Meeting of the Finance Audit & Risk Sub-committee

Date: Wednesday 7 March 2018

Time: 9.00am

|

Venue:

|

Council Chamber

Hawke's Bay Regional Council

159 Dalton Street

NAPIER

|

Agenda

Item Subject Page

1. Welcome/Notices/Apologies

2. Conflict

of Interest Declarations

3. Confirmation of

Minutes of the Finance Audit & Risk Sub-committee meeting held on 4

December 2017

4. Follow-ups from

Previous Finance Audit & Risk Sub-committee Meetings 3

Decision Items

5. Six-Monthly Risk

Assessment and Management Update 15

6. Procurement

Internal Audit Scope and Water Management Internal Audit Progress Update 29

Information or Performance Monitoring

7. HBRC Works Group

Update 41

8. Resource

Management Information System Implementation Update 43

9. Local Government

Act Section 17a Reviews 47

10. March 2018 Update on the

Sub-committee Work Programmes 49

HAWKE’S BAY REGIONAL COUNCIL

Finance

Audit & Risk Sub-committee

Wednesday 07 March 2018

SUBJECT: Follow-ups from Previous Finance

Audit & Risk Sub-committee Meetings

Reason for Report

1. In order to track items raised at previous meetings that require

follow-up, a list of outstanding items is prepared for each meeting. All

follow-up items indicate who is responsible for each, when it is expected to be

completed and a brief status comment. Once the items have been completed and

reported to the Committee they will be removed from the list.

Decision

Making Process

2. Council is required to make every decision in

accordance with the Local Government Act 2002 (the Act). Staff have assessed

the in relation to this item and have concluded that as this report is for

information only and no decision is required, the decision making procedures

set out in the Act do not apply.

|

Recommendation

That the Finance, Audit and Risk Sub-committee receives

and notes the report “Follow-ups from Previous Finance Audit and

Risk Sub-committee Meetings”.

|

Authored by:

|

Leeanne

Hooper

Governance Manager

|

|

Approved by:

|

Jessica Ellerm

Group Manager Corporate Services

|

|

Attachment/s

|

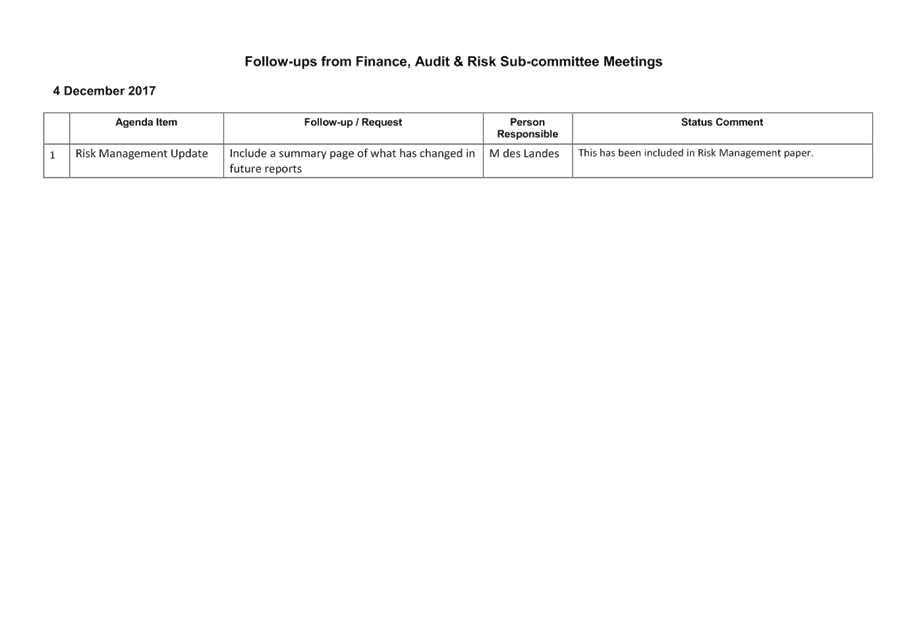

⇩1

|

Follow-ups

from 4 Dec 2017 FA&R meeting

|

|

|

|

Follow-ups

from 4 Dec 2017 FA&R meeting

|

Attachment 1

|

HAWKE’S BAY REGIONAL

COUNCIL

Finance

Audit & Risk Sub-committee

Wednesday 07 March 2018

Subject: Six-Monthly Risk

Assessment and Management Update

Reason

for Report

1. To provide the

Sub-committee with a six monthly review of the risks that Council is exposed to

and the mitigation actions in place to manage Council’s risk profile.

