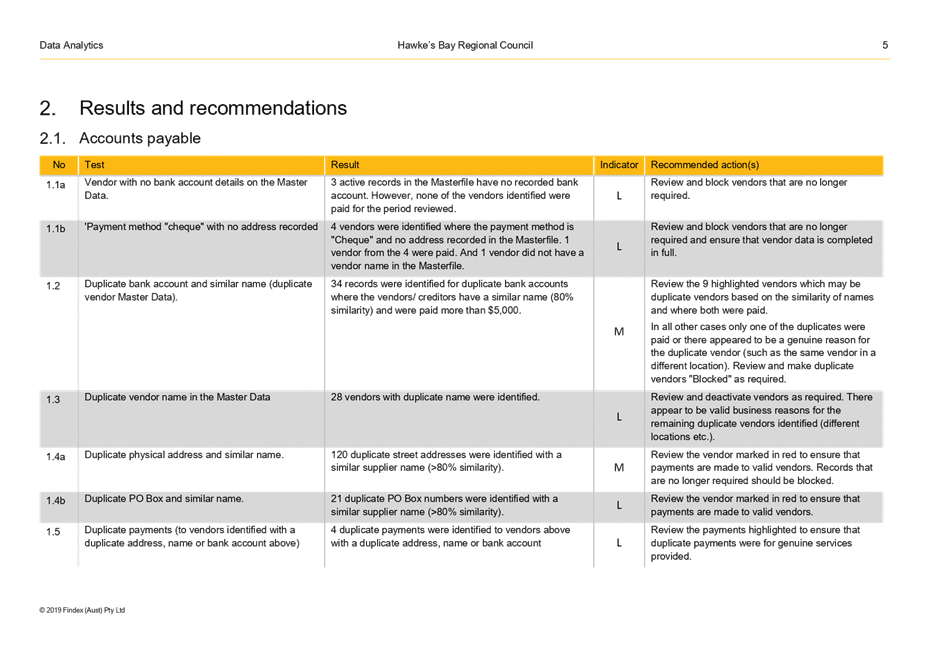

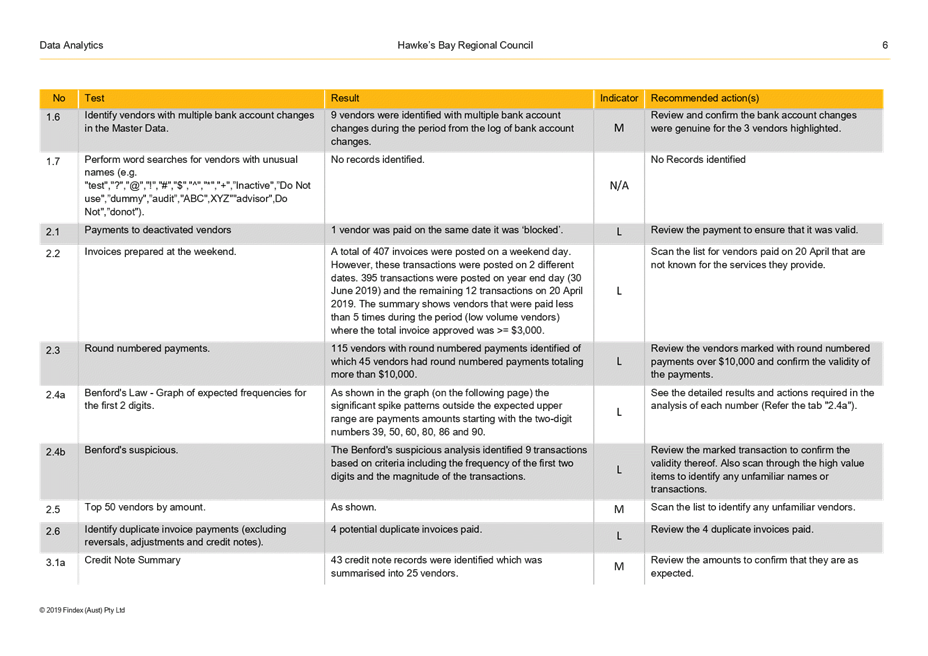

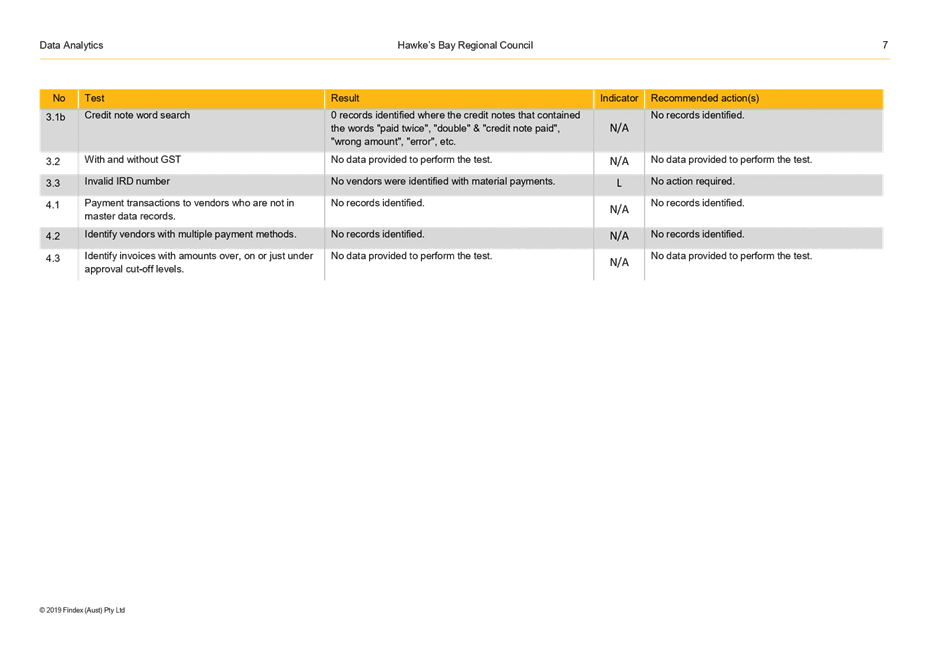

Council Chamber

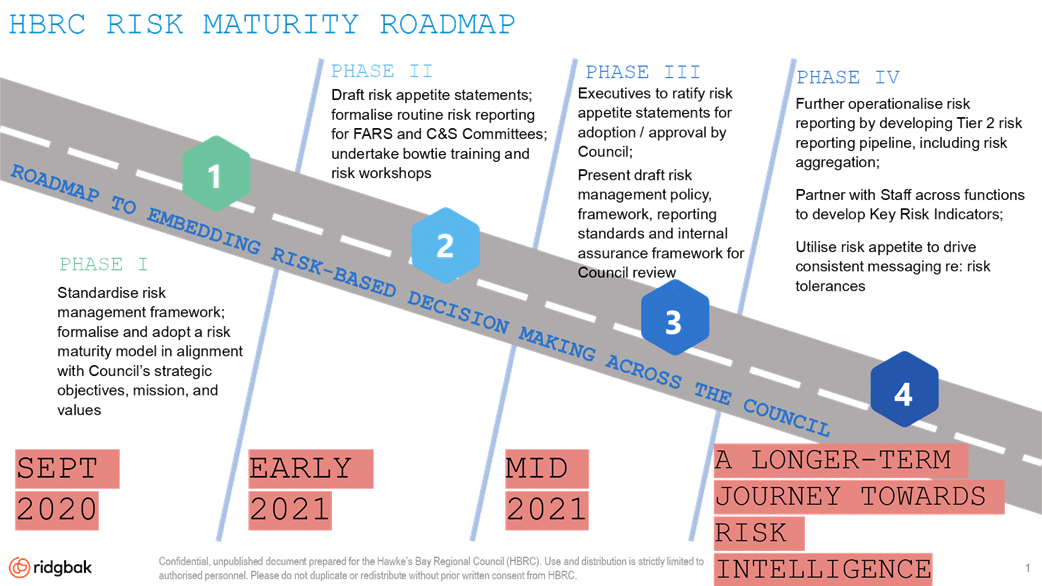

Hawke's Bay Regional Council

159 Dalton Street

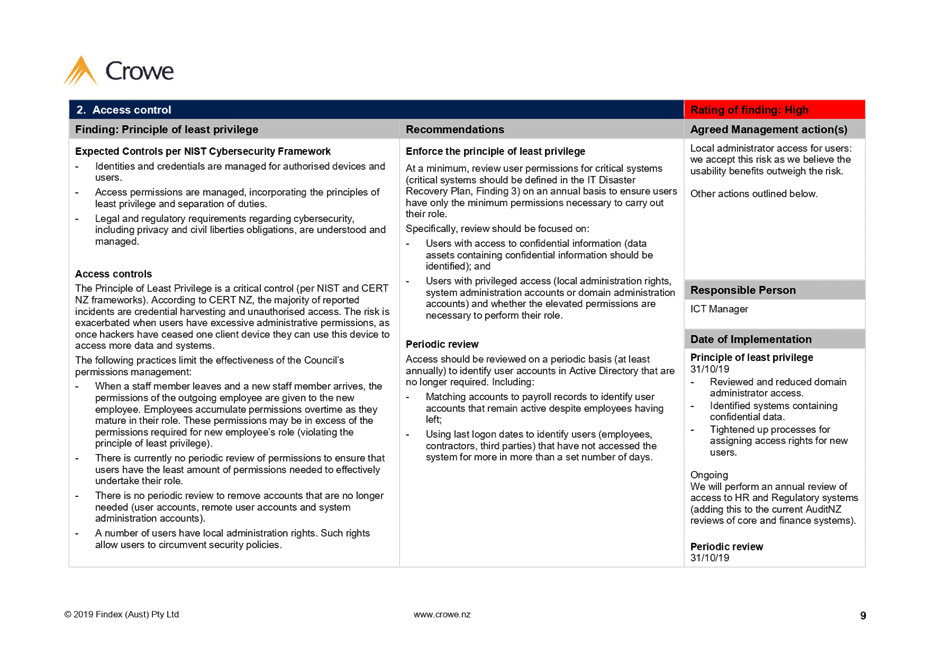

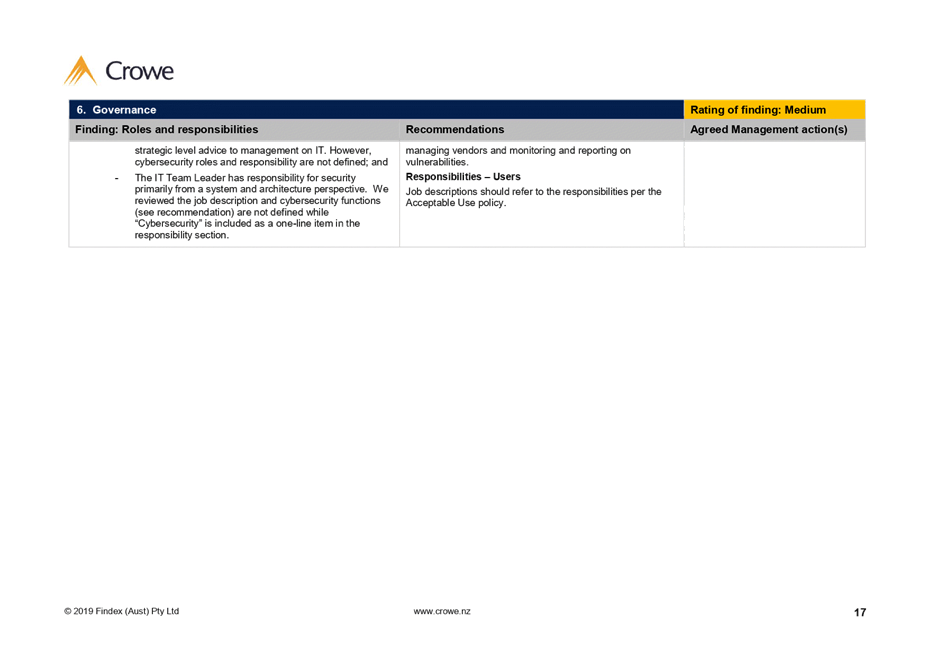

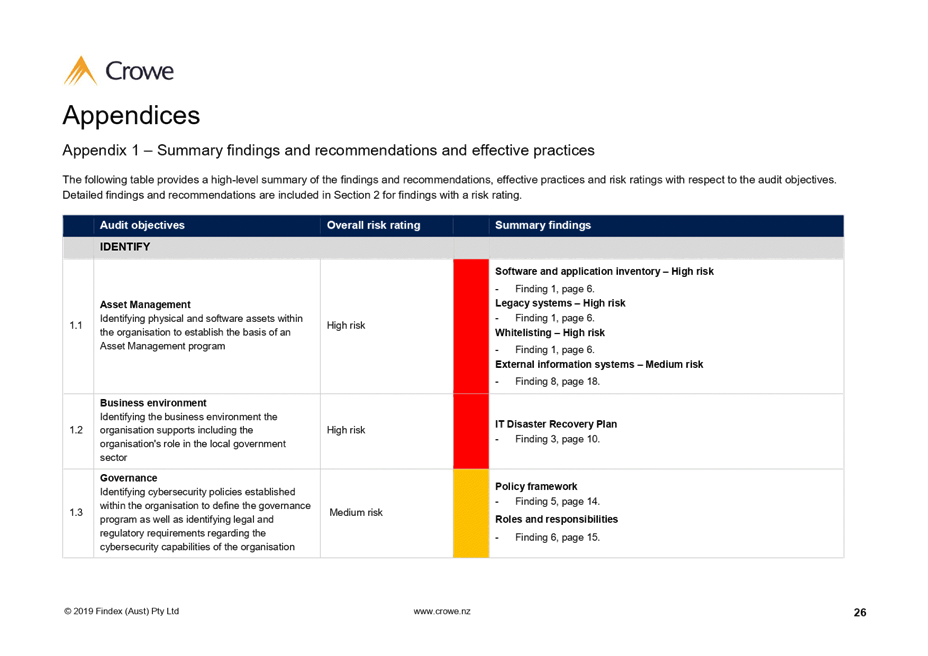

NAPIER

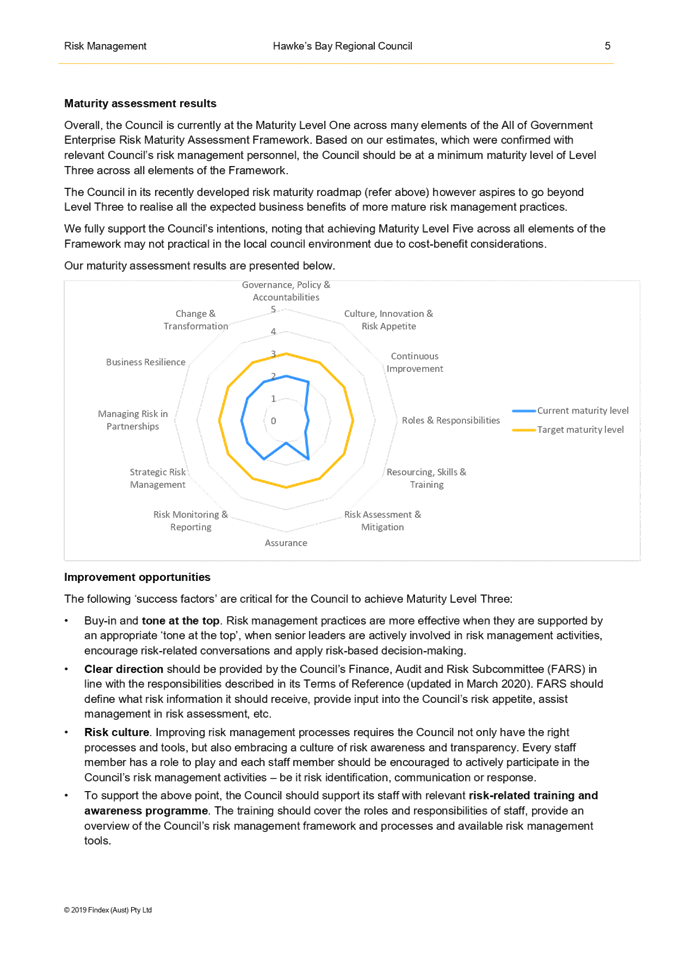

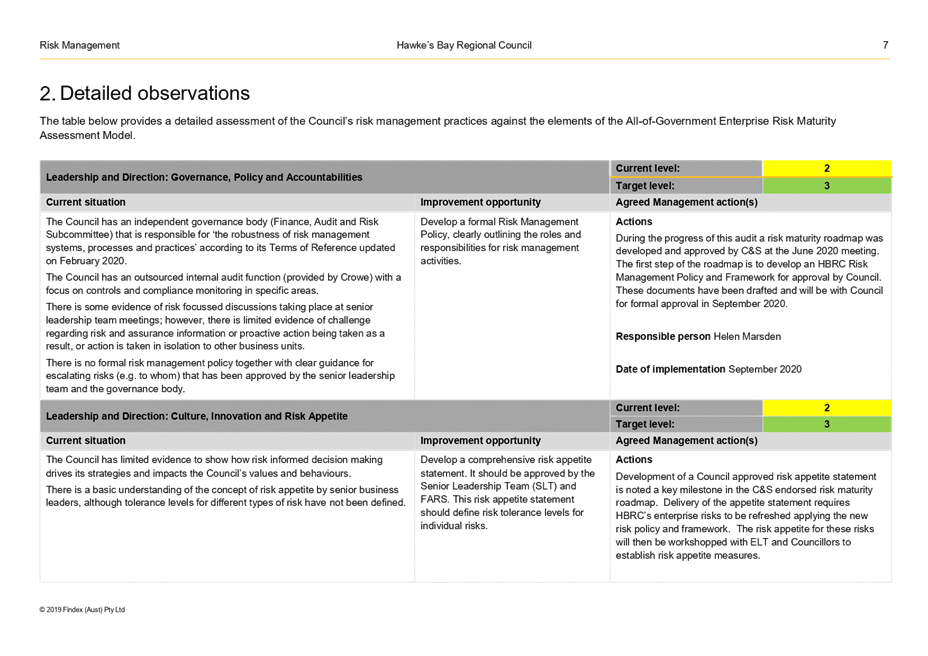

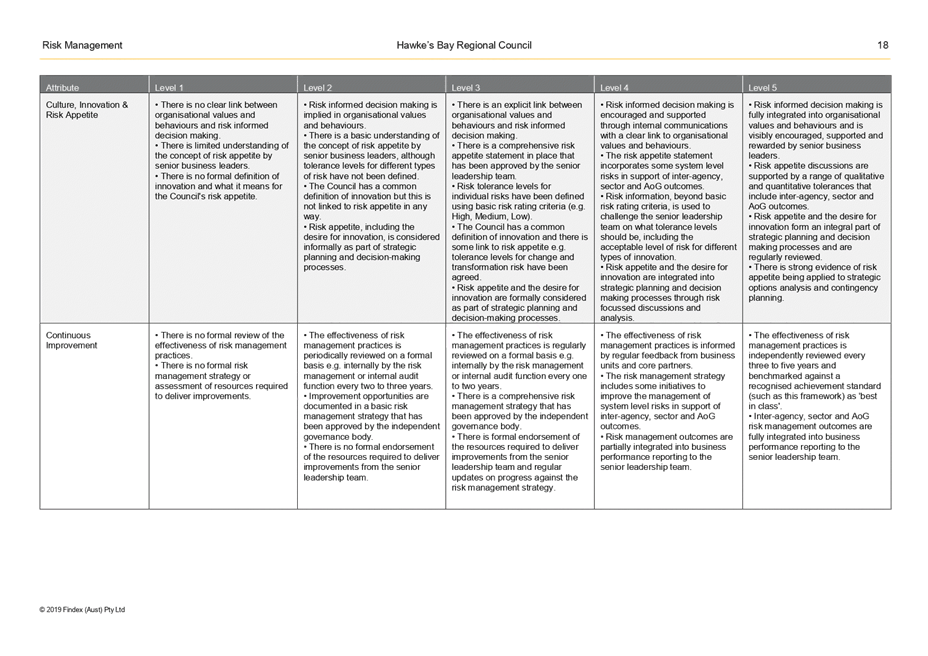

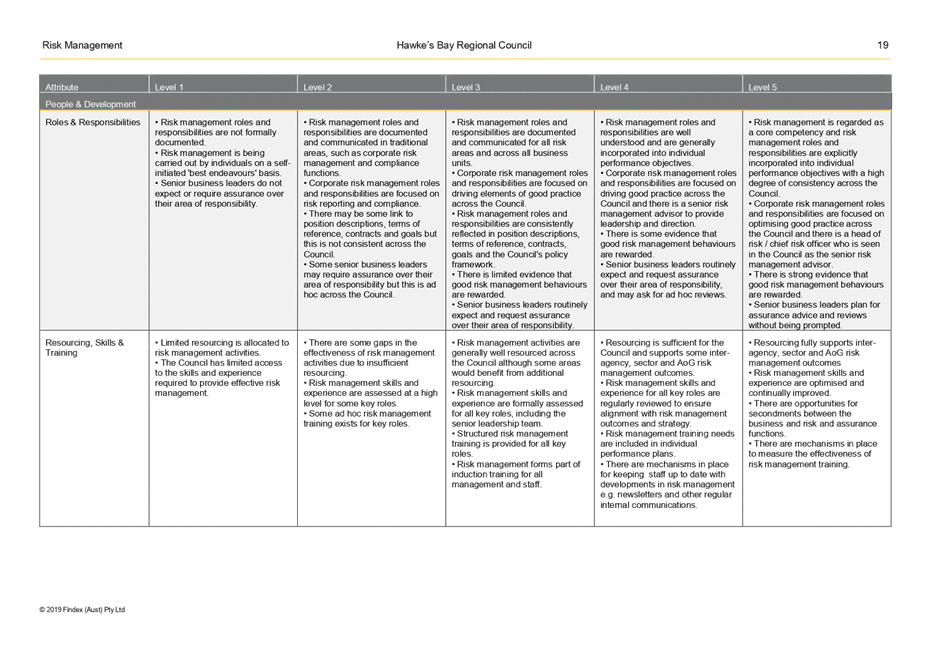

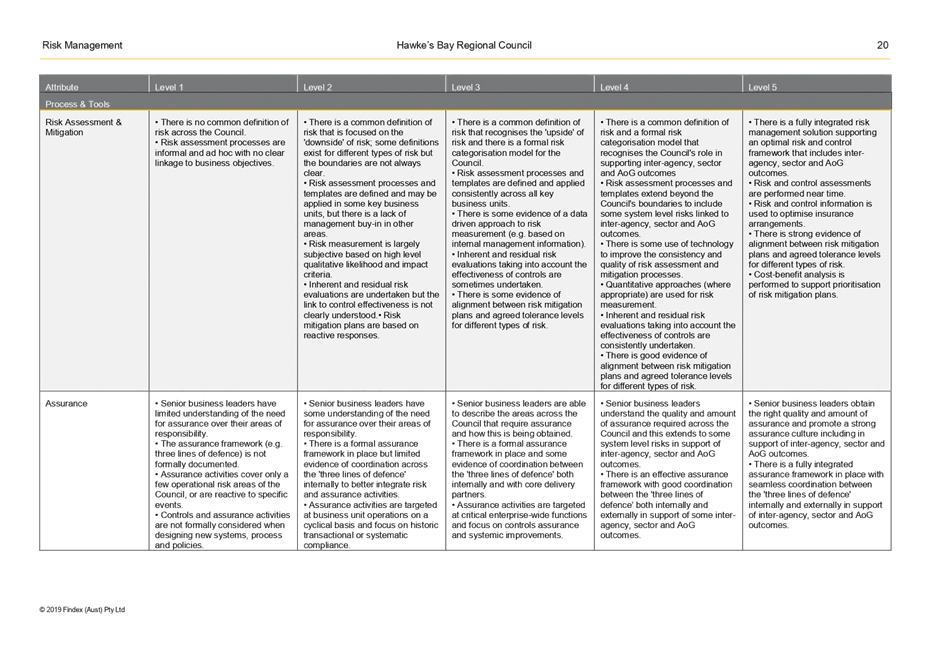

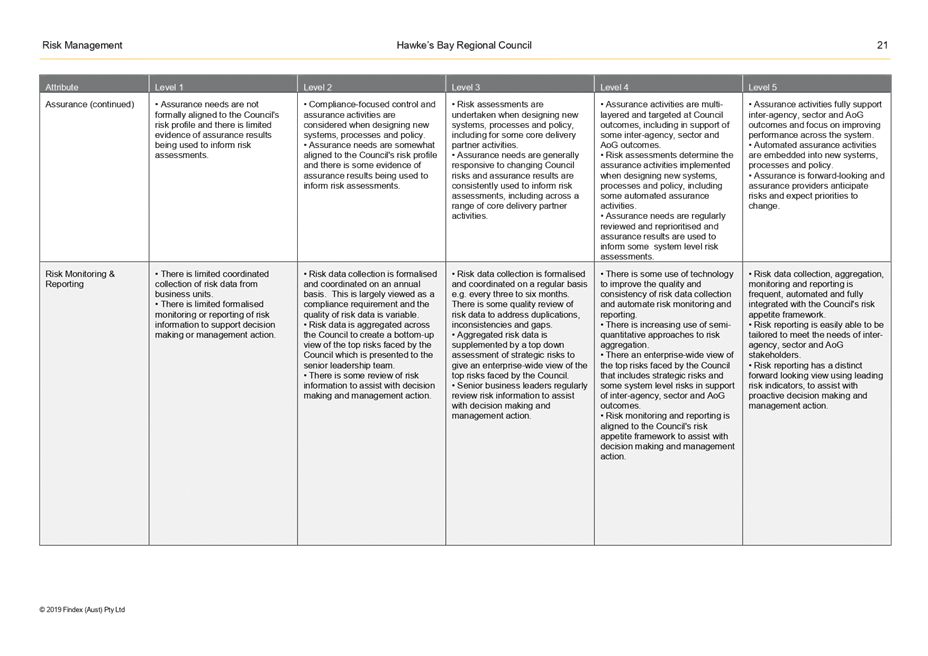

|

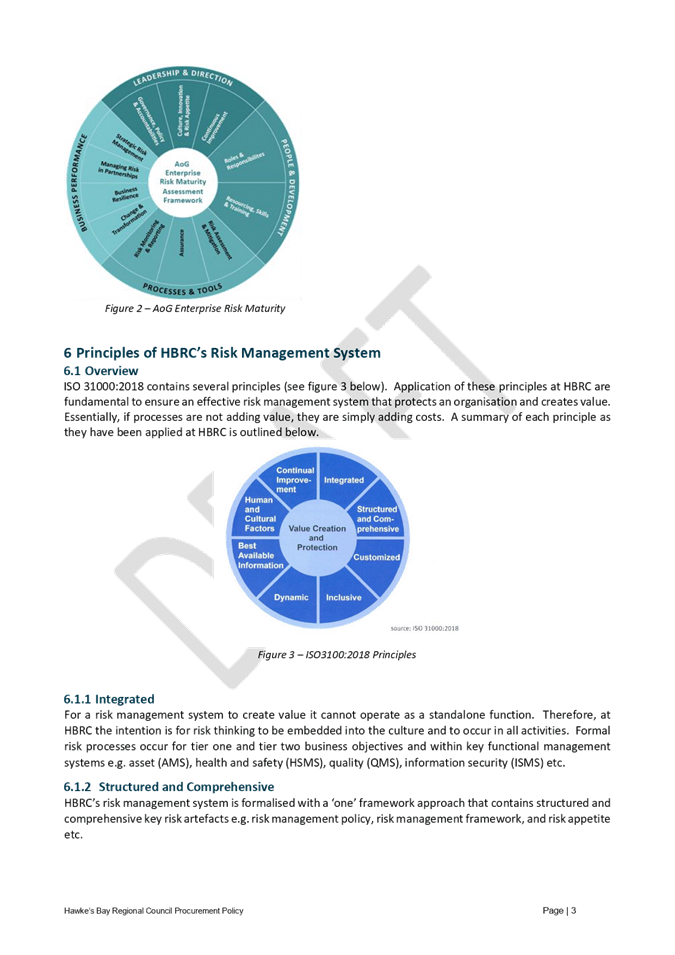

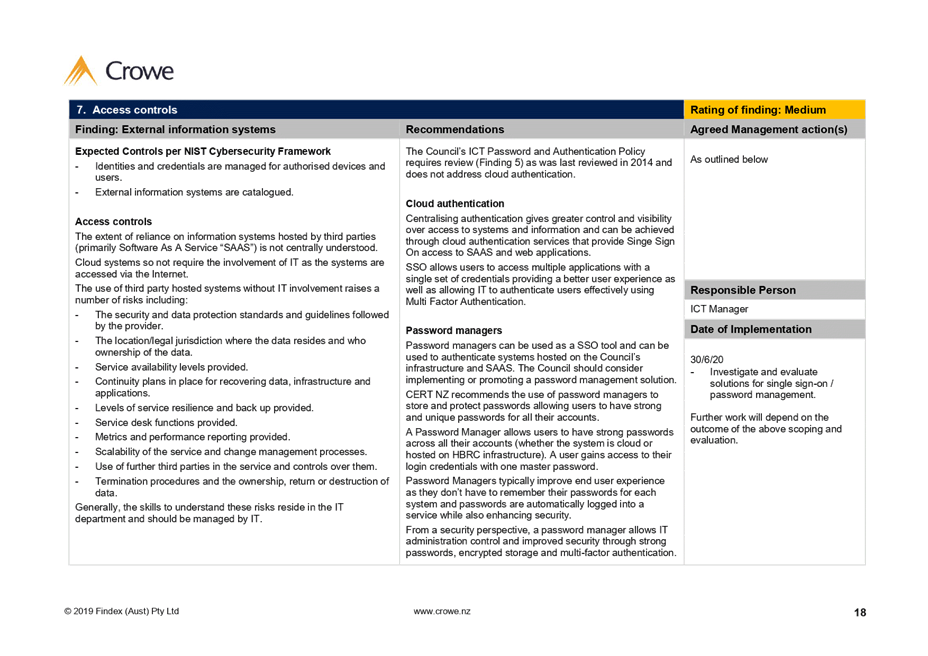

Agenda

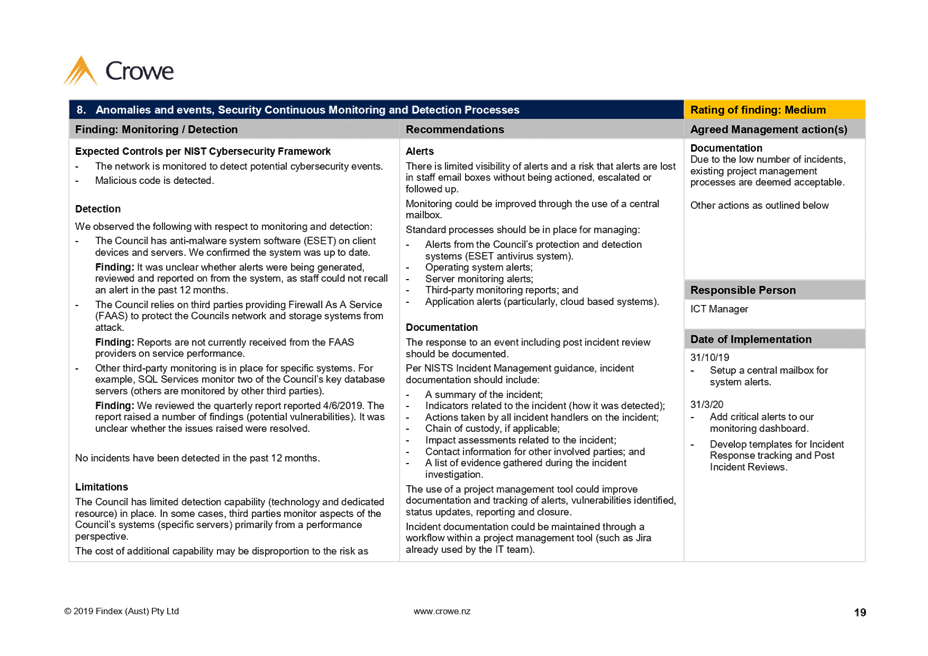

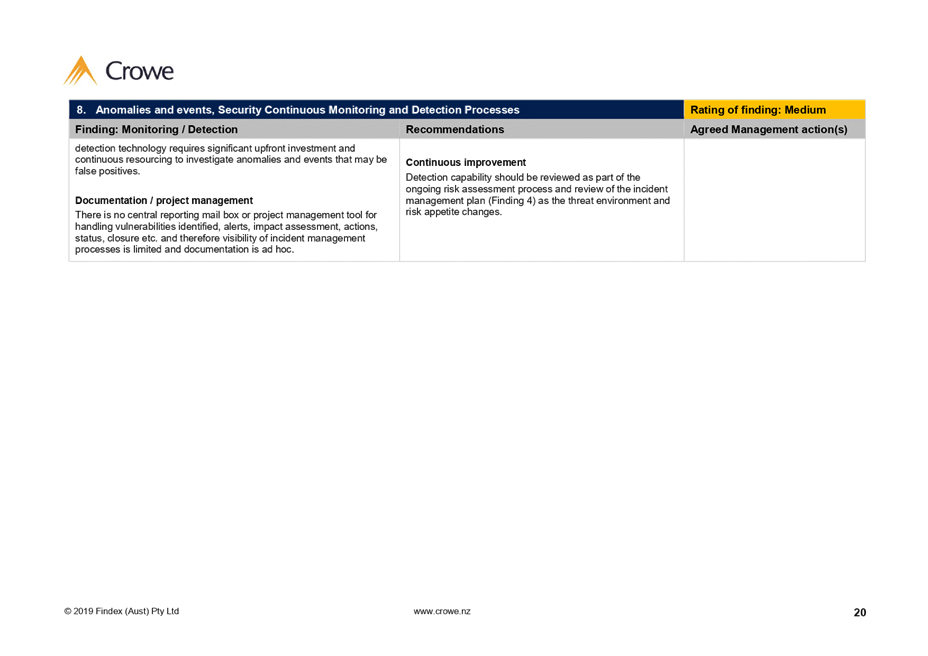

Item Title Page

1. Welcome/Notices/Apologies

2. Conflict

of Interest Declarations

3. Confirmation of

Minutes of the Finance Audit & Risk Sub-committee meeting held on 12

February 2020

Decision Items

4. Procurement Policy

Amendments to Support the HB Economic Recovery 3

5. Risk Maturity 51

6. Six Monthly

Enterprise Risk Management Report 117

7. Annual 2020-21

Internal Audit Work Plan 145

8. 2019-20 Annual

Report Audit Plan 163

9. Cyber Security

Internal Audit Follow-up 191

10. Data Analytics Internal Audit

Report 231

11. Internal Audits Review and

Action Plan 247

12. Sub-committee Work Programme

August 2020 Update 283

13. Treasury

Report to 30 June 2020 (late item to come)

HAWKE’S BAY REGIONAL COUNCIL

Finance

Audit & Risk Sub-committee

Wednesday 12 August 2020

Subject: Procurement Policy

Amendments to Support the HB Economic Recovery

Reason for Report

1. This item

provides an update on progress implementing the HBRC Procurement Policy and

Manual adopted by Council in July 2019. These documents incorporate

recommendations made by Crowe Horwath in a 2018 audit report, guidance issued

by the Office of the Auditor General and subsequent best practices guidelines

and templates issued by the Ministry of Business, Innovation

& Employment.

2. Since council adopted the Procurement Policy in July 2019 there have

been factors such as Covid-19, climate change mitigation and the development of

a risk framework which should be reflected through updates to the procurement

policy.

3. The report also provides a 2019-20 year-end report of

procurement metrics requested by the Finance Audit and Risk Sub-committee.

Officers’ Recommendation(s)

4. Officers

recommend councillors review the updated draft Procurement Policy and Manual

(attached), and consider the proposed changes as highlighted which include

Climate.Smart.Recovery. suggestions made at the Regional Council meeting on

20 May, to strengthen HBRC’s ability to support the region’s

economic recovery.

Background / Discussion

5. As a

‘live’ document the HBRC Procurement Policy is being updated to

reflect drivers for change. Since June 2019 when the policy was adopted

by Council a greater emphasis on climate change mitigation; supporting local

economic recovery from Covid-19 and alignment to the HBRC development of a risk

framework have been requested.

6. On 15 May 2020

a letter was sent to local government CEOs from the Auditor General. article

on OAG website. Included with the letter was a report with key

observations and recommendations to review procurement policy and procedure at

a local level. The report noted that while it is not mandatory for HBRC

to comply with OAG Govt procurement rules, being known and accepted as best

practice, it would be difficult to justify deviation. Key references from

the report are listed below.

7. Governance

and operational – “OAG often sees examples of

procurements where the lines between governance and management are

blurred. For example, mayors or other elected members might be part of

tender evaluation panels. This is not good practice. However, it is

entirely appropriate for major procurements to require sign-off by the

governing body. In order for elected members to approve procurement

decisions when required, they need enough information to make informed decisions.”

Action – Strengthened the

HBRC procurement manual to include procurement plans and tender recommendation

templates to the tenders committee for items over $400k, not covered the

CEO’s delegated financial authorities and including a probity sign off

check list to assure informed decisions, keep the organisation

‘safe’ and to get best value for money for ratepayers.

8. Conflicts of

interest – “Under no circumstances should a procurement process

allow council staff or elected members to receive preferential treatment.

There are two specific restrictions that apply to elected members under the

Local Authorities (Members’ Interests) Act 1968. Under the Act, an

elected member cannot:

8.1. enter into

contracts with their local authority worth more than $25,000 in a financial

year; or

8.2. discuss or

vote on matters before their authority in which they have a direct or indirect

pecuniary interest, other than an interest in common with the public”

9.3 Action

– Added the above wording to the Procurement policy under 5.2

and reference Gifts and inducements (HBRC Policy 18) and Sensitive expenditure

(HBRC Policy 24). This application will also be extended to HBRC committee

members to ensure consistency.

9. Emergency

procurement – There are no actions required as this is already

covered in the current policy and manual

10. Capability and capacity

– Policy and training. “Councils need to ensure

that there are regular internal audits, or other reviews, of procurement

activity. The findings from these reviews should be reported to the

governing body either directly or through the audit and risk committee.

Regular reviews of procurement practice can also help to identify training

needs and other risks.”

10.1. Action – As

identified in points 19 and 20. Training and audit functions for procurement

will be developed over the next six months supported by an internal

communications programme. HBRC will be taking part in a national

procurement benchmarking survey (Procurement Capability Index) conducted by

MBIE in October 2020.

11. Broader Outcomes

procurement The Government Procurement Rules require agencies to

“consider, and incorporate where appropriate, broader outcomes when

purchasing goods, services or works”. The rules define broader outcomes

“as the secondary benefits that are generated from the procurement

activity. They can be environmental, social, economic

or cultural benefits.

11.1. Although it is not

mandatory for councils to comply with the rules, they are encouraged to do

so. Councils that fail to comply with legislative requirements, or follow

best practice in their procurement practices will be at risk of legal challenge

and additional scrutiny and criticism from stakeholders and other third

parties.

11.2. Councils can mitigate

some of this risk by engaging with their elected members about their strategic

objectives and how they can align these with their intended procurement

outcomes. For example, if elected members want to prioritise using local

suppliers, or support suppliers that pay a living wage, councils should be

exploring ways to build those objectives into procurement policies and

processes.

12.3 Action – This

is covered by HBRC procurement policy principle No.1 now extended to include

Climate.Smart.Recovery. Practical considerations No.6; policy clauses 5.7 and

5.9 include local purchasing and fair wage. It is

intended that sustainability criteria being used as part of HBRC evaluation

processes be reviewed to reflect developments on an annual basis.

Procurement activity reporting 2019-20

12. Procurement reporting to

FARS for the period 1 July 2019 to 30 June 2020

12.1. 212 contracts were

created

12.2. 15 contracts were

awarded with a value of $100k+, 6 contracts were valued at $75k-$100k, and 9

contracts valued at $50-$75k were awarded

12.3. 150 contracts (70%) were

assessed by the contract owners as being low risk, 54 contracts (25%) were

assessed as being medium risk, and 8 contracts (3.7%) assessed as high risk

12.4. Of the 32 contracts with

a value greater than $50,000 9 completed an RFP/RFQ process, 19 considered

local suppliers, and 14 confirmed living wage payments

12.5. There are 27 contracts

expiring in the next three months that will be subject to post contract

evaluation.

13. Procurement information is

now available ‘live’ at organisation and group level utilising the

Power BI Dashboard. Further levels of drill down detail are available at group,

service and contract manager levels. A demonstration of the reporting

data base could be provided to the FARS at a future meeting if required.

14. On average, five contracts

are being generated across the organisation every week, with the contract being

one part of a three stage (planning, sourcing and managing) process. The

contract and deliverables are managed by the individual contract managers.

15. A contract expiring

triggers an automated evaluation process with the contract owner, collecting

data on advisability of supplier future use based on timeliness, budget

performance, meeting specification, health and safety performance, shared HBRC

environmental vision, professionalism and any learnings from the

project/contract delivery.

Next Steps

16. Procurement monitoring

will continue to develop as an iterative process with the procurement team

applying a continuous improvement to meet organisational need.

17. Over the next six months

there will be a review to increase the use of ‘All of Government’

contracts, which may provide an opportunity for further cost savings.

18. The development of an

ongoing internal procurement training and procurement communications programme.

19. The design and

implementation of an internal procurement audit programme in conjunction with

the Strategic Risk Framework currently being developed.

20. Continued engagement with

the Hawke’s Bay councils to develop and implement a Regional Strategic

Procurement Plan (attachment 3). This will include utilising the results of the

Procurement Capability Index survey being undertaken in October 2020.

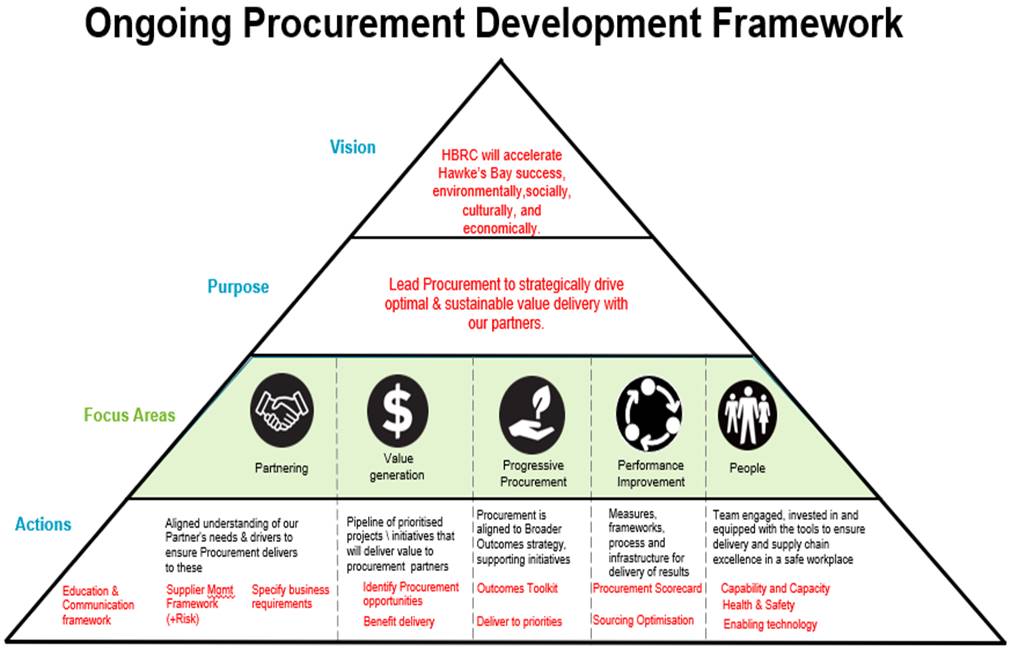

Strategic Fit

21. The development of a

centralised procurement and contract management function has assisted HBRC to

adopt best procurement practice, to support HBRC strategic goals associated

with Climate.Smart.Recovery.

Decision Making

Process

22. Council

and its committees are required to make every decision in accordance with the

requirements of the Local Government Act 2002 (the Act). Staff have

assessed the requirements in relation to this item and have concluded:

22.1. The

decision does not significantly alter the service provision or affect a

strategic asset.

22.2. The use

of the special consultative procedure is not prescribed by legislation.

22.3. The

decision is not significant under the criteria contained in Council’s

adopted Significance and Engagement Policy.

22.4. Any decision of the

sub-committee is in accordance with the Terms of Reference and decision-making

delegations adopted by Hawke’s Bay Regional Council 25 March 2020,

specifically the Finance, Audit and Risk Sub-committee shall have

responsibility and authority to:

22.4.1. Receive the internal and

external audit report(s) and review actions to be taken by management on

significant issues and recommendations raised within the report(s)

22.4.2. Ensure that recommendations

in audit management reports are considered and, if appropriate, actioned by

management.

|

Recommendations

That the

Finance, Audit and Risk Sub-committee:

1. Reviews the

updated draft Procurement Policy and Manual and accepts the proposed changes

as highlighted.

2. Receives and

notes the reporting metrics provided for the period 1 July 2019 to 30 June

2020.

3. Recommends

that the Corporate and Strategic Committee adopts the Procurement Policy and

Manual with amendments as proposed.

|

Authored by:

|

Mark Heaney

Manager Client Services

|

|

Approved by:

|

Jessica

Ellerm

Group Manager

Corporate Services

|

|

Attachment/s

|

⇩1

|

Revised

Procurement Policy 2020

|

|

|

|

⇩2

|

Draft Revised

Procurement Manual

|

|

|

|

⇩3

|

Procurement

Development Framework 2020

|

|

|

|

Revised

Procurement Policy 2020

|

Attachment 1

|

|

Draft Revised Procurement

Manual

|

Attachment 2

|

|

Procurement Development

Framework 2020

|

Attachment 3

|

HAWKE’S BAY REGIONAL COUNCIL

Finance

Audit & Risk Sub-committee

Wednesday 12 August 2020

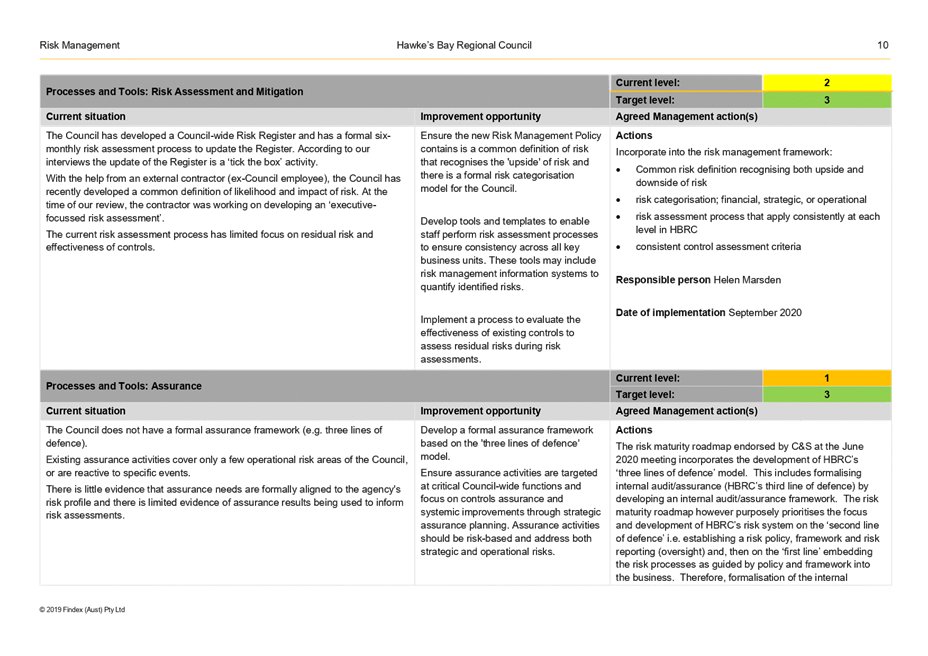

Subject: Risk Maturity

Reason for Report

1. This item

introduces to the Committee the draft risk management policy (attachment 1),

the draft risk management framework (attachment 2), and Crowe’s finalised

internal audit on HBRC’s enterprise risk management maturity assessment (attachment

3).

Officers’ Recommendation(s)

2. Council

Officers recommend that Finance Audit and Risk Sub-Committee (FARS) members:

2.1. approve both

the HBRC Risk Management Policy and Framework as proposed, for recommending to

the Corporate & Strategic Committee for adoption

2.2. consider

Crowe’s report on HBRC’s enterprise risk management maturity

assessment

2.3. note the risk

maturity roadmap (attachment 4) as amended to include an internal assurance

framework in phase III.

Executive Summary

3. At the

Corporate and Strategic (C&S) Committee meeting held on 10 June 2020

external consultant Shash Davé from Ridgbak Consulting presented a

high-level risk maturity assessment for HBRC. That assessment highlighted

HBRC Risk Management System (RMS) needed to mature to ensure that it remained

current and added value to the organisation. At the same meeting and in

response to Shash Davé’s risk maturity assessment a risk maturity

roadmap for HBRC was presented and endorsed by the Committee.

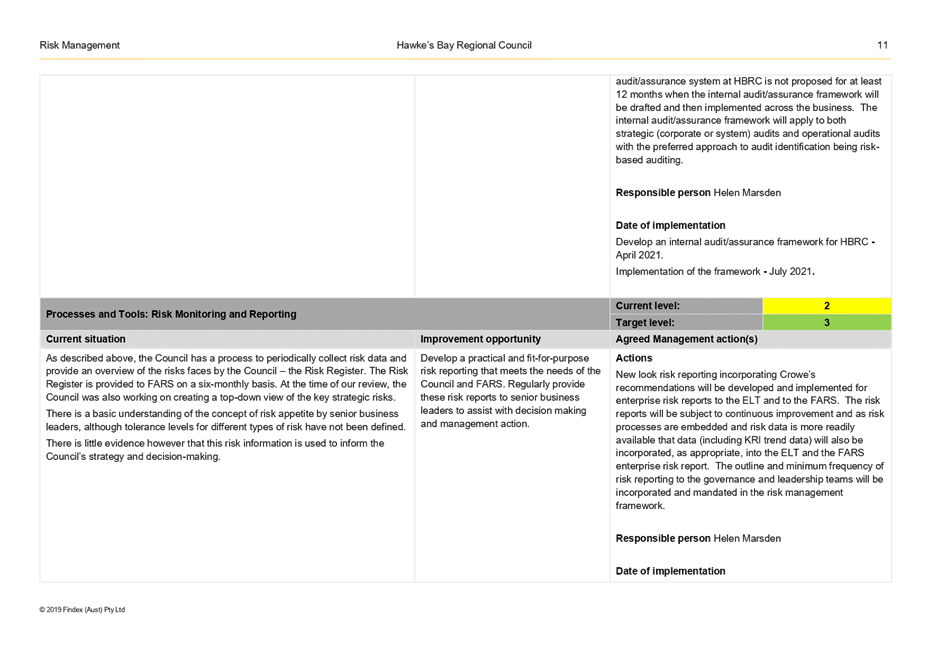

4. As part of risk

maturity roadmap, a risk management policy and risk management framework was

developed. Therefore, this paper seeks endorsement from the FARS that the

scope of these documents adequately addresses the desired risk system

maturity. At the time of the C&S meeting on 10 June 2020, Crowe as

part of the FY20 internal audit plan had commenced, but not finalised, an

internal audit that was to provide a detailed assessment of HBRC RMS maturity.

That audit report is now finalised and as it relates to risk maturity has been

included with this paper. Crowe’s audit report reinforced the need

to mature HBRC’s RMS. Crowe’s internal audit report findings

and recommendations were reviewed against the risk maturity roadmap.

Phase III of the risk maturity roadmap was subsequently updated to include the

development of an HBRC internal assurance framework. All other internal

audit report recommendations and findings were adequately addressed by the

roadmap.

Background

5. All

organisations (large and small) are faced with operating in a challenging and

rapidly changing world. This changing external business environment

brings an increase in uncertainties and therefore increase in risks to

organisations as they attempt to effectively set business objectives and

efficiently execute on those objectives. Some examples of changes in the

external environment include: rapidly changing stakeholder demands and expectations

(e.g. social fairness, cultural, environmental, and economic), changing

regulatory/political or legal landscape, increase reliance on third parties,

and advancements of technology that maybe either a business disruptor or

enabler.

6. By definition ‘risk’

is referred to as uncertainty on objectives. Therefore,

acknowledging the rapidly changing world, Council along with the ELT identified

the growing importance of a robust and embedded risk management system

(RMS). An external consultant, Shash Dave from Ridgbak Consulting, was

commissioned to undertake a high-level risk maturity assessment. In

addition, as part of the FY20 annual internal audit programme, Crowe undertook

an audit to review the design and operating effectiveness of HBRC’s

RMS. The maturity assessment undertaken by Shash Davé along with

the audit findings by Crowe identified the need for HBRC’s risk system to

mature so that it becomes: formalised, structured and embedded into the

business.

7. Acknowledging

the need to mature HBRC’s RMS, C&S at the meeting on 10 June 2020

endorsed a four phased risk maturity roadmap that was developed in conjunction

with the external consultant, Shash Davé. This paper covers the

execution of components of phase I to III of the risk maturity roadmap,

specifically the development of both HBRC’s risk management policy and

framework. Several key decisions were required to right-size the

formalised RMS for HBRC, these decisions are outlined in the discussion section

of this paper. Essentially, the context of the RMS as it applies to HBRC

is outlined in the risk management policy. While the scope of the RMS as

it applies to HBRC is outlined in the proposed risk management framework.

8. Due to the

six-monthly reporting cycle of risks to the FARS, management agreed to

fast-track the development of the risk management policy and framework from

phase III into phase I. These were formalised so that the proposed risk

management policy and framework could be used as the basis to revise

HBRC’S enterprise risks. The revised enterprise risks are included

in the August 2020 risk report to the FARS. Both the draft risk

management policy and framework were ratified by the Executive Leadership Team

(ELT) at their meeting held on Monday 29 June 2020, and then workshopped with

Councillors at 15 July 2020 FARS workshop.

9. It is noted

that when Shash Davé presented his high-level risk maturity assessment

and risk maturity roadmap to the C&S on 10 June 2020, Crowe’s HBRC

risk management maturity assessment that formed part of the FY20 internal audit

plan was not finalised. That internal audit is now finalised, and it is

noted that Crowe in conjunction with staff reviewed the audit report findings

and recommendations against the risk maturity roadmap. Subject to the inclusion

of a requirement to develop an internal assurance framework the maturity

roadmap adequately addresses Crowe’s audit findings. The

development of an internal assurance framework has been added to phase III of

the roadmap.

10. Crowe’s risk

management maturity internal audit is summarised as follows. Crowe used

the All-of-Government (AoG) enterprise risk maturity assessment framework as

the benchmark for the audit. As part of the audit, Crowe with input from

HBRC’s staff determined that given HBRC’s size, scale and mandate a

minimum maturity level of ‘3’ would need to be attained using the

AoG model. It was noted that a maturity level of ‘3’ would

only drive a level of compliance rather than ‘value add’ and that

HBRC’s risk maturity roadmap that was endorsed by the Corporate and

Strategic (C&S) Committee at the meeting on 10 June 2020 would likely take

HBRC to a maturity level beyond level ‘3’.

11. The

audit report determined across all dimensions within the AoG enterprise risk maturity

framework HBRC’s scored below the minimum threshold of

‘3’. The framework dimensions that noted the largest maturity

gaps included:

11.1. Leadership and

Direction:

11.1.1. Establishing a long-term

vision for risk management to provide a frame that enables continuous

improvement

11.1.2. Adequately trained

specialist risk resources across the business (e.g. BU Risk Champions) that can

assist with embedding a consistent approach to risk identification, risk

assessment, risk management and risk escalation

11.2. People

and Development

11.2.1. Development of a risk policy

that identifies of clear risk roles and responsibilities that is supported by

adequate training

11.3. Process and Tools

11.3.1. An absence of a formal

‘three lines of defence’ assurance framework that guides the

corporate and operational annual internal audit programme and the execution of

the individual audits within those programmes.

12. The

full risk assessment maturity gaps using the AoG model is outlined in the

spider diagram below. Full details for each individual dimension and the

specific gaps can be found in the full Crowe internal audit report.

13. Lastly, within the report

Crowe outlined specific ‘success factors’ that HBRC will need to

maintain throughout the risk maturity journey. These success factors as

detailed on page five of the report and are italics below:

13.1. Buy-in and tone at

the top. Risk management practices are more effective when they are supported

by an appropriate ‘tone at the top’, when senior leaders are

actively involved in risk management activities, encourage risk-related

conversations and apply risk-based decision-making

13.2. Clear direction

should be provided by the Council’s Finance, Audit and Risk Subcommittee

(FARS) in line with the responsibilities described in its Terms of Reference

(updated in March 2020). FARS should define what risk information it should

receive, provide input into the Council’s risk appetite, assist

management in risk assessment, etc

13.3. Risk culture.

Improving risk management processes requires the Council not only have the

right processes and tools, but also embracing a culture of risk awareness and

transparency. Every staff member has a role to play and each staff member

should be encouraged to actively participate in the Council’s risk

management activities – be it risk identification, communication or

response

13.4. To support the above

point, the Council should support its staff with relevant risk-related training

and awareness programme. The training should cover the roles and responsibilities

of staff, provide an overview of the Council’s risk management framework

and processes and available risk management tools.

Discussion

14. The following section

outlines the key decisions recommended by the ELT regarding the scope and

context of HBRC’s RMS. These decisions are documented in either the

proposed risk management policy or framework:

14.1. Enterprise risks will be

reviewed by the ELT rather than establishing a separate Executive Risk

Committee that focusses solely on risk management. The ELT are required

to have a standing item on the ELT agenda to receive HBRC’s enterprise

risks at least four times per year

14.2. Each business unit (BU)

will appoint a BU Risk Champion to coordinate and oversee that BU risk

activities. BU Risk Champions are required to attend risk forums to

aggregate HBRC’s risks

14.3. The risk vision of

HBRC’s RMS be: All HBRC staff take responsibility for owning

HBRC’s risks with consistent and transparent risk intelligent decision

making

14.4. The frequency of the

formal risk reporting continues at least every six months to the FARS while now

at least quarterly to the ELT

14.5. The formal

identification, analysis and aggregation of risks including the use of

‘bowtie analysis’ be undertaken for all tier one and tier two

critical risks

14.6. A three-rating approach

be applied for control assessments being: effective, requires improvement or

ineffective

14.7. A system exists so that

any control correct actions are monitored and tracked until closed.

14.8. The risk likelihood

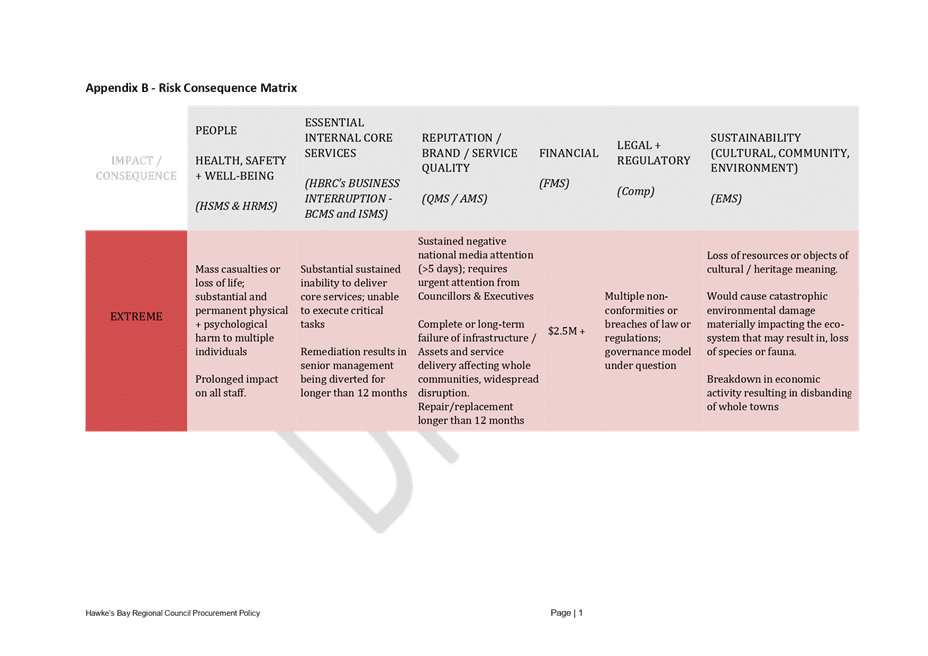

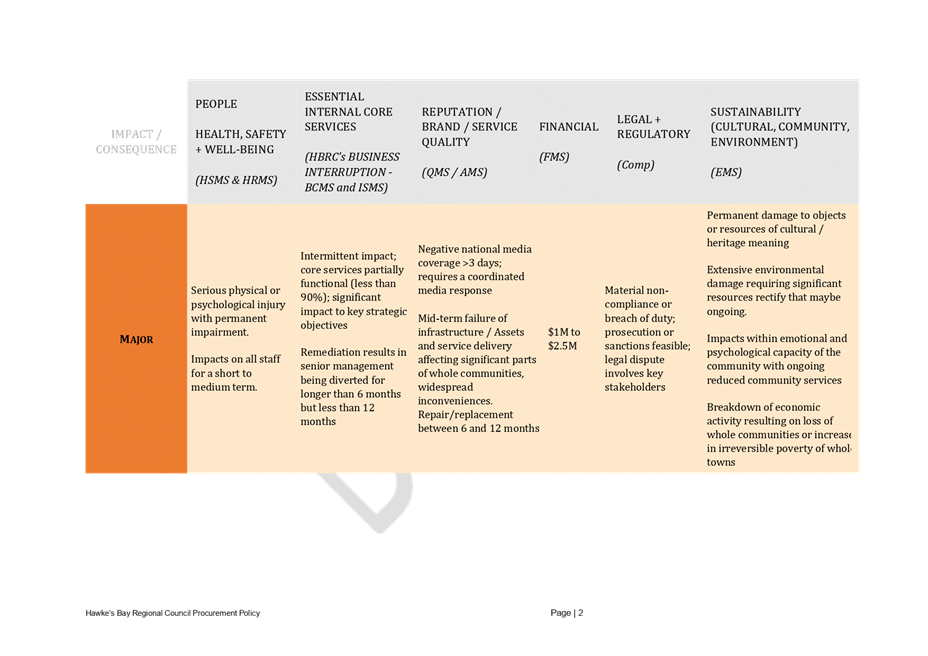

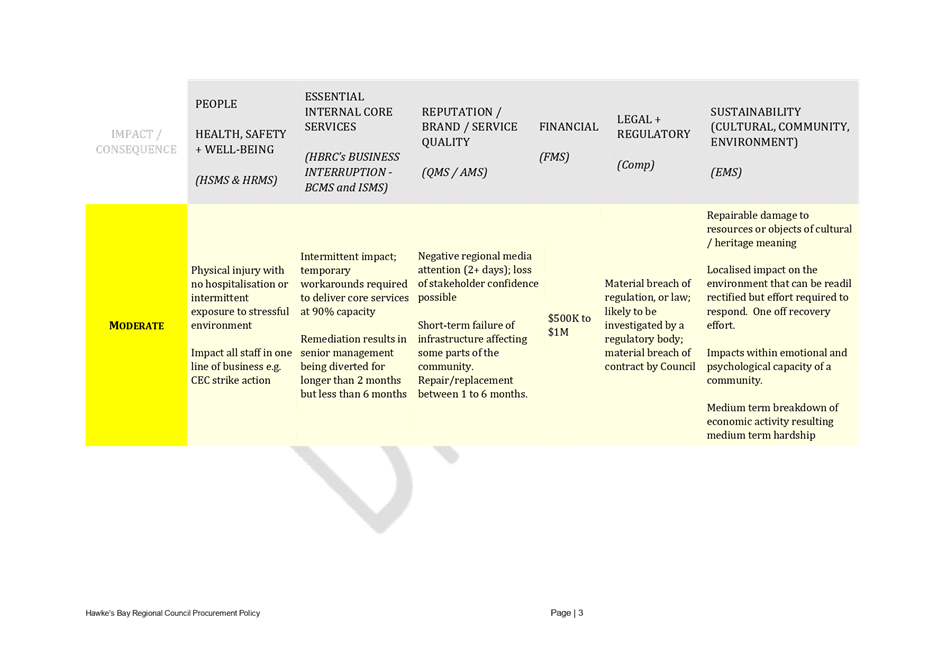

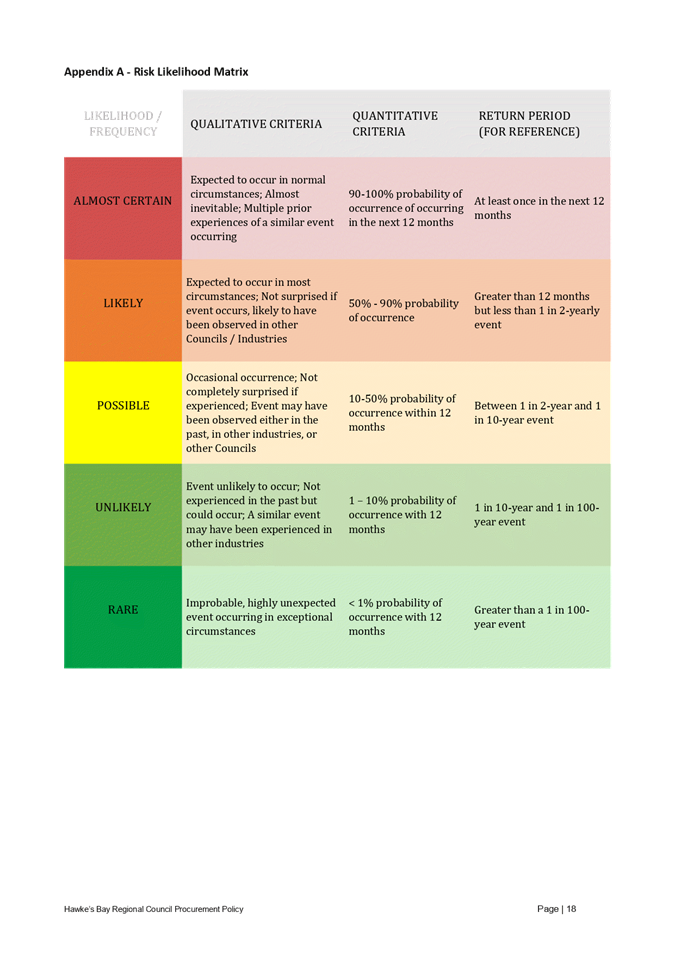

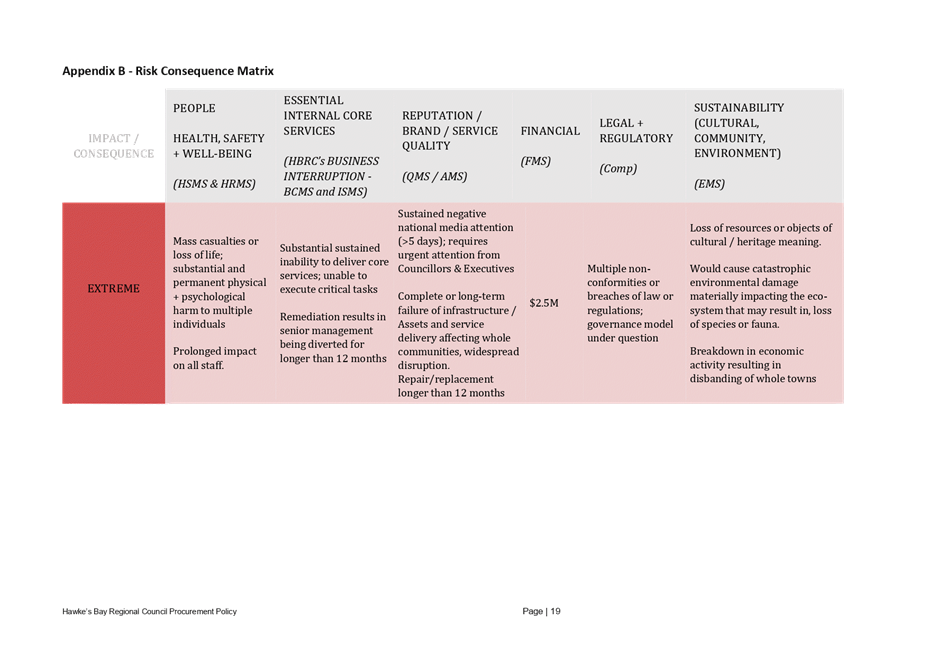

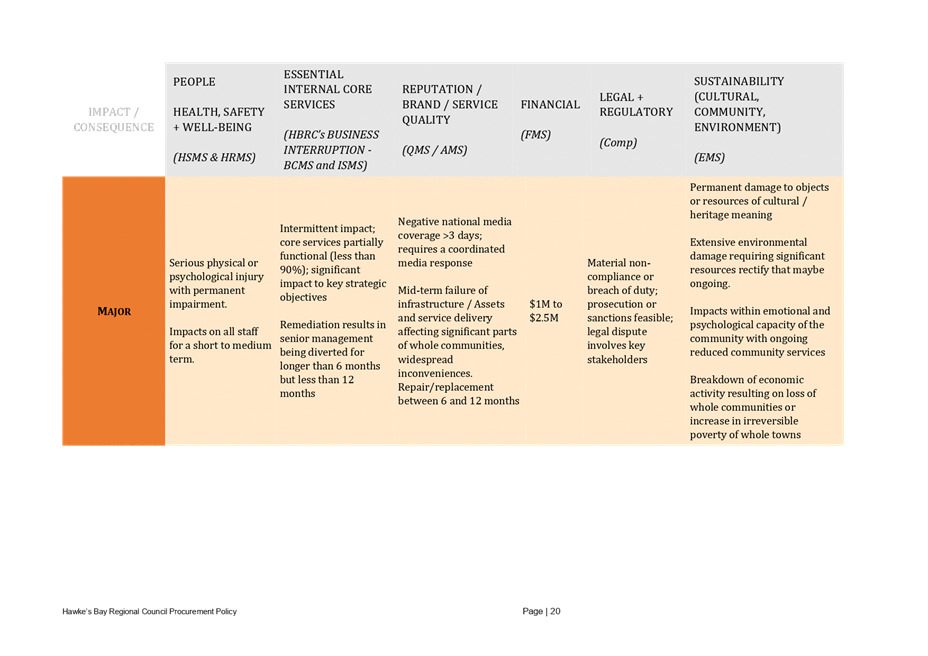

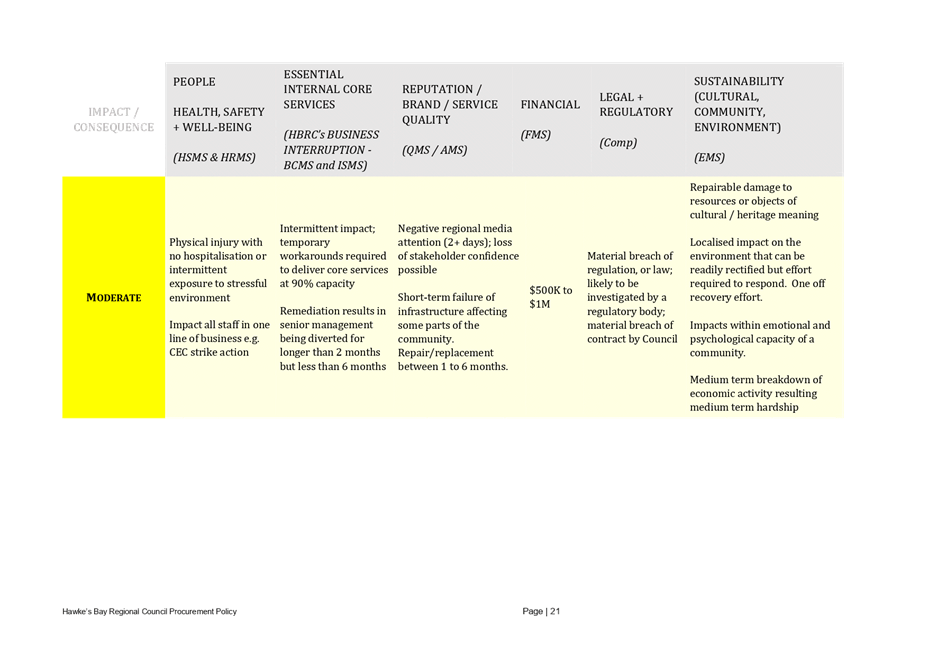

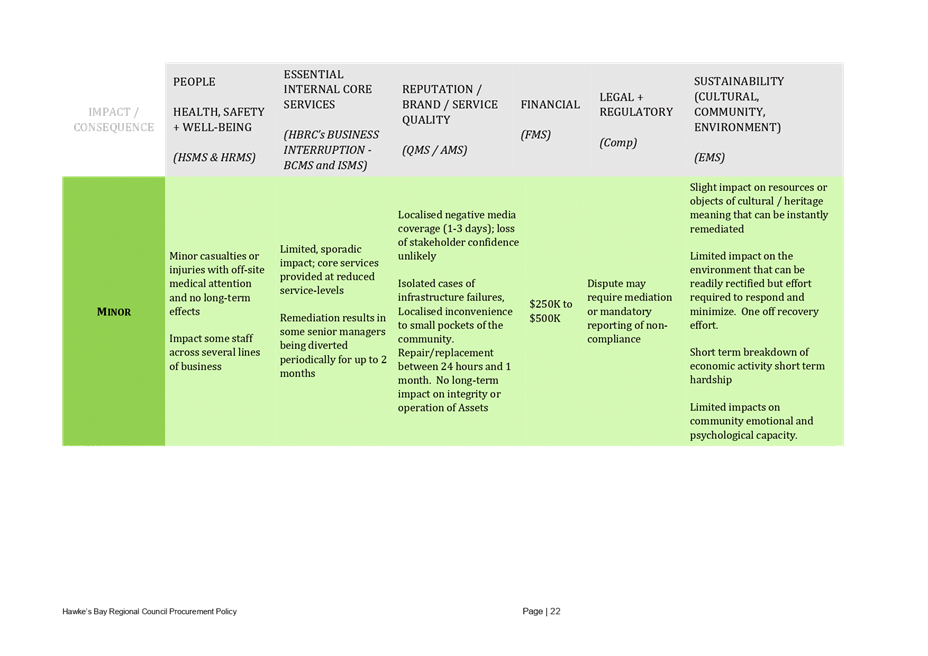

matrix includes both a quantitative and qualitative criterion (see appendix A

of the risk management framework)

14.9. That the risk

consequence matrix includes both a quantitative and qualitative criterion (see

appendix B of the risk management framework)

14.10. The enterprise risk report will include a

risk heatmap to provide a quick snapshot residual risk comparison (see appendix

C of the risk management framework)

14.11. A risk escalation scale for reporting

increasing risks in real time be adopted (see appendix D of the risks

management framework)

14.12. ‘Accepted risks’ those deemed

outside of Council’s risk appetite be reported to the ELT whenever they

receive a risk report, and to the FARS every meeting for the duration that the

risk remains an ‘accepted’ risk. This ensures management

continually scan for new and cost-effective risk mitigations

14.13. The effectiveness and maturity of the RMS

be considered through an annual review of both HBRC’s risk management

policy and framework.

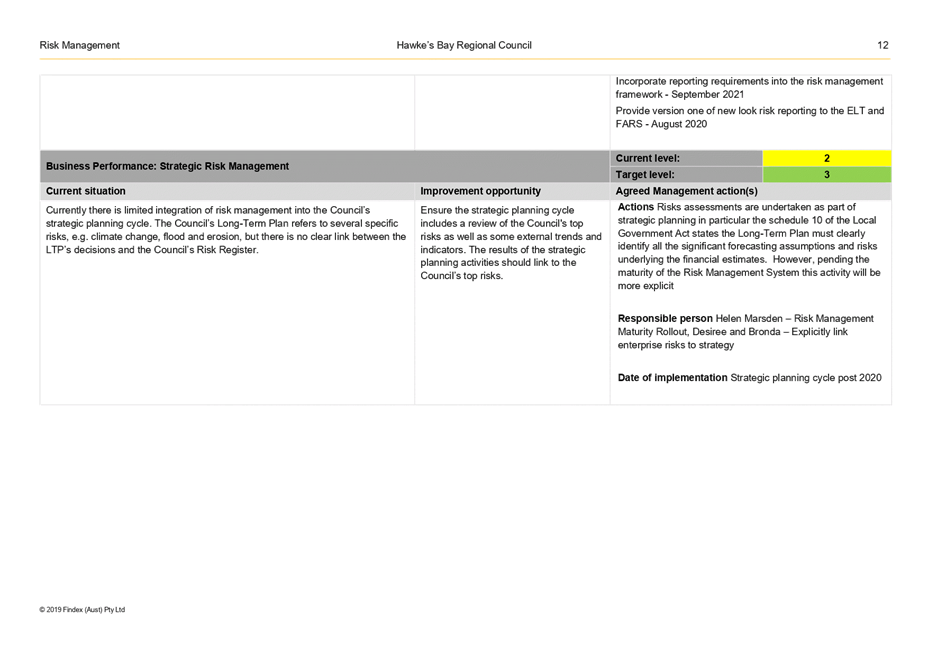

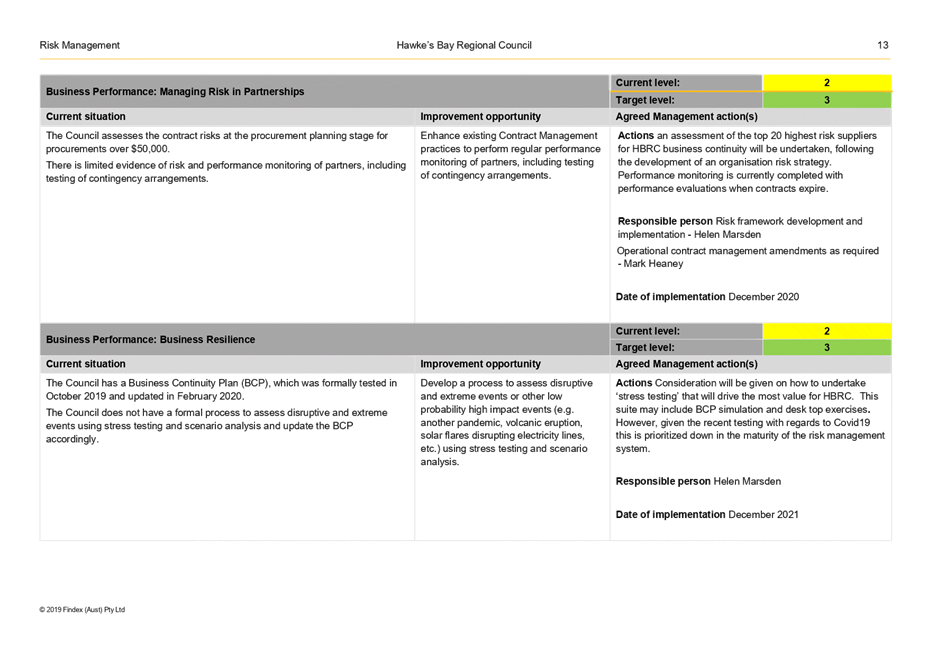

Strategic Fit

15. Maturity of HBRC’s

risk management system contributes towards achieving all strategic

goals/vision. A mature risk system provides consistent risk intelligent

decision making enabling the efficient prioritisation of finite organisational

resources to deliver on strategy.

Considerations of

Tangata Whenua

16. Based on feedback provided

at the Corporate and Strategic Committee meeting the inclusion of

‘objects and resources of cultural and heritage meaning and

importance’ was specifically added to the risk management framework as a

key dimension within the risk consequence matrix. In addition, within the

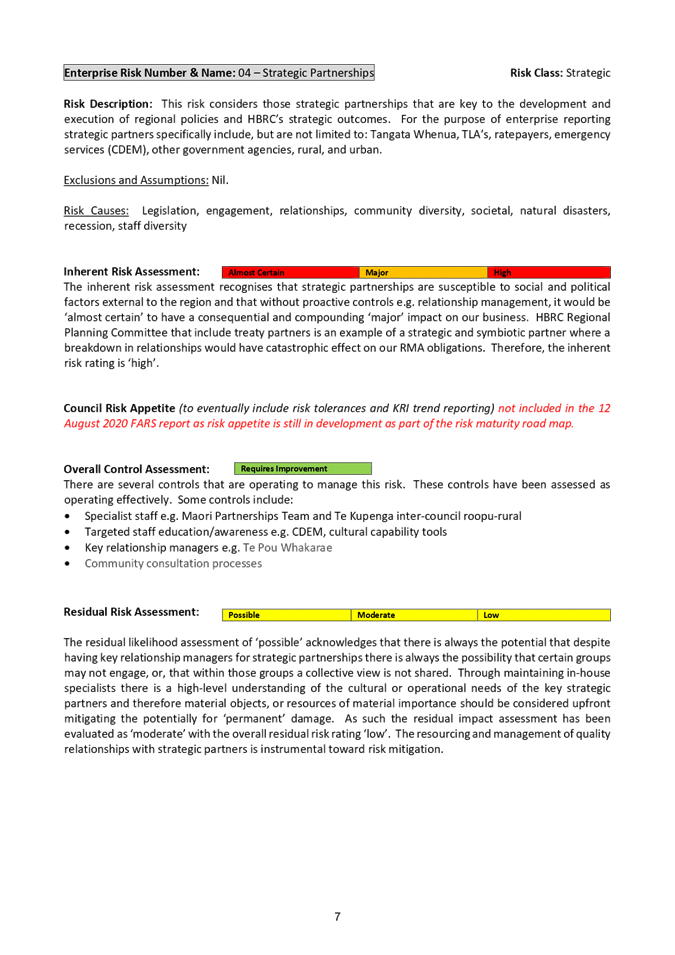

revised suite of risks, under risk 04 ‘Strategic Partnerships’

Tangata Whenua has been specifically detailed.

Financial and

Resource Implications

17. Maturity of the risk

management system is phased to minimise budgetary implications. Some

facilitated workshops will be required to establish the risk appetite with

Council.

Next Steps

18. With the FARS endorsement

of both the Risk Management Policy and Framework, the Risk and Assurance Lead

will develop detailed RMS implementation project plan. The plan will

continue to deliver on the RMS roadmap while embedding into the business risk

practices and processes as described by the risk management policy and

framework.

Decision Making Process

19. Council

and its committees are required to make every decision in accordance with the

requirements of the Local Government Act 2002 (the Act). Staff have assessed

the requirements in relation to this item and have concluded:

19.1. The

decision does not significantly alter the service provision or affect a

strategic asset, nor is it inconsistent with an existing policy or plan.

19.2. The use

of the special consultative procedure is not prescribed by legislation.

19.3. The

decision is not significant under the criteria contained in Council’s

adopted Significance and Engagement Policy.

19.4. The

decision of the sub-committee is in accordance with the Terms of Reference and

decision-making delegations adopted by Hawke’s Bay Regional Council

25 March 2020, specifically the Finance, Audit and Risk Sub-committee

shall have responsibility and authority to:

19.4.1. Review whether Council

management has a current and comprehensive risk management framework and

associated procedures for effective identification and management of the

council’s significant risks in place

19.4.2. Undertake periodic

monitoring of corporate risk assessment, and the internal controls instituted

in response to such risks

19.4.3. report on the robustness of

risk management systems, processes and practices to the Corporate and Strategic

Committee to fulfil its responsibilities.

|

Recommendations

That the Finance, Audit and Risk Sub-committee:

1. receives and considers the “Risk

Maturity” staff report

2. confirms it is comfortable that management actions undertaken or

planned for the future adequately respond to the findings and recommendations

of the Crowe Internal Audit – Risk Management Maturity Assessment

report

3. recommends that the Corporate and Strategic Committee approves both the Risk Management Policy and the Risk Management

Framework as being sufficiently robust to manage Council’s significant

risks.

|

Authored by: Approved

by:

|

Helen Marsden

Risk and Assurance Lead

|

Joanne

Lawrence

Group

Manager Office of the Chief Executive and Chair

|

Attachment/s

|

⇩1

|

draft Risk

Management Policy August 2020

|

|

|

|

⇩2

|

draft HBRC

Risk Management Framework 2020

|

|

|

|

⇩3

|

2020 Crowe

HBRC Risk Management Maturity Assessment Report

|

|

|

|

⇩4

|

Path to Risk

Maturity Exhibits August 2020

|

|

|

|

draft

Risk Management Policy August 2020

|

Attachment 1

|

|

draft HBRC Risk Management

Framework 2020

|

Attachment 2

|

|

draft

HBRC Risk Management Framework 2020

|

Attachment 2

|

|

draft

HBRC Risk Management Framework 2020

|

Attachment 2

|

|

2020

Crowe HBRC Risk Management Maturity Assessment Report

|

Attachment 3

|

|

2020

Crowe HBRC Risk Management Maturity Assessment Report

|

Attachment 3

|

|

2020

Crowe HBRC Risk Management Maturity Assessment Report

|

Attachment 3

|

|

2020

Crowe HBRC Risk Management Maturity Assessment Report

|

Attachment 3

|

|

2020

Crowe HBRC Risk Management Maturity Assessment Report

|

Attachment 3

|

|

Path

to Risk Maturity Exhibits August 2020

|

Attachment 4

|

HAWKE’S BAY REGIONAL COUNCIL

Finance

Audit & Risk Sub-committee

Wednesday 12 August 2020

Subject: Six Monthly Enterprise

Risk Management Report

Reason

for Report

1. This item provides the Finance Audit and Risk Sub-committee (FARS)

with the six-monthly update of Council’s enterprise risk profile.

The update includes:

1.1. a residual

risk rating for each enterprise risk

1.2. control

corrective actions

1.3. supporting

risk information such as known emerging issues or uncertainties that may impact

Council’s risk profile.

Officers’ Recommendation(s)

2. Council

Officers recommend that FARS members:

2.1. note the

revised enterprise risks, the enterprise risk assessments for the revised

risks, and the ‘new look’ risk reporting

2.2. note the

control corrective actions that are in progress

2.3. note the

supporting risk information.

Executive Summary

3. As part of

HBRC’s enterprise risk management system (RMS) maturity a risk management

policy and risk management framework were developed. Using both the risk

management policy and framework the enterprise risks were revised and a

‘new look’ risk report produced. The revised risks and

‘new look’ risk report has been used to present HBRC’s

enterprise risks to the FARS for this reporting period.

4. The August 2020

risk report noted that no enterprise risks had a residual risk rating of

‘high’. While the overall control assessment for some

enterprise risks have been noted as ‘requires improvement’,

controls for enterprise risks were working to a satisfactory level to mitigate

any ‘high’ residual risk rating.

5. Seven

enterprise risks have an overall control assessment noted as ‘requires

improvement’. Of those seven risks three have been identified as a

key focus for corrective actions and resource prioritisation. Those risks

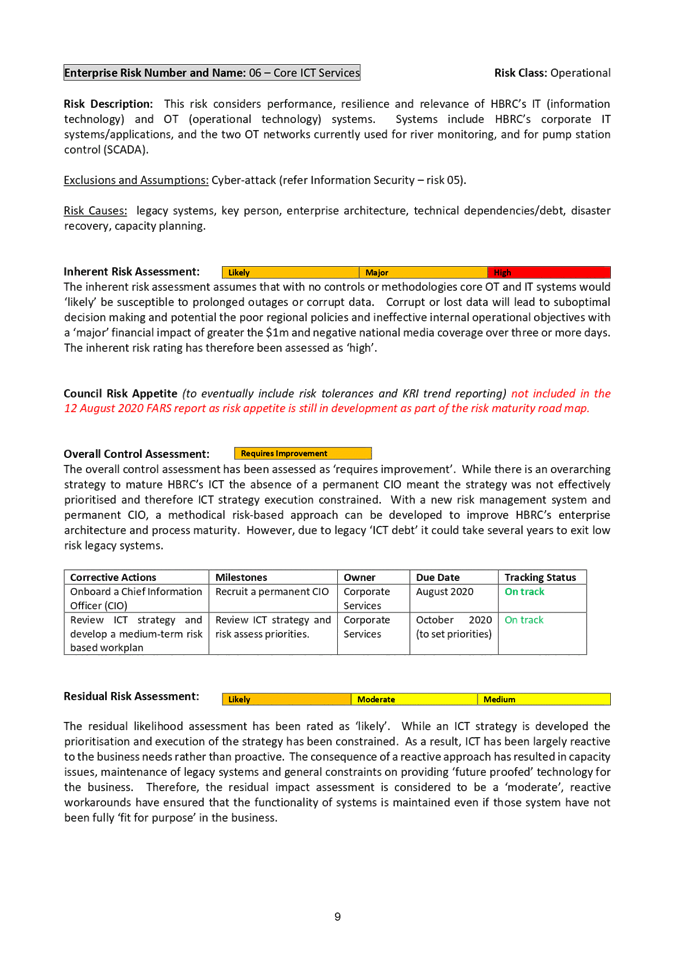

include; risk 06 – Core ICT Services, risk 09 – People Capability,

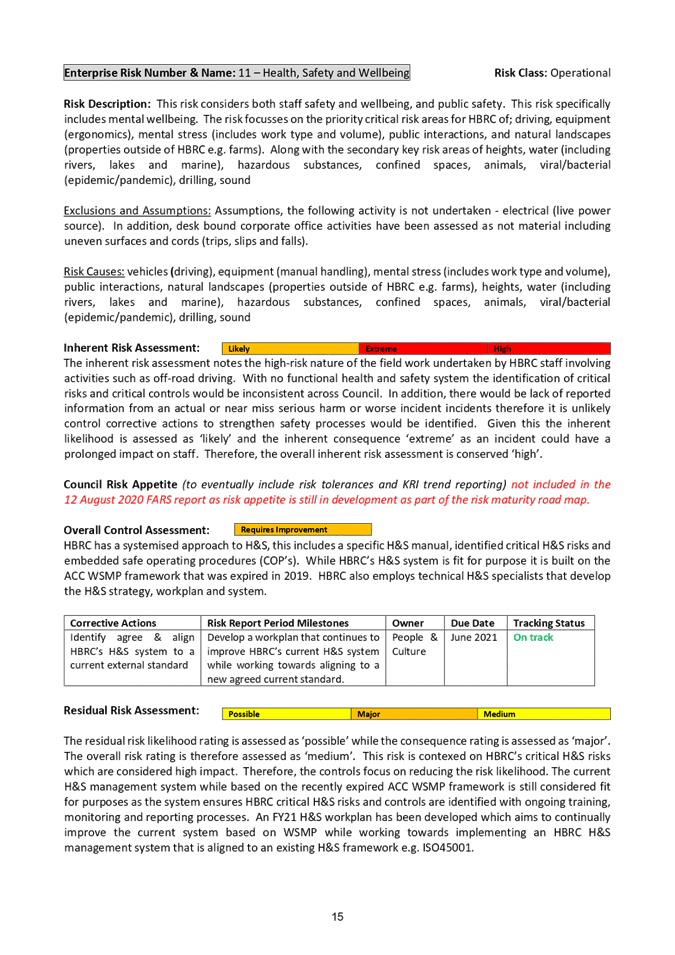

and risk 11 – H&S and Wellbeing.

6. The remaining

risk that had control assessments noted as ‘requires improvement’

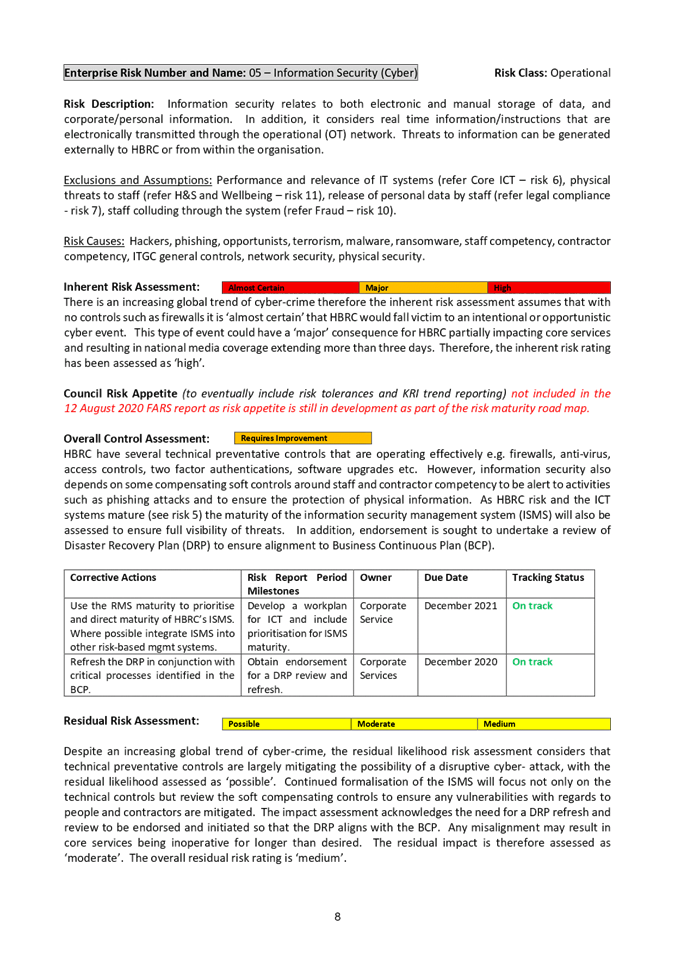

included: risk 01 – Strategic, risk 05 – Information Security, risk

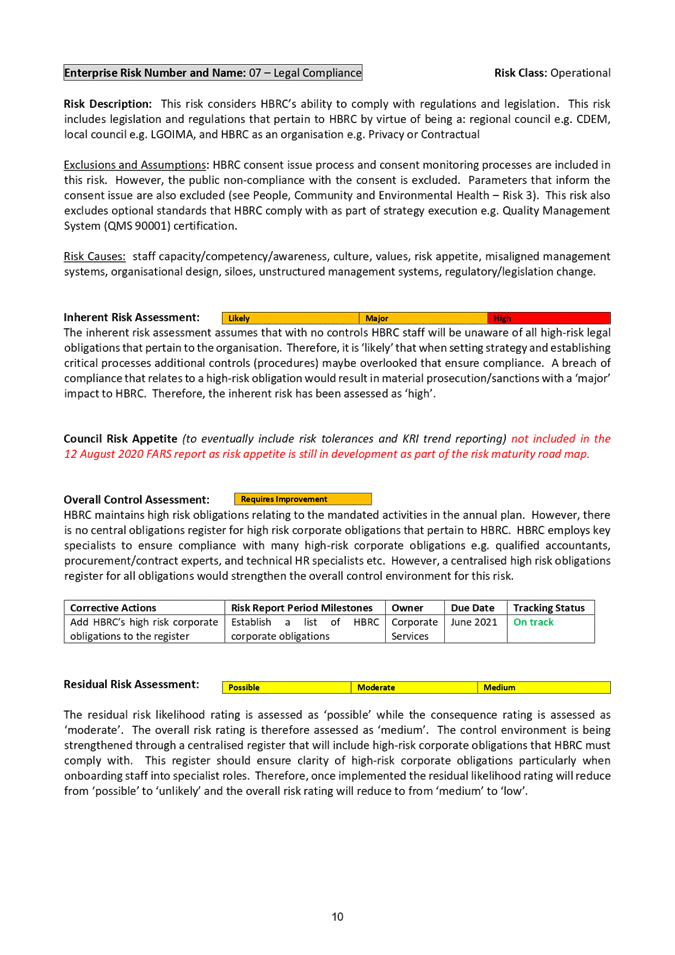

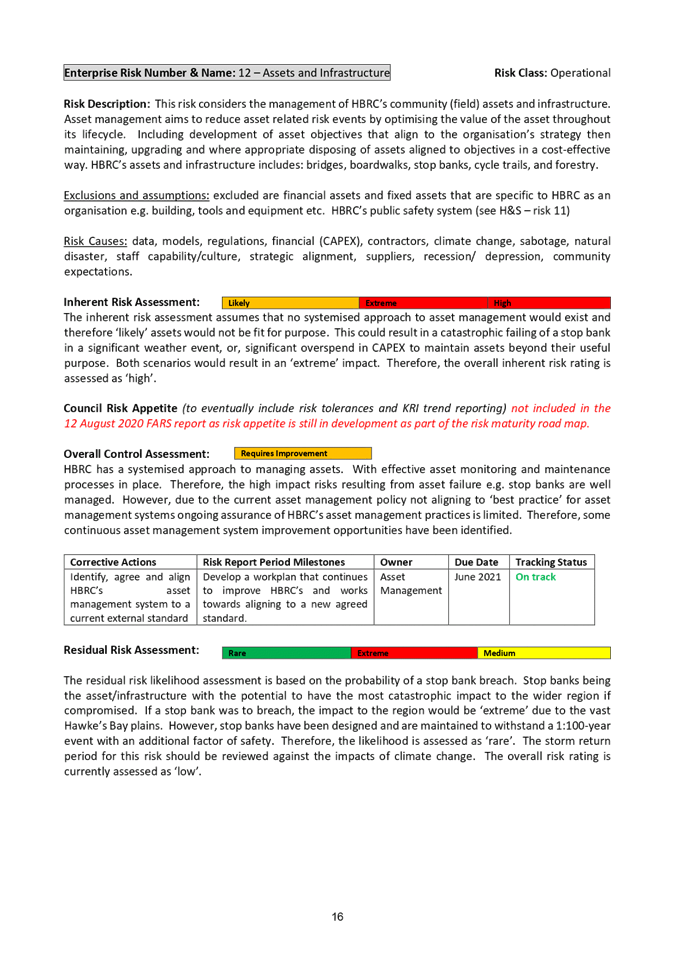

07 - Legal Compliance, and risk 12 - Assets and Infrastructure. However,

the control corrective actions for these risks while important where not deemed

as substantive and critical to mitigating HBRC’s residual risk profile.

Background

7. At the

Corporate and Services (C&S) Committee meeting on 10 June 2020 the RMS

maturity roadmap was endorsed. Included in the RMS maturity roadmap was

the development of both a single risk management policy and framework.

These documents are intended to standardise risk management activities across

HBRC including processes to identify and assess risks and risk controls.

8. Due to the

six-monthly reporting cycle of enterprise risks to the FARS being August 2020,

management agreed to fast-track the development of the risk management policy

and framework from phase III to phase I of the RMS maturity roadmap. This

was to enable the August 2020 FARS enterprise risk report to contain revised

enterprise risks based on a more mature RMS with guidance from the draft risk

management policy and framework. Both the draft risk management policy

and framework were ratified by the Executive Leadership Team (ELT) at the ELT

meeting on 29 June 2020, and also permitted in principle by members of the FARS

at 15 July 2020 FARS workshop.

9. With both the

risk management policy and framework being ratified by the ELT and permitted in

principle by the FARS. The enterprise risks were revised and ‘new

look’ risk report developed (attachment 1).

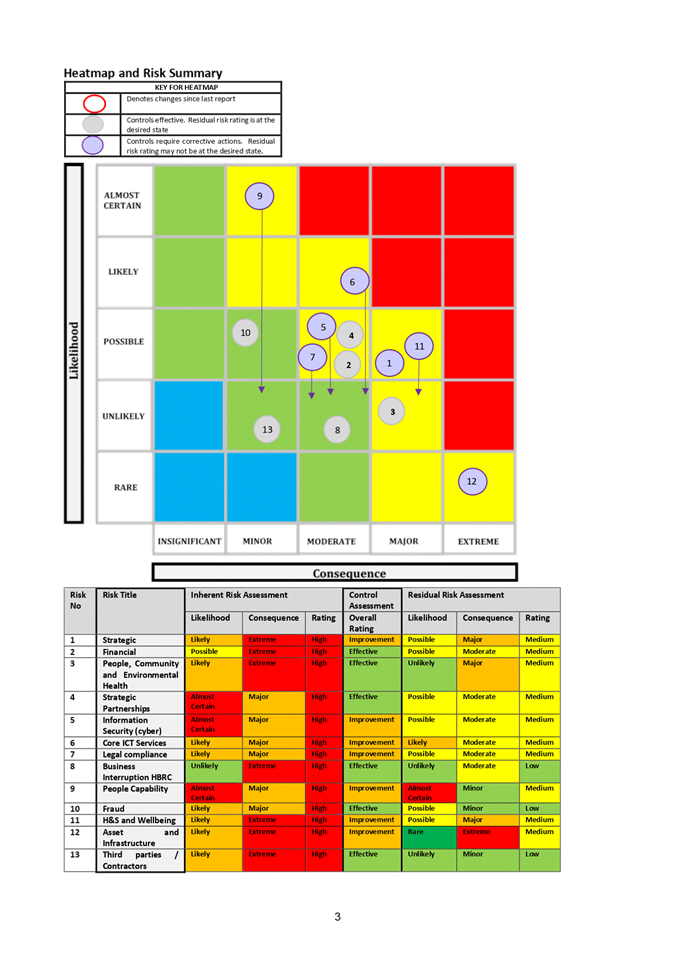

10. The ‘new look’

risk report provides; supporting risk information, a snapshot comparison of the

residual enterprise risks presented through the risk heat map, and a risk

summary ‘one-pager’ for each enterprise risk. The risk

‘one pager’ for each risk contains:

10.1. a risk description

10.2. risk exclusions and

assumptions

10.3. risk causes

10.4. an inherent risk

assessment and summary

10.5. a high-level control

summary

10.6. an overall control

assessment and where applicable control corrective actions, and

10.7. a residual risk

assessment and summary.

11. It should be noted that

due to the tight timeframe between completing the ‘final’ draft of

both the risk management policy and framework, revising the enterprise risk

with ELT and developing the risk ‘one-pagers’ has been stretched;

not all bowties for each enterprise risk were finalised and workshopped.

As per the RMS maturity road each enterprise risk will continue to be mapped

using bowtie analysis over the next quarter. The bowtie analysis will

strengthen the identified risk causes and risk controls therefore further

enhancing the residual risk assessment and allowing continual improvements of

the risk report to FARS for the next six-monthly reporting period.

12. The revised enterprise

risks, risk assessments, and risk one-pagers were formally discussed by the ELT

at the ELT meeting on 3 August 2020. It is noted that full implementation

of the risk management framework requires a structured approach to risk

aggregation through a designated business unit (BU) Risk Champions.

Implementation of the risk aggregation process will occur over the next six

months as part of the RMS risk maturity roadmap therefore BU Risk Champions

have not yet been assigned. Consequently, for this six-monthly report to

the FARS as an interim solution the enterprise risk and control assessments

were discussed where applicable with the Tier 3 staff member responsible for

the management of that risk. Discussions with Tier 3 staff were done

ahead of the risk report being presented to the ELT to provide bottom up risk

insights and risk-based challenge to the ELT in lieu of the structured risk aggregation

process.

Discussion

13. The following section

provides staffs summary of the enterprise risk report that is attached.

It is noted that no enterprise risks had a residual risk

rating of ‘high’. While the overall control assessment for

some enterprise risks have been noted as ‘requires improvement’

controls for enterprise risks were working to a satisfactory level that has

mitigated any high residual risk rating.

14. Seven enterprise risks

have an overall control assessment noted as ‘requires improvement’.

Of those seven risks three have been identified as a key focus for corrective

actions and resource prioritisation. Those risks include; risk 06 –

Core ICT Services, risk 09 – People Capability, and risk 11 – H&S

and Wellbeing.

15. Reason for prioritising

the control corrective actions for these risks include:

15.1. Risk 06 – Core ICT

Services is considered a core corporate competency that provides reliable

information for good decision making, process automation, and consistency of

output. Therefore, effective ICT is a foundational function that enables

an organisation to strive for excellence as it executes its

strategy.

15.1.1. The control corrective

actions for this include the onboarding of a permanent Chief Information

Officer (CIO), and the proactive review of the ICT strategy that risk assesses

priorities. The ICT strategy review will be led by the newly appointed

CIO once fully on-boarded.

15.2. Risk 09 – People

Capability, the control corrective actions identified are key mitigations to

this risk. In addition, people capability is a core

corporate competency for good decision making and the operational execution of

strategy.

15.2.1. The control corrective

actions for this risk include implementation of the new ELT structure to

strengthen HBRC leadership. A cohesive ELT should reduce the negative

impacts of silos and can proactively lead the desired corporate culture

15.2.2. The recruitment of a People

and Culture (P&C) Manager who using a new P&C strategy will proactively

drive improvement to P&C processes and controls that ensure HBRC maintains

the ‘right’; people capacity, competency and culture.

15.3. Risk 11 – H&S

and Wellbeing, people safety and wellbeing is one of Council’s core

commitments. From the Health and Safety internal audit undertaken in 2018

nine recommendations are still being worked on and therefore H&S remains a

key focus area. A full work programme has been developed and additional staff

resourcing put in place.

15.3.1. The control corrective

actions for this risk are the development of a work plan that will continue to

mature HBRC’s H&S system to an agreed and recognised standard.

The previous ACC WSMP framework that HBRC used was retired late 2019.

16. In addition to the risk

corrective actions that have been prioritised above the enterprise risk report

also identified control improvements for, risk 01

– Strategic, risk 05 – Information Security, risk 07 - Legal

Compliance, and risk 12 - Assets and Infrastructure. However, the control

corrective actions for these risks while important where not assessed as

substantive and critical to mitigating HBRC’s residual risk profile.

17. The residual risk ratings

for each enterprise risks took into consideration supporting risk information

outlined in the risk report. Specifically, the continued uncertainty from

the Covid19 global pandemic, and the internal audit close out reports for; data

analytics, risk management system maturity assessment, and the actions

follow-up from previous audits.

Next Steps

18. Risk and Assurance Lead to

continue to implement risk maturity actions as guided by the risk management

framework that will support the continued improvement of the six-monthly FARS

enterprise risk report.

19. The Risk and Assurance

Lead to track control corrective action progress.

Decision Making

Process

20. Council

and its committees are required to make every decision in accordance with the

requirements of the Local Government Act 2002 (the Act). Staff have

assessed the requirements in relation to this item and have concluded:

20.1. The

decision does not significantly alter the service provision or affect a

strategic asset and is not inconsistent with an existing policy or plan.

20.2. The use

of the special consultative procedure is not prescribed by legislation.

20.3. The

decision does not fall within the definition of Council’s policy on

significance.

20.4. The

decision of the sub-committee is in accordance with the Terms of Reference and

decision-making delegations adopted by Hawke’s Bay Regional Council

25 March 2020, specifically the Finance, Audit and Risk Sub-committee

shall have responsibility and authority to:

20.4.1. review

whether Council management has a current and comprehensive risk management

framework and associated procedures for effective identification and management

of the council’s significant risks in place, and

20.4.2. undertake

periodic monitoring of corporate risk assessment, and the internal controls

instituted in response to such risks

20.4.3. report the

robustness of risk management systems, processes and practices to the

Corporate and Strategic Committee to fulfil its responsibilities.

|

Recommendations

That the Finance, Audit and Risk Sub-committee:

1. receives and considers the “Six Monthly Enterprise Risk

Management” staff report

2. confirms its confidence that Council

management has undertaken an effective risk identification and risk

management process for Council’s significant risks, and that actions

taken to date to mature HBRC’s risk management system are in line with

Council’s expectations as provided to the 10 June 2020 Corporate and

Strategic Committee meeting in the Risk Maturity Roadmap.

|

Authored by:

|

Helen Marsden

Risk and Assurance Lead

|

|

Approved by:

|

Jessica

Ellerm

Group Manager

Corporate Services

|

Joanne

Lawrence

Group Manager Office of the Chief Executive

and Chair

|

Attachment/s

|

⇩1

|

August 2020

Enterprise Risk Report

|

|

|

|

August

2020 Enterprise Risk Report

|

Attachment 1

|

|

August

2020 Enterprise Risk Report

|

Attachment 1

|

HAWKE’S BAY REGIONAL

COUNCIL

Finance

Audit & Risk Sub-committee

Wednesday 12 August 2020

Subject: Annual 2020-21 Internal

Audit Work Plan

Reason for Report

1. This item

presents the proposed Annual Internal Audit Plan for the 2020-21 financial year

(FY21) for the Sub-committee’s adoption, along with an overview of other

review activities under way across the organisation.

Officers’ Recommendation(s)

2. Council

Officers recommend that the Sub-committee adopts the FY21 Annual Audit Plan as

proposed by Crowe in Attachment 1 and confirms the direction of travel for

management of other types of reviews across the organisation, including LGA

s17a reviews.

Background /Discussion

3. Council’s philosophy toward the annual internal audit plan is

to select areas of the organisation where councillors seek independent

assurance based on perceived organisational risks or opportunities; both of

which can drive business improvement. This proactive approach aligns with good

business practices of continuous business improvement, risk management and

assurance.

4. For the past three years Crowe has been contracted by HBRC to manage

the FARS annual internal audit plan. This agreement was based on a

three-year contract which contained a further one year right of renewal.

HBRC staff have exercised the one year right of renewal and Crowe will manage

the annual internal audit plan for FY21.

5. Crowe has prepared a draft FY21 Annual Internal Audit Plan (attachment

1) with consideration of previous internal audits, insights and observations of

current risks and issues in the local government sector, coverage across HBRC’s

functions and activities, discussions with staff, and available budget.

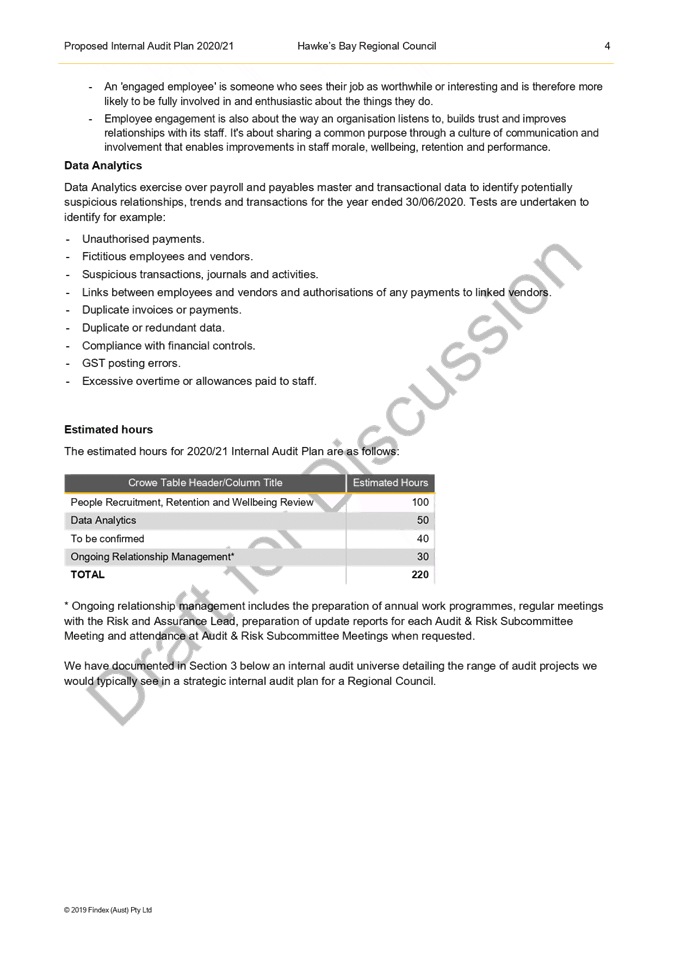

6. The Crowe plan proposes two internal audits and that 40 hours be

retained as audit capacity should a specific risk area arise during the

financial year that the FARS seeks specific assurance on.

7. The two reviews recommended by Crowe are:

7.1. People

Recruitment, Retention and Wellbeing Review: This audit will assess

HBRC’s people recruitment, retention and wellbeing strategies against the

Institute of Internal Auditors Guidance for Auditing Business Functions –

Human Resources. Note this audit does not review the People and

Capability team structure or delivery.

7.2. Data Analytics: currently this audit is a 12-monthly

cyclical review exercised over payroll and payables master and transactional

data to identify potentially suspicious relationships, trends and transactions

for transactions to 30 June 2020.

8. In addition to the above reviews supplementary internal audits

regularly occur across the organisation in the form of operational audits.

Operational audits test the operational effectiveness of HBRC’s codes of

practice in areas such as Health and Safety or Quality.

9. It should be noted that under the proposed risk management framework

any activities, including audits, that identify high risks are required to be

escalated to the Chief Executive and Council, therefore providing some

assurance that any supplementary audits with high risk findings in FY21 will be

visible to the FARS members.

10. At the FARS workshop on 15

July 2020 staff were asked to consider the inclusion of an audit of the

execution of projects to achieve the 24 strategic outcomes in the 2020-21

internal audit programme. There are currently control corrective actions

underway to improve the reporting to Council, with better milestone

progress and trajectory linkages. A review to ensure that the improved

reporting is effective will therefore be included in the 2021-22 annual

internal audit plan.

11. Crowe’s

proposed internal audit plan for FY21 contains a table that lists the suite of

audits that they have undertaken from FY18 to FY20, and other internal audits

undertaken by other providers prior to FY18.

Financial and

Resource Implications

12. Budget has been provided

through the annual plan budget process and provides 220 hours of capacity

for Crowe to manage the FY21 annual internal audit plan.

LGA s17a Reviews

13. The Local Government Act

requires Council to review the cost effectiveness of its service delivery

including options for the governance, funding, and delivery of infrastructure,

services, and regulatory functions. There are currently two such reviews under

way, being:

13.1. S17a Review of the Works

Group – this report is currently being finalised with Management and is

expected to be presented to the November 2020 FARS meeting.

13.2. S17a Biosecurity review

– this review is currently in progress and a high-level update has been

included in the ‘work programme update’ agenda item for this

meeting.

14. These reviews will now be overseen, at a high level, by the Risk and Assurance Lead through

the proposed “Audit Universe” to be developed as part of Risk

Maturity.

Other Review Activities

15. From time

to time reviews may be initiated by a Business Unit (BU) or Group for specific

purposes. It is intended that all significant reviews, right across the

organisation, will be overseen, at a high level, by the Risk and Assurance Lead

through the proposed “Audit Universe” to be developed as part of

Risk Maturity. A preliminary snapshot of current reviews in progress is

attached (attachment 2) for the Sub-committee’s information and feedback.

Decision Making Process

16. Council

and its committees are required to make every decision in accordance with the

requirements of the Local Government Act 2002 (the Act). Staff have assessed

the requirements in relation to this item and have concluded:

16.1. The

decision does not significantly alter the service provision or affect a

strategic asset, nor is it inconsistent with an existing policy or plan.

16.2. The use

of the special consultative procedure is not prescribed by legislation.

16.3. The

decision is not significant under the criteria contained in Council’s

adopted Significance and Engagement Policy.

16.4. The

decision of the sub-committee is in accordance with the Terms of Reference and

decision-making delegations adopted by Hawke’s Bay Regional Council

25 March 2020, specifically the Finance, Audit and Risk Sub-committee

shall have responsibility and authority to:

16.4.1. receive the

internal and external audit report(s) and review actions to be taken by

management on significant issues and recommendations raised within the

report(s)

16.4.2. confirm the

terms of appointment and engagement of external auditors, including the nature

and scope of the audit, timetable, and fees

16.4.3. report the

independence and adequacy of internal and external audit functions to

the Corporate and Strategic Committee to fulfil its responsibilities.

|

Recommendations

That the

Finance, Audit and Risk Sub-committee:

1. receives and considers the “Annual 2020-21 Internal Audit

Work Plan” staff report

2. adopts the 2020-21 Internal Audit Work Plan as proposed.

|

Authored by:

|

Helen Marsden

Risk and Assurance Lead

|

|

Approved by:

|

Jessica

Ellerm

Group Manager Corporate Services

|

Joanne

Lawrence

Group Manager Office of the Chief Executive

and Chair

|

Attachment/s

|

⇩1

|

Crowe

Proposed 2020-21 HBRC Internal Audit Plan

|

|

|

|

⇩2

|

HBRC Audit

Universe Snapshot 2020-21

|

|

|

|

Crowe

Proposed 2020-21 HBRC Internal Audit Plan

|

Attachment 1

|

|

Crowe

Proposed 2020-21 HBRC Internal Audit Plan

|

Attachment 1

|

|

Crowe

Proposed 2020-21 HBRC Internal Audit Plan

|

Attachment 1

|

|

HBRC

Audit Universe Snapshot 2020-21

|

Attachment 2

|

HBRC’s

Audit Universe SNAPSHOT 2020-21

|

RISK

NUMBER & NAME

|

Review(s)

|

Audit (Internal or External)

|

Completed 2019/2020

|

|

1. Strategic

· Decision

· Implementation

· Delivered

|

|

|

Risk

Management Maturity Assessment

|

|

2. Financial

· Market

· Liquidity

· Credit

|

|

Audit

NZ – External Financial Audit

|

|

|

3. People

(Community) and Environmental Health

|

· S17a

Biosecurity review

· Forestry

consenting and regulation review, including sediment erosion control

guidelines

|

|

Water

Management Follow-up Internal Audit

|

|

4. Strategic

Partnerships

|

|

|

|

|

5. Information

Security (incl cyber)

|

|

|

Cyber

Security Internal Audit

|

|

6. Core

ICT Services

|

|

|

|

|

7. Legal

compliance

|

Privacy

Policies review in anticipation of Privacy Act amendments

|

|

|

|

8. Business

Interruption to HBRC

|

Covid19

Debrief

|

|

|

|

9. People

Capability (People Assets)

|

|

People Recruitment, Retention and Wellbeing

Internal Audit

|

|

|

10. Fraud

|

|

Data Analytics Internal Audit

|

Data

Analytics

|

|

11. H&S

and Wellbeing (worker & public)

|

|

|

Health

& Safety Follow-up Internal Audit

|

|

12. Assets

and Infrastructure

|

|

|

|

|

13. 3rd

Party / Contractors

|

S17a

Review of the Works Group

|

|

· Contracts

Management Internal Audit

· Procurement

Follow-up Internal Audit

|

|

Miscellaneous (other)

|

· Quality

Management System (QMS) interim surveillance audit by Telarc

· Civil

Defence Covid-19 Response Review

|

|

|

HAWKE’S BAY REGIONAL COUNCIL

Finance

Audit & Risk Sub-committee

Wednesday 12 August 2020

Subject: 2019-20 Annual Report

Audit Plan

Reason for Report

1. This report is to update the Finance, Audit and Risk Subcommittee on

the 2019-20 Annual Report Audit Plan.

2. Karen Young, Director, Audit NZ will be in attendance of the meeting

to discuss the Audit Plan and respond to any queries.

Background

3. As part of the audit for the Annual Report each year, an audit plan

is developed with management for the delivery of the audit of the Annual

Report.

4. As per the Terms of Reference, the plan is being presented to the

subcommittee as part of its responsibilities to review the scope of the audit

and the timetable.

Discussion

5. The 2019-20 Audit Plan is being presented at this meeting due to the

cancellation of the Finance, Audit and Risk subcommittee meeting during COVID

and receipt of the Audit Plan in May 2020.

6. The plan sets out the approach to the audit and the main risks and

issues that Audit NZ will focus on during the audit.

7. This year the following key risks and issues have been highlighted

7.1. Valuation of investments in HBRIC

7.2. COVID-19 impact on public sector accounting standards

7.3. Revaluation of Infrastructure Assets

7.4. Fair Value of other revalued assets

7.5. Changes in the Group capital structure

7.6. Managed Funds Investments

7.7. Consolidation process

7.8. Adjustments to ensure HBRIC and NPHL results are correctly

incorporated into HBRC's group results

7.9. Valuation of investment properties

7.10. The

risk of management override of internal controls and fraudulent reporting

7.11. Ethics

and integrity.

8. The interim audit of Internal Controls and the pre-final audit have

been conducted to date and there are some minor items to review as part of the

year end audit.

Next

Steps

9. FARS committee members are asked to provide feedback on the Audit

Plan to enable its finalisation.

10. Officers

will continue to work with Audit NZ to provide the information required for the

audit to ensure that the timetable for adoption of the Annual Report is met.

Decision Making Process

11. Staff have assessed the

requirements of the Local Government Act 2002 in relation to this item and have

concluded that:

11.1. as this report is for

information only, the decision making provisions do not apply.

11.2. any

decision of the sub-committee (in relation to this item) is in accordance with

the Terms of Reference and decision-making delegations adopted by Hawke’s

Bay Regional Council 25 March 2020, specifically the Finance, Audit and Risk

Sub-committee shall have responsibility and authority to:

11.2.1. Satisfy

itself that the financial statements and statements of service performance are

supported by adequate management signoff and adequate internal controls and

recommend adoption of the Annual Report by Council

11.2.2. Confirm that processes are

in place to ensure that financial information included in Council’s

Annual Report is consistent with the signed financial statements

11.2.3. Confirm the

terms of appointment and engagement of external auditors, including the nature

and scope of the audit, timetable, and fees.

|

Recommendation

That the Finance, Audit and Risk

Sub-committee receives and notes the “2019-20 Annual Report Audit Plan” staff report and agrees the Audit Plan as proposed.

|

Authored by:

|

Bronda Smith

Chief Financial Officer

|

|

Approved by:

|

Jessica

Ellerm

Group Manager

Corporate Services

|

|

Attachment/s

|

⇩1

|

Draft 2019-20

Annual Report Audit Plan

|

|

|

|

Draft

2019-20 Annual Report Audit Plan

|

Attachment 1

|

HAWKE’S BAY REGIONAL COUNCIL

Finance

Audit & Risk Sub-committee

Wednesday 12 August 2020

Subject: Cyber Security Internal

Audit Follow-up

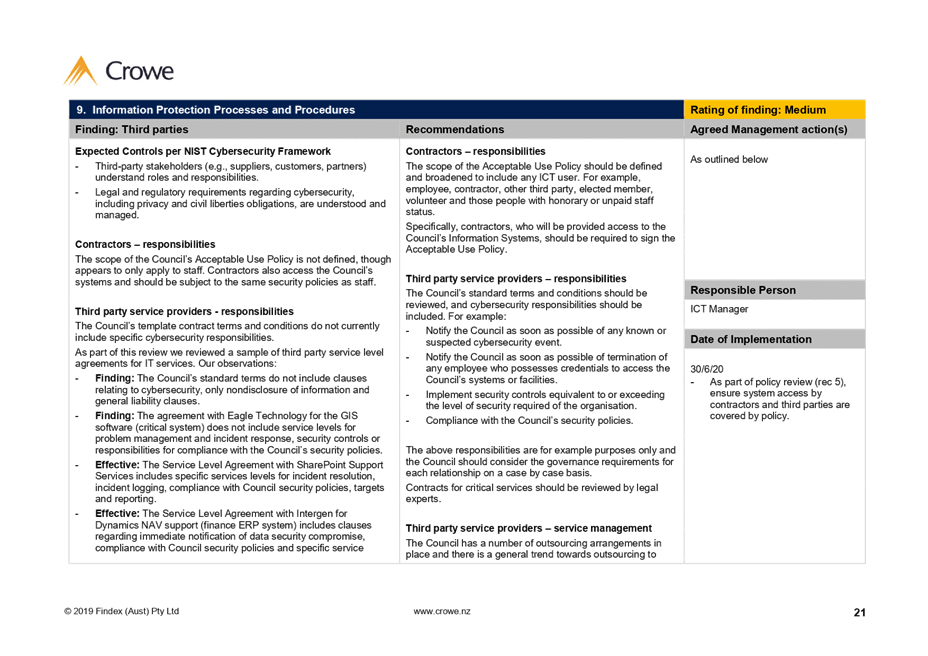

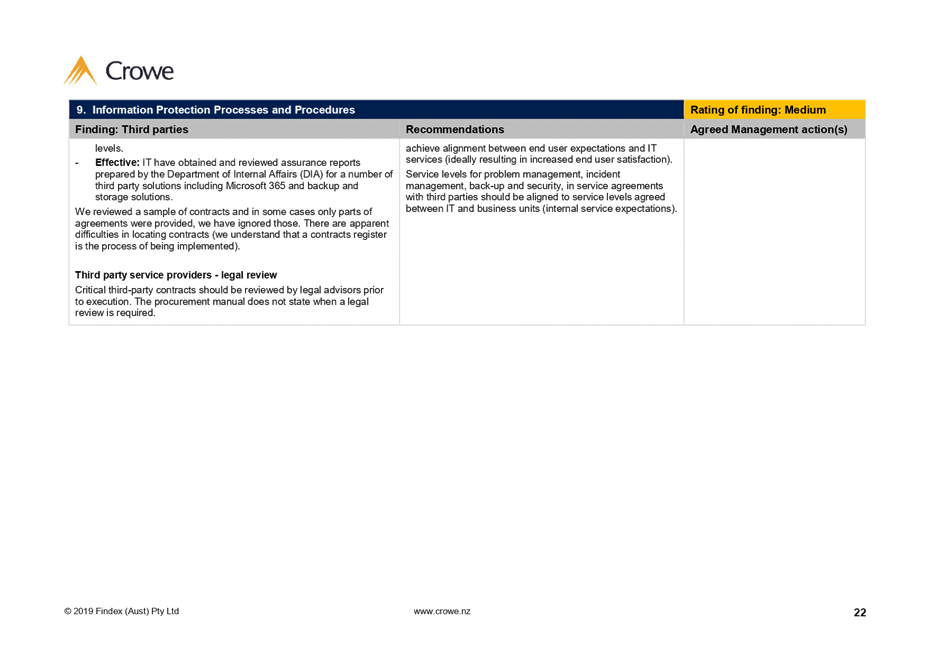

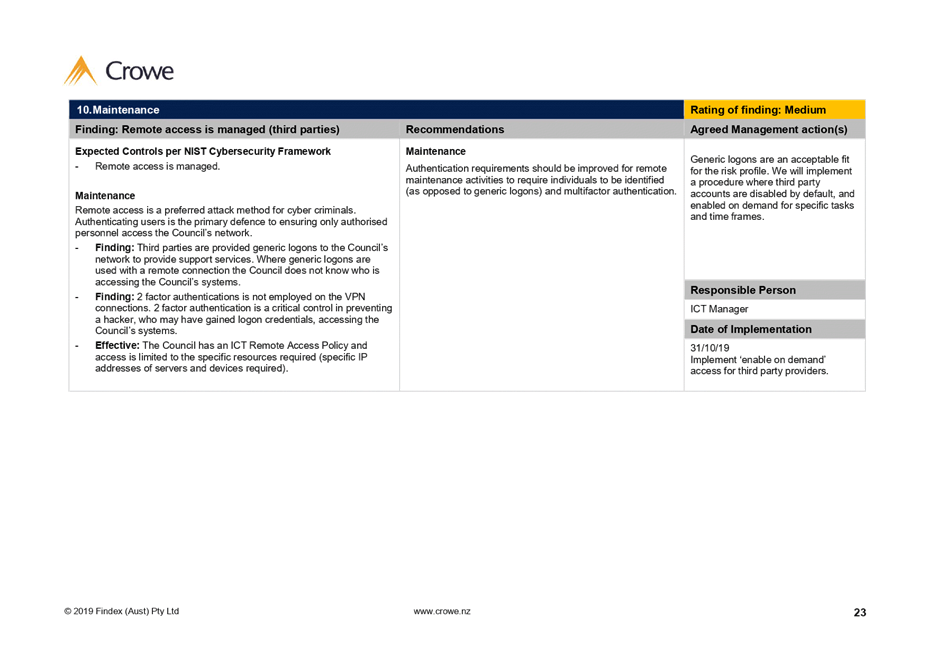

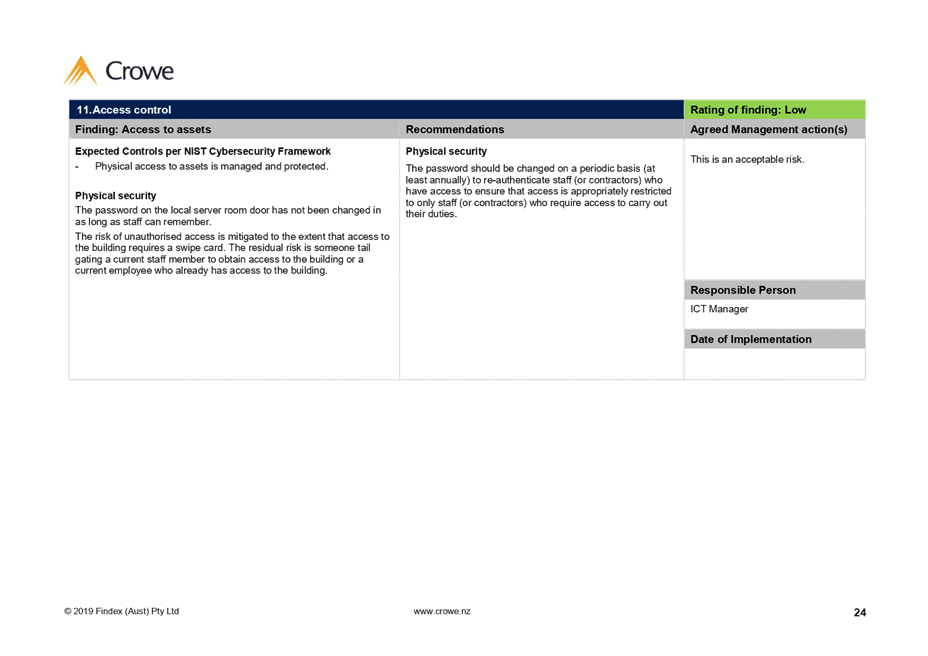

Reason for Report

1. This item provides the Sub-committee with an update on the

recommendations arising from the Crowe Horwath Cyber Security internal audit

report as requested by the 12 February 2020 Finance, Audit and Risk

Sub-committee meeting.

Background

2. The Finance, Audit and Risk Sub-committee (FARS) agreed at its

meeting on 22 May 2019 as part of the internal audit work programme, to engage

Crowe Horwath to conduct an internal audit of Council’s cybersecurity

controls.

3. The agreed scope and purpose of the audit was to evaluate the

maturity of cybersecurity processes, policies, procedures, governance and other

controls.

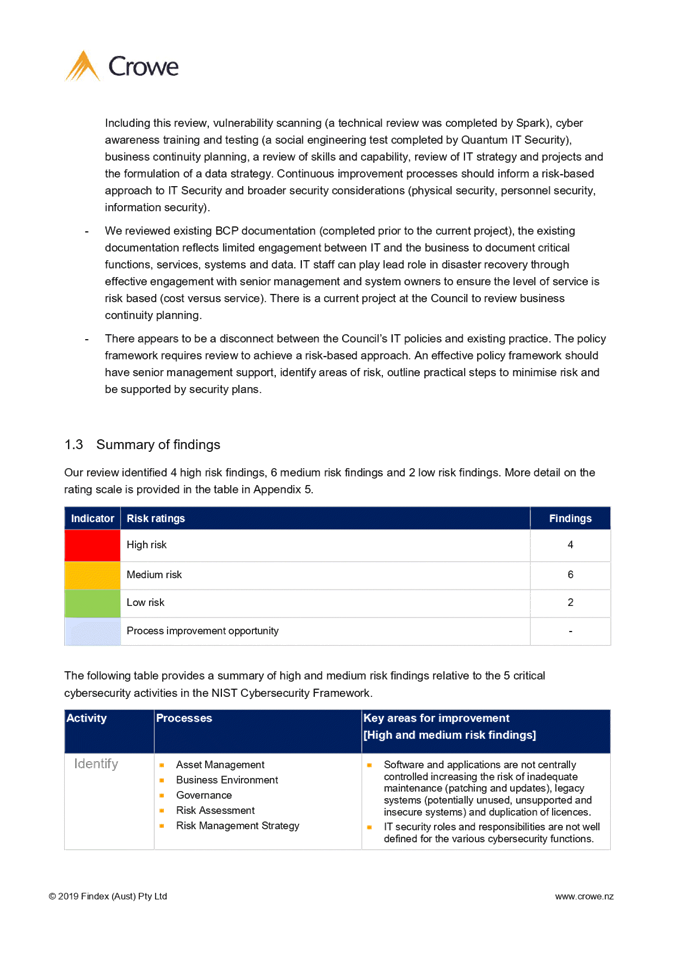

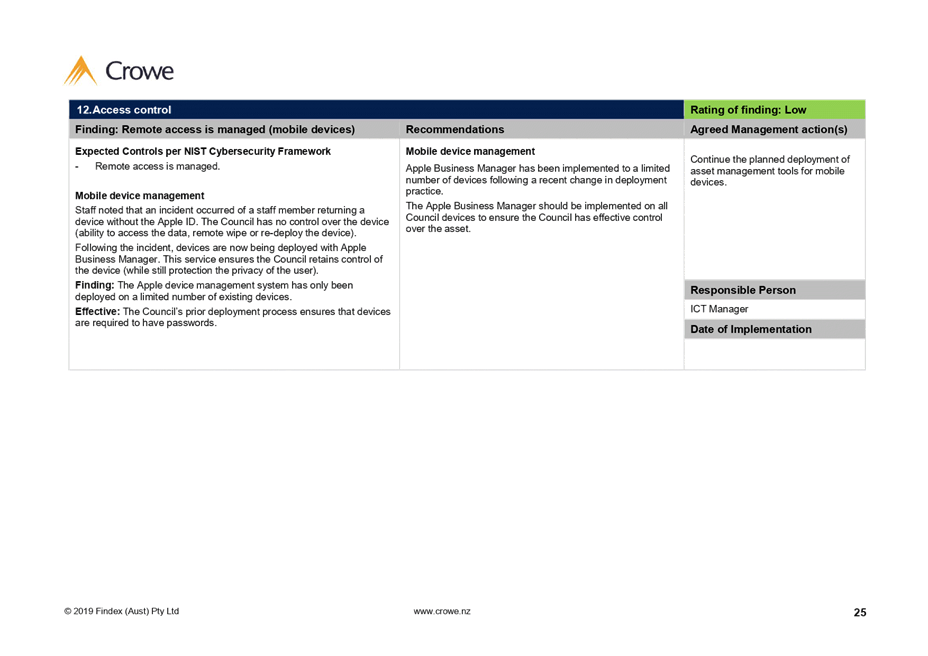

4. The audit identified four high risk findings, six medium risk

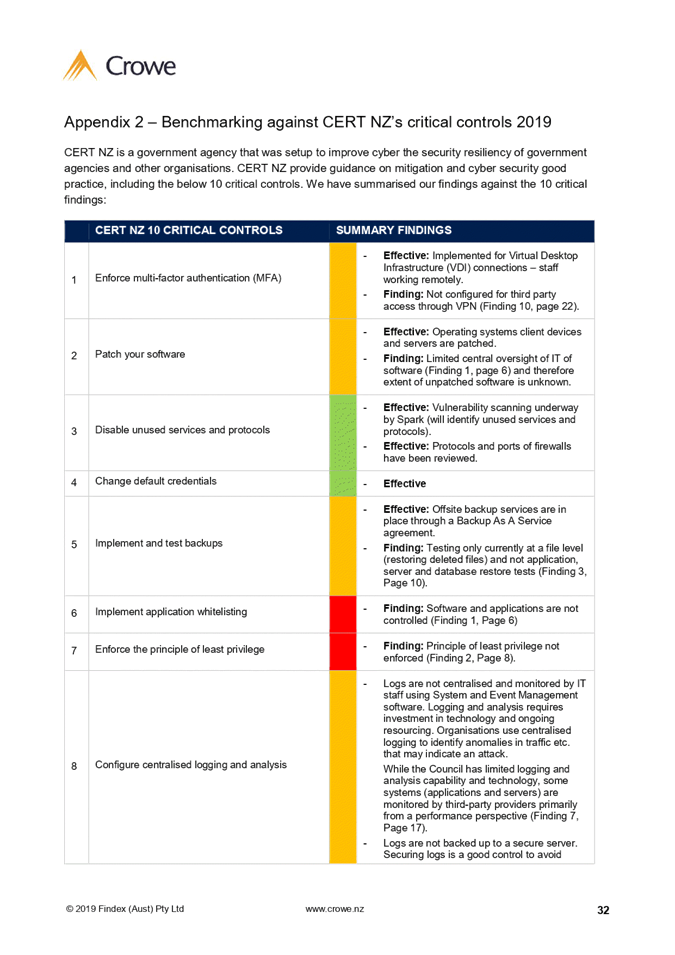

findings and two low risk findings.

5. Following a review of findings and recommendations, commentary has

been provided in the audit document describing management actions that have

been undertaken or that are planned for the future.

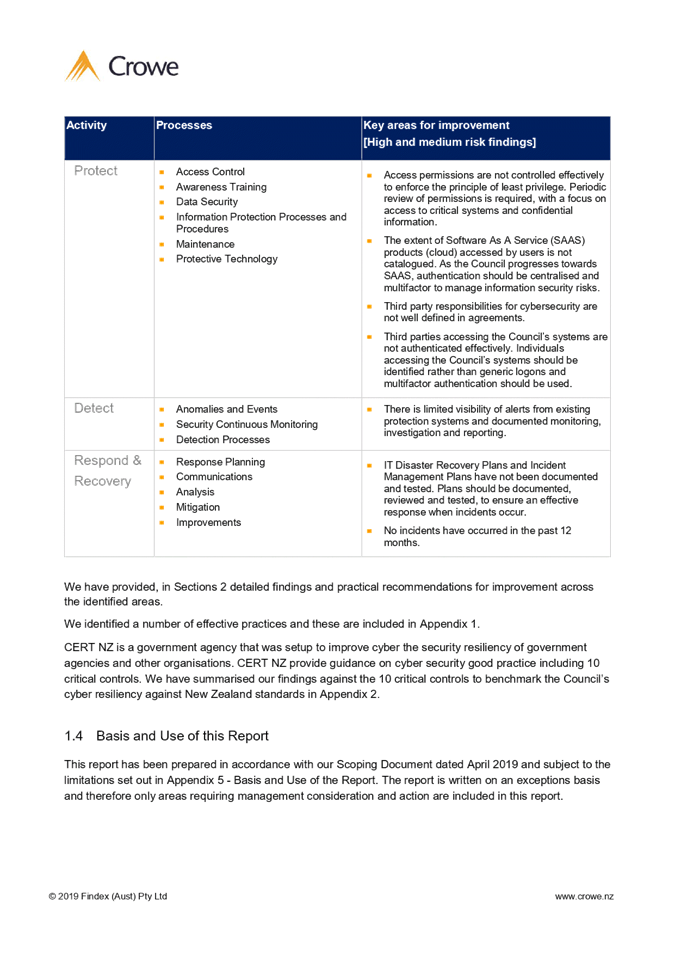

6. Key areas for improvement are summarised below and further detail

can be found in section 2 of the report.

7. Further reporting will be provided to this sub-committee in the

future to provide status updates on the planned management actions outlined in

the audit report.

Report Analysis

8. The following comments summarise the management actions and map to

the summary of findings in section 1.3 of the attached report.

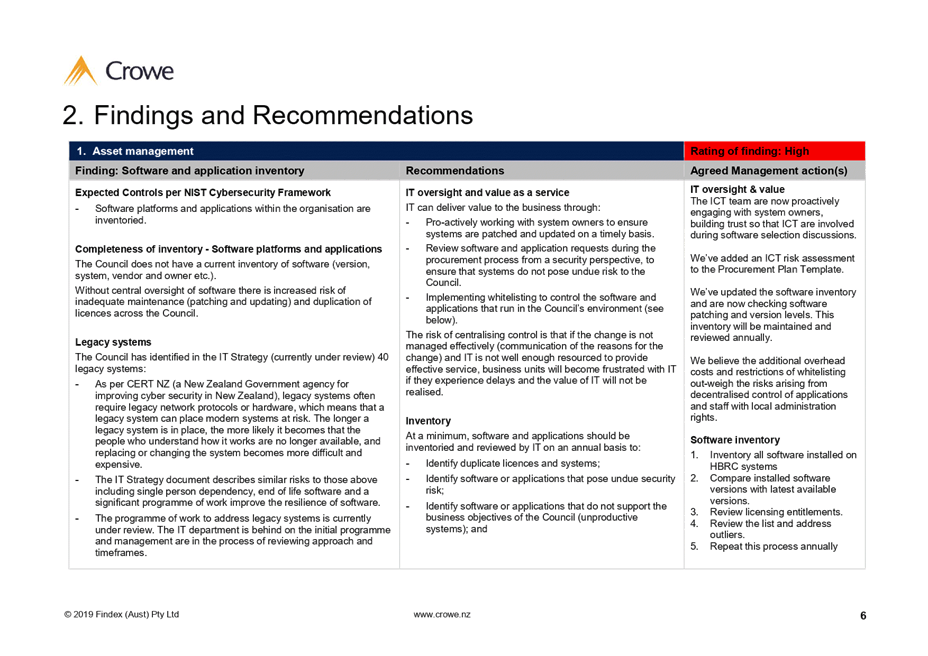

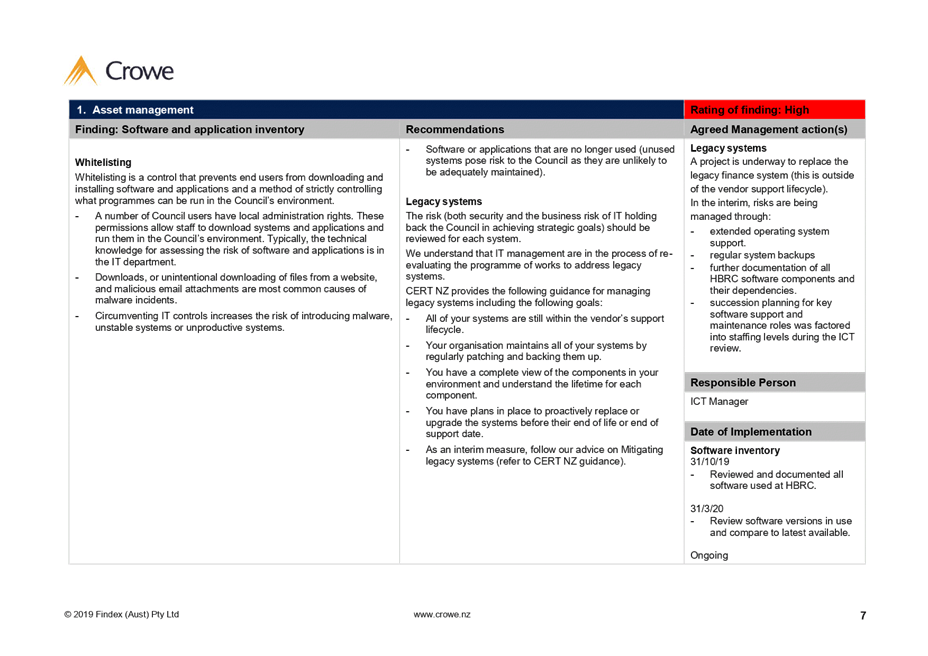

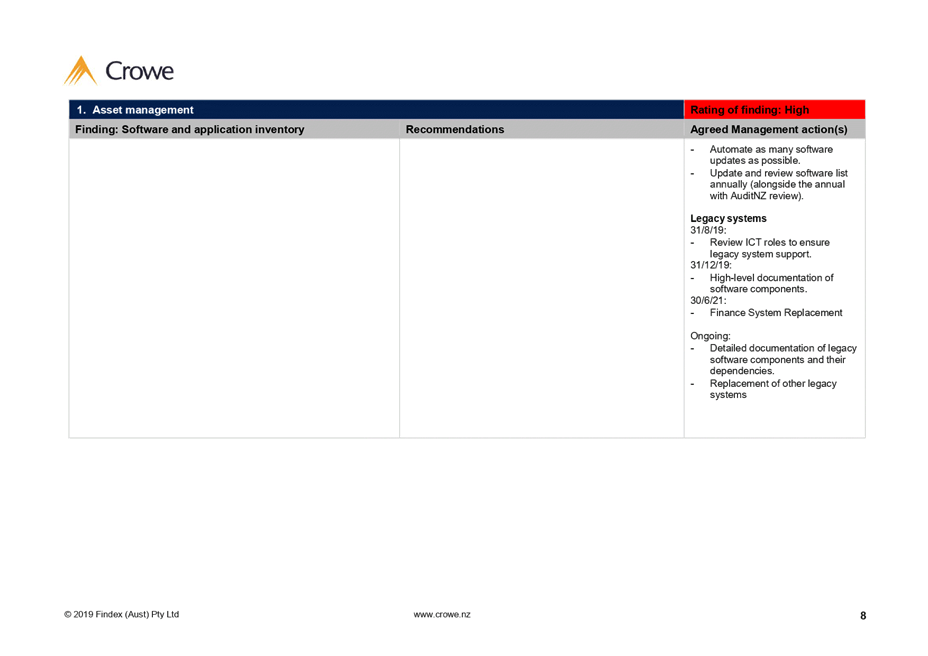

9. IDENTIFY – Improve management of legacy software risks.

9.1. A project is underway to renew the financial management system.

9.2. The HBRC software inventory has been updated.

9.3. Software dependencies are being documented and their risks assessed.

10. IDENTIFY

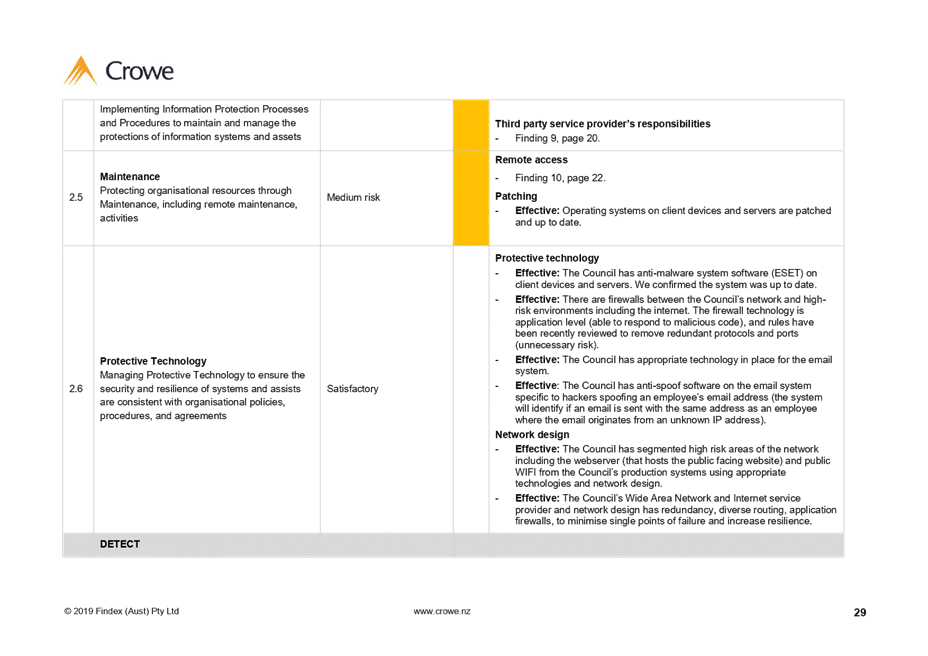

– Improve the definition of ICT security roles and responsibilities.

10.1. A

recent review of the ICT section identified the team and role with primary

responsibility for cybersecurity.

10.2. Further

work planned includes:

10.2.1. A review of the ICT Policy framework.

10.2.2. Adding a

reference to the ICT acceptable use policy in the job description template for

all staff.

10.2.3. Develop a RACI matrix for specific cybersecurity roles and

responsibilities.

10.2.4. Adding a

reference to cybersecurity responsibilities in third party software support

contracts.

11. PROTECT

– Improve control and review processes for access permissions.

11.1. An

annual review of access permissions is performed by Audit NZ to assess access

to financial systems.

11.2. The ICT

department will perform an annual review of access to other systems that

contain confidential data (HR and Regulatory systems) at the same time as the

Audit NZ review.

11.3. Third

party access to Council systems has been restricted to ‘enable on

demand’.

12. DETECT

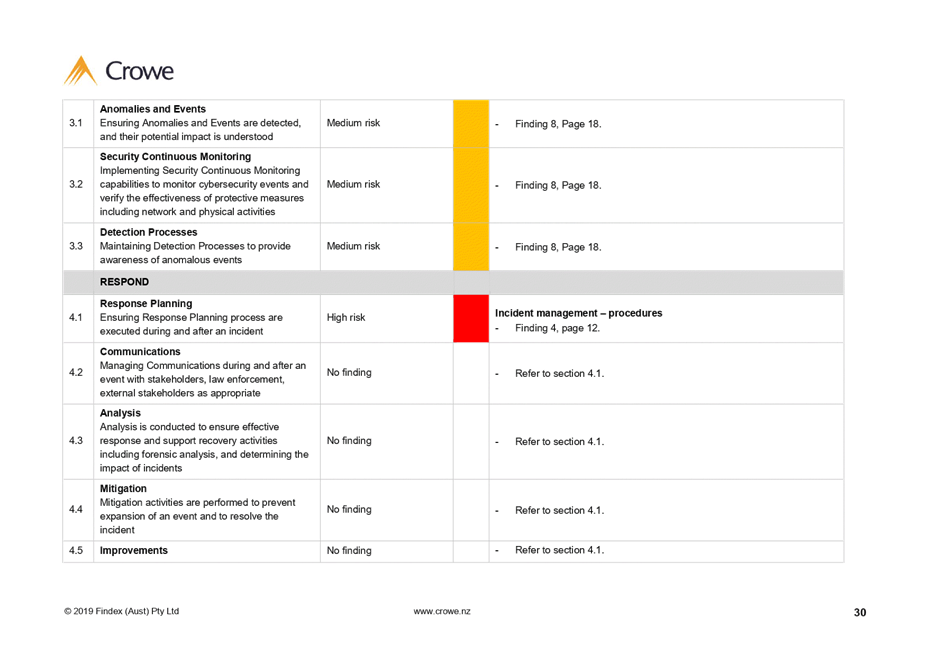

– Improve visibility of alerting systems.

12.1. A

central mailbox for alerts has been setup and is actively monitored by key

personnel.

12.2. Cybersecurity

alerts will be added to the ICT dashboard that is being developed – and

is displayed on a screen in the ICT work area.

13. RESPOND

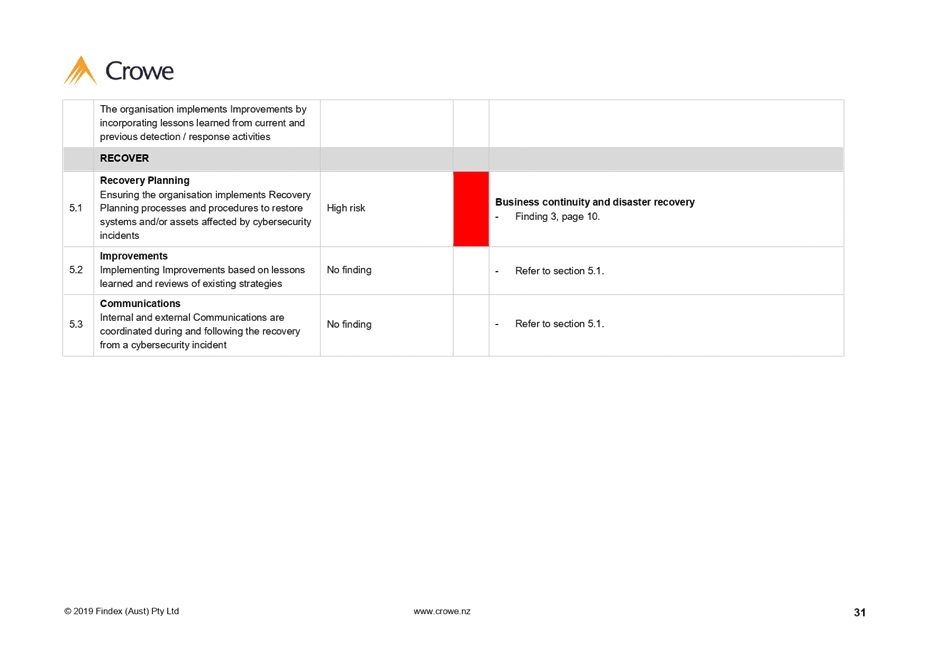

AND RECOVER – Develop ICT Disaster Recovery Plans and Incident Management

Processes.

13.1. Funding has been

requested in the annual plan for the development and implementation of an ICT

Disaster Recovery Plan.

13.2. Incident Management

processes and templates will be developed.

Decision Making Process

14. Staff have assessed the

requirements of the Local Government Act 2002 in relation to this item and have

concluded that:

14.1. as this report is for

information only, the decision making provisions do not apply

14.2. any

decision of the sub-committee is in accordance with the Terms of Reference and

decision-making delegations adopted by Hawke’s Bay Regional Council

25 March 2020, specifically the Finance, Audit and Risk Sub-committee

shall have responsibility and authority to:

14.2.1. Receive the

internal and external audit report(s) and review actions to be taken by

management on significant issues and recommendations raised within the

report(s)

14.2.2. Ensure that

recommendations in audit management reports are considered and, if appropriate,

actioned by management.

|

Recommendation

That the Finance, Audit & Risk

Sub-Committee Committee:

1. receives and considers the “Cyber Security Internal Audit” staff report

2. confirms it is comfortable that management actions undertaken or

planned for the future adequately respond to the findings and recommendations

of the Crowe Internal Audit – IT Security report.

|

Authored by: Approved

by:

|

Andrew

Siddles

Acting ICT Manager

|

Jessica

Ellerm

Group

Manager

Corporate Services

|

Attachment/s

|

⇩1

|

Hawke's Bay

Regional Council Internal Audit - IT Security, August 2019

|

|

|

|

Hawke's

Bay Regional Council Internal Audit - IT Security, August 2019

|

Attachment 1

|

|

Hawke's

Bay Regional Council Internal Audit - IT Security, August 2019

|

Attachment 1

|

|

Hawke's

Bay Regional Council Internal Audit - IT Security, August 2019

|

Attachment 1

|

HAWKE’S BAY REGIONAL

COUNCIL

Finance

Audit & Risk Sub-committee

Wednesday 12 August 2020

Subject: Data Analytics Internal

Audit Report

Reason for Report

1. To present the internal audit report (attached) for the Data

Analytics audit undertaken by Crowe Horwath in late 2019.

Background

2. The Finance, Audit and Risk Sub-committee (FARS) agreed at its

meeting on 22 May 2019, as part of the internal audit work programme, to engage

Crowe Horwath to conduct an internal audit of Council’s Data Analytics.

3. The agreed scope and purpose of the audit was to review payables and

payroll, and master and transactional data for the financial year ended 30 June

2019. This data was then analysed independently by Crowe Horwath for any

potential anomalies or suspicious transactions.

4. The report was then provided to staff, along with a separate

spreadsheet listing the transactions that required review. These spreadsheets

were initially analysed by the Payroll Officer and the Team Leader Finance and

then reviewed by the Chief Financial Officer to identify any findings requiring

further investigation.

5. This is the third annual Data Analytics audit conducted by Crowe

Horwath. Previously reporting the findings of the 2017-18 audit to the

sub-committee on 12 February 2019. A comparison to previous findings is also

provided in the attached analysis.

Discussion

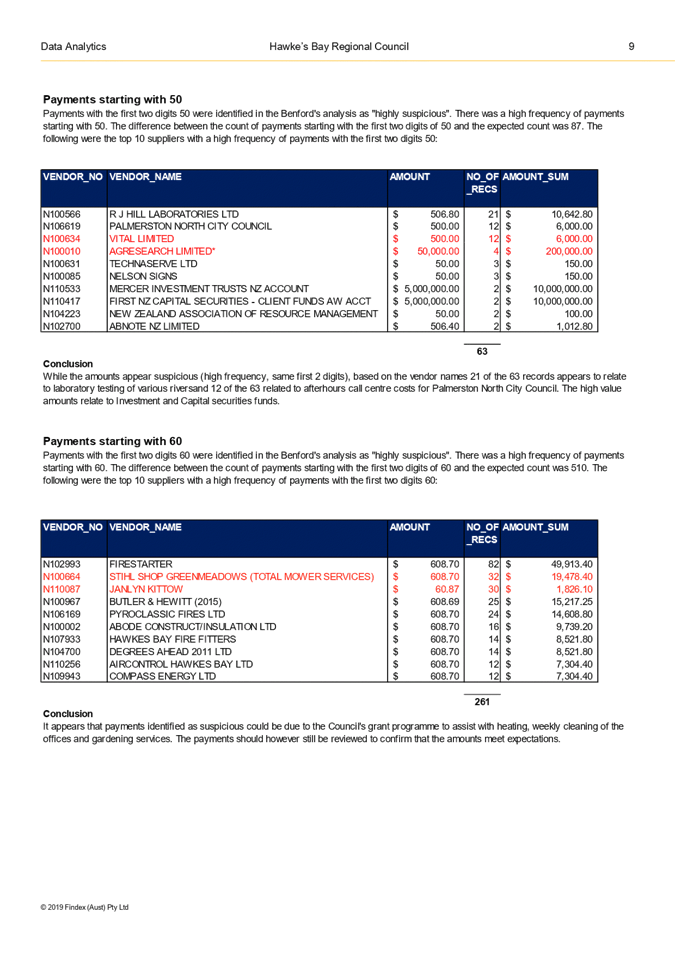

6. It is important to note that when a transaction is identified; it

does not necessarily indicate that there is anything suspicious. There are

often legitimate business reasons for a transaction being identified, such as

different types of payments to a Council (rates credits versus payment for

services) by way of pure example. These types of transactions may display in

areas such as “duplicate address”, “GST/non-GST

transactions”, or “duplicate IRD number” for example.

7. In addition, some transactions are listed purely for review purposes

due to their deemed higher risk nature, such as “review of top 50

vendors” as an example. This in itself allows staff to easily assess

whether vendors are in line with expectations and would highlight any vendors

that may appear erroneous.

8. Given the small size of Hawke’s Bay, there are often times

when an employee may share the same address as a vendor, usually a spouse.

Transactional processing staff ensure that employee approvals are not allowed

where any conflicts exist between an employee and a vendor.

9. Across the Accounts Payable data identified in the report, a review

of each vendor and transaction required has been undertaken. This consisted of

blocking vendors where required or giving valid explanations.

10. There

were 4 possible duplicate payments identified with 3 payments being genuine

payments. There was 1 invoice of $608.00 paid twice which has been refunded.

This was an application for a Clean Heat grant that was sent twice by the

applicant and processed again in error.

11. In terms

of the cross matching of data between payroll and accounts payable all records

were reviewed with no issues to note.

12. For the

payroll data, all data was review with no issues noted.

2017-18

Comparison

13. The list

of duplicates within the supplier master file has decreased substantially. For

example, duplicate bank accounts have decreased from 89 to 34. Of these 34, all

were legitimate duplicates, such as instances when a vendor has more than one

business function i.e. Hastings District Council.

14. The

number of possible duplicate payments decreased from 40 to 4 with one being an

actual duplicate which was of a low value.

15. Overall

improvement in internal processes is noticeable since the prior data analytics

assignment was performed, with additional checks reducing the number of

transactions arising within the review. Staff recognize that there is a need to

maintain appropriate process to reduce errors and to ensure correct internal

controls are used to reduce the risk of fraud or misappropriation.

Next

Steps

16. A proposed

2020-21 internal audit plan will be presented at the 12 August 2020 FARS

meeting. Staff are seeking feedback as to whether this Sub-committee would like

to see another data analytics assignment included in that proposal, as Auditors

recommend completing a data analytics audit every year.

Decision Making Process

17. Staff have assessed the

requirements of the Local Government Act 2002 in relation to this item and have

concluded that:

17.1. as this report is for

information only, the decision making provisions do not apply

17.2. any

decision of the sub-committee is in accordance with the Terms of Reference and

decision-making delegations adopted by Hawke’s Bay Regional Council

25 March 2020, specifically the Finance, Audit and Risk Sub-committee

shall have responsibility and authority to:

17.2.1. Receive the

internal and external audit report(s) and review actions to be taken by

management on significant issues and recommendations raised within the

report(s)

17.2.2. Ensure that recommendations

in audit management reports are considered and, if appropriate, actioned by

management.

|

Recommendation

That the Finance, Audit and Risk

Sub-committee receives and notes the “Data Analytics Internal Audit Report”.

|

Authored by:

|

Bronda Smith

Chief Financial Officer

|

|

Approved by:

|

Jessica

Ellerm

Group Manager

Corporate Services

|

|

Attachment/s

|

Data

Analytics Report

|

Attachment 1

|

|

Data

Analytics Report

|

Attachment 1

|

|

Data

Analytics Report

|

Attachment 1

|

|

Data

Analytics Report

|

Attachment 1

|

|

Data

Analytics Report

|

Attachment 1

|

HAWKE’S BAY REGIONAL

COUNCIL

Finance

Audit & Risk Sub-committee

Wednesday 12 August 2020

Subject: Internal Audits Review

and Action Plan

Reason for Report

1. This item

updates the Finance Audit and Risk Sub-committee (FARS) on Crowe’s final

report for the ‘Follow-up Audit’ of previous internal audits.

This internal audit was requested by the FARS through the FY20 internal audit

plan internal. Crowe’s full audit report headed, ‘Hawke’s Bay Regional Council Internal Audit –

Follow-up Audit’, dated 25 May 2020 is attached to this paper (attachment

1).

Officers’ Recommendation(s)

2. Council Officers recommend that Finance Audit and Risk Sub-Committee

(FARS) members consider Crowe’s internal audit final report and note the

staff management comments in response to each internal audit finding contained

within the report.

Executive

Summary

3. As part of the

FY20 internal audit plan Council approved an internal audit to review

management actions relating to previous audits. The objective of the

audit was to ensure that previously agreed recommendations and actions had been

effectively implemented by staff, or, that senior management had specifically

accepted the risk of taking no action.

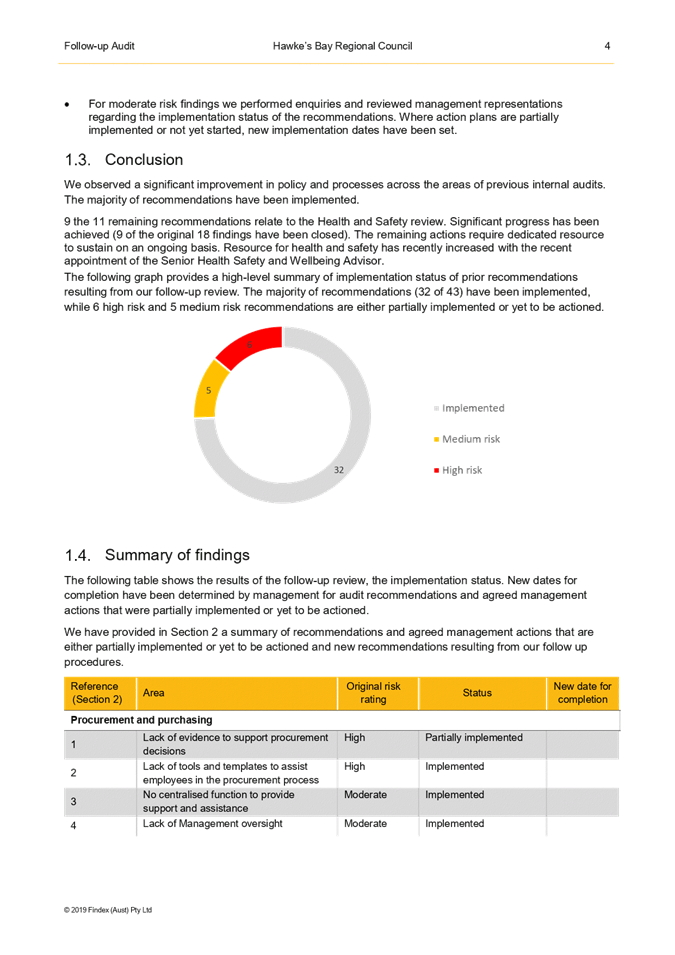

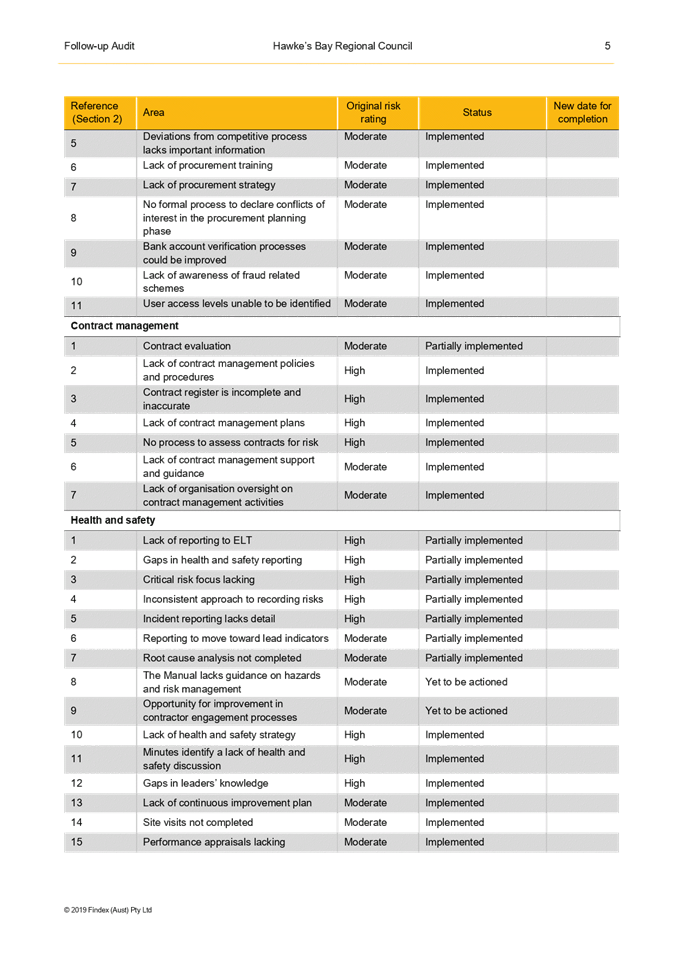

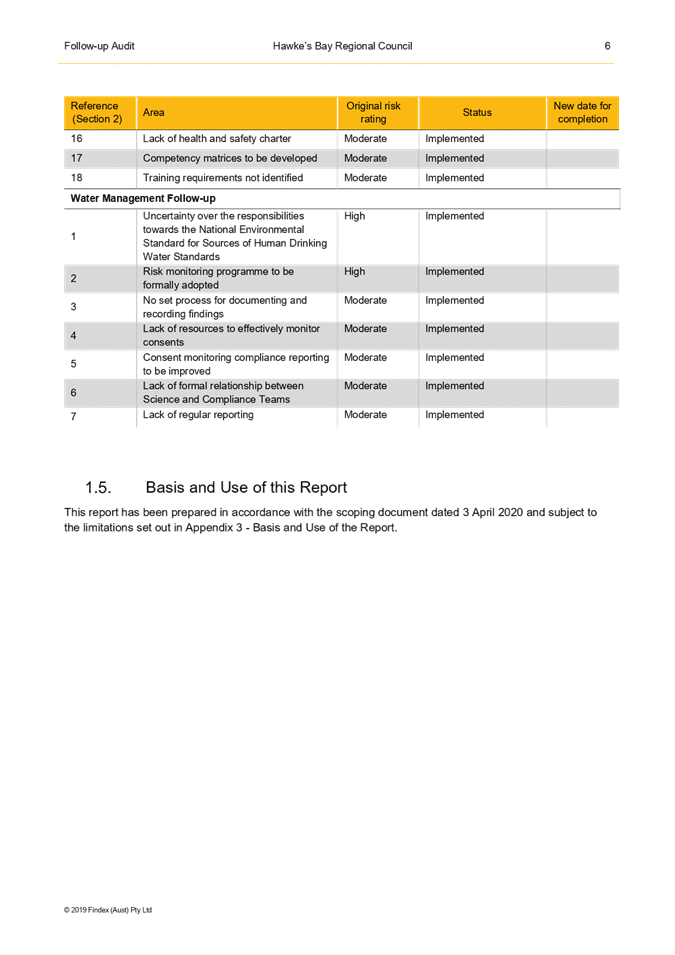

4. Previous audits

reviewed as part of this internal audit included:

4.1. Procurement

and Purchasing - May 2018

4.2. Contracts

Management - May 2018

4.3. Health and

Safety - September 2018, and

4.4. Water

Management Follow-up - May 2019.

5. Crowe noted in

their conclusion that they observed ‘significant improvement in policy

and processes across the areas of previous internal audits. The majority of

recommendations have been completed, with 32 of the 43 recommendations

implemented’.

Discussion

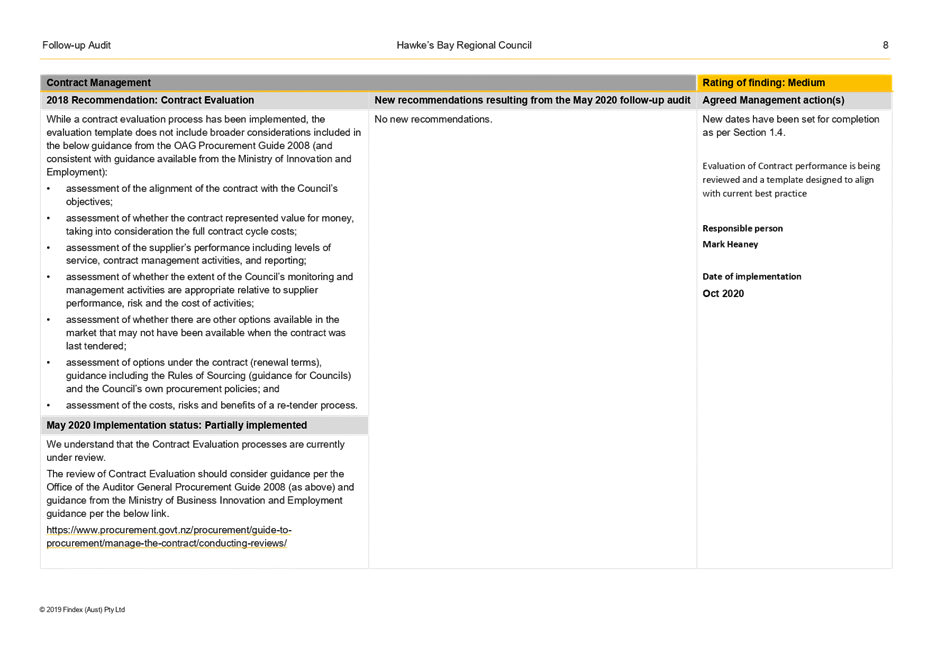

6. As

part of the FY20 internal audit plan Council approved an internal audit to

review management actions relating to the following prior internal audits:

6.1. Procurement

and Purchasing - May 2018

6.2. Contracts

Management - May 2018

6.3. Health and

Safety - September 2018, and

6.4. Water

Management Follow-up - May 2019

7. Crowe were

commissioned to undertake the internal audit throughout April and May

2020. The objective of the audit was to ensure agreed recommendations and

actions from the listed previous internal audits had been effectively

implemented, or, that senior management had specifically accepted the risk of

taking no action.

8. Crowe noted in

their conclusion that they observed ‘significant improvement in policy

and processes across the areas of previous internal audits. The majority of

recommendations had been completed, with 32 of the 43 recommendations

implemented’. Nine of the remaining 11 outstanding recommendations

related to the previous Health and Safety internal audit. However, it was

also noted that of the original 18 recommendations from the Health and Safety

audit nine of the actions were implemented with the remaining nine outstanding

actions requiring a dedicated Health and Safety resource to sustain the

required actions on an ongoing basis. At the time of the Crowe’s

internal audit report (May 2020) a Senior Health Safety and Wellbeing Advisor

had recently been appointed.

9. The total

number of outstanding audit actions broken down by the individual audits is

summarised the sections below. Staff responsible for the overall actions

for each individual audit have contributed to the summary update.

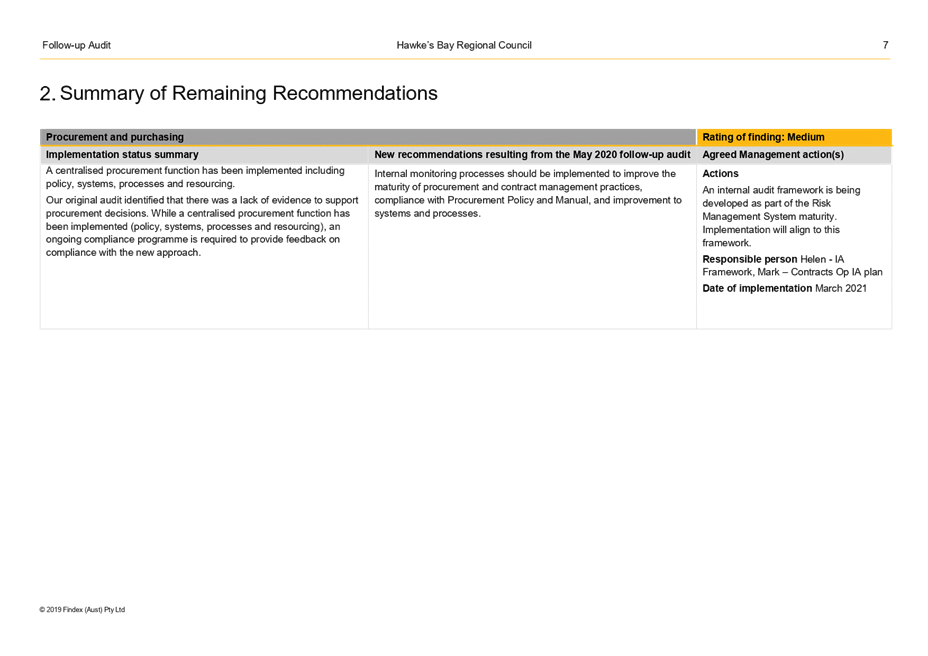

Procurement and

Purchasing

10. There was one audit action

that was rated as ‘high’ in the original audit that is partially

implemented and now has a residual rating of ‘medium’. The

original finding related to a lack of evidence to support procurement

decisions.

11. To fully close out the

original audit finding the remaining outstanding action requires an internal

monitoring process to ensure the procurement and contract processes comply with

the procurement policy and manual. Procurement plan to implement an

operational audit process aligned to the proposed HBRC internal assurance

framework that is being developed as part of the HBRC risk maturity

roadmap. The internal audit structure will leverage off the structure

that is used within the quality management system (QMS). The target date

to close out this finding is March 2021.

Contract

Management

12. There was

one audit action that was rated as ‘moderated’ in the original

audit that has been partially implemented, within the Crowe report that audit

action is now noted as ‘medium’. The original finding related

to the contract evaluation process.

13. Evaluation

of contract performance is currently being reviewed with a template partially

designed with good progress made. It is expected that the template design

will be ready for implementation in October 2020

Water Management

Follow-up

14. No

unactioned outstanding internal audit findings were noted.

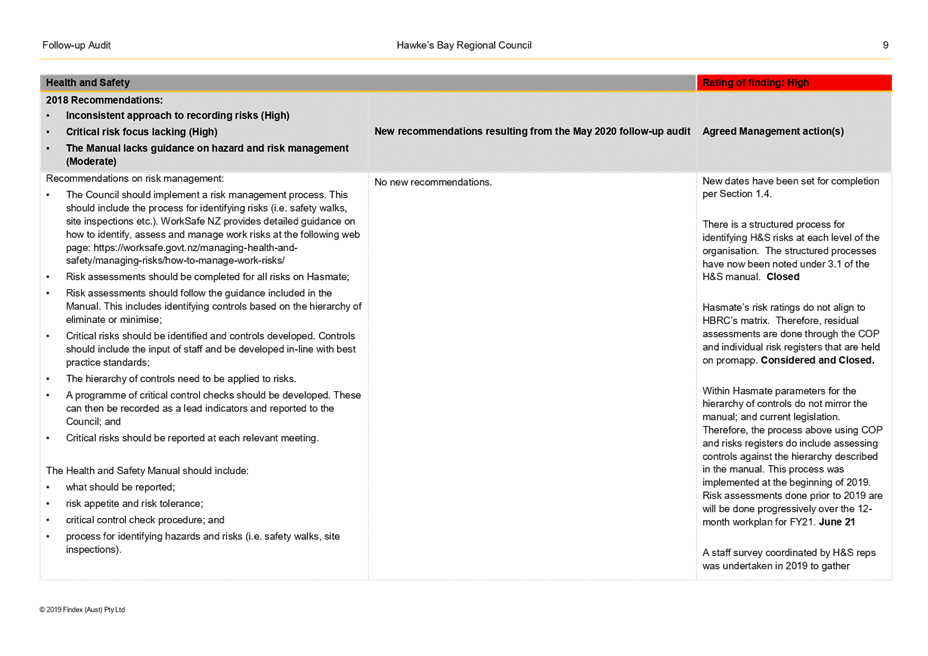

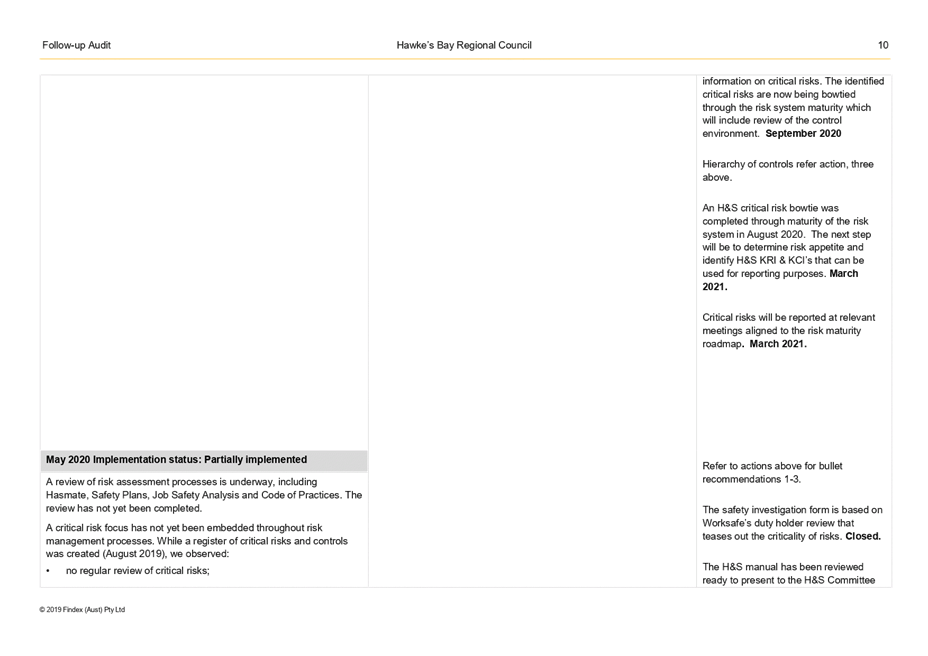

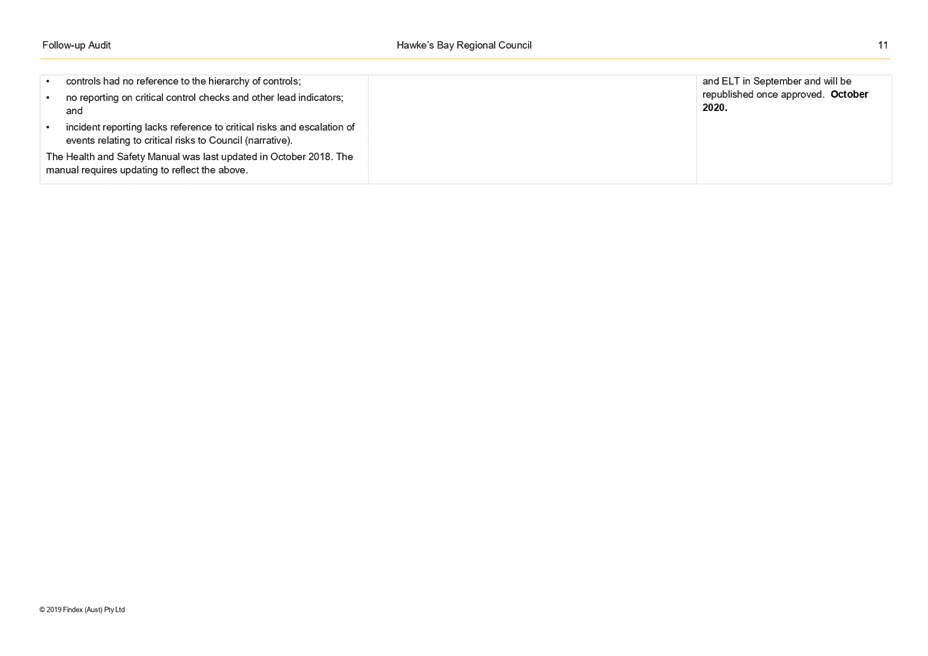

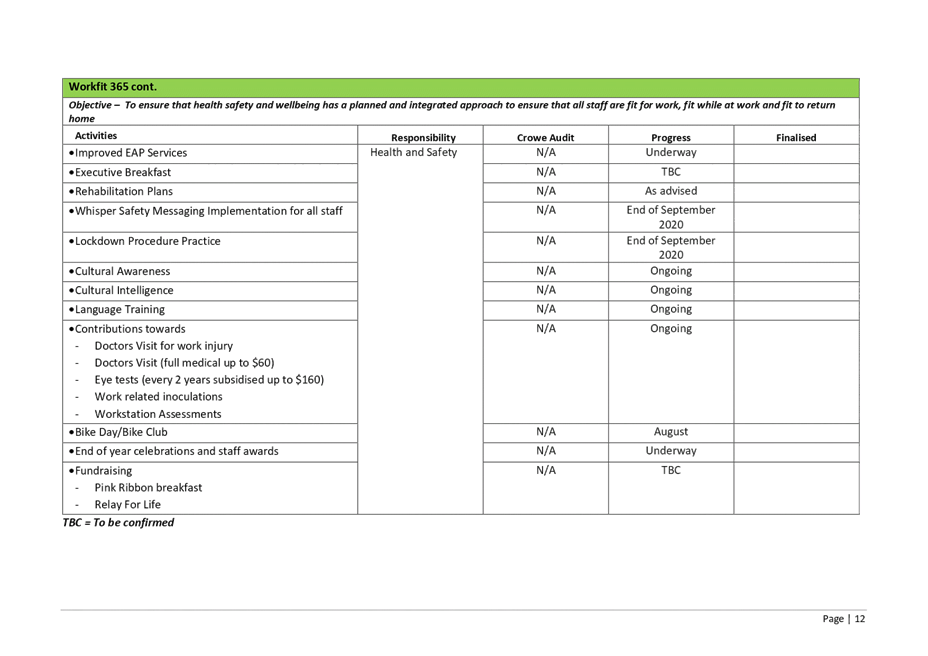

Health and Safety

15. Of the 18 audit actions

reviewed from the September 2018 Health and Safety internal audit. Nine

audit actions were noted as ‘implemented’, five ‘high’

audit actions were noted as ‘partially implemented’, two

‘moderate’ audit actions were noted as ‘partially

implemented’, and two ‘moderate’ audit actions were noted as

‘yet to be actioned’.

16. In response to the

follow-up Health and Safety audit the Senior Health Safety and Wellbeing

Advisor has provided the subsequent update in italics below and attached to

this paper the full Health, Safety and Wellbeing Work Programme for 2019-21 (attachment

2).

16.1. As a result of a combination of the 2018 audit, the June 2020

follow-up audit recommendations, and feedback from the Executive team the

health and safety implementation plan has been reviewed and updated.

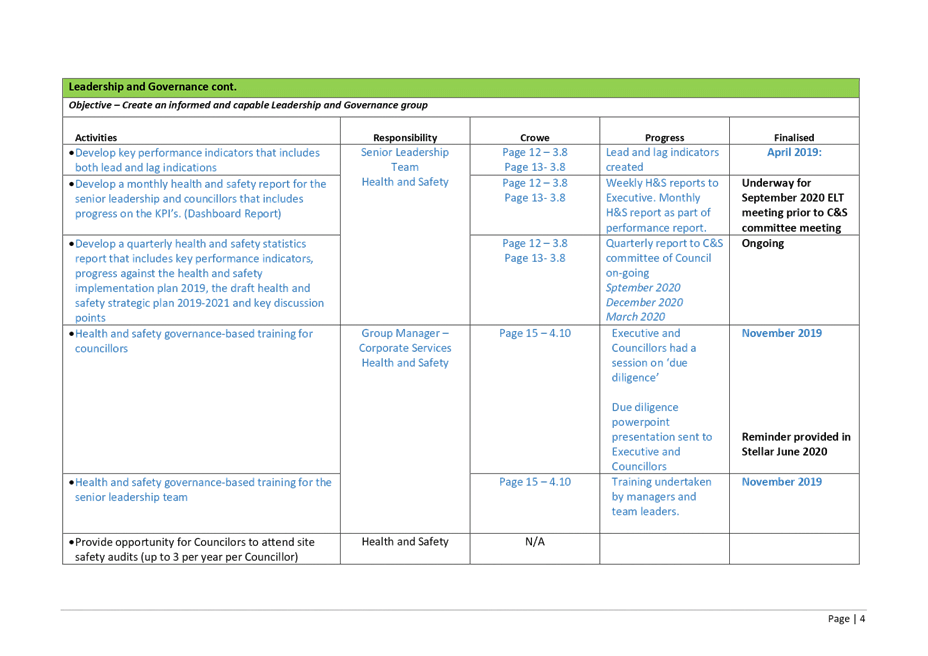

16.2. Hawke’s Bay Regional Council will utilise the institutional

knowledge of Franz Assenmacher, the external health and safety advisor from

Safe On Site, who has been contracted by Council for a considerable number of