HAWKE’S BAY REGIONAL COUNCIL

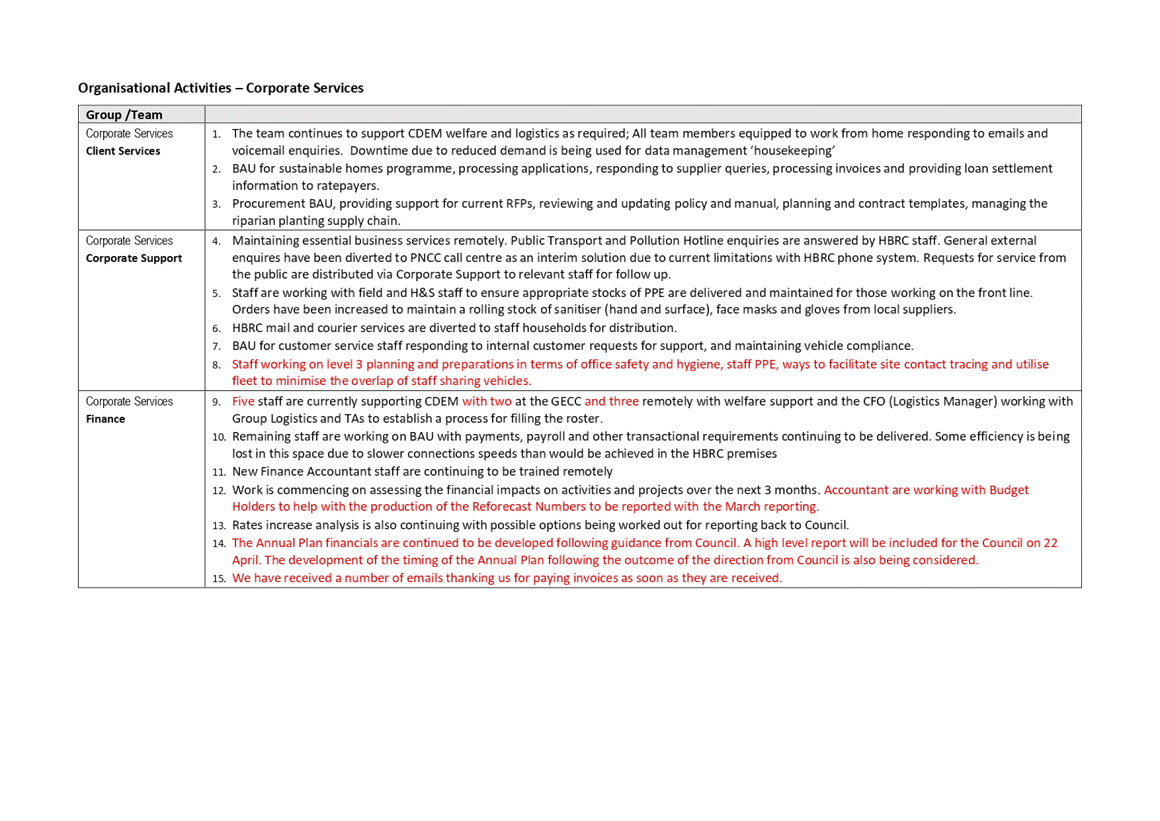

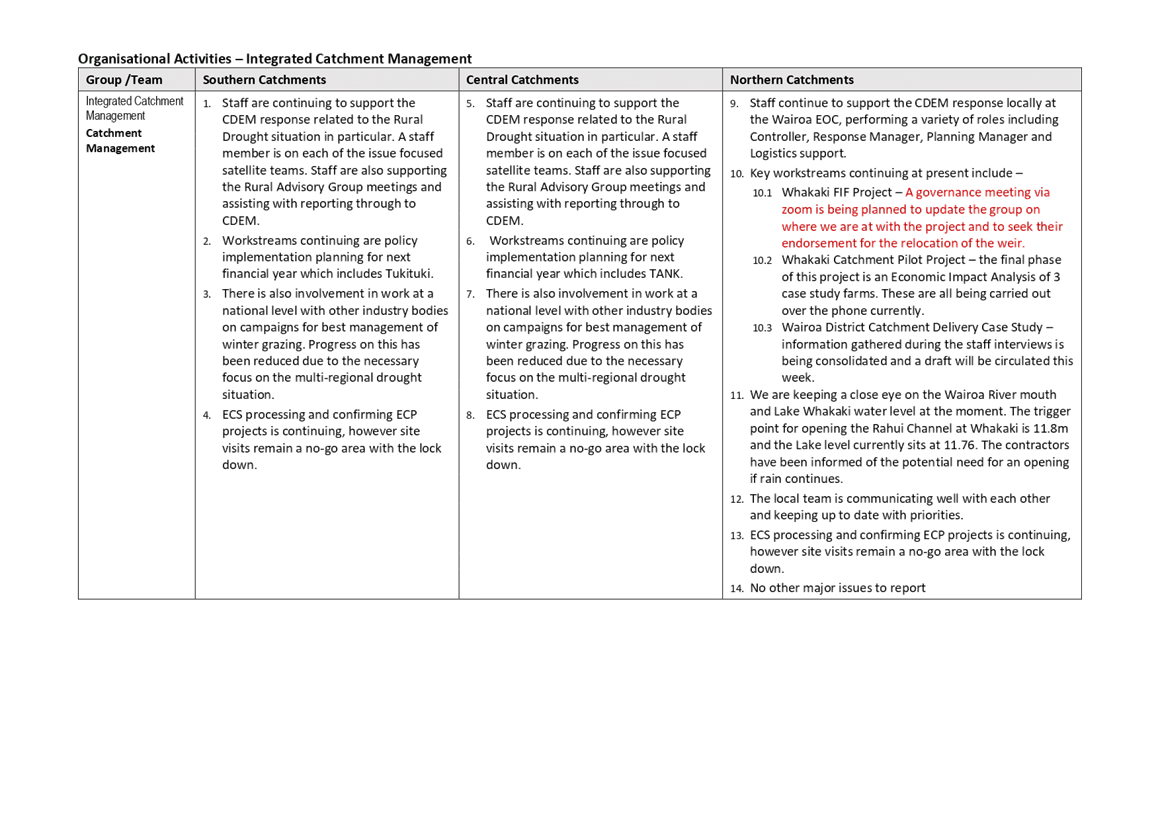

Wednesday 22 April 2020

Subject: May 2020 Meetings

Reason for Report

1. This item seeks

Council’s decision, by way of resolution, to extend the suspension of

committee delegations and meetings during the Covid-19 pandemic through to the

end of May, and to confirm the meeting schedule for May 2020

Officers’ Recommendation(s)

