Meeting of the Finance Audit & Risk Sub-committee

Date: Wednesday 6 June 2018

Time: 9.00am

|

Venue:

|

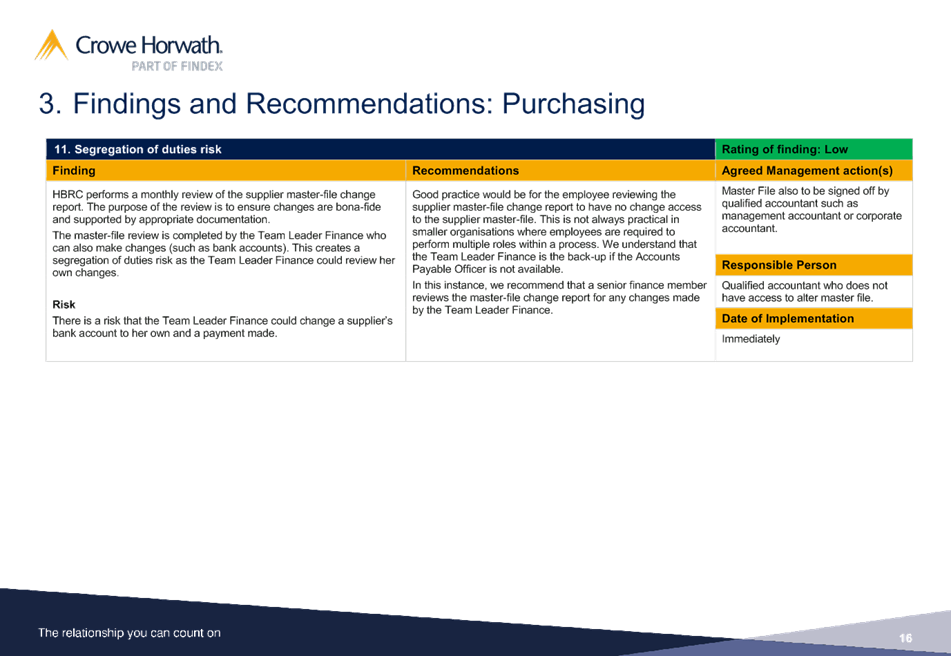

Council Chamber

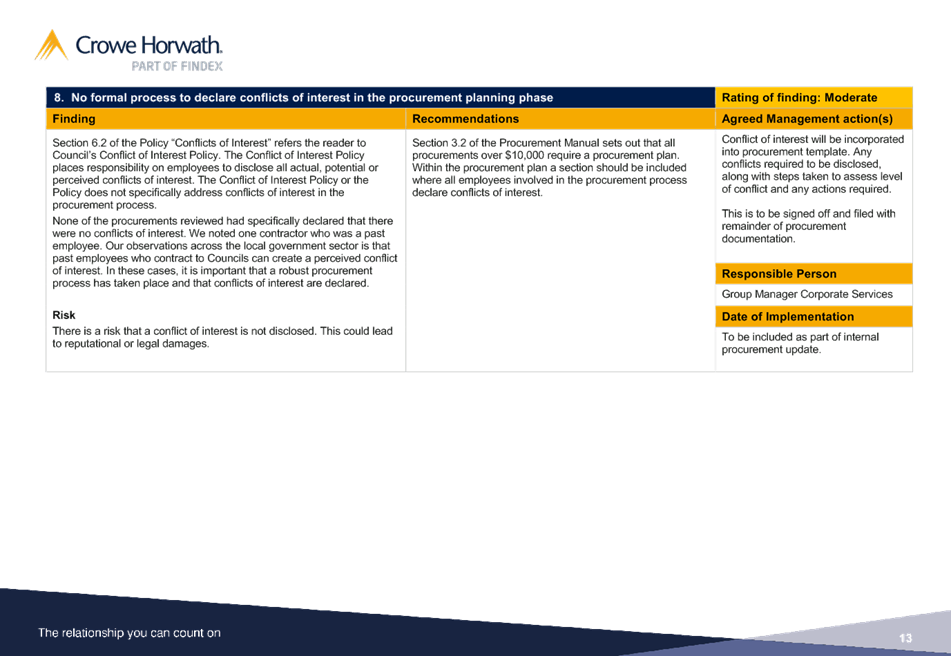

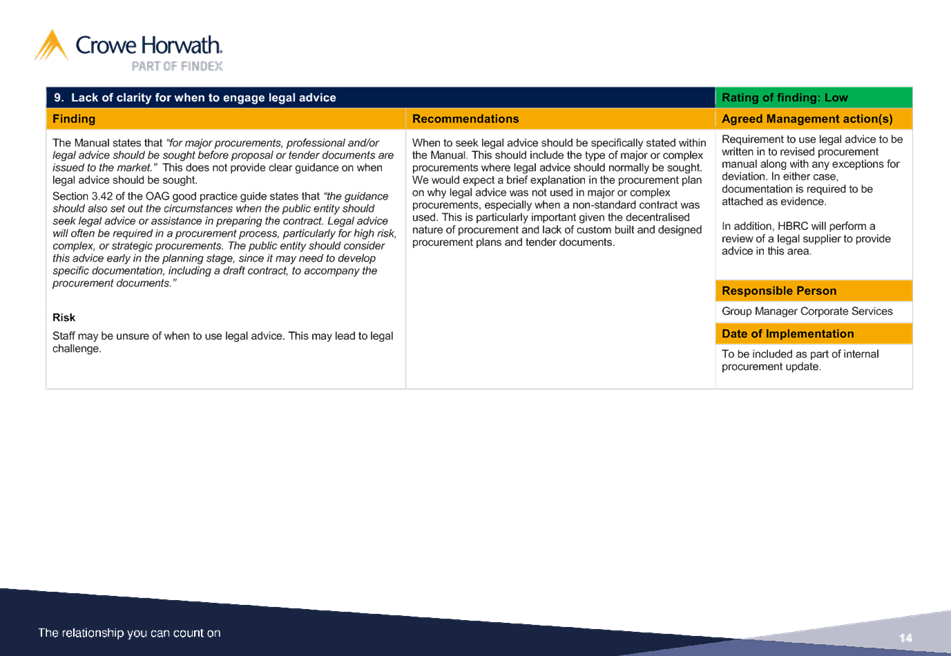

Hawke's Bay Regional Council

159 Dalton Street

NAPIER

|

Agenda

Item Subject Page

1. Welcome/Notices/Apologies

2. Conflict

of Interest Declarations

3. Confirmation of

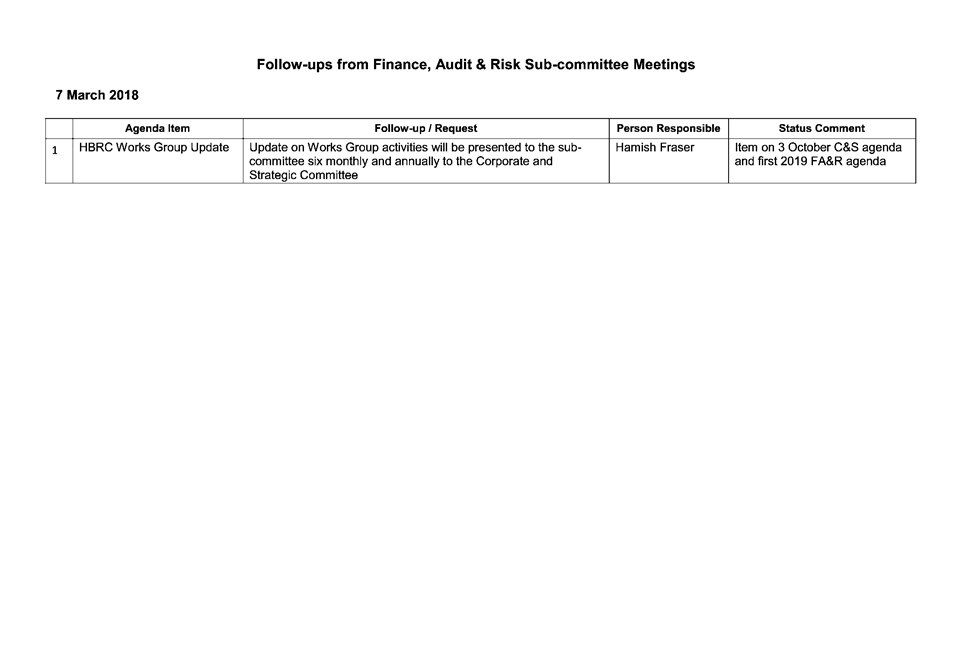

Minutes of the Finance Audit & Risk Sub-committee held on 7 March 2018

4. Follow-ups from

Previous Finance Audit & Risk Sub-committee Meetings 3

Decision Items

5. Procurement and

Contract Management Internal Audit 7

6. Living Wage

Implications Memorandum 47

7. Water Management

Internal Audit 67

8. Proposed 2018-19

Internal Audit Programme 97

9. HBRIC Ltd and

Napier Port Valuations 119

Information or Performance Monitoring

10. Local Government Act Section

17a Reviews 121

11. Resource Management

Information System Implementation Update 127

12. David Benham Resignation 129

13. June 2018 Update on the

Sub-committee Work Programmes 131

Decision Items (Public Excluded)

14. Proposed 2018-19 Council

Insurance Programme 133

HAWKE’S BAY REGIONAL COUNCIL

Finance

Audit & Risk Sub-committee

Wednesday 06 June 2018

SUBJECT: Follow-ups from Previous Finance

Audit & Risk Sub-committee Meetings

Reason for Report

1. In order to track items raised at previous meetings that require

follow-up, a list of outstanding items is prepared for each meeting. All

follow-up items indicate who is responsible for each, when it is expected to be

completed and a brief status comment. Once the items have been completed and

reported to the Committee they will be removed from the list.

Decision

Making Process

2. Council is required to make every decision in

accordance with the Local Government Act 2002 (the Act). Staff have assessed

the in relation to this item and have concluded that as this report is for

information only and no decision is required, the decision making procedures

set out in the Act do not apply.

|

Recommendation

That the Finance, Audit and Risk Sub-committee receives

and notes the report “Follow-ups from Previous Finance Audit and

Risk Sub-committee Meetings”.

|

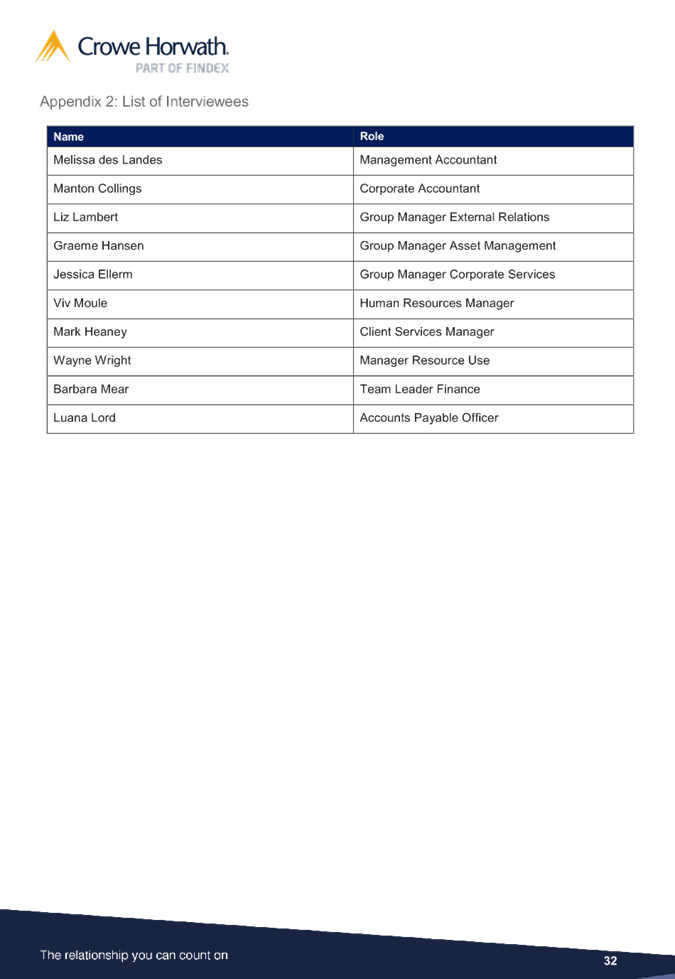

Authored by:

|

Melissa des

Landes

Management Accountant

|

|

Approved by:

|

Jessica

Ellerm

Group Manager Corporate Services

|

|

Attachment/s

|

⇩1

|

Follow-ups

from Prevoius Sub-committee Meetings

|

|

|

|

Follow-ups

from Prevoius Sub-committee Meetings

|

Attachment 1

|

HAWKE’S BAY REGIONAL COUNCIL

Finance

Audit & Risk Sub-committee

Wednesday 06 June 2018

Subject: Procurement and

Contract Management Internal Audit

Reason for Report

1. To present the

internal audit report for Procurement (with the Living Wage extension covered

in a separate item).

Background

2. The Finance,

Audit and Risk Sub-committee included Procurement as part of the internal audit

work programme for 2017-18, and agreed to the scope on 7 March 2018.

3. During the

Procurement audit it was identified that there were several links with Contract

Management so the audit scope was extended to include this, rather than having

to do a separate audit at a later date.