Background

2. The

Sub-committee last considered the risk management report at its meeting held

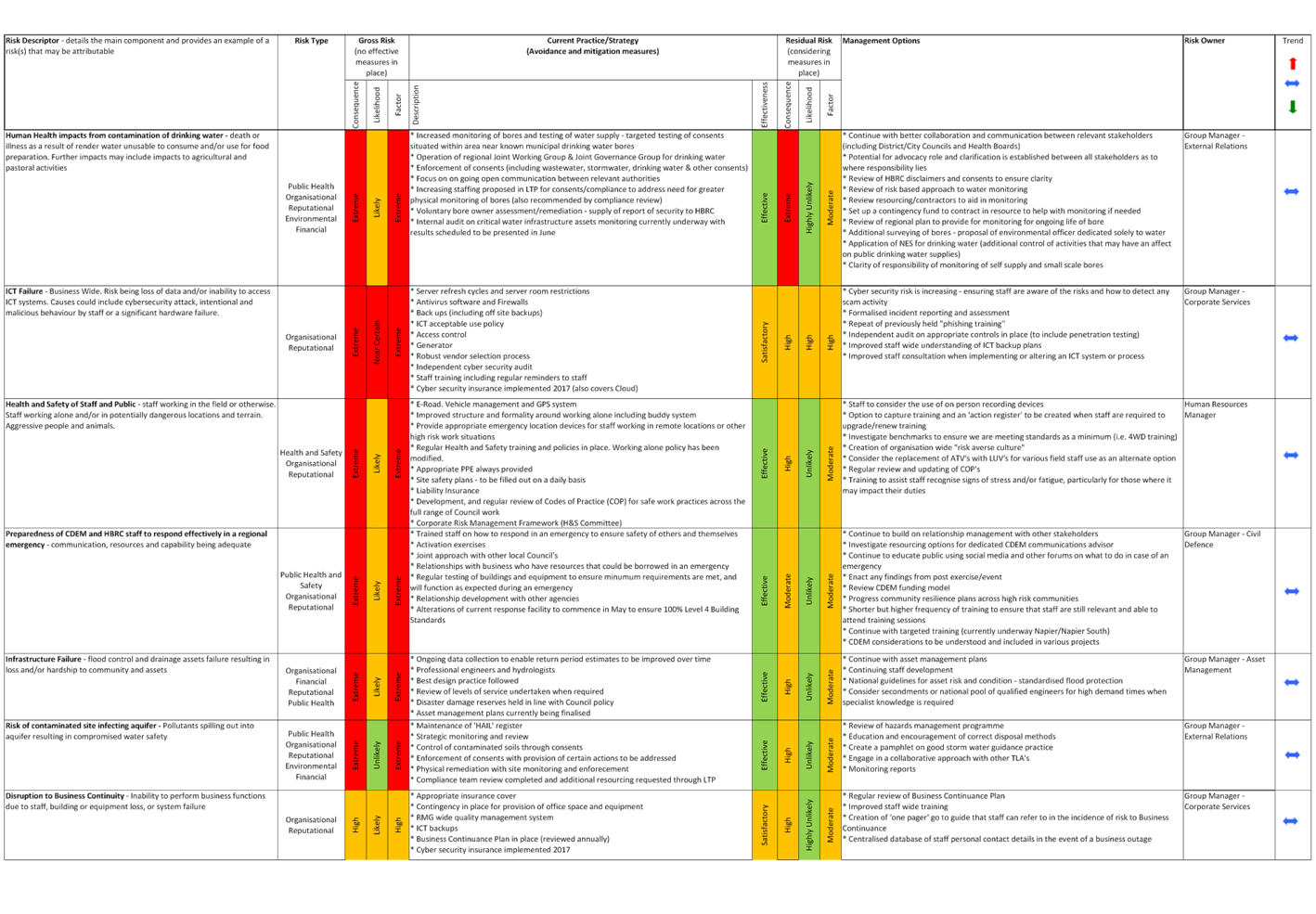

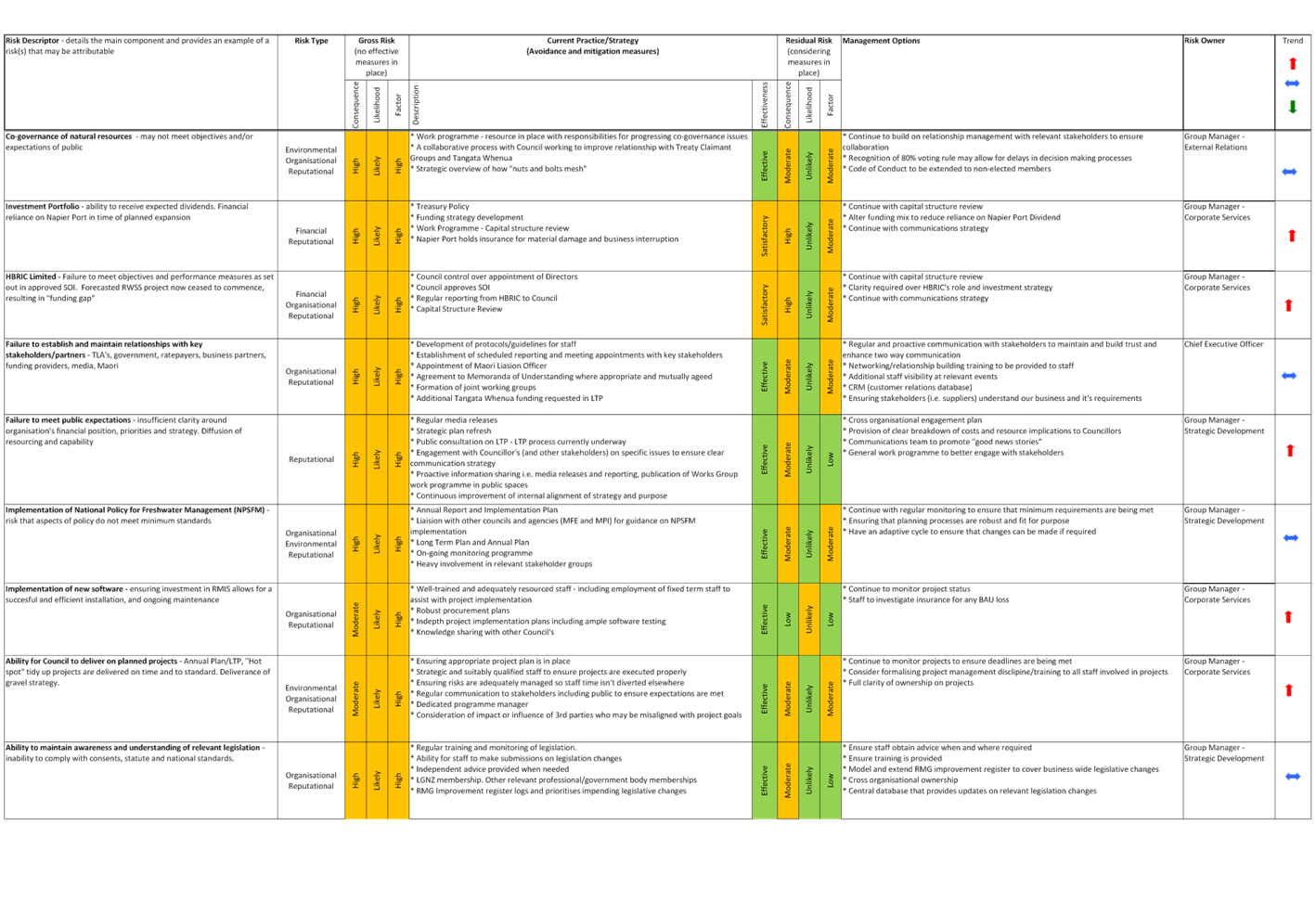

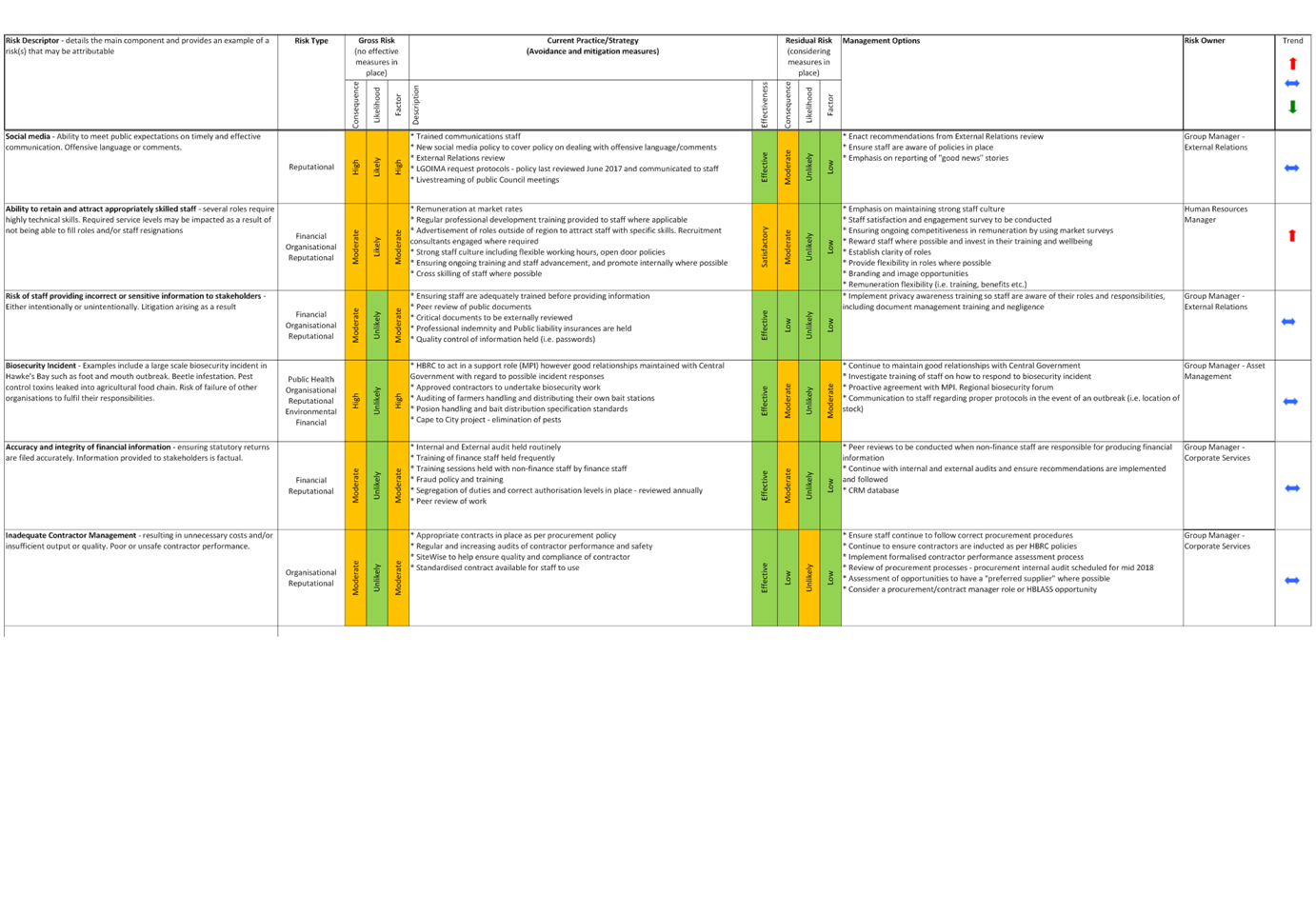

4 December 2017. The updated risk register is attached.

3. Following on

from a series of risk management workshops held in January/February and

executive interrogation of findings, high consequence risks and upwards

trending risks, attached is the latest risk management update for Councillors

review.

4. At the previous

meeting, Councillors requested an update on anything that has

“moved” in the risk register, along with a request for a report on

consideration of project risks (attached).

Key

Changes

5. While not

exhaustive, commentary around most significant changes has been provided below

of any major changes or action points to the risk register for Councillors

attention. Items listed below are in addition to risk management strategies

already reported on previously.

6. All key

strategic level risks now have a dedicated “risk owner” is to

remain accountable for action points and follow ups.

7. Consideration

of education of non ICT staff of ICT risks due to potential high causation factor

as well as consideration of independent audit of our ICT security and backups.

8. Recognition of

Joint Drinking Water Groups is proving effective. Some additional work required

in clarity of responsibility of monitoring small scale/self-supply bores - to

be addressed during upcoming group meetings.

9. Recognition of

stress and fatigue as a Health and Safety issue that may affect staff’s

wellbeing and performance. To be covered by executive during their next

“away day”.

10. Staff have requested

shorter/higher frequency Civil Defence training to ensure the knowledge of

their roles is current in how to respond to an emergency. This is to be

reviewed as part of a Civil Defence training review.

11. Due to the current LTP

process underway, it has been recognised that the failure to meet public

expectations risk should be elevated to high. These are being mitigated through

open and effective communication strategies.

12. Due to the proposal of

several new highly skilled/experience staff, the ability to retain and attract

appropriately skilled staff risk has also been elevated to “high”.

While Council provides good training and is proud of its culture, it also

recognised the ability to attract staff to both Hawke’s Bay and a Council

environment may be a challenge.