2. Council

officers recommend that Council reviews the period of suspension of the

delegations to and meetings of Council’s committees as previously

resolved on 25 March 2020, and extends those suspensions to the end of

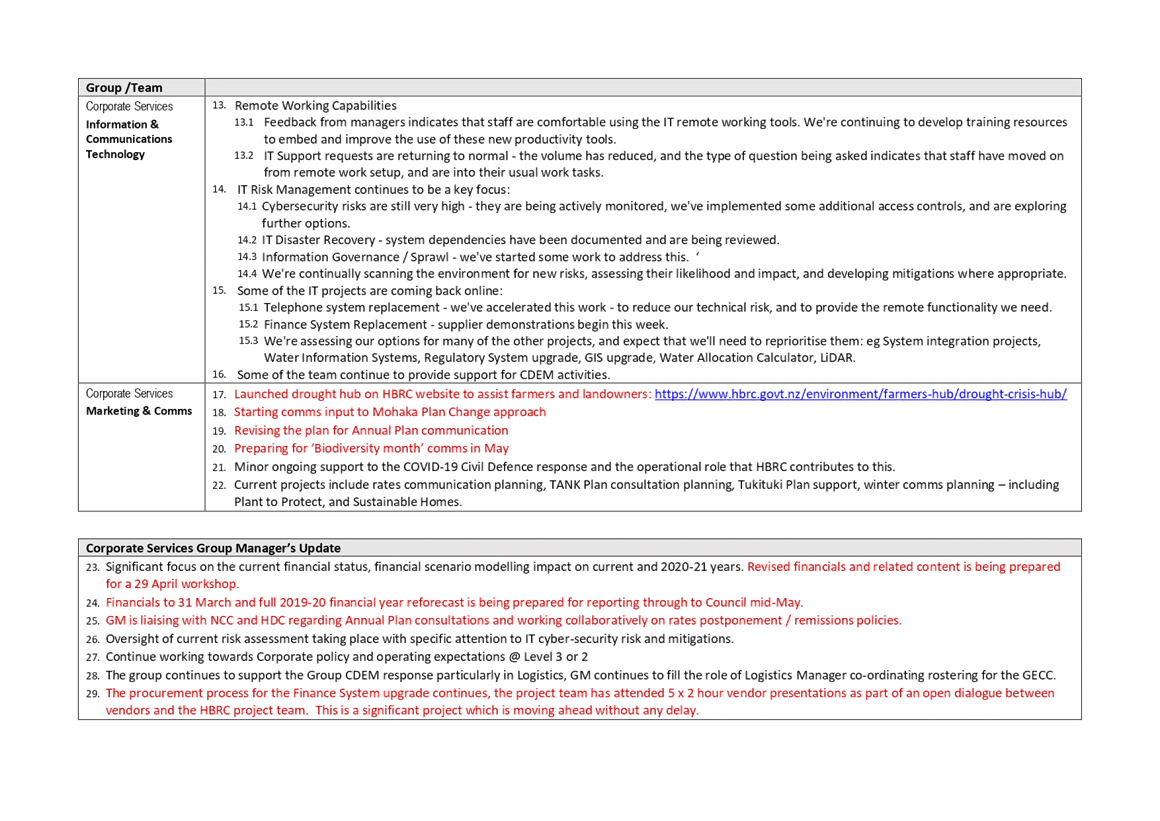

May.

3. Further, staff

also recommend that Council confirms the proposed schedule of Council meetings

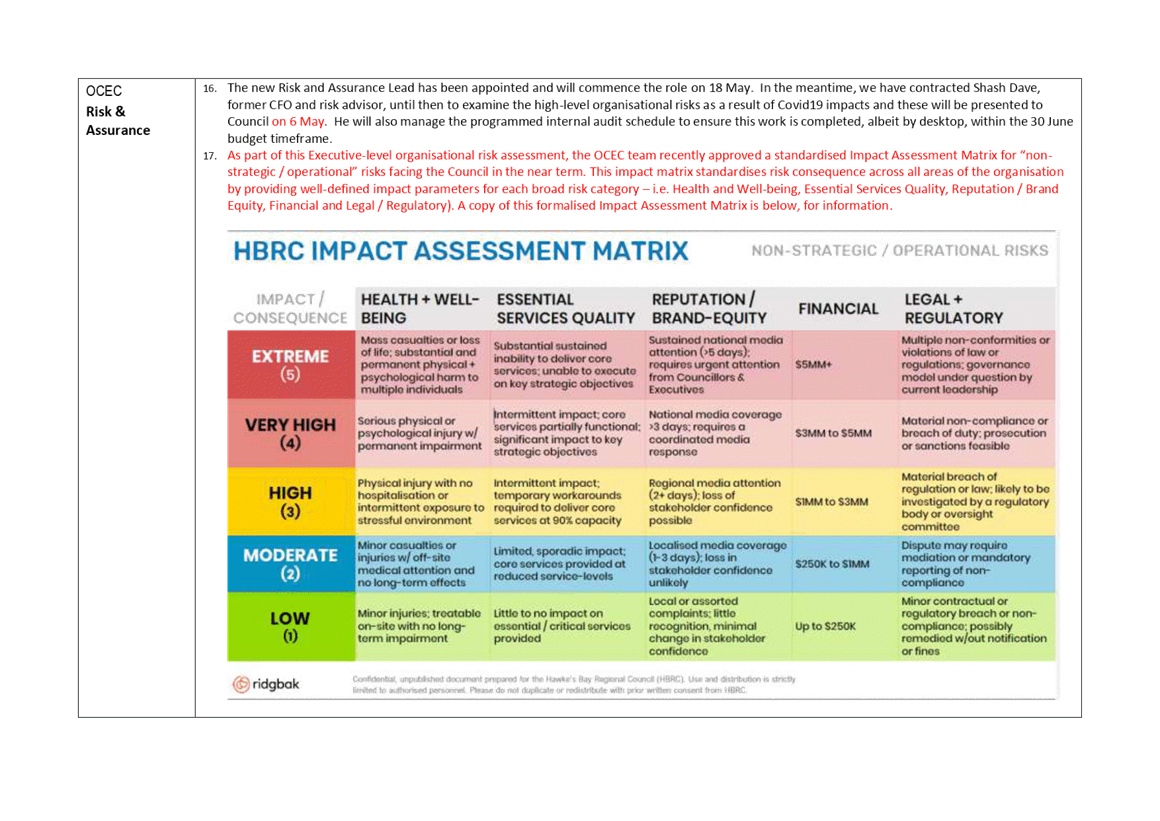

through to the end of May.

Background

4. Consistent with Central Government advice and the

restrictions imposed by the Covid-19 Alert Levels 3 and 4, Council resolved to

suspend committee meetings for the period during which restrictions would be in

place, and that the resolution would reviewed on 22 April.

5. In order for

the business of Council to carry on through the period of the pandemic and

while Committee meetings were suspended, it was proposed that any

business normally considered at committee meetings be dealt with by the Council

meetings.