4. The audit

report, with management commentary provided against each recommendation, is

attached.

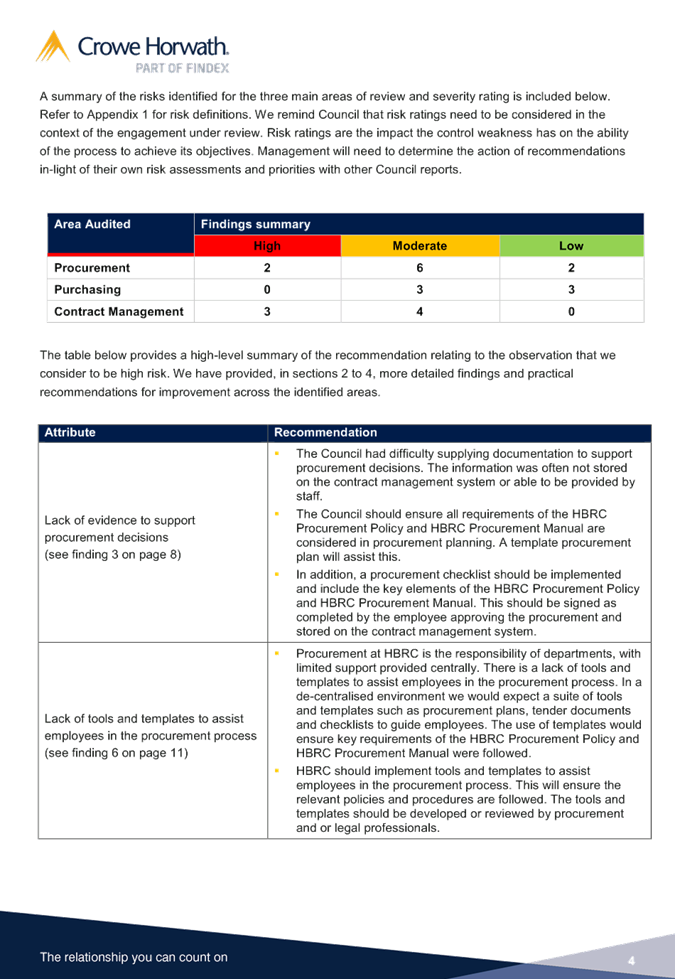

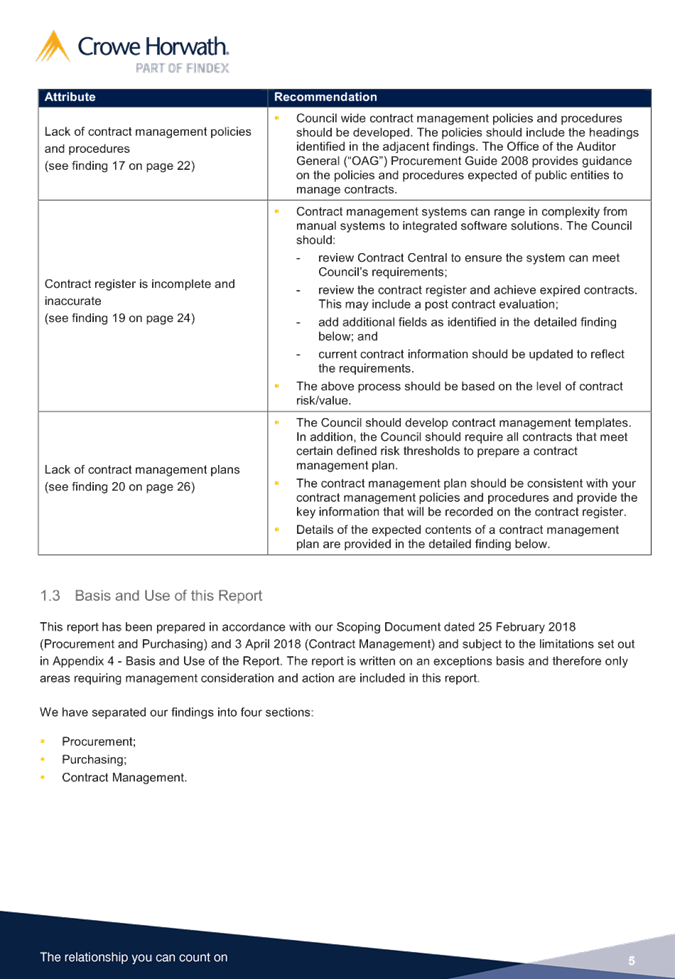

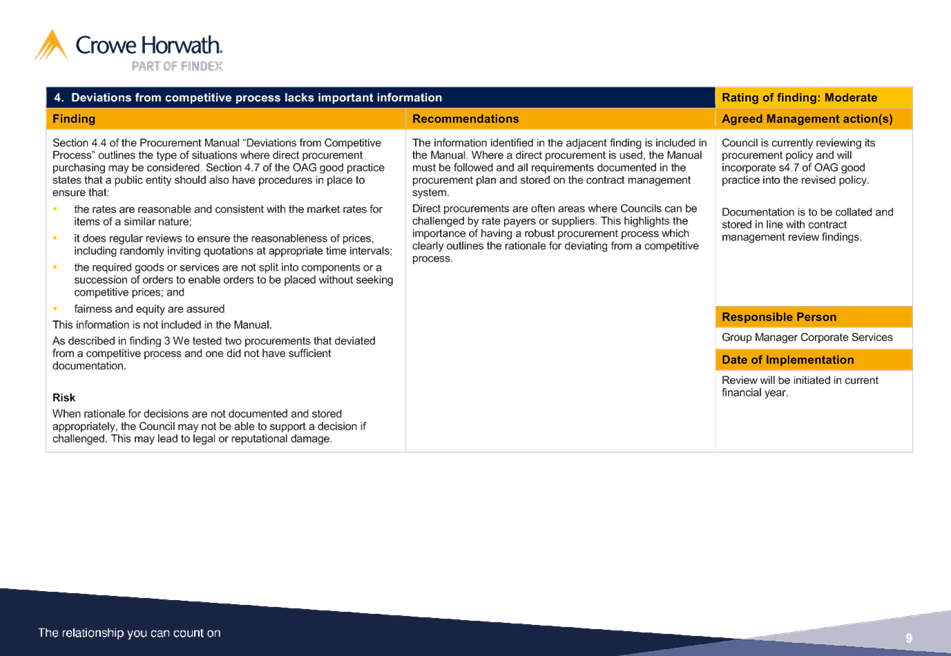

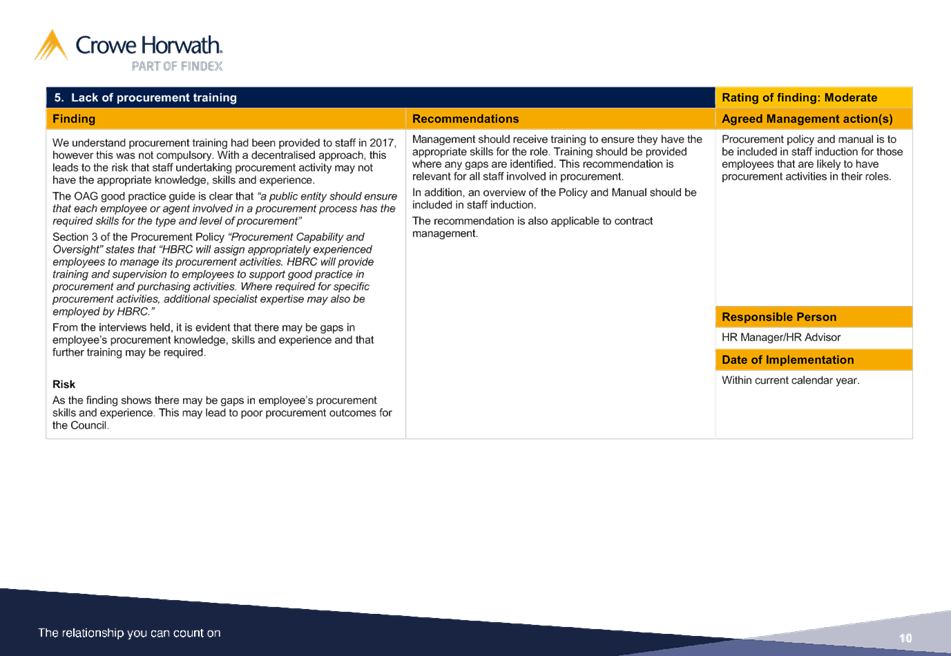

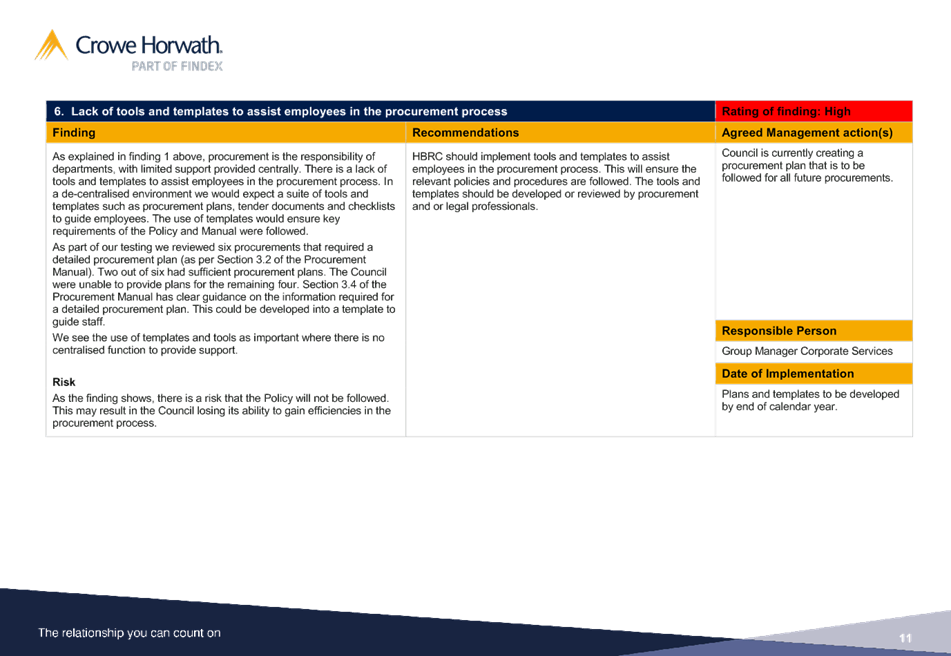

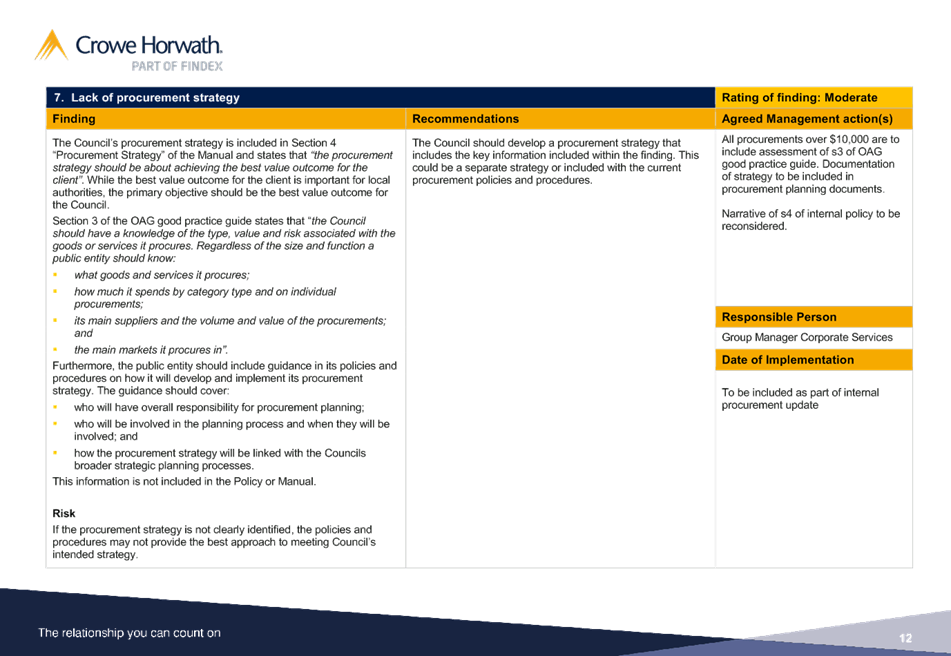

Key Findings

5. The findings

from the Crowe Horwath report are summarised below:

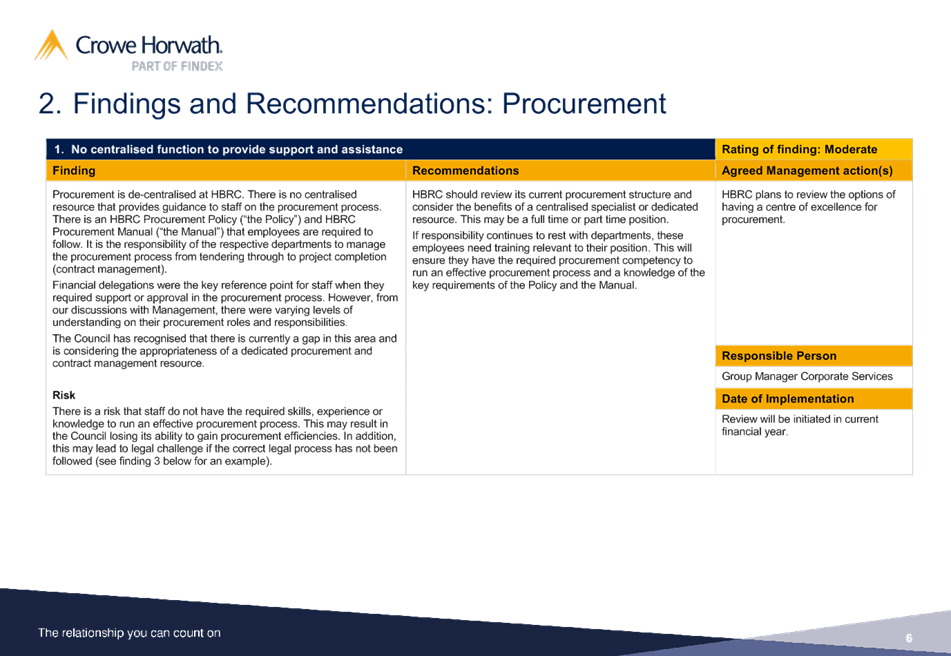

6. There is a lack

of a procurement “Centre of Excellence” within Council. Each team

is expected to manage their own procurement processes with no centralised point

for advice, review, or input from a procurement specialist. There is a risk of

inconsistent processes being used due to lack of knowledge or oversight.