13. It has been recognised

that Council’s current contract engagement and monitoring could provide

for extra efficiencies. A procurement audit is scheduled with results to be

available in June whereby Council will review and enact any recommendations from

the findings it deems viable.

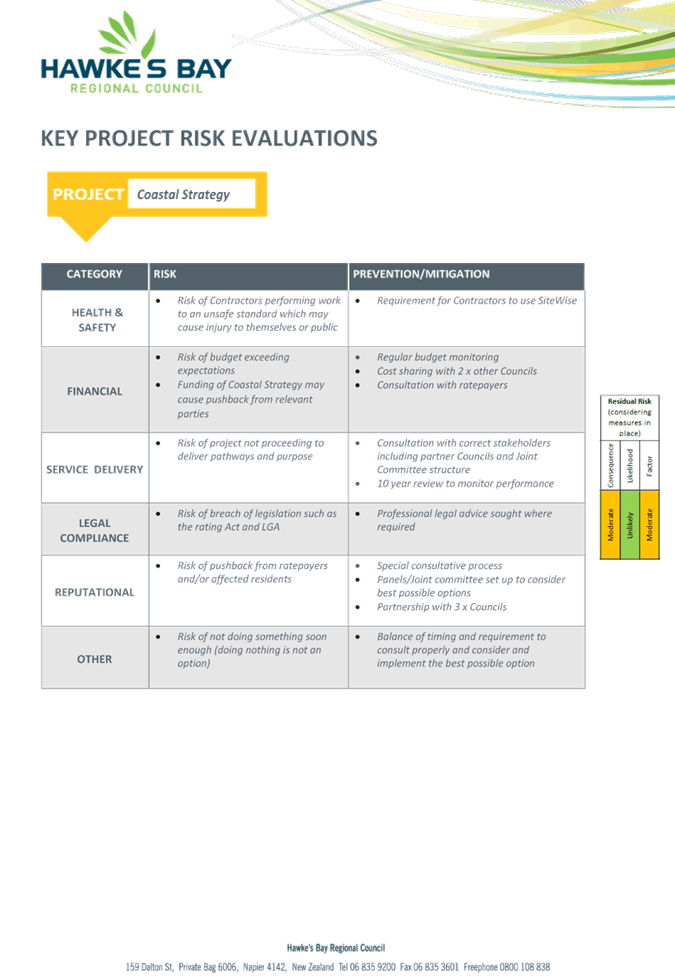

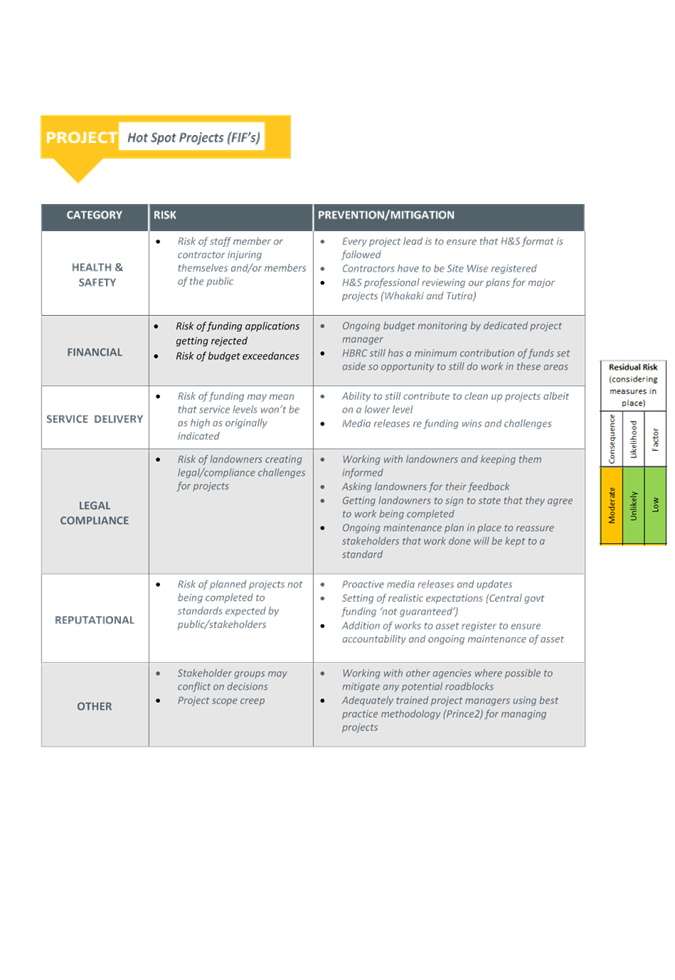

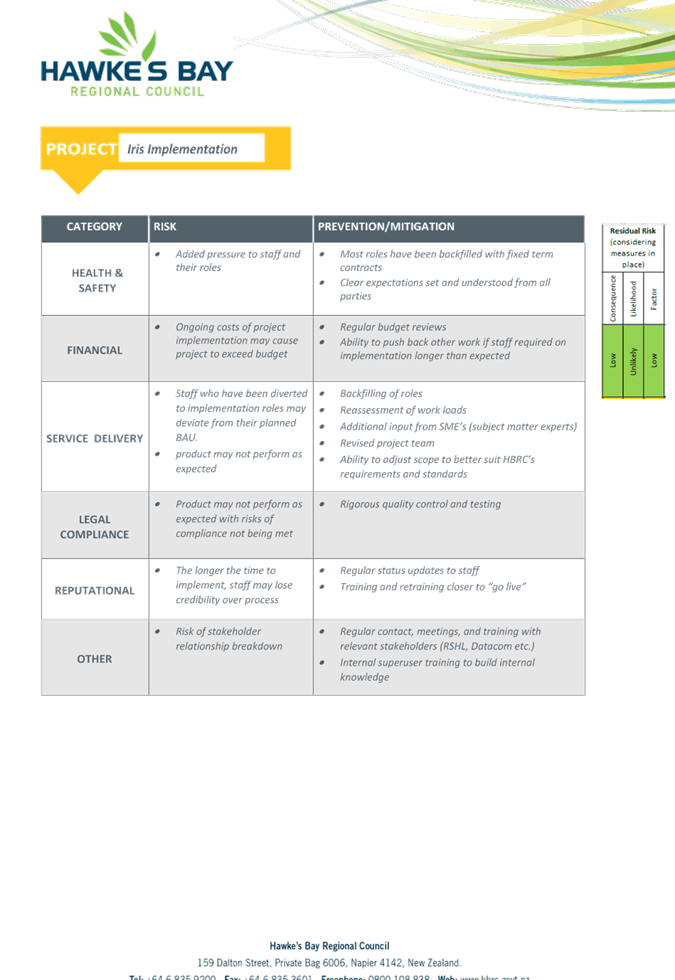

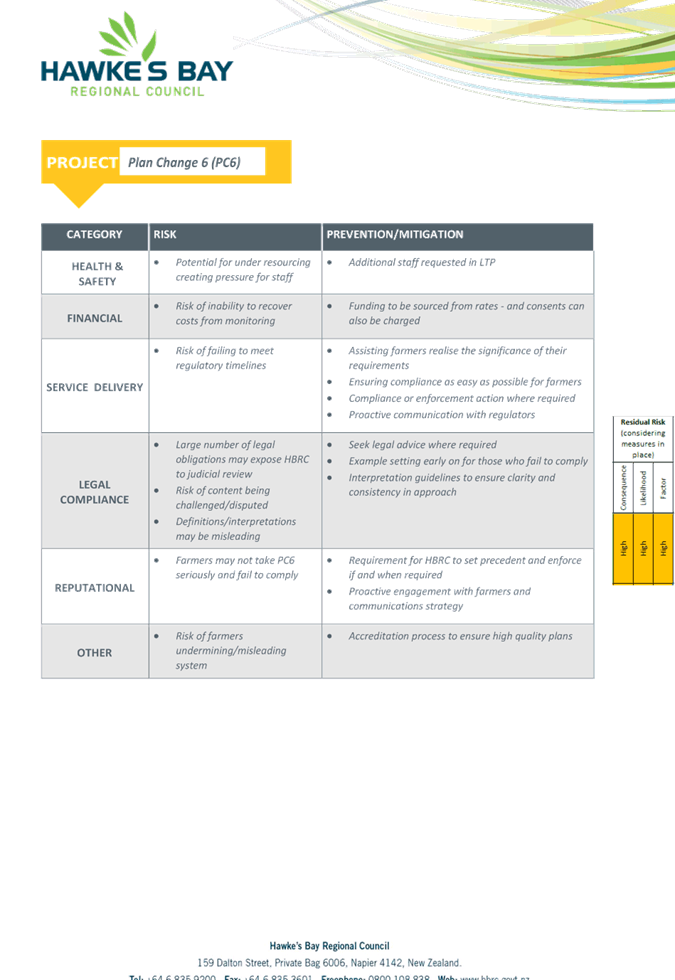

Project Risks

14. During the recently

conducted risk management workshops, specific project risks were added as an

additional element to discussions. Five topical/high risk projects were

identified and discussed along with what potential risks we may face with the

execution of these projects.

15. Projects reported on are

Plan Change 6, TANK, Iris Implementation, Costal Strategy and Hot Spots

(FIF’s). In addition to this, discussions were held as to what

Council is doing to mitigate any risks that may arise as a result of these

projects.

16. It is important to note

that this is in addition to the risk mitigation strategies Council already

conducts as an organisation. Project risk mitigation methods have been listed

as specific to each project and is an additional layer to what is already

recorded in the risk register.

17. Budgeting and planning

regarding an organisational project management system including common

methodologies and a consistent approach to project management has been

initiated. It has been decided that this sits under the Corporate Services

function and there is sufficient budget in the LTP to allow for this.

18. It is intended that

project risks are to be embedded in future risk management discussions and

strategies in the future.

Decision Making

Process

19. Council

is required to make every decision in accordance with the requirements of the

Local Government Act 2002 (the Act). Staff have assessed the requirements

in relation to this item and have concluded:

19.1. The decision

does not significantly alter the service provision or affect a strategic asset.

19.2. The use of

the special consultative procedure is not prescribed by legislation.

19.3. The decision

does not fall within the definition of Council’s policy on significance.

19.4. The persons potentially