6. At a subsequent

Council meeting it was further resolved that any decisions normally made by a

Committee would be subject to confirmation at the following Council meeting to

allow for a period of reflection and the opportunity for double debate.

Discussion

7. With staff

continuing to work from home and gatherings of more than 10 persons restricted

under Covid Alert Level 3, Council officers anticipate the need for Council to

continue meeting virtually. The meetings will continue to be streamed

and recordings put onto the website as usual, and in order to retain the

conduit to Māori Committee and RPC, tangata whenua representatives will be

invited to attend.

8. The continuation of regular Council meetings is intended to enable

staff to proceed with work to develop the Annual and Long Term plans and other

essential Council business as well as keep councillors up to date with the

latest developments in the Covid-19 pandemic response and recovery.

Decision Making

Process

9. Council and its committees are required to make every decision in

accordance with the requirements of the Local Government Act 2002 (the Act).

Staff have assessed the requirements in relation to this item and have

concluded:

9.1. The decision does not significantly alter the service provision or

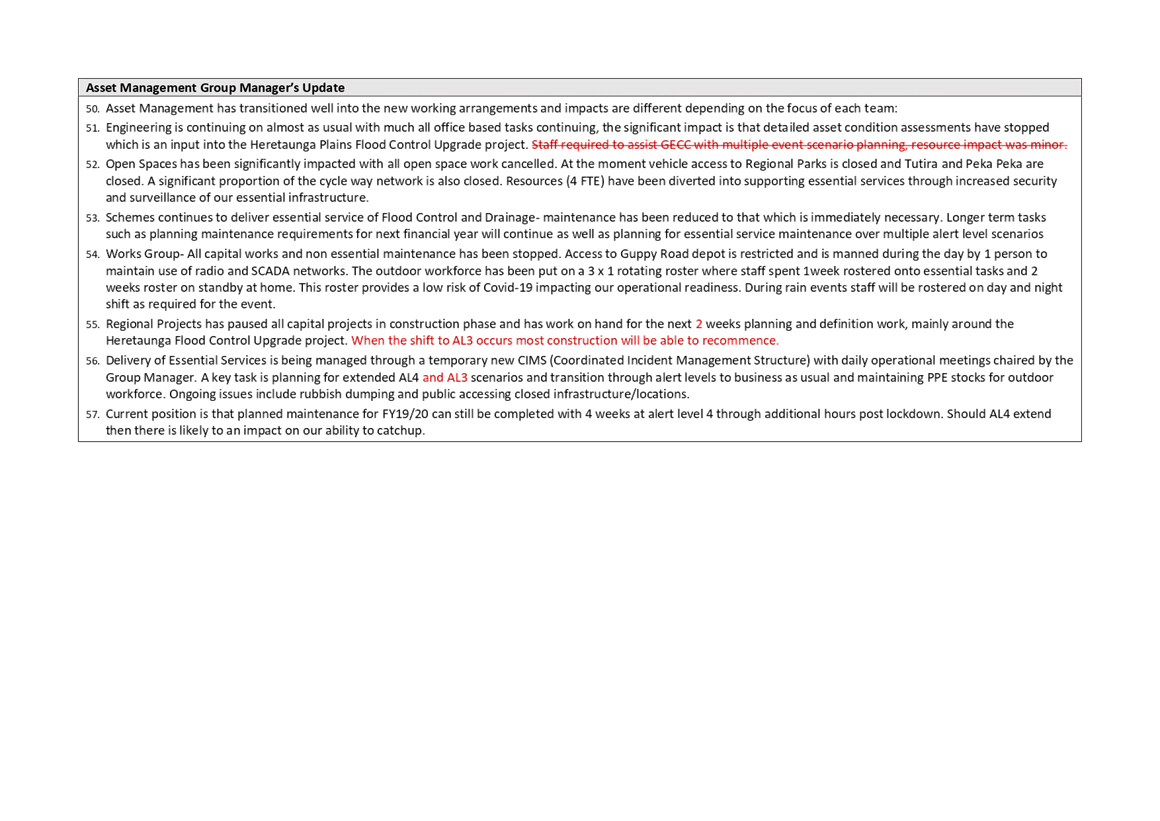

affect a strategic asset.

9.2. The use of the special consultative procedure is not prescribed by

legislation.

9.3. The decision is not significant under the criteria contained in

Council’s adopted Significance and Engagement Policy.

9.4. The decision is not inconsistent with an existing policy or plan.

9.5. Given the nature and significance of the issue to be considered and

decided, and also the persons likely to be affected by, or have an interest in

the decisions made, Council can exercise its discretion and make a decision

without consulting directly with the community or others having an

interest in the decision.

|

Recommendations

That

Hawke’s Bay Regional Council:

1. Receives and considers the “May 2020 Meetings” staff

report.