7. There is a lack

of standardised procurement templates within HBRC. There is no

procurement planning checklist to indicate areas for consideration such as

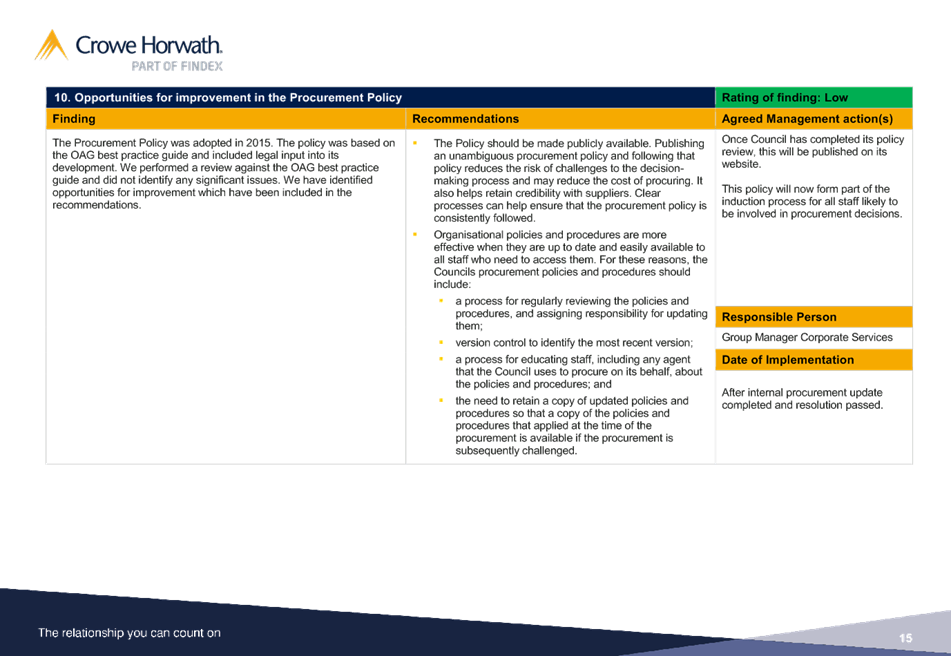

conflicts of interest, buying local or sustainable business practices.

8. The HBRC

procurement policy was deemed to be good overall, however certain aspects

needed further refinement. For example there is currently no guidance on when

obtaining legal advice could be beneficial or essential.

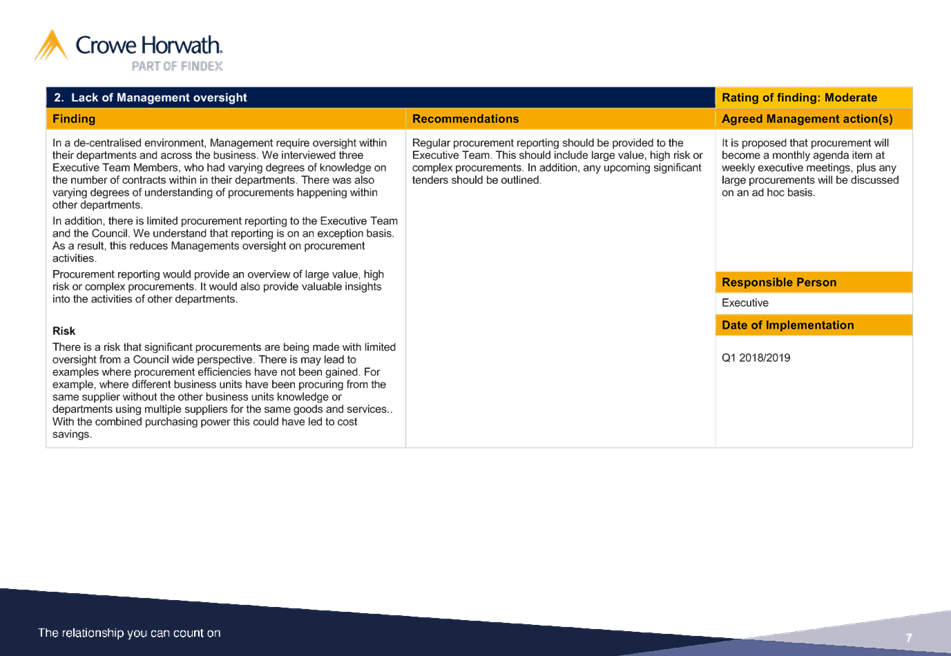

9. There is no

standard or regular forum for management and executive to share oversight of

procurement activities, such as any major or high public interest procurements.

This lack of information sharing may also lead to risk of failure to identify

opportunities for procurement efficiencies.

10. The current document

management system HBRC uses is very basic in nature and is not being utilised

consistently. It also has limited functionality and is deemed to be more of a

storage system as opposed to a document management system.

11. Council currently has a

large volume of contracts and oversight is inconsistent. Some contracts are

routinely extended and it is not clear or documented whether these contracts

are providing best value for money. A dedicated resource would assist with

ensuring completeness and proper negotiation of renewals. This work may also

tie in with Section 17a reviews.

Analysis

12. The key finding from the

procurement and contract management audit is that the current decentralisation

of these activities leads to various risks. It is noted that the preferred

methodology to combat this is by the creation of a dedicated procurement

specialist role.

13. Staff have sought guidance

from the Ministry of Business and Innovation (MBIE) procurement department, and

feedback regarding the employment of a procurement specialist has been strongly

recommended. This is also benchmarked against other councils of similar size.

14. Specifically, for an

organisation of HBRC’s size and scale, MBIE have informally recommended 1

x procurement FTE to be at Senior Leadership Team level. This is due to the

level of work likely to be involved, along with the requirement for that person

to have sufficient stature within the organisation to drive results.

15. MBIE has provided HBRC

with a full procurement competency framework which outlines roles and

responsibilities of various individuals involved in procurement. A headline of

job titles is provided below and HBRC would be best to recruit in the Level 2/

3 space.

16. Staff note, however, that

the cost efficiencies gained by a procurement resource can often be difficult

to quantify although feedback given from MBIE and other councils is that a

dedicated procurement resource tends to “pay for itself”. This

extends beyond the financial benefits, to reducing reputational risks by

ensuring that proper probity has been followed. Dedicated procurement also

allows scope for innovation and value-add opportunities.

Options

17. Staff have considered the

findings of this report and noted that additional resource is needed in the

procurement and contract management space. Due to timing of the delivery of the

report, funding for a dedicated new hire has not been included in the LTP.

18. Staff appreciate that

2018-19 budgets may not allow for a dedicated resource for immediate hire, and

so management will be exploring options including:

18.1. A phased approach with

the development of procurement templates and plans created internally where

capacity allows. This approach is affordable under current budgets however it

is noted that the process will be slow and does not sufficiently mitigate procurement

risks due to lack of dedicated oversight.

18.2. Create a new procurement

specialist role responsible for ensuring consistency in approach to procurement

policies, internal advice to staff, drive s17a efficiency reviews and be

involved in negotiating contracts. The role would also provide oversight to the

contract management storage system to ensure that it is being used correctly

and ensure best value for money is consistently achieved throughout Council.

This option is not provided for in the 2018-19 budgets and would rely on cost

savings achieved elsewhere in the organisation for funding.

18.3. Employ a staff member on

a fixed term basis to create and roll out correct procurement templates, plans

and contracts within HBRC. Upon expiry of the contract, it would be

staff’s responsibility to use the correct templates consistently. This

may not address the requirement for ongoing contract negotiation and

monitoring, does not sufficiently address long term procurement risks and is

not funded in 2018-19 budgets.

18.4. A combination of the

above, that internal staff create templates using existing MBIE

procurement guideline templates, and a dedicated procurement resource be

further explored in the 2019-20 financial year.

Decision

Making Process

19. Council

and its committees are required to make every decision in accordance with the

requirements of the Local Government Act 2002 (the Act). Staff have assessed

the requirements in relation to this item and have concluded:

19.1. The decision

does not significantly alter the service provision or affect a strategic asset.

19.2. The use of

the special consultative procedure is not prescribed by legislation.

19.3. The decision

does not fall within the definition of Council’s policy on significance.

19.4. The persons affected by this

decision are HBRC staff.

19.5. The decision

is not inconsistent with an existing policy or plan.

19.6. Given

the nature and significance of the issue to be considered and decided, and also

the persons likely to be affected by, or have an interest in the decisions

made, Council can exercise its discretion and make a decision without

consulting directly with the community or others having an interest in

the decision.

|

Recommendations

That the Finance, Audit and Risk Sub-committee:

1. Receives and notes the “Procurement and Contract

Management Internal Audit Report” staff report.

2. Accepts the commentary, including any

follow-up actions, provided against each of the report’s

recommendations by HBRC Executive staff.

|

Authored by:

|

Melissa des

Landes

Management Accountant

|

Mark Heaney

Manager Client Services

|

Approved by:

|

Jessica

Ellerm

Group Manager Corporate Services

|

|

Attachment/s

|

⇩1

|

Crowe Horwath

Procurement & Contract Management Review Internal Audit Report

|

|

|

|

Crowe

Horwath Procurement & Contract Management Review Internal Audit Report

|

Attachment 1

|

|

Crowe

Horwath Procurement & Contract Management Review Internal Audit Report

|

Attachment 1

|

|

Crowe

Horwath Procurement & Contract Management Review Internal Audit Report

|

Attachment 1

|

HAWKE’S BAY REGIONAL

COUNCIL

Finance

Audit & Risk Sub-committee

Wednesday 06 June 2018

Subject: Living Wage

Implications Memorandum

Reason

for Report

1. To provide the

Sub-committee with the Crowe Horwath Living Wage memorandum for review and

consideration.

2. Staff are

requesting feedback from the Sub-committee, in the form of recommendations to

the Corporate and Strategic Committee, then on to Council, about the potential

inclusion of ‘living wage’ considerations in Council’s

procurement policy.

Background

3. In response to

a petition from First Union submitted in October 2017, the Corporate and

Strategic Committee agreed, at its meeting on 11 December 2017, to align a

review of the living wage with the planned Procurement internal audit review.

The agreed scope of the Living Wage review was to assess the possible

implications of promoting the living wage for contractors and more specifically

for GoBus drivers.

4. Council’s

internal auditor, Crowe Horwath, was engaged to provide a memorandum (attached)

on the implications of requiring contractors to pay the Living Wage.

5. Staff have

reviewed the findings and have provided some general commentary, along with

commentary specific to the GoBus contract.

Living Wage Analysis

6. HBRC recently

confirmed that it pays all of its own staff the living wage, however has not

consciously made this a permanent commitment by way of internal remuneration

policy.

7. In order for

businesses to pay their staff the living wage, there is a question of who would

absorb these costs. If businesses are operating at low margins, then the cost

would likely be passed on to their customers through raising prices which may

impact on their ability to be competitive.

8. If the

subsequent cost increases were passed on to HBRC, this could give rise to

section 17a issues where HBRC is required to “provide cost effective

services to the ratepayer”. This could also be seen as penalising other

low paid workers in the region to subsidise those fortunate enough to work on

HBRC contracts. For example, a self-employed worker on a low income (who does

not provide services to HBRC) would have their rates bill increase to pay for

the benefit of other workers.

9. The breaking of

contracts to introduce a living wage requirement for contractors and suppliers

may have legal and financial implications that may outweigh the benefits. A

challenge could be raised by unsuccessful suppliers who may have included

paying staff the living wage in their original tendering documents but were

unsuccessful due to price.

National Approach

10. A small number of other

Councils have decided to begin implementing the living wage selectively.

Those councils are in larger cities with a higher cost of living than

Hawke’s Bay (Wellington, Auckland and Christchurch).