affected by this decision are staff or persons in the community that rely on

Council services.

19.5. Options for

Council in regard to this paper are to defer or not consider risks that this

Council is exposed to. This paper adopts the option of Council reviewing

the risk profile.

19.6. The decision

is not inconsistent with an existing policy or plan.

19.7. Given

the nature and significance of the issue to be considered and decided, and also

the persons likely to be affected by, or have an interest in the decisions

made, Council can exercise its discretion and make a decision without

consulting directly with the community or others having an interest in

the decision.

|

Recommendations

1. That the Finance, Audit and Risk Sub-committee:

1.1 Receives and considers the “HBRC Risk Assessment and

Management” staff report.

2. The Finance, Audit and Risk Sub-committee recommends that the

Corporate and Strategic Committee:

2.1. Agrees the decisions to be made are not significant under the

criteria contained in Councils’ adopted Significance and Engagement

Policy, and that Council can exercise its discretion and make decisions on

this issue without conferring directly with the community.

2.2. Confirms the Finance Audit and Risk Sub-committee’s

confidence that the risk assessment processes are appropriate processes to

identify and assess organisational risks.

|

Authored by:

|

Melissa des

Landes

Management Accountant

|

|

Approved by:

|

Jessica

Ellerm

Group Manager Corporate Services

|

|

Attachment/s

|

⇩1

|

HBRC Risk

Register March 2018

|

|

|

|

⇩2

|

March18 Key

HBRC Projects Risk Management

|

|

|

|

HBRC

Risk Register March 2018

|

Attachment 1

|

|

HBRC

Risk Register March 2018

|

Attachment 1

|

|

HBRC

Risk Register March 2018

|

Attachment 1

|

|

March18

Key HBRC Projects Risk Management

|

Attachment 2

|

HAWKE’S BAY REGIONAL COUNCIL

Finance

Audit & Risk Sub-committee

Wednesday 07 March 2018

Subject: Procurement Internal

Audit Scope and Water Management Internal Audit Progress Update

Reason for Report

1. To confirm the

scope for the upcoming Procurement Internal Audit, and to provide the

Sub-committee with an update on the status of the Water Management internal

audit currently under way.