2. Agrees that the decisions to be made are not significant under the

criteria contained in Council’s adopted Significance and Engagement

Policy, and that Council can exercise its discretion and make decisions on

this issue without conferring directly with the community or persons likely

to an interest in the decision.

3. Suspends delegations to the Corporate &

Strategic and Environment & Integrated Catchments committees and the

Finance, Audit & Risk Sub-committee

4. Meets virtually as a full Council in lieu of

the Corporate & Strategic, Environment & Integrated Catchments and

Finance, Audit & Risk committees until 20 May 2020, or such time as

Covid-19 restrictions are lifted.

5. Confirms the May 2020 meetings schedule as proposed, being:

5.1. 6 May 2020 Māori

Committee meeting to proceed as previously scheduled

5.2. 13 May 2020 Extraordinary Regional Council meeting in lieu of Finance, Audit & Risk Sub-committee (FARS)

5.3. 20 May 2020 additional Extraordinary

Regional Council meeting (including confirmation of 13 May decisions normally

made by FARS)

5.4. 27 May 2020 Regional Council meeting to proceed as previously

scheduled.

|

Authored by:

|

Leeanne

Hooper

Governance Lead

|

|

Approved by:

|

Joanne

Lawrence

Group Manager Office of the Chief Executive

and Chair

|

James Palmer

Chief Executive

|

Attachment/s

There are no

attachments for this report.

HAWKE’S BAY REGIONAL COUNCIL

Wednesday 22 April 2020

Subject: Annual Plan Update

Reason for Report

1. This report

provides an update to Hawke’s Bay Regional Council (Council), and

high-level timeline, on progression of the 2020-/21 Annual Plan, following the

Notice of Motion on the 25 March 2020.

2. The objective

of this work is to ensure Council is responding to, and acknowledging, the

economic impact of recent events on the community and the uncertainty and

stress that ratepayers will be under.

3. This report provides a public summary of the information presented

to Council for the 8 April workshop, and subsequent discussion that took

place.

Background

4. On 25 March

2020 Council resolved for the Chief Executive to provide Council with urgent

advice on how the Council can deliver the 2020-21 Annual Plan with zero rates

increase.

5. This was in

response to a Notice of Motion introduced by Cr Rex Graham. The rationale being

a need to recognise the current pressures on the community in the context of

the Drought, TB outbreak and Covid-19.

6. Prior to the

motion, officers had begun looking at how to best incorporate and respond to

the potential impact to the region following the escalation of COVID-19 to a

pandemic status by the World Health Organisation on 11 March 2020 and the

subsequent announcement of the Four Stage Alert System on 21 March 2020 by the

Government.

7. Legal advice

was sought to establish the options available to Council within the bounds of

the Local Government Act 2002, and its requirements for consultation for any

significant or material differences from the 2018-28 Long Term Plan (LTP).

8. On 8 April

2020, Officers workshopped the options available to Council and sought guidance

from Council on which options it would prefer to investigate.

9. Officers

recommended an approach which involves an overall assessment of the current

circumstances and updating of known and significant changes to assumptions, but

largely maintains the current proposed levels of service. This is on the basis

that any budget should be constructed using the best information available at

the time. Officers therefore requested time to incorporate the most up to date

information such as known significant changes to investment income expectations

including portfolio returns and Napier Port dividend.

10. Once the

impact of the above is known or better predicted staff recommend utilising the

Rates Remission and Postponement Policies in conjunction with the intent to

debt fund, as required, an unbalanced budget. It is possible to adopt an

unbalanced budget when deemed prudent and in exceptional circumstances.

Discussion

Legislation requirements and Consultation

11. This cautionary note originates

from the obligation in section 101(1) of the Local Government Act 2002 (LGA)

for councils to manage their finances prudently and in a manner that promotes

the current and future interests of the community. Section 14(1)(g) also sets

out a principle in similar terms that councils must act in accordance with in

performing their roles.

12. A decision to rework and

set an annual plan based on an overall 0% rates increase would very likely

require consultation before the decision is made. This is because the proposed

change in rates impact for 2020-21 (7.3% decrease) is certainly a significant

and/or material change from what the LTP set out for the 2020-21 year (section

95(2) and (2A) of the LGA). In this regard, section 95 applies regardless of

whether the change is a proposed increase or decrease in rates.