11. Statistics NZ provides

information on cost of living by region, however the living wage is not indexed

to reflect those regional variations. As an example, the cost of living for an

average household is approximately $416 per week (or 36%) lower for those in

the regions than those living in Auckland.

12. In light of this,

Palmerston North City Council recently requested a review to determine a

“Palmerston North” living wage, which has currently been set at

$17.50 an hour. This reflects a lower cost of living in Palmerston North than

in major centres.

13. These Councils have also

only implemented the living wage under certain criteria, often only for their

direct staff – which HBRC currently has in place. A summary of each is

outlined below:

Auckland Council

13.1. Policy updated to

include living wage payments to staff and CCOs only. Policy excludes

contractors, volunteers and trainees.

Wellington City Council

13.2. Resolved to consider

implementing the living wage on a case by case basis however this decision was

subject to challenge by Wellington Chamber of Commerce (WCoC) noting an

intention to bring judicial review proceedings against the Council decision.

This is due to belief that a higher cost of cleaning contracts did not

represent prudent use of ratepayer resources.

13.3. After several months of

negotiations between the WCoC, Wellington City Council agreed that when a

significant contract is under renewal, there is a commitment to pay the living

wage via a phased implementation, on selected contracts only and in

consultation with WCoC.

Greater Wellington Regional Council

13.4. Has agreed to pay living

wage for staff only. Has requested Local Government New Zealand provide a legal

opinion on this area, of which the results are still outstanding.

13.5. Sees living wage as one

set of criteria in purchasing process alongside others, such as environmental

practices.

13.6. Notes that ratepayers

are likely to foot the bill and that this appears to be a problem that central

government should step in and resolve.

Christchurch City Council

13.7. Has agreed to pay living

wage to staff with the skills and experience to work unsupervised. No comment

provided by CCC on contractors/suppliers.

GoBus

Contract

14. The GoBus contract

currently sits under the national PTOM (Public Transport Operating Model). PTOM

was introduced in 2013 with the intention of driving down bus fares for its

users (bus fares currently offset approximately 50% of total operating costs,

the remainder is made up by local government and NZTA).

15. It is noted that the

Hawkes Bay GoBus contract expiry date is not until 2025. A review of this

contract now could bring about legal challenge from other suppliers who missed

out on the tender, along with potential litigation from commerce groups as

evidenced in Wellington.

16. Bay of Plenty’s

(BOP) bus contract came up for renewal last month in April and it is noted that

the winning tender agreed to pay the living wage in its contract. It should be

recognised that the winning tenderer was not GoBus, and the recent winning

supplier for BOP was a failed tender for the Hawke’s Bay contract. BOP

procurement notes that the living wage was a “factor” in its decision

making, rather than a requirement. It is also noted that this service cost an

additional $2m per annum – although this cost is made up of a number of

factors.

17. Other Councils have only

implemented living wage in contracts up for renewal. The review of unexpired

contracts has not been conducted due to challenges outlined in the memorandum.

In the case of GoBus there is an added dimension to this, including the NZTA

51% funding agreement which is also party to the contract, along with

consideration of how this will impact on bus fares.

18. On this basis, a

theoretical retender may mean that GoBus may lose the contract and the drivers

could possibly be out of jobs altogether. This is not factoring in legal

challenge costs which subject to any damages paid out, would likely go to GoBus

owners and not the drivers. The ratepayer would be required to foot this bill.

19. It should be highlighted

that GoBus drivers are also paid several dollars above minimum wage and

wages for drivers are reviewed annually at a rate in line with or above

inflation. The GoBus CEO has defended its recent pay negotiations, insisting

workers have just been given a pay increase “recently those drivers

received a very generous increase from the company, well in excess of

inflation”. GoBus drivers are now also paid at time and a half for work

on Sundays, and at a rate above the Palmerston North hourly ‘living

wage’ rate.

20. Staff have reviewed the

GoBus tender documents and note several complexities due to the NZTA

requirements and recommend that specific legal advice is obtained before

looking any further at opening up the contract.

Central Government Action

21. There is a currently a

review being conducted nationally regarding the PTOM which the GoBus contract

was formed under. This review will include the assessment of wages for bus

drivers. If Council were to make changes in line with a PTOM review overhaul,

it is unlikely that there would be any legal implications due to following of

national policy.

22. Specifically, The Ministry

of Transport has contracted an independent consultancy firm to review the PTOM

model and the effect this has on worker’s conditions and wage rates. HBRC

was contacted by the Ministry recently and advised that the consultancy firm

will be in contact to request information on conditions and wage rates for bus

drivers in our region.

23. Staff intend to report

back to the Finance, Audit & Risk sub-committee with updates and results

that arise from this review.

Decision

Making Process

24. Council

and its committees are required to make every decision in accordance with the

requirements of the Local Government Act 2002 (the Act). Staff have assessed

the requirements in relation to this item and have concluded:

24.1. The

decision does not significantly alter the service provision or affect a

strategic asset.

24.2. The use

of the special consultative procedure is not prescribed by legislation.

24.3. The

decision does not fall within the definition of Council’s policy on

significance.

24.4. The

decision is not inconsistent with an existing policy or plan.

Given the nature and significance of the

issue to be considered and decided, and also the persons likely to have an

interest in the decisions made, Council can exercise its discretion and make a

decision without consulting directly with the community or others having an

interest in the decision.

|

Recommendations

That the Finance, Audit and Risk

Sub-committee:

1. Receives and notes the Crowe Horwath “Living

Wage” memorandum and staff report.

2. Accepts the commentary provided by HBRC Executive

staff in response to the Crowe Horwath memorandum.

The Finance, Audit and Risk Sub-committee recommends that the

Corporate and Strategic Committee:

3. Agrees that the decisions to be made are not significant under the

criteria contained in Council’s adopted Significance and Engagement

Policy, and that the Committee can exercise its discretion and make decisions

on this issue without conferring directly with the community and persons

likely to be affected by or to have an interest in the decision.

4. Recommends that Council:

4.1. Participates

in and continually monitors results of the Public Transport Operating Model

review and/or any central government policy changes that necessitate the

reassessment of the GoBus contract to align with legislation and its own

internal policies accordingly.

4.2. Requests

that staff amend Council’s procurement policy to give weighting to

contractors who are paying the living wage, alongside other important factors

such as environmentally friendly business practices and overall

affordability, in Tender evaluation processes.

4.3. Requests

that Council’s procurement policy is published on the HBRC website (in

line with the Procurement Review recommendations from Crowe Horwath).

|

Authored by:

|

Melissa des

Landes

Management Accountant

|

Manton

Collings

Corporate Accountant

|

Approved by:

|

Jessica

Ellerm

Group Manager Corporate Services

|

|

Attachment/s

|

Living

Wage Memo

|

Attachment 1

|

HAWKE’S BAY REGIONAL COUNCIL

Finance

Audit & Risk Sub-committee

Wednesday 06 June 2018

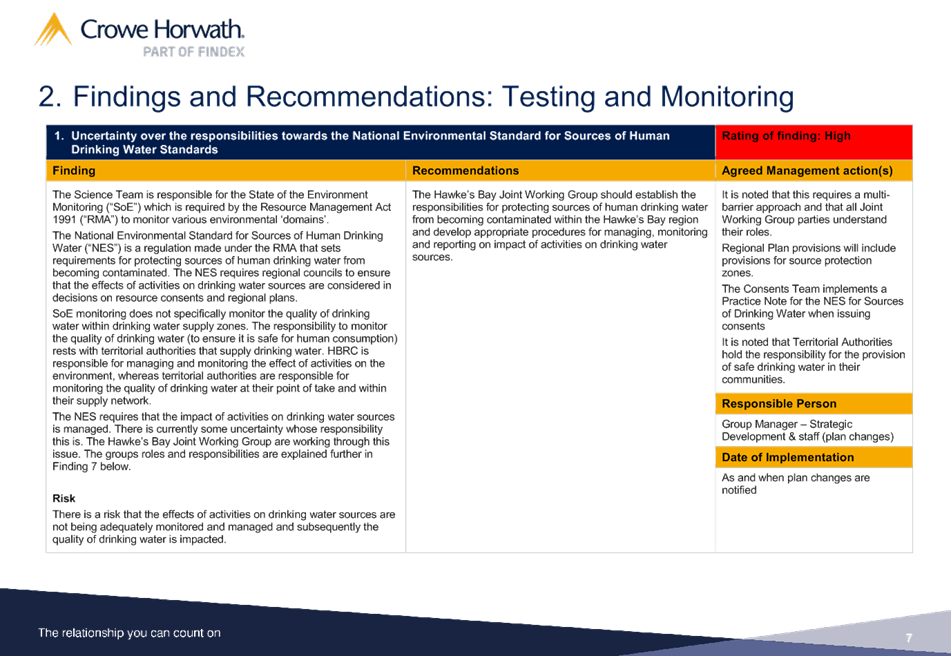

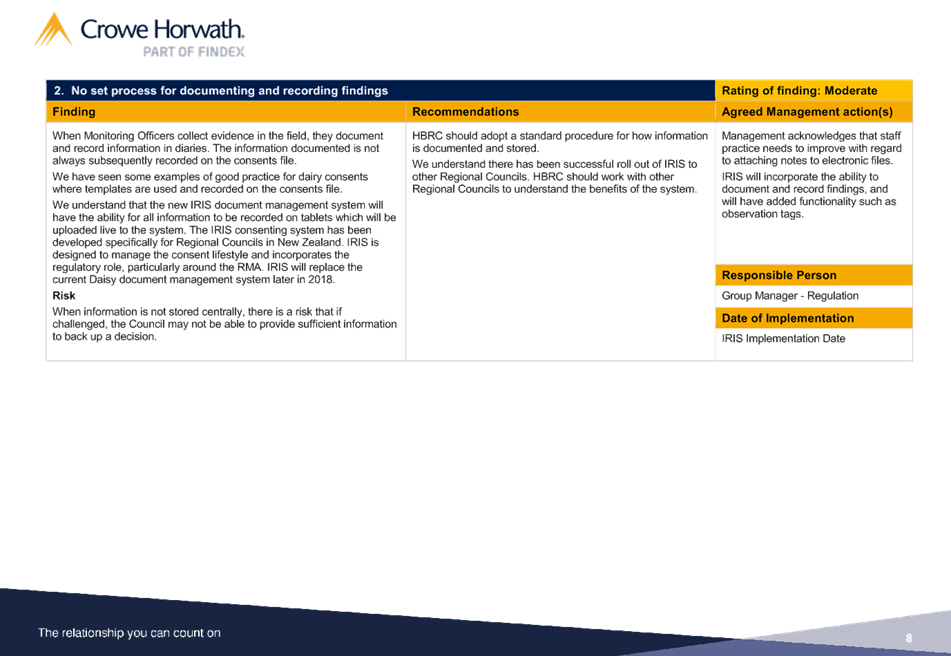

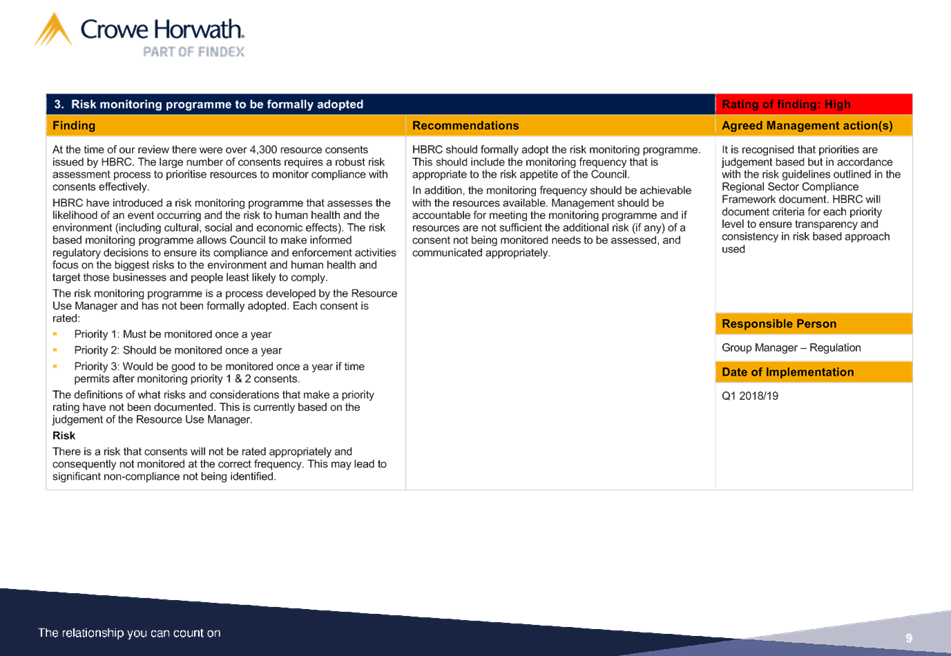

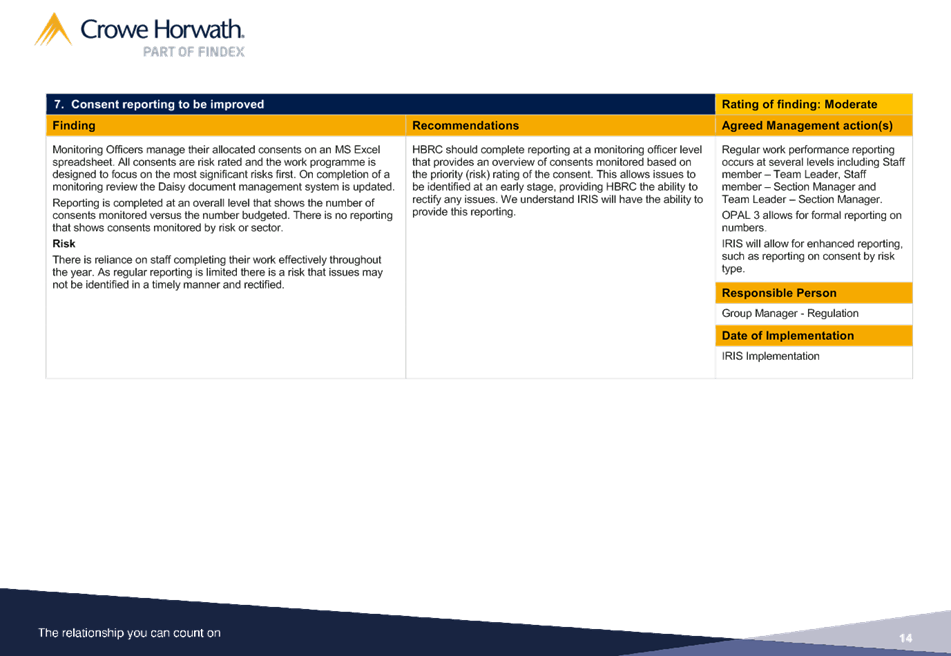

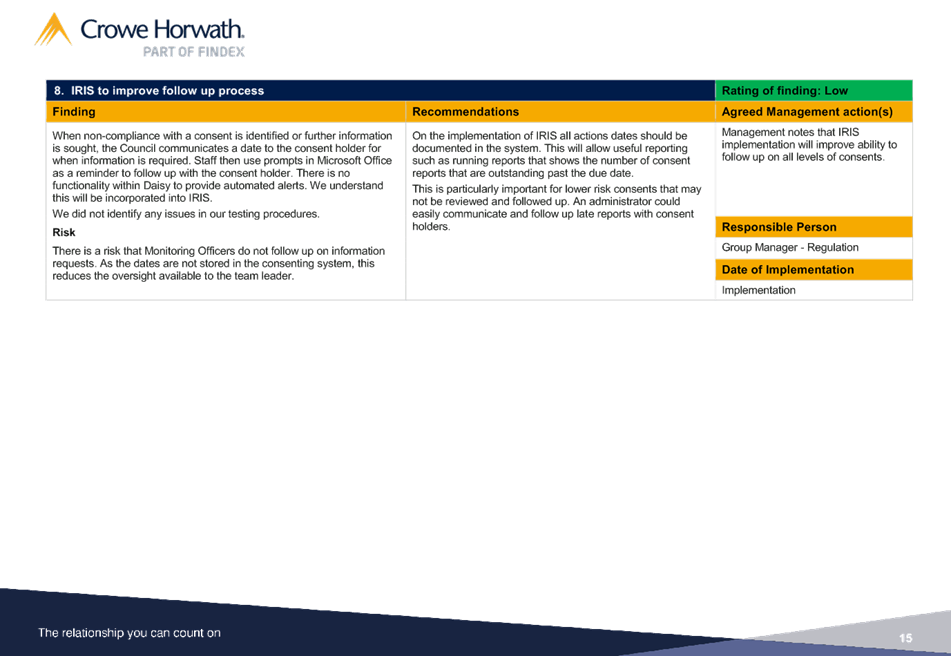

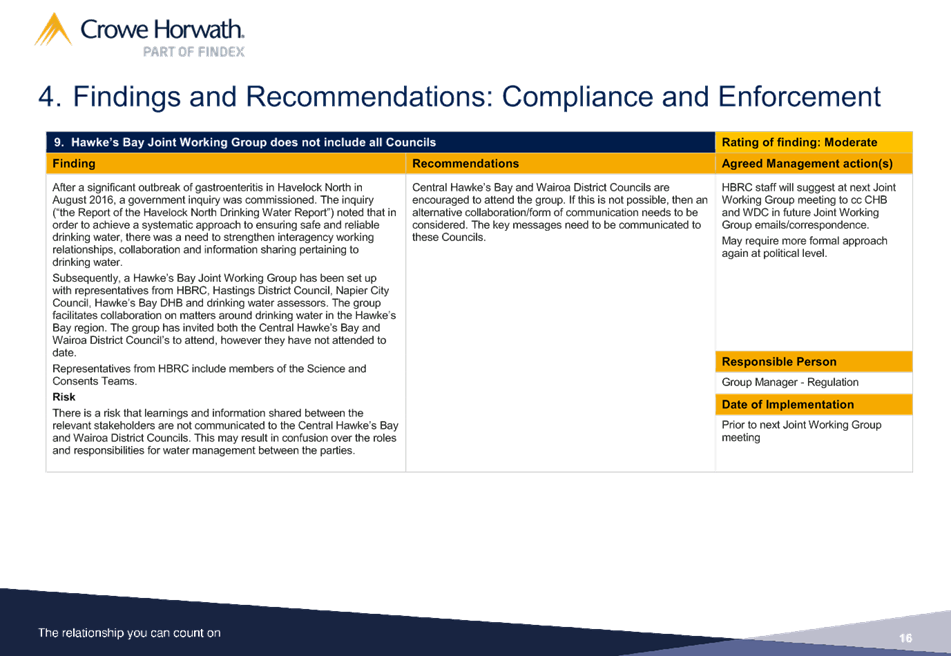

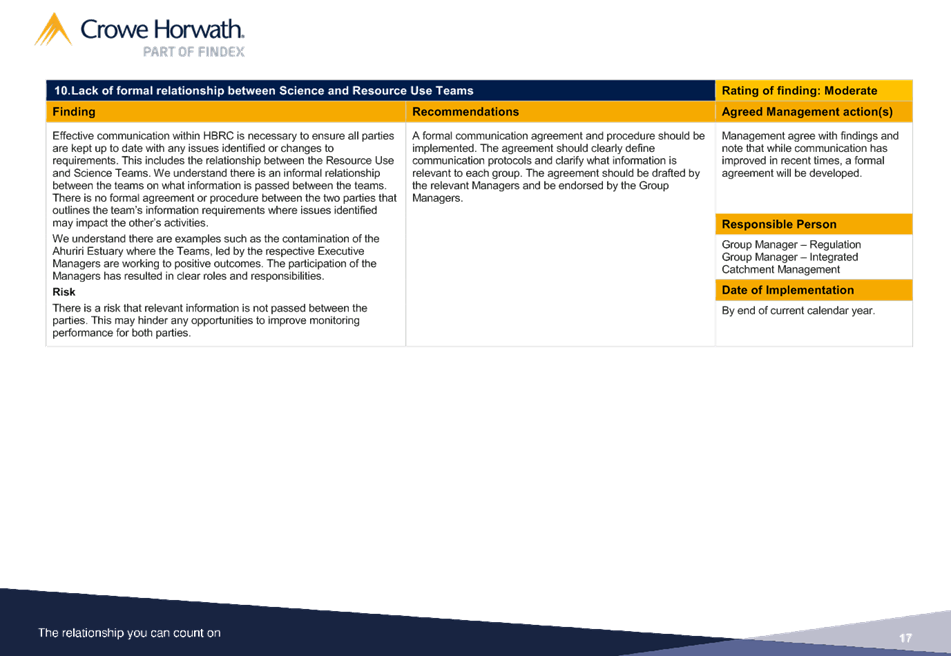

Subject: Water Management

Internal Audit

Reason for Report

1. To provide the

Crowe Horwath Water Management internal audit report (attached) for review by

the Sub-committee.

Background

2. The Finance,

Audit and Risk sub-committee agreed at its meeting on 9 September 2017 to

include Water Management as part of the internal audit work programme. After a

series of iterations, the scope was agreed at the Regional Council meeting on

31 January 2018.

3. The findings report

has been reviewed by the HBRC Executive team, who have provided commentary

against each of the recommendations.

Decision

Making Process

4. Council and its committees are required to make every decision in

accordance with the requirements of the Local Government Act 2002 (the Act).

Staff have assessed the requirements in relation to this item and have

concluded:

4.1. The decision does not significantly alter the service provision or

affect a strategic asset.

4.2. The use of the special consultative procedure is not prescribed by

legislation.

4.3. The decision does not fall within the definition of Council’s

policy on significance.

4.4. The persons

affected by this decision are HBRC staff.

4.5. The decision is not inconsistent with an existing policy or plan.

4.6. Given the nature and significance of the issue to be considered and

decided, and also the persons likely to be affected by, or have an interest in

the decisions made, the Finance, Audit and Risk Sub-committee can exercise its

discretion and make a decision without consulting directly with the community

or others having an interest in the decision.

|

Recommendations

The Finance,

Audit and Risk Sub-committee:

1. Receives and notes the Crowe Horwath Water Management Internal

Audit report.

2. Accepts the commentary, including any

follow-up actions, provided against each of the report’s

recommendations by HBRC Executive staff.

|

Authored by: Approved

by:

|

Melissa des

Landes

Management Accountant

|

Liz Lambert

Group

Manager External Relations

|

Attachment/s

|

⇩1

|

Crowe Horwath

Water Management Internal Audit Report

|

|

|

|

Crowe

Horwath Water Management Internal Audit Report

|

Attachment 1

|

|

Crowe

Horwath Water Management Internal Audit Report

|

Attachment 1

|

|

Crowe

Horwath Water Management Internal Audit Report

|

Attachment 1

|

HAWKE’S BAY REGIONAL

COUNCIL

Finance

Audit & Risk Sub-committee

Wednesday 06 June 2018

Subject: Proposed 2018-19

Internal Audit Programme

Reason for Report

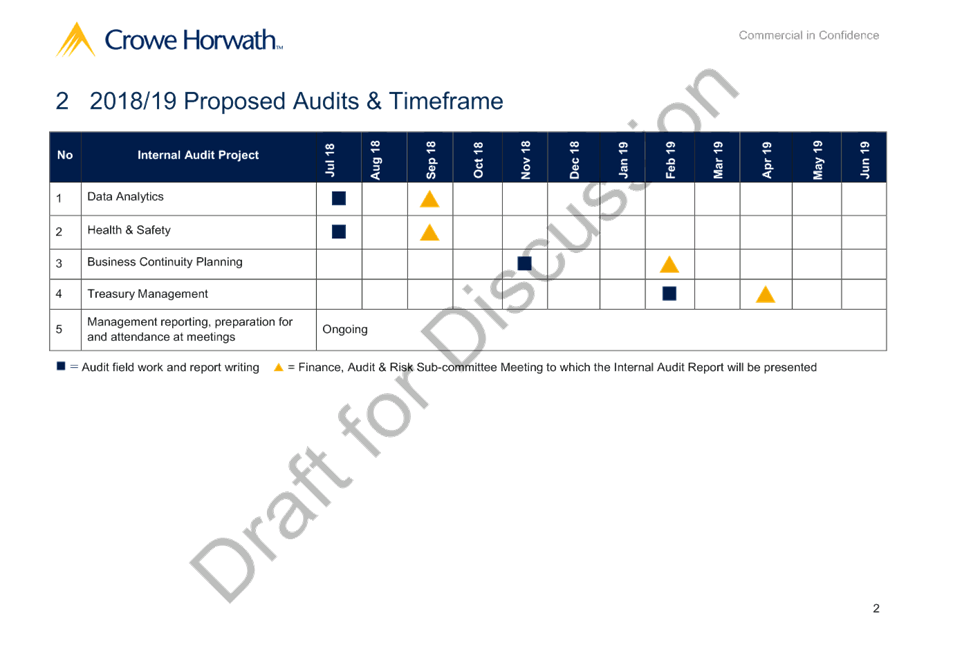

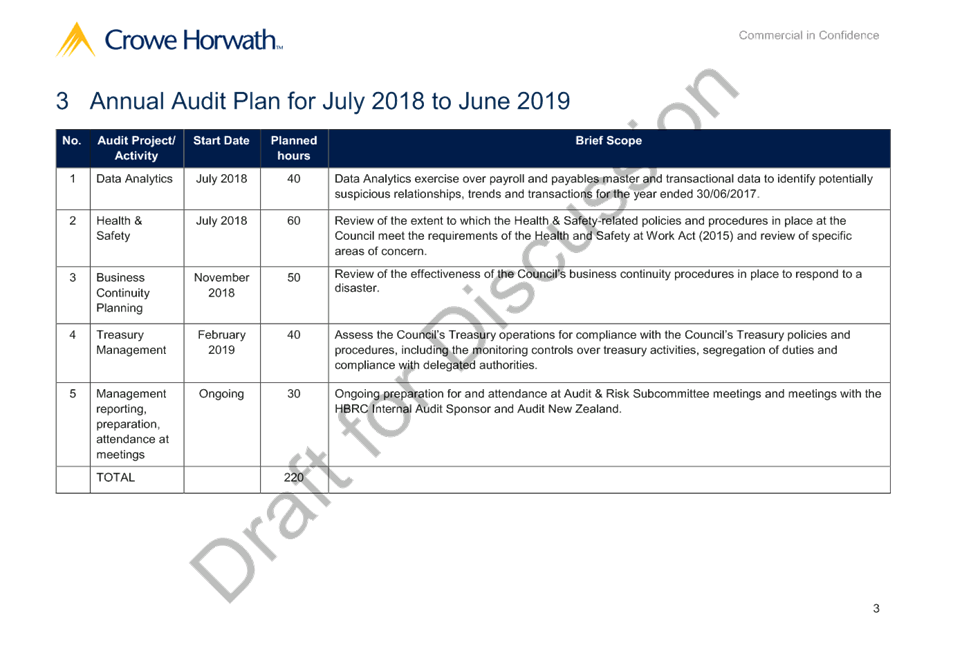

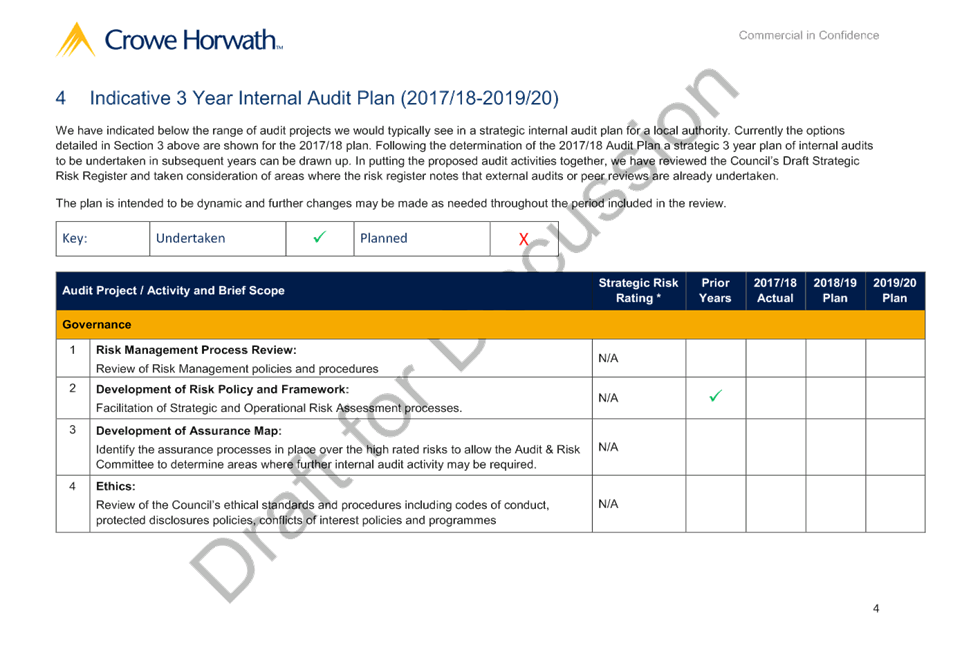

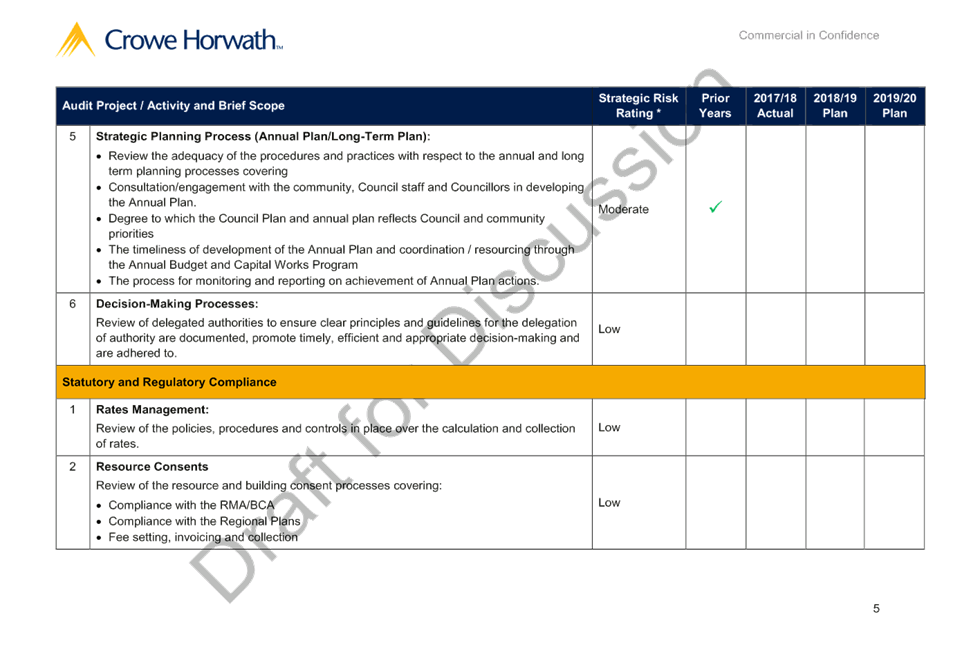

1. To propose an

internal audit programme for the 2018-19 financial year for agreement of the

Sub-committee.

Background

2. During the

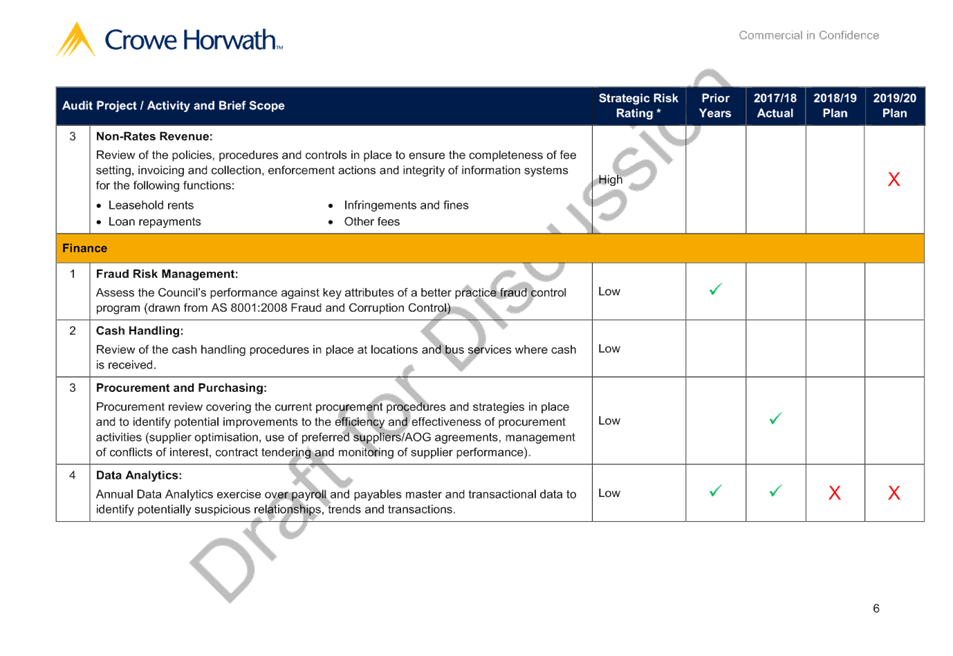

current financial year HBRC’s internal auditors, Crowe Horwath, have

conducted a series of internal audits including:

2.1. Data

Analytics

2.2. Water

Management

2.3. Procurement/Living

Wage/Contract Management.

Options Assessment

3. In consultation

with Crowe Horwath, and based on HBRC’s risk register, staff recommend the

following internal audit programme.

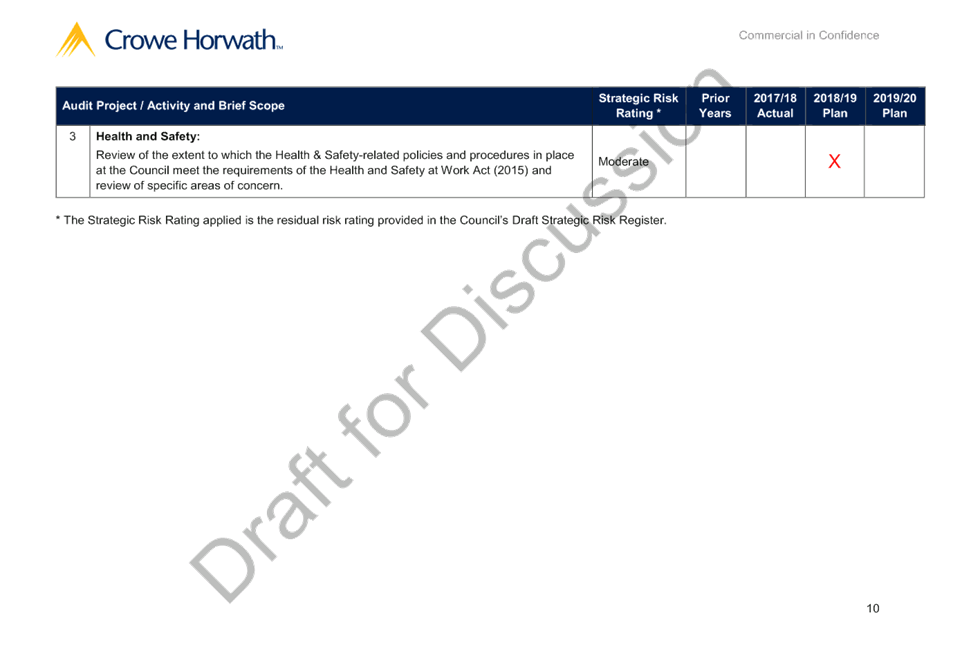

3.1. Health &

Safety

3.2. Data

Analytics

3.3. Treasury

3.4. Business

Continuity and Disaster Recovery Planning

4. Health and

Safety has been proposed due to the increasingly complex legislation in this

area and the high priority placed on health and safety by HBRC. A scope

for this audit is attached for the sub-committee to review and approve.

5. The Data

Analytics audit is proposed to be repeated due to the useful information that

it provided previously and the opportunity to benchmark improvements made to

processes since that prior audit. As this audit was performed previously,

the cost and staff time involved will be reduced.

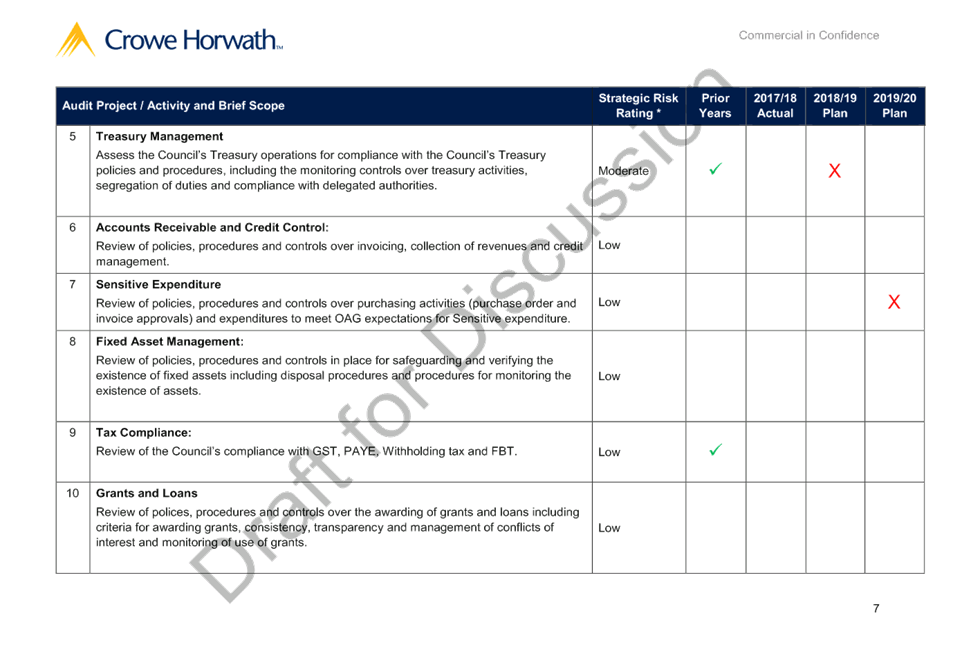

6. Treasury has

been selected due to a significant change in direction of Council’s

financial strategy signalled in the LTP, including the placement of investment

funds into a managed portfolio and significant borrowing. This audit will look

at monitoring controls, segregation of duties and compliance with delegated

authorities.