Background

2. At its meeting

on 19 September 2017, the sub-committee agreed to internal audit work programme

for the 2017-18 financial year to include Data Analytics, Water Management, and

Procurement.

3. At its meeting

4 December 2017 the sub-committee received internal audit report on first audit

in agreed work programme, “Data Analytics”. Water Management scope

has been agreed to and work is currently underway, Procurement scope to be

reviewed at this meeting and work will commence following.

Data Analytics

4. The report on

data analytics highlighted that Council has strong transactional processes for

both payroll and accounts payable, however identified some possible

improvements in its procedures.

5. Council has now

applied the changes to controls by training staff on using a consistent

approach when creating new supplier accounts thus reducing the possibility of

entering a duplicate vendor. In addition to this process, staff are now

performing a Companies Office search when setting up a new supplier to ensure

supplier existence. Duplicate vendors have also been minimised by blocking any

current duplicate suppliers. Staff have implemented an additional step of

searching by IRD number before entering new suppliers to reduce the risk of multiple

vendors being created in the future.

6. Another gap

identified was a handful of invoices paid twice (albeit of minimal value) which

was caused by a large volume of invoices being issued to staff. Council has

worked with suppliers to ensure credits/refunds of these payments have been

issued. Council has also negotiated with our catering suppliers to provide us

with one weekly invoice, as opposed to several each week. This hasn’t

reduced payment frequency to these suppliers, however has reduced both time and

paperwork for both parties, along with reduced risk of duplication of

transactions.

Water Management

7. At its meeting

on 4 December, the sub-committee agreed to “water management”

internal audit scoping document. This assignment was originally intended to

proceed immediately, however after this document was provided to Corporate

& Strategic Committee 11 December, there were concerns raised around the

breadth of the assignment.

8. It was agreed

to refine the scope to cover local authority consent holders, and water sources

that specifically affect the health and safety of the community. This scope was

refined and presented to Council 31 January 2018, whereby the scope was agreed

to by resolution. The internal audit fieldwork commenced immediately following.

9. The Water

Management internal audit was originally scheduled to be presented to this

sub-committee meeting, however due to alterations in the scope causing a delay

of 8 weeks, this report will now be pushed out to the following sub-committee

meeting scheduled for 6 June 2018.

Procurement

10. At its meeting held 19

September, the subcommittee agreed to its work programme for the 2017-18

financial year, the final audit for this period being procurement. A scoping

document is attached for the sub-committees review, it is noted that the scope

has been extended to include a review of payment of “living wage”

to contractors.

11. Following resolution of

the Procurement Scoping document, fieldwork is scheduled to commence

immediately with findings to be presented at 6 June 2018 sub-committee meeting.

2018-19 Internal Audit Programme

12. At its meeting scheduled

for 6 June, the sub-committee will receive a proposed work programme for the

2018-19 financial year, which will again consist of three separate audits

spaced out over the financial year.

13. It is intended that

relevant Group Manager is to review any future scoping documents prior to their

presentation to the Finance, Audit and Risk Sub-committee to allow for

specialist input. This will ensure that scoping documents are fit for

Council’s purpose and operating environment, and will ensure efficiency

in the process in future.

14. It is also planned for

Council to speak with other HB LASS Council’s regarding their own

internal work programme and maximise on information sharing opportunities where

possible.

Decision Making

Process

15. Council

is required to make every decision in accordance with the requirements of the

Local Government Act 2002 (the Act). Staff have assessed the requirements in

relation to this item and have concluded:

15.1. The decision

does not significantly alter the service provision or affect a strategic asset.

15.2. The use of

the special consultative procedure is not prescribed by legislation.

15.3. The decision

does not fall within the definition of Council’s policy on significance.

15.4. The decision

is not inconsistent with an existing policy or plan.

15.5. Given

the nature and significance of the issue to be considered and decided, and also

the persons likely to be affected by, or have an interest in the decisions

made, Council can exercise its discretion and make a decision without

consulting directly with the community or others having an interest in

the decision.

|

Recommendations

1. That the Finance, Audit and Risk Sub-committee receives and notes

the “Procurement Internal Audit Scope and Water Management Internal

Audit Progress Update” staff report.

2. The Finance, Audit and Risk recommends that the Corporate and

Strategic Committee:

2.1. Agrees that the decisions to be made are not significant under the

criteria contained in Council’s adopted Significance and Engagement

Policy, and that the Committee can exercise its discretion and make decisions

on this issue without conferring directly with the community and persons

likely to be affected by or to have an interest in the decision.

2.2. Approves the scope for the Procurement internal audit, including

agreed amendments, and the initiation of the Audit.

|

Authored by:

|

Melissa des

Landes

Management Accountant

|

|

Approved by:

|

Jessica

Ellerm

Group Manager Corporate Services

|

|

Attachment/s

|

⇩1

|

Procurement

and Purchasing Audit scope

|

|

|

|

Procurement

and Purchasing Audit scope

|

Attachment 1

|

HAWKE’S BAY REGIONAL COUNCIL

Finance

Audit & Risk Sub-committee

Wednesday 07 March 2018

Subject: HBRC Works Group Update

Reason for Report

1. To provide the sub-committee with an update on the overall financial

performance and other areas of interest of Council’s Works Group. It

is intended that a regular, six monthly or annual update will be provided to

the Sub-committee on financials and work programme highlights for the Group.

2. Hamish Fraser (Works Group Manager) and Kathy Hughes (Office

Administrator) will attend the meeting to provide a presentation.