13. The finance team is

continuing to analyse what the impacts of a 0% increase would change in terms

of service delivery. We note that in certain circumstances, section 97(1)(a)

and 97(2) of the LGA might be triggered – decisions to alter

significantly the intended level of service provision for any significant

activity undertaken by or on behalf of the Council, or a decision to cease (or

commence) such activity can only be made if the decision is explicitly provided

for in a long term plan and the proposal was consulted on in a LTP consultation

document. Given 2020-21 is an annual plan year, this means if section 97 is

engaged that the Council would need to undertake an LTP amendment, which

includes consultation.

14. Council could set an

unbalanced budget for 2020-21 if it considers it financially prudent to do so

after considering:

14.1. section 101(1) and (2)

of the LGA 02, and

14.2. the

matters stated in section 100(2)(a) to (d) of the LGA 02.

Debt Levels and Debt Covenants

15. Current external debt is

$35 million. In the 2018-28 LTP debt was forecast to peak at $38.1m in

2027-28. Part of the reason for that is that a conservative approach was

applied to loan terms which means significant amounts were budgeted to be

repaid.

16. The current draft AP

revenue for 2020-21 (based on the 7.3% rates increase) is budgeted to be

$64.5m. This puts the current debt ceiling at around the $100m

mark. So there is no concern with the amount Council can borrow or the

150% ceiling.

17. The

following are the debt covenants of Council.

|

|

HBRC

|

LGFA

|

|

Net external

debt as a percentage of total revenue

|

<150%

|

<175%

|

|

Net interest

on external debt as a percentage of annual rates revenue

|

<20%

|

<25%

|

|

Net interest

on external debt as a percentage of total revenue

|

<15%

|

<20%

|

|

Liquidity

buffer amount comprising liquid assets and available committed debt facility

amounts relative to existing total external debt

|

>10%

|

n/a

|

18. The debt limit is

something each council sets based on its risk appetite and the requirements of

the council as part of the LTP. Some councils take a more conservative

stance than others. The LGFA limit gives an upper limit where, if you exceed

that limit you will not be able to access further funding from LGFA (and cost

of borrowing may increase).

19. The ability for HBRC to

borrow is not the issue to consider. The issue is the ability, with a

relatively small revenue base that is substantially comprised of rates, to

service debt. Further, consideration should be made to the magnitude of future

rate increases as Council rebalances its finances over the coming years.

20. As HBRC’s LTP shows,

there is an incremental impact from increasing the level of Council’s

borrowings. Debt servicing becomes an increasing proportion of the cost

structure to be funded each year. Local Government debt, in general, does not

generate a commercial return so the total cost of servicing falls on

ratepayers.

21. Council

needs to focus on what Council, and the community, would be comfortable

servicing (and paying for through rates). In addition to HBRC rates, ratepayers

have been facing significant increases from the territorial councils (HDC, NCC,

etc) as they grapple with the increased costs of infrastructure (water, etc).

Council must also be mindful of the issue of intergenerational equity.

Considering how much is reasonable to ask future generations to pay. If Council

takes on extra debt now, how quickly should this be repaid?

Rating

Information

22. The

following table shows the breakdown of the rating revenue (GST incl) from the

rating database for 2019-20.

|

Category

|

$0

|

%

|

|

Residential

|

$14,135

|

50%

|

|

Lifestyle

|

$1,486

|

5%

|

|

Industrial

|

$2,211

|

8%

|

|

Commercial

|

$2,114

|

7%

|

|

Pastoral

|

$5,484

|

19%

|

|

Horticultural

|

$1,912

|

7%

|

|

Dairy

|

$297

|

1%

|

|

Forestry

|

$579

|

2%

|

|

Utility

|

$102

|

0%

|

|

Specialist

|

$44

|

0%

|

|

Mining

|

$2

|

0%

|

|

Other

|

$152

|

1%

|

|

Unidentified

|

$6

|

0%

|

|

Total

Rate take

|

$28,522

|

100%

|

Options Analysis of how to achieve a 0%

rates increase

23. Taking all the advice into

account, a prudent approach would involve an overall assessment of

circumstances and decision-making that takes a long-term view with

consideration of future financial and non-financial consequences of the

decision.

24. Based on this Council

needs to consider if, in the long term, a 0% rates increase is a prudent

decision to make on behalf of the ratepayers.

25. A number

of options are available to Council to achieve a 0% rates increase depending on

the options that Council would like to consider and the targeted response that

may be considered.

Table / Option 1

|

Continue

with the Proposed Rates Increase / Levels of Service (LoS) and use the

Remissions of Rates in Special Circumstances Policy to remit the rates

increase and fund the shortfall by borrowing through a resolution of Council.

|

|

Pros

|

Cons

|

|

· Relief is given to rate payers based on

the rates increases expected this year which reduces their rates required to

be paid this year.