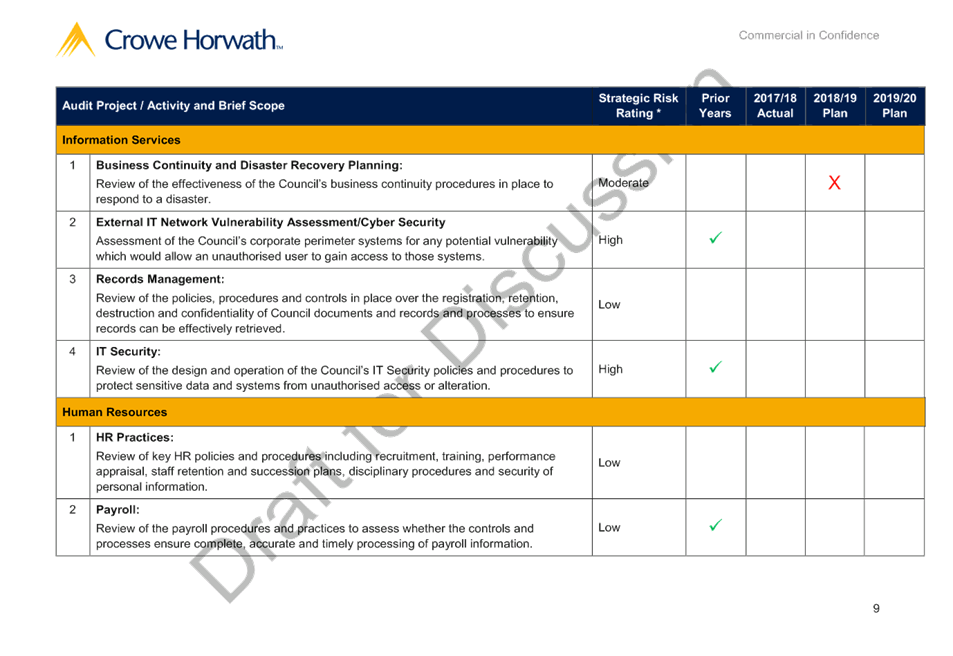

7. Business Continuity

and Disaster Recovery Planning has been selected as the current policy is due

for review and this area is listed as high risk on Council’s risk

register.

8. All of these

areas are recommendations at this stage and staff will take any guidance from

the Sub-committee for additional or reprioritising topics, as well as refining

of scope.

Decision

Making Process

9. Council and its committees are required to make every decision in

accordance with the requirements of the Local Government Act 2002 (the Act).

Staff have assessed the requirements in relation to this item and have

concluded:

9.1. The decision does not significantly alter the service provision or

affect a strategic asset.

9.2. The use of the special consultative procedure is not prescribed by

legislation.

9.3. The decision does not fall within the definition of Council’s

policy on significance.

9.4. The persons

affected by this decision are HBRC staff.

9.5. The decision is not inconsistent with an existing policy or plan.

9.6. Given the nature and significance of the issue to be considered and

decided, and also the persons likely to be affected by, or have an interest in

the decisions made, the Finance, Audit and Risk Sub-committee can exercise its

discretion and make a decision without consulting directly with the community

or others having an interest in the decision.

|

Recommendations

That the Finance, Audit and Risk sub-committee:

1. Receives and notes the “Proposed 2018-19 Internal

Audit Programme” staff report.

2. Agrees to the schedule of Internal Audits to be carried out during

the 2018-19 financial year, being:

2.1. Health and Safety

2.2. Data Analytics

2.3. Treasury

2.4. Business Continuity and Disaster Recovery Planning.

|

Authored by:

|

Melissa des

Landes

Management Accountant

|

|

Approved by:

|

Jessica

Ellerm

Group Manager Corporate Services

|

|

Attachment/s

|

⇩1

|

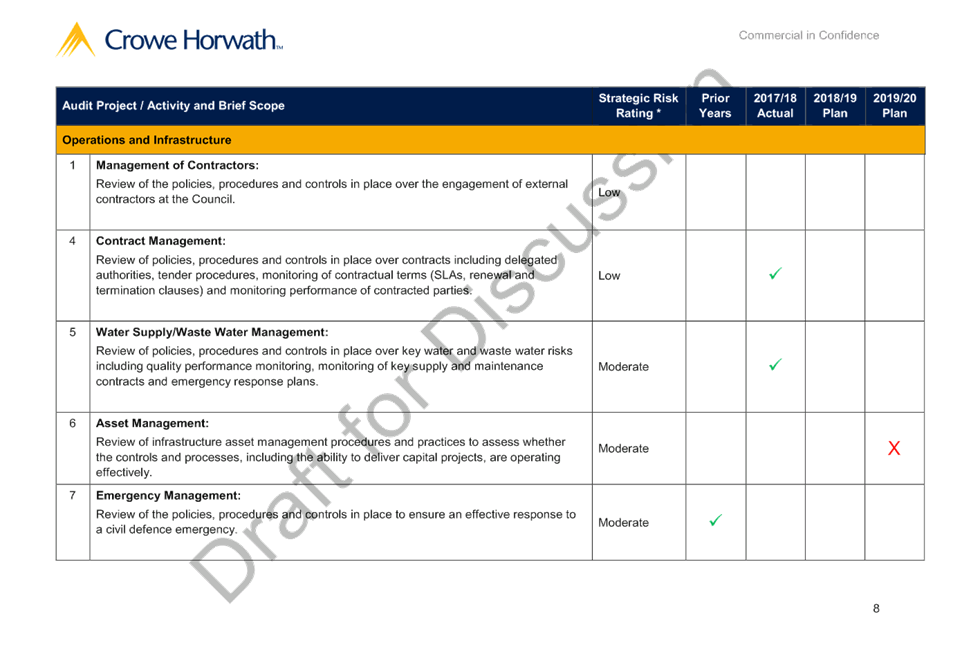

HBRC Proposed

Internal Audit Plan 2018-19

|

|

|

|

⇩2

|

HBRC HS

Assessment Proposal

|

|

|

|

HBRC

Proposed Internal Audit Plan 2018-19

|

Attachment 1

|

|

HBRC

Proposed Internal Audit Plan 2018-19

|

Attachment 1

|

|

HBRC

Proposed Internal Audit Plan 2018-19

|

Attachment 1

|

|

HBRC

HS Assessment Proposal

|

Attachment 2

|

HAWKE’S BAY REGIONAL COUNCIL

Finance

Audit & Risk Sub-committee

Wednesday 06 June 2018

Subject: HBRIC Ltd and Napier

Port Valuations

Reason for Report

1. To seek the

Sub-committee’s recommendation to the Corporate and Strategic Committee

on an approach for the triennial valuation of the Hawke’s Bay Regional

Investment Company Ltd (HBRIC Ltd) for the year ended 30 June 2018.

Background

2. In line with

accounting guidelines, Council revalues the HBRIC Ltd investment on a triennial

basis. This valuation incorporates HBRIC Ltd’s own valuation of their

investment in Napier Port. This was last completed for the year ended 30 June

2015, so is due to be completed again.

3. Council

previously used Deloitte to undertake the triennial valuations of both HBRIC

Ltd and Napier Port, and to carry out annual reviews of those valuations to

notify of any significant movements in the interim years.

Discussion

4. HBRIC Ltd has

indicated that they will use Flagstaff materials to perform the valuation of

Napier Port given the amount of work that Flagstaff has done for the Port in

relation to capital funding options. The reason for doing so is not to incur

costs of around $15,000 given the work has already effectively been undertaken

by Flagstaff.

5. Flagstaff

valuations are based on potential sale values from a possible capital

transaction and this may be different from the traditional accounting

valuation, which is likely more conservative. The valuation is dependent

on which methodology is used and what assumptions are incorporated into the

model.

6. Council needs

to decide if they are comfortable using the Flagstaff information as the basis

for the HBRIC Ltd valuation or if they wish to get an independent valuation of

both. At the end of the process Council needs to have comfort about the

value on the HBRC and Group financial statements, while the HBRIC Ltd board

will need to ensure their own comfort over the valuation used in their

financial statements.

7. The complexity

is that the valuation may affect the perceived sale price of any capital value.

8. There is budget

set aside for a full valuation of both entities.

Decision

Making Process

9. Council is required to make every decision in accordance with the

requirements of the Local Government Act 2002 (the Act). Staff have assessed

the requirements in relation to this item and have concluded:

9.1. The decision does not significantly alter the service provision or

affect a strategic asset.

9.2. The use of the special consultative procedure is not prescribed by

legislation.

9.3. The decision does not fall within the definition of Council’s

policy on significance.

9.4. Given the nature and significance of the issue to be considered and

decided, and also the persons likely to be affected by, or have an interest in

the decisions made, Council can exercise its discretion and make a decision

without consulting directly with the community or others having an

interest in the decision.

|

Recommendations

1. That the Finance, Audit and Risk Sub-committee receives and notes

the “HBRIC Ltd and Napier Port Valuations “ staff

report.

2. The Finance, Audit and Risk Sub-committee recommends that the

Corporate and Strategic Committee:

2.1. Agrees that the decisions to be made are not significant under the

criteria contained in Council’s adopted Significance and Engagement

Policy, and that the Committee can exercise its discretion and make decisions

on this issue without conferring directly with the community and persons

likely to be affected by or to have an interest in the decision.

2.2. Recommends to Council that it uses the Napier Port valuation

provided by HBRIC Ltd as the basis for the valuation of HBRIC Ltd

OR

2.3. Recommends to Council that it seeks independent valuations of both

Napier Port and HBRIC Ltd.

|

Authored by:

|

Manton

Collings

Corporate Accountant

|

|

Approved by:

|

Jessica

Ellerm

Group Manager Corporate Services

|

|

Attachment/s

There are no

attachments for this report.

HAWKE’S BAY REGIONAL COUNCIL

Finance

Audit & Risk Sub-committee

Wednesday 06 June 2018

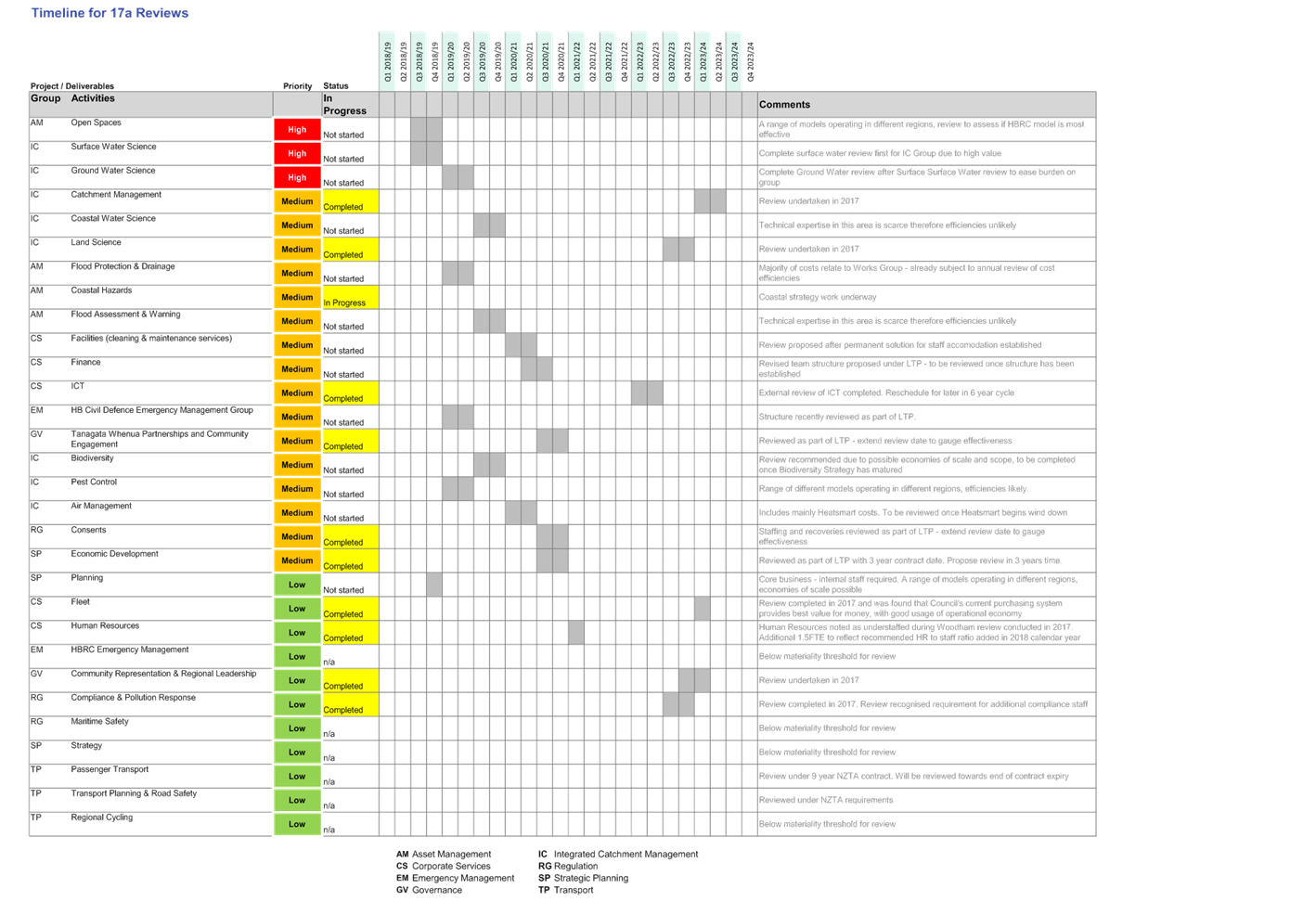

Subject: Local Government Act

Section 17a Reviews

Reason for Report

1. To provide an update on progress with s17a activities reviews.

Introduction

2. At its meeting held 7 March 2018, the Finance, Audit & Risk

Sub-committee was advised that staff would report back to this meeting to

advise a proposed plan to review the efficiencies of its activities to meet its

obligations under s17a of the Local Government Act (2002).

3. The Sub-committee was also advised that Council has been actively

reviewing various aspects of the organisation’s efficiency through various

functional reviews undertaken in the current financial year and/or through

development of the Long Term Plan.