Background

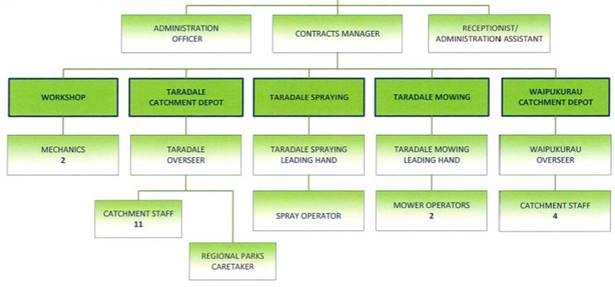

3. The Works Group sits in the organisational structure under the Asset

Management Group of Activities, and is structured as follows.

Decision Making

Process

4. Staff have

assessed the requirements of the Local Government Act 2002 in relation to this

item and have concluded that, as this report is for information only, the

decision making provisions do not apply.

|

Recommendation

That the Finance, Audit and Risk

Sub-committee receives and notes the “HBRC Works Group Update”

staff report and presentation.

|

Authored by:

|

Melissa des

Landes

Management Accountant

|

|

Approved by:

|

Jessica

Ellerm

Group Manager Corporate Services

|

|

Attachment/s

There are no

attachments for this report.

HAWKE’S BAY REGIONAL

COUNCIL

Finance

Audit & Risk Sub-committee

Wednesday 07 March 2018

Subject: Resource Management

Information System Implementation Update

Reason for Report

1. To provide an update on progress with the

implementation of the new Resource Management Information System software.

Milestones and

Progress

2. Good progress has been made with key milestones

resulting in the successful delivery of:

2.1. Infrastructure and Platforms; and

2.2. Solution Planning and Configuration for the core

Consents Business functions.

3. As a result of a 3-month check-point review, it

was identified that there was significantly more complexity around some key

project tasks than initially anticipated resulting in forecast timelines and

delivery targets being unrealistic and forecast resource requirements being

insufficient.

4. Also, as a result of the 3-month check-point

review, it was identified that a number of project tasks, namely data mapping

and data migration, had not been performed adequately due in part to resource

constraints, the readiness of data and an unsatisfactory engagement between the

ICT Team and the Business.

5. It was identified that there had been a lack of

continuity in resource and engagement of senior stakeholders since the

procurement phase of the project resulting in a misalignment between the ICT

Team and the Business and misunderstandings about exactly what the solution

would, and wouldn’t, achieve.

6. These finding resulted in a number of corrective

actions which have largely been executed, including:

6.1. Refinement of the Project Management Structure

6.2. Implementation of a system to plan, monitor and

manage the project lifecycle

6.3. Introduction of an agile methodology for project

phases and tasks

6.4. Strong focus on engagement between the ICT Team

and the Business

6.5. Increased buy-in, and participation in

decision-making, by the Senior Stakeholders in the Business

6.6. Engagement of a fixed-term resource exclusively

dedicated to data quality and cleansing.

7. With corrective actions in place, the wider

project team (ICT Team and the Business) are now able to accurately forecast

resource requirements, timeframes and have agreed definition of the

functionality of the solution including the Critical Success Factors that will

measure and confirm project success.

8. The result of reforecasting the resource

requirements and delivery targets has tentatively rescheduled the delivery of

the solution to November 2018, this is 6 months later than we initially

expected to deliver Consents and Compliance functionality and 2 months later

than initially intended to deliver Incidents and Enforcements functionality. It

is worth noting that this is to achieve baseline functionality or what is

referred to as a Minimum Viable Product (MVP).

9. This delay has no adverse impact on how the Consents and Compliance

Teams perform their duties or deliver core services. The rescheduling and delay,

has been approved by senior Stakeholders across the business and has been

collectively devised to ensure that timeframes and workloads are realistic,

that business risks are minimal, and that the delivery of core services are not

affected.

10. A primary reason for this significant delay in

Consents and Compliance functionality is that, as engagement between the ICT

Team and the Business increased, it was identified that a significant oversight

had been made in regard to the required functionality of the Compliance

function. Specifically, this oversight was that of the Water Information

Services (WIS) function. Although this is typically a Compliance function,

within HBRC it is not performed by the Compliance Team but rather the Client

Services Team and was therefore not well represented nor scoped during solution

planning workshops.

11. The oversight of WIS functionality has

contributed to approximately 6-8 weeks of the 6 month delay. It has directly,

and indirectly, incurred an additional $55k external cost due to requiring a

6-month part-time fixed-term resource to assist the Client Services Team and

also an additional 6 month fixed-term resource to implement the Incidents and

Enforcements module due to ICT staff being repurposed to focus on WIS activities.

12. Also, it was identified that although the

functionality of the solution that would be delivered would be ‘fit for

purpose’ and satisfy core requirements as an MVP, it may not be fully

maximising the investment HBRC are making. Therefore, a list of potential

feature and functionality additions is being generated by the Business that

will be evaluated for feasibility. If feasible, these can either be included

within the scope of the current project (resource and costs permitting) or

earmarked for incremental release post project. Examples of these so far

include a Surface Water Allocation Calculator as used by Waikato Regional

Council or integration with external services such as the Companies Register or

NZ Post postal addresses to improve efficiencies and increase data quality.

13. The project team will spend the next two months

evaluating the potential feature and functionality additions with a view to

present a revised Scope, Cost and Timeframes for the project at the next

Finance, Audit and Risk Sub-committee meeting on 6 June 2018. Depending on the

extent of feasible feature and functionality additions, there could be an

additional, parallel and/or subsequent project to deliver these so there

isn’t undue delay in the core solution delivery.

14. It

is worth noting that regardless of the delays, the project is now considered in

very good health, with a very high level of engagement and alignment between

the ICT Team and the Business and an extremely robust and professional

methodology and approach in place.

