Meeting of the Finance Audit & Risk Sub-committee

Date: Tuesday 19 September 2017

Time: 10.00am

|

Venue:

|

Council Chamber

Hawke's Bay Regional Council

159 Dalton Street

NAPIER

|

Agenda

Item Subject Page

1. Welcome/Notices/Apologies

2. Conflict

of Interest Declarations

3. Confirmation of

Minutes of the Finance Audit & Risk Sub-committee held on 10 May 2017

4. Follow-ups from

Previous Finance Audit & Risk Sub-committee Meetings 3

Decision Items

5. 10.30am

Introduction to the Internal Audit Service Provider 7

Information or Performance Monitoring

6. Internal Audit

Report - Event Response Review 33

7. Resource

Management Information System Implementation Update 59

8. 11.00am 2016-17

Annual Report - Audit NZ Discussions 65

9. September 2017

Update on the Sub-committee Work Programmes 89

Decision Items (Public Excluded)

10. Risk Assessment and Management 91

HAWKE’S BAY REGIONAL COUNCIL

Finance

Audit & Risk Sub-committee

Tuesday 19 September 2017

SUBJECT: Follow-ups from Previous Finance

Audit & Risk Sub-committee Meetings

Reason for Report

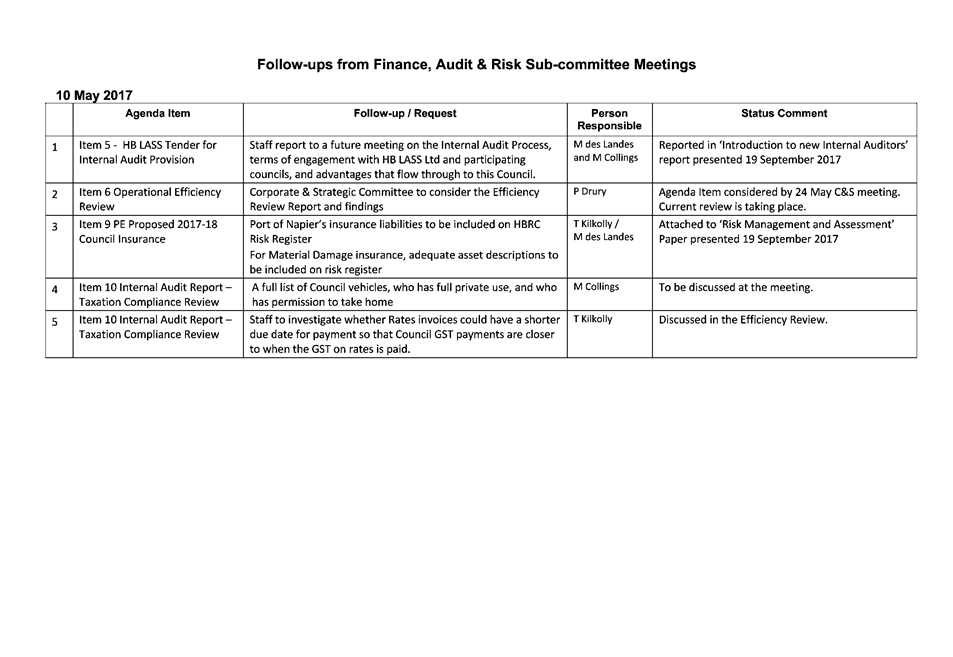

1. In order to track items raised at previous meetings that require

follow-up, a list of outstanding items is prepared for each meeting. All

follow-up items indicate who is responsible for each, when it is expected to be

completed and a brief status comment. Once the items have been completed and

reported to the Committee they will be removed from the list.

Decision

Making Process

2. Council is required to make every decision in

accordance with the Local Government Act 2002 (the Act). Staff have assessed

the in relation to this item and have concluded that as this report is for

information only and no decision is required, the decision making procedures set

out in the Act do not apply.

|

Recommendation

That the Finance, Audit and Risk Sub-committee receives

and notes the report “Follow-ups from Previous Finance Audit and

Risk Sub-committee Meetings”.

|

Authored by:

|

Melissa des

Landes

Management Accountant

|

|

Approved by:

|

Jessica

Ellerm

Group Manager

Corporate Services

|

|

Attachment/s

|

⇩1

|

Follow-ups

from Previous Finance, Audit & Risk Sub-committee Meetings

|

|

|

|

Follow-ups

from Previous Finance, Audit & Risk Sub-committee Meetings

|

Attachment 1

|

HAWKE’S BAY REGIONAL COUNCIL

Finance

Audit & Risk Sub-committee

Tuesday 19 September 2017

Subject: Introduction to the

Internal Audit Service Provider

Reason for Report

1. To introduce

the Sub-committee to the successful Internal Audit service provider and propose

an internal audit programme for the current financial year.