· The ability to possibly target the

ratepayers that are most affected

· The ability for some ratepayers that are

not affected to pay their full rates

· The ability to relax the criteria on the

remission policy easily.

· The rates increase in Year 1 of the LTP

will be based on the new rates values rather than a lowered value from this

year. E.g. the increase will not be this year’s missing increase plus

the increase for the first year if the LTP.

· Levels of services are not impacted as

the budgets remain the same.

· Benefit to the community of us continuing

with planned programme of work (economic activity etc)

|

· The media ignoring the remission process

proposed and reporting that we are still increasing rates / expenditure in

the current climate, which could be mitigated with a strong comms programme

· The funding requirement to cover the

reduction in income will need to be recovered future from rates.

|

26. Option 1

provides the ability to apply either:

26.1. A - A

universal rates remittance so all rate-payers receive a zero % rates increase

(this assumes the community is all impacted equally)

OR

26.2. B - A

more targeted approach to benefit sectors / groups of rate-payers most affected

(staff need to do more analysis and come back with options of what this looks

like)

OR

26.3. C

– Remission for those who apply for it only.

27. Staff are

seeking legal advice on whether this option would require consultation. It may

be that Council can adopt this option with an unbalanced budget should the

Council deem it to be prudent without having to consult.

Table / Option 2

|

Continue

with the Proposed Rates Increase / LoS and use the Postponement in Cases of

Financial Hardship or Natural Disaster Policy to postpone rates increase and

funding the shortfall by borrowing through a resolution of Council.

|

|

Pros

|

Cons

|

|

· Postponement is given to rate payers

based on the rates increases expected this year

· The ability to target the ratepayers that

are most affected

· The ability for some ratepayers that are

not affected to pay their full rates

· The ability to relax the criteria on the

postponement policy

· The rates increase in Year 1 of the LTP

will be based on the new rates values rather than a lowered value from this

year. E.g. the increase will not be this year’s missing increase plus

the increase for the first year if the LTP.

· Levels of services are not impacted as

the budgets remain the same.

· The funding requirement to cover the

delay in receiving income will be reduced to only the time required to cover

the postponement period

|

· The media ignoring the remission process

and reporting that we are still proceeding with rates increases in the

current climate

· The rates will still be required to be

paid by the ratepayer at a future date and the debt of ratepayers will sit on

our balance sheet.

|

28. This

option would not require consultation. The use of the postponement policy means

that the rates are still due and therefore the Levels of Services and the

Annual Plan would be adopted as proposed.

Table / Option 3

|

Re-work the

Annual Plan Budget by amending / reducing levels of service to reduce

expenditure to achieve a 0% Rates Increase

|

|

Pros

|

Cons

|

|

· Simple and clear media reporting of no

budget increases

· The ability to include alternative

expenditure based on the Council’s appetite for additional Economic

Development / Recovery programs, if these can be funded within a zero rates

increase.

· Potential to fast track capital projects,

if these can be funded within a zero rates increase.

· Allows us to reflect changes to revenue

assumptions based on the information we have now

· Community trust / onboard with the Annual

plan reflecting the current operating context.

|

· Impacts all budgets and has implications

for delivering the Levels of Service in each activity as we come out of the

impact of COVID-19.

· Is likely to trigger an LTP amendment

requirement due to the reduction in the Levels of Service.

· Consultation on the changes would be

required with consideration of how this would be achieved satisfactorily with

the Alert Level 4 requirements.

· It is likely the adoption of the Annual

Plan by 30 June will not be met and a delay in striking rates will be

required.

· The rates increase in Year 1 of the LTP

will be based on a lowered value from this year, e.g. the increase will be

this year’s missing increase plus the increase for the first year of

the LTP.

· Possible continued impact to Service

Delivery into the first year of the next LTP as rate increase are done off a

lowered base from the previous year if the missing rates are not included in

the Year 1 of the LTP.

· Targeted Rates Reserves will reduce as

the reduction of the rates flows into the reserves for future years.

|

29. Option 3 would require

Consultation as the changes to Annual Plan would be classified as significant.

This may also result in a concurrent LTP amendment if the Levels of Service are

impacted by the changes to the budgets.

30. At the

workshop Council asked Officers to investigate the following option (4).

Table / Option 4

|

Continue

with the Proposed Levels of Service (LoS). Update known changes to revenue

assumptions, reduce rates income to the same level as 2019/20 and fund the

shortfall by borrowing through a resolution of Council.

|

|

Pros

|

Cons

|

|

· Simple and clear media reporting of no

rates increases

· Allows us to reflect changes to revenue

assumptions based on the information we have now

· Community trust / onboard with the Annual

plan reflecting the current operating context.