Finances and Resources

15. At this stage, with all of the above taken into

consideration, to achieve a MVP will take approximately 2 months longer overall

than initially forecast and could incur up to $180,000 in external costs

(combination of additional Time and Materials from Datacom and resourcing via

fixed-term contracts). A summary of where these costs are likely to be incurred

is set out in the table below, and will be taken into consideration in the

March reforecast for the full year to 30 June 18.

|

Reason

|

Description

|

Cost

|

|

Data Quality and Cleansing Resource

|

Data in existing systems was not

suitable for data migration and required dedicated ICT resource to cleanse

the data on behalf of the business unit.

|

$65,000

|

|

WIS Resourcing

|

A key function of Compliance is WIS, due

to this being delivered by a team outside Compliance, it was overlooked and

not scoped during Compliance Solution Planning Workshops and requires

additional resource in the Client Services Team to ensure the solution is fit

for purpose.

|

$15,000

|

|

Incidents and Enforcements Resourcing

|

The ICT Team has inadequate resourcing

levels to perform the solution planning, configuration and testing due to ICT

resource being repurposed to focus on WIS.

|

$40,000

|

|

Additional Vendor Costs

|

Due to the change in functional

requirements (WIS) and extended duration of the project, significant addition

costs will be incurred as a result.

|

$60,000

|

16. Significant and unplanned time has been spent on

the project by internal staff although this has no material impact on the

balance sheet.

17. The

increased cost will have minimal impact on the 2017-18 financial year given the

delay will require the carry-forward of existing funding and the expenses will

be capitalized and depreciated over a 10-year period.

18. Further resourcing and funding may be required as a result

of the evaluation of the potential feature and functionality additions and

these will be tabled for consideration at the next Finance, Audit and Risk

Subcommittee Meeting on 6 June 2018.

Decision Making

Process

19. Staff have assessed the

requirements of the Local Government Act 2002 in relation to this item and have

concluded that, as this report is for information only, the decision making

provisions do not apply.

|

Recommendation

That the Finance, Audit & Risk

Sub-committee receives and notes the “Resource Management Information

System Implementation Update” report.

|

Authored by:

|

Kahl Olsen

Information and Communications Technology

Manager

|

|

Approved by:

|

Jessica

Ellerm

Group Manager Corporate Services

|

|

Attachment/s

There are no

attachments for this report.

HAWKE’S BAY REGIONAL

COUNCIL

Finance

Audit & Risk Sub-committee

Wednesday 07 March 2018

Subject: Local Government Act

Section 17a Reviews

Reason for Report

1. To provide an update on progress with s17a Activities Reviews. It

has been agreed that s17a would be a standing item in the Finance, Audit &

Risk sub-committee agenda.

Background

2. At its meeting held 11 December 2017 the Corporate and Strategic

Committee received a paper which provided information behind s17a Activity

Review requirements as required under the Local Government Act (2002).

3. The paper advised that Council has been actively reviewing various

aspects of the organisation’s efficiency through various functional reviews

that have taken place in the current financial year. The paper also proposed

that staff report back to this current Finance, Audit & Risk sub-committee

meeting with a formal proposal for further work programme for discussion.

4. Due to capacity constraints as a result of LTP requirements, staff

have been unable to complete this process in time for this meeting. It is

proposed that staff report back to 6 June Finance, Audit & Risk

sub-committee meeting with a formal proposal for a work programme.

Decision Making

Process

5. Staff have

assessed the requirements of the Local Government Act 2002 in relation to this

item and have concluded that, as this report is for information only, the

decision making provisions do not apply.

|

Recommendation

1. That the Finance Audit & Risk sub-committee receives the “Local Government Act Section 17a Reviews” report.

|

Authored by:

|

Melissa des

Landes

Management Accountant

|

|

Approved by:

|

Jessica

Ellerm

Group Manager Corporate Services

|

|

Attachment/s

There are no

attachments for this report.

HAWKE’S BAY REGIONAL

COUNCIL

Finance

Audit & Risk Sub-committee

Wednesday 07 March 2018

Subject: March 2018 Update on

the Sub-committee Work Programmes

Reason for Report

1. In order to ensure the sub-committee’s ability to effectively and

efficiently fulfill its role and responsibilities, an overall update on its

work programme is provided following.

|

Task

|

Item

|

Scheduled / Status

|

|

Internal Audits

|

Water

Supply/ Wastewater/ Stormwater Management

|

Report to 6

June 2018 FA&R meeting

|

|

Procurement

and Purchasing

|

Report to 6

June 2018 FA&R meeting

|

|

2018-19

Schedule of Internal Audits

|

To FA&R

6 June 2018 FA&R meeting

|

|

Risk Assessment & Management

|

Reporting on risks

(6-monthly) affecting Council plus noting changes / improvements / areas that

require attention from last report (3-monthly)

|

2018

FA&R 7 March & 19 September meetings

|

|

Insurance

|

Council’s

proposed 2018-19 Insurance programme

|

Aligned with

insurance renewal dates each year. Report to 6 June 2018 FA&R meeting

|

|

Annual Report

|

Discussion on Audit

Management Letter

|

Auditor

scheduled to attend December 2017 FA&R meeting

|

|

Discussion

on the major issues (if any) in the audit report on the Annual Report.

|

Aligned with

Audit NZ & legislative requirements Sept-Nov each year

|

|

Reviews

|

Review of the

Council’s capital structure, taking into account the value of dividends

in supporting Council operations.

|

Ongoing work

forming part of LTP process including consultation. Statement of Expectation

paper to be presented to 14 March C&S meeting.

|

|

Investment Returns Monitoring

|

Update on progress in

obtaining required level of dividend from PONL

|

PONL to

present to 14 March C&S meeting

|

Decision Making Process

2. As this report

is for information only and no decision is to be made, the decision making

provisions of the Local Government Act 2002 do not apply.

|

Recommendation

1. That the Finance, Audit and Risk

Sub-committee receives and notes the “March 2018 Update on

Sub-committee Work Programmes” staff report.

|

Authored by: Approved

by:

|

Melissa des

Landes

Management Accountant

|

Jessica Ellerm

Group

Manager Corporate Services

|

Attachment/s

There are no

attachments for this report.