Background

2. At its meeting

on 10 May, the Sub-committee was provided an update on the combined HBLASS

Councils request for proposal (RFP) for internal audit services process, with

shortlisted suppliers undergoing final evaluation at that time.

3. The internal

audit RFP process concluded in June with the successful tenderer being Crowe

Horwath. Representatives in attendance are Phil Sinclair, Engagement Partner,

and Jessica Cranswick, Senior Manager & Account Manager.

4. Crowe Horwath

was awarded the highest scoring tender in unanimous agreement with all HBLASS

Council representatives. This process assessed both price and non-price

information. Non price-information included capability, capacity, approach and

methodology, and value add.

5. The contract

for services has been executed by both parties, including signing by the

Hawke’s Bay Regional Council, Chief Executive as noted as having

delegation to enter such an agreement at the Sub-committee meeting 10 May.

6. The contract

has been signed as agreed for a three year period, with a possibility of a

two-year extension. The contract is valued at $30,000 + GST per annum, which is

in line with Council budget provisions.

Advantages of HB Lass Approach

7. As requested at

the previous subcommittee meeting, advantages of the combined HBLASS approach

to Internal Audit Services are explained below.

8. Councils

previously had different providers of internal audit and the development of

these audits were at varying levels of sophistication and delivery. Endorsement

of the HBLASS approach was received at the 20 September 2016 sub-committee

meeting. Merits determined at this meeting of a combined approach included:

8.1. Councils

would have the same provider

8.2. There would

be a sharing of knowledge between councils on internal audit requirements and

delivery

8.3. There would

be economies of scale achieved in both approach and learnings, which can be

used in each subsequent audit in the participating councils

8.4. Improved

access to skills, specifically in the specialist area audits, i.e. non-traditional

financial audits.

9. A consistent

service delivery team would be able to identify learning opportunities for

sharing across the Councils and provide a mechanism for doing this. A combined

approach will enable informed decisions to be made with respect to whether

review activity should be duplicated or rather findings/recommendations be

shared across the Councils (subject to confidentiality/privacy issues being

cleared). Where an element of duplication existed in the performance of

assignments across the Councils there may be opportunities to realise

performance efficiencies.

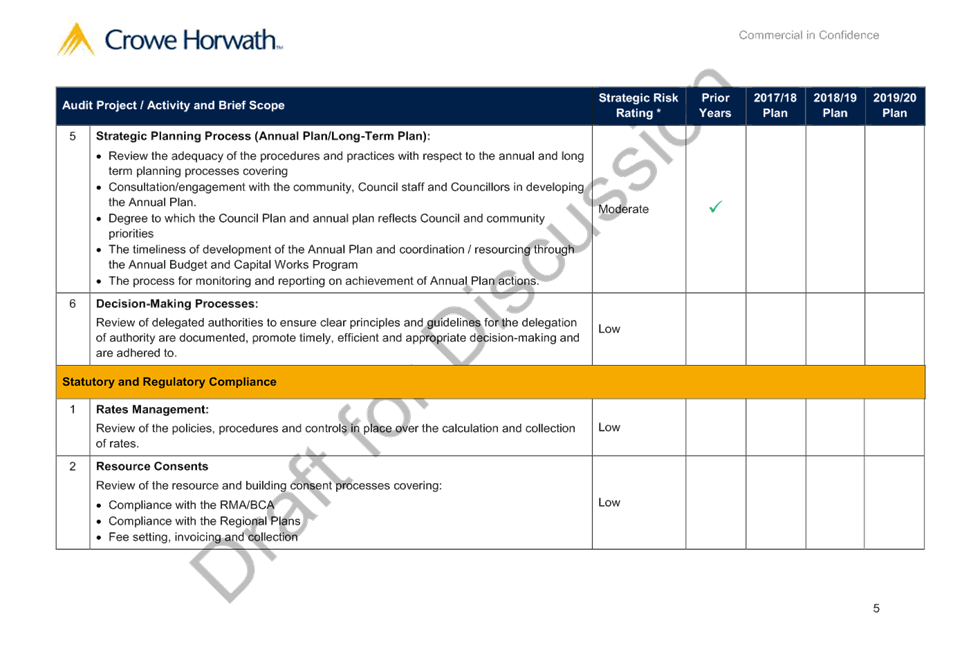