Legislative Background

4. Section 17a reviews were introduced as part of the

Government’s 2012 Better Local Government reform programme, designed to

encourage and enable local authorities to improve the efficiency and

effectiveness of their operations and processes.

5. Council is required to give effect to the purpose of local

government as prescribed by Section 10 of the LGA, which is “to meet the

current and future needs of communities for good quality local infrastructure,

local public services, and performance of regulatory functions in a way that is

most cost effective for households and businesses. Good quality means

infrastructure, services and performance that are efficient and effective and

appropriate to present and anticipated future circumstances.”

6. S17a reviews are required:

6.1. Every six years after previous review

6.2. Before expiry of contracts related to the delivery of infrastructure,

services or regulatory functions

6.3. When significant changes to service levels are considered.

Threshold

7. Initial steps required under s17a include proposing a materiality

threshold value for the reviews. Analysis has been undertaken and the

level for creating exceptions to Section 17a has been assessed at $300,000

based on peer review and total Council spend (total budgeted operational and

capital expenditure).

8. In the absence of other factors (e.g. high probability of

significant savings, high public interest in the service), where a service has

gross annual expenditure of less than $300,000 it will be assumed that the

costs of undertaking Section 17a reviews would be in excess of the likely

benefits and a review will not be carried out on those services.

Priority Review Areas

9. A number of reviews have been undertaken in recent years in various

forms and contexts and these are deemed as completed. The priority for Council

should be on repurposing those reviews and incorporating any Section 17a

requirements. Other priorities will be set by the expiry or renewal of

significant contracts where staff identify opportunities to explore service

improvements and efficiency gains.

10. Due to

the recent internal reorganisation and LTP processes, several of

Council’s functional activities have been reviewed more recently. It is

therefore proposed that these be re-reviewed in a few years’ time, once

the most recent restructure and LTP process has matured. It is further

proposed that no reviews are undertaken in Q1 and Q2 of the 2018-19 financial

year due to resourcing constraints. Council has forecast a senior accountant as

part of the realignment of the finance team to assist with these reviews.

11. Staff

have undertaken analysis and sought guidance from the Executive team and have

recommended priority review areas (attached) for the sub-committee to provide

feedback on. These have been sorted by priority and are proposed to

begin once the significant LTP process has been completed.

12. The approach in determining a work programme is

to seek out opportunities to add practical value to the services and activities

that the Council provides or undertakes for and on behalf of its community,

including:

12.1. Understanding the nature of and rationale for

services or activities currently provided or undertaken

12.2. Looking at the context (including service

demand) in which these services are and will be delivered, now and into the

future

12.3. Identifying opportunities that might arise for

improving the efficiency or effectiveness of the services or activities,

including opportunities that might arise from a collaborative approach with

other parties

12.4. Assessing those opportunities to see if they

might add value for the Hawke’s Bay community.

13. In addition

staff have reviewed external guidance on best practice approaches to determine

priority review areas for Council. SOLGM’s guidance recommends

using the activities (not groups) disclosed for reporting in the Long Term

Plans as a starting point for defining ‘services’ to be

reviewed. Determination of priority options is based on guidance which is

highlighted further in this section below.

14. External

advice suggests the following principles when considering whether an activity

should be reviewed.

14.1. The

bigger the budget the more efficiency gains are possible

14.2. Capital

intensive services are more likely to generate savings

14.3. The

greater the cost of a review as a percentage of the total cost of service, the

less value in a review

14.4. The

more generic the service the more opportunity for economies of scale or scope

14.5. Services

which are core competencies and have non-commercial objectives should be

retained in house

14.6. There

is value in conducting a review if it could further Council’s strategic

priorities or responds to a demographic trend or future problem

14.7. The

success of many alternative service delivery methods depends on the existence

of a competitive market

14.8. Services

that have been the subject of comprehensive review under other procurement or

legislative processes are less likely to generate new and better ways of doing

things

14.9. A

service that consistently achieves its performance targets is evidence that it

meets customer expectations, and a review is less likely to realise benefits

14.10. If operating costs are

comparable with other suppliers then a review is less likely to realise

efficiency gains

14.11. Council will get the

most “bang for buck” by focusing on services that are important to

citizens and are failing to meet their expectations

14.12. The more elapsed time

since the last review, the greater value in a review

14.13. Service reviews realise

the most benefits when there is certainty around the operating environment in

which the service is delivered

14.14. Reviews undertaken

jointly with relevant councils and service providers will realise the most

value.

15. Where

another Council is planning to review its similar activities, a joint approach

will be investigated to establish whether it is likely to bring cost

efficiencies to the review process.

Summary

16. Staff

will continue to undergo reviews in accordance with 17a requirements in line

with the review proposal sheet. Progress updates and findings from these

reviews will be reported back to this committee every quarter.

Decision Making

Process

17. Staff have assessed the

requirements of the Local Government Act 2002 in relation to this item and have

concluded that, as this report is for information only, the decision making

provisions do not apply.

|

Recommendation

That the Finance Audit & Risk

sub-committee:

1. Receives and notes the “Local Government Act Section 17a Reviews” staff report

2. Agrees the recommended work programme as proposed.

|

Authored by:

|

Melissa des

Landes

Management Accountant

|

Jessica Ellerm

Group Manager Corporate Services

|

Approved by:

|

James Palmer

Chief Executive

|

|

Attachment/s

|

⇩1

|

HBRC 17a

Programme Timeline

|

|

|

|

HBRC

17a Programme Timeline

|

Attachment 1

|

HAWKE’S BAY REGIONAL COUNCIL

Finance

Audit & Risk Sub-committee

Wednesday 06 June 2018

Subject: Resource Management

Information System Implementation Update

Reason for Report

1.

To provide an update on progress with the

implementation of the new Resource Management Information software (IRIS).

Milestones and Progress

2.

The project team and business units have completed

reforecasting and it has been agreed that Consents and Compliance Go Live with

IRIS in November 2018 with Incidents and Enforcements following in February

2019.

3.

Consents user acceptance testing (UAT) is on

track with no significant issues reported. This stage is due for completion on

the 8th June 2018.

4.

Solution planning for Compliance and Water

Information Services has been completed with a view to have data migration and

configuration completed by late July.

Key Assumptions

5.

The revised timelines are dependent on the

successful and timely recruitment of two new permanent roles; Business

Application Specialist – IRIS and GIS Analyst. The assumption was that

these roles would be appointed and commence no later than 1 July 2018 and

should this not occur, the reforecast timelines may be subject to further

delays. One of these roles is approved and in progress and the other is yet to

be approved.

Scope

6.

Although Water Information Services is part of

the IRIS Compliance module, it has been agreed it should be run as a

stand-alone work-stream due to the need for specific council defined fields and

complexity around water consents. This module will run in parallel with

Compliance and will Go Live alongside Consents and Compliance in November.

7.

A functionality log was used to capture

potential feature and functionality additions. These items were prioritised by

the business and will be delivered within an agreed timeframe.

Cost

|

Reason

|

Description

|

Cost

|

|

Fixed-term Contract Extensions

|

Due to the

delay in go live, key fixed-term contracts needed to be extended. In

addition, a new fixed-term contract to assist with WIS is required. The total

cost of this has been offset by a $40k contingency.

|

$60,000

|

|

External Costs

|

Due to the

delay in go live, and additional requirements as a result of further

evaluating WIS, significant additional costs will be incurred in consultancy

from Datacom. This has been largely offset by a $90k contingency.

|

$10,000

|

|

Contingency

|

Due to the

complexity and nature of this project, and given original contingency has

been exhausted (set out above), it is recommended further contingency is

provisioned.

|

$80,000

|

|

|

|

$150,000

|

Revised Timeline

8.

The original Go Live date for Consents and

Compliance was 16th April 2018 followed by Incidents and Enforcements

in September 2018. The revised timeline means that Consents and Compliance

(with WIS) will Go Live in November 2018. Incidents and Enforcements will run

in parallel from September and will Go Live in February 2019.

Decision Making Process

9.

Staff have assessed the requirements of the

Local Government Act 2002 in relation to this item and have concluded that, as

this report is for information only, the decision making provisions do not

apply.

|

Recommendation

That the Finance, Audit & Risk

Sub-committee receives and notes the “Resource Management

Information System Implementation Update” staff report.

|

Authored by: Approved

by:

|

Kahl Olsen

Information and Communications Technology

Manager

|

Jessica

Ellerm

Group

Manager Corporate Services

|

Attachment/s

There are no

attachments for this report.

HAWKE’S BAY REGIONAL

COUNCIL

Finance

Audit & Risk Sub-committee

Wednesday 06 June 2018

Subject: David Benham

Resignation

Reason for Report

1. To formally

advise the resignation of David Benham as independent member of the Finance,

Audit and Risk Sub-committee.

Decision Making

Process

2. Staff have

assessed the requirements of the Local Government Act 2002 in relation to this

item and have concluded that, as this report is for information only, the decision

making provisions do not apply.

|

Recommendations

That the

Finance, Audit and Risk Sub-committee receives and notes the resignation of

David Benham as independent member, effective 6 June 2018.

|

Authored by:

|

Leeanne

Hooper

Governance Manager

|

|

Approved by:

|

Jessica

Ellerm

Group Manager Corporate Services

|

|

Attachment/s

There are no

attachments for this report.

HAWKE’S BAY REGIONAL

COUNCIL

Finance

Audit & Risk Sub-committee

Wednesday 06 June 2018

Subject: June 2018 Update on the

Sub-committee Work Programmes

Reason for Report

1. In order to ensure the sub-committee’s ability to effectively

and efficiently fulfill its role and responsibilities, an overall update on its

work programme is provided following.

|

Task

|

Item

|

Scheduled / Status

|

|

Internal Audits

|

Water Supply/ Wastewater/ Stormwater Management

|

Report to 6 June 2018 FA&R meeting

|

|

Procurement and Purchasing

|

Report to 6 June 2018 FA&R meeting

|

|

2018-19 Schedule of Internal Audits

|

To FA&R 6 June 2018 FA&R meeting

|

|

Risk Assessment & Management

|

Reporting

on risks (6-monthly) affecting Council plus noting changes / improvements /

areas that require attention from last report (3-monthly)

|

2018 FA&R 7 March & 19 September meetings.

Risk management discussions and follow ups now being

documented at each monthly meeting at Exec.

|

|

Insurance

|

Council’s

proposed 2018-19 Insurance programme

|

Aligned with insurance renewal dates each year.

Report to 6 June 2018 FA&R meeting

|

|

Annual Report

|

Discussion

on Audit Management Letter

|

Auditor scheduled to attend December 2019 FA&R

meeting

|

|

Discussion on the major issues (if any) in the audit

report on the Annual Report.

|

Aligned with Audit NZ & legislative requirements

Sept-Nov each year

|

|

Reviews

|

Review

of the Council’s capital structure, taking into account the value of

dividends in supporting Council operations.

|

Phase II report released. Workshop held 9th

May to review Counsellors appetite on options identified.

|

|

Investment Returns Monitoring

|

Update

on progress in obtaining required level of dividend from PONL

|

PONL presented at 14 March C&S meeting. Draft

SOI presented at 30 May 2018 Council meeting.

|

|

Treasury

|

Update

on Treasury function within Council

|

Currently working with PWC to produce a draft

Treasury Policy and updated SIPO to align with Council’s new strategic

direction. Draft policy to be presented at 13 June 2018 C&S meeting.

Plan to present a treasury report quarterly, which

will include analysis of performance of all investments including financial

investments and HBRIC.

|

Decision Making

Process

2. As this report

is for information only and no decision is to be made, the decision making

provisions of the Local Government Act 2002 do not apply.

|

Recommendation

That the Finance, Audit and Risk

Sub-committee receives and notes the “June 2018 Update on Sub-committee

Work Programmes” staff report.

|

Authored by:

|

Jessica

Ellerm

Group Manager Corporate Services

|

|

Approved by:

|

James Palmer

Chief Executive

|

|

Attachment/s

There are no

attachments for this report.

HAWKE’S BAY REGIONAL COUNCIL

Finance

Audit & Risk Sub-committee

Wednesday 06 June 2018

Subject: Proposed 2018-19

Council Insurance Programme

That Council excludes the public

from this section of the meeting, being Agenda Item 14 Proposed 2018-19 Council

Insurance Programme with the general subject of the item to be considered while

the public is excluded; the reasons for passing the resolution and the specific

grounds under Section 48 (1) of the Local Government Official Information and

Meetings Act 1987 for the passing of this resolution being:

|

GENERAL SUBJECT OF THE ITEM TO BE

CONSIDERED

|

REASON FOR PASSING THIS RESOLUTION

|

GROUNDS UNDER SECTION 48(1) FOR THE

PASSING OF THE RESOLUTION

|

|

Proposed 2018-19 Council Insurance Programme

|

7(2)(i) That the public

conduct of this agenda item would be likely to result in the disclosure of

information where the withholding of the information is necessary to enable

the local authority holding the information to carry out, without prejudice

or disadvantage, negotiations (including commercial and industrial

negotiations).

|

The Council is specified, in the First Schedule to this

Act, as a body to which the Act applies.

|

Authored by:

|

Melissa des

Landes

Management Accountant

|

|

Approved by:

|

Jessica

Ellerm

Group Manager Corporate Services

|

|