· The rates increase in Year 1 of the LTP

will be based on the new rates values rather than a lowered value from this

year. E.g. the increase will not be this year’s missing increase plus

the increase for the first year if the LTP.

· Levels of services are not impacted as

the budgets remain the same.

· Benefit to the community of us continuing

with planned programme of work (economic activity etc)

|

· Consultation on the changes would be

required with consideration of how this would be achieved satisfactorily with

the Alert Level 4 requirements.

· It is likely the adoption of the Annual

Plan by 30 June will not be met and a delay in striking rates will be

required.

· The funding requirement to cover the

reduction in income will need to be recovered future from rates.

|

31. High-level

analysis of option 4, to date, estimates the shortfall in revenue for the

2020-21 year to be between $6m to $10m.

The Annual Plan

and Consultation

32. Online engagement is

sensible, but consultation using only the internet is unlikely to be adequate

in terms of s.82 of the LGA 02. Councils should provide consultation

information in their usual ways except by any means which would breach Covid-19

lockdown rules, or which are no longer available due to external constraints

(eg, community newspapers no longer being published/delivered).

33. Councillors should also

consider alternatives to the internet, such as:

33.1. using local radio

stations to raise awareness and provide information about engagement and

participation opportunities

33.2. options for contacting

people by telephone and enabling telephone submissions

33.3. household mailouts

and/or special deliveries of printed documents under certain circumstances, and

33.4. accepting and processing

hard copy submissions by post with reference to advice from health authorities.

34. We note that current

advice on essential services published by the Ministry of Business Innovation

and Employment advises that “News (including news production) and

broadcast media is considered essential. Daily delivery of newspapers is

considered essential. Non-daily newspapers for communities that are hard to

reach due to physical location and with limited access to digital connectivity,

or for non-English language material audiences are considered essential.”

35. Officers consider that the

difficulty with Consultation based on the current climate should not be a

reason for Council to manufacture an outcome that does not require

consultation. Following the assessment of the impact of COVID-19 and to revisit

the Annual Plan and update assumptions with the best / latest information,

Officers will be in a better position to understand if consultation is required

and to develop a plan to ensure that Consultation is completed adequately in

terms of s.82 of the Local Government Act.

36. If

Consultation is required, then it is likely that adoption of the 2020-21 Annual

Plan could be delayed until after 30 June.

Next

Steps

37. Officers are assessing the

impact of COVID-19 and revisiting the Annual Plan to update assumptions with

the best / latest information available to us. Staff will present back the

financials to a Council workshop on 29 April, clarify what the revenue

shortfall is likely to be and the impact on current Levels of Service.

38. Officers will also provide

information on the impact to significant projects with many having been

impacted by the current lockdown, for example the LiDAR project where flying

has temporarily stopped.

39. Further, analysis on the

rating database is being undertaken to explore how to break down the rating

database with current information and to be able to assess the impact of the

above on a variety of ratepayers.

40. Following this revisit of

the Annual Plan, staff will confirm if the revised Annual Plan will require

Consultation due to significant or material changes based on the requirements

of section 95(2) and (2A) of the LGA.

41. Officers suggest that a

‘package’ of works / initiatives to respond to and address both the

immediate effects and the economic recovery to come, are developed as a

response to COVID-19, the Drought and any impact of the TB outbreak.

42. The

following timeline is indicative only and based on the assumption the Annual

Plan will require consultation.

|

Date

|

Key

deliverable

|

|

29 April

(Council workshop)

|

Revised

financials presented

|

|

20 May

|

Any new

postponement and remission policies adopted (subject to consultation)

Supporting

Information adopted

Consultation

Document adopted

|

|

25 May

|

Comms Plan

implemented

|

|

1 – 22

June

|

Public

consultation undertaken

|

|

8 July

|

Hearings and

deliberations

|

|

23 July

|

Revised

Annual Plan document completed

|

|

29 July

|

Annual Plan

and any new postponement and remission policies adopted

|

Decision Making

Process

43. Staff have assessed the

requirements of the Local Government Act 2002 in relation to this item and have

concluded that, as this report is for information only, the decision making

provisions do not apply.

|

Recommendation

That Hawke’s Bay Regional Council

receives and notes the “Annual Plan Update” staff report.

|

Authored by:

|

Bronda Smith

Chief Financial Officer

|

|

Approved by:

|

Jessica

Ellerm

Group Manager

Corporate Services

|

|

Attachment/s

There are no

attachments for this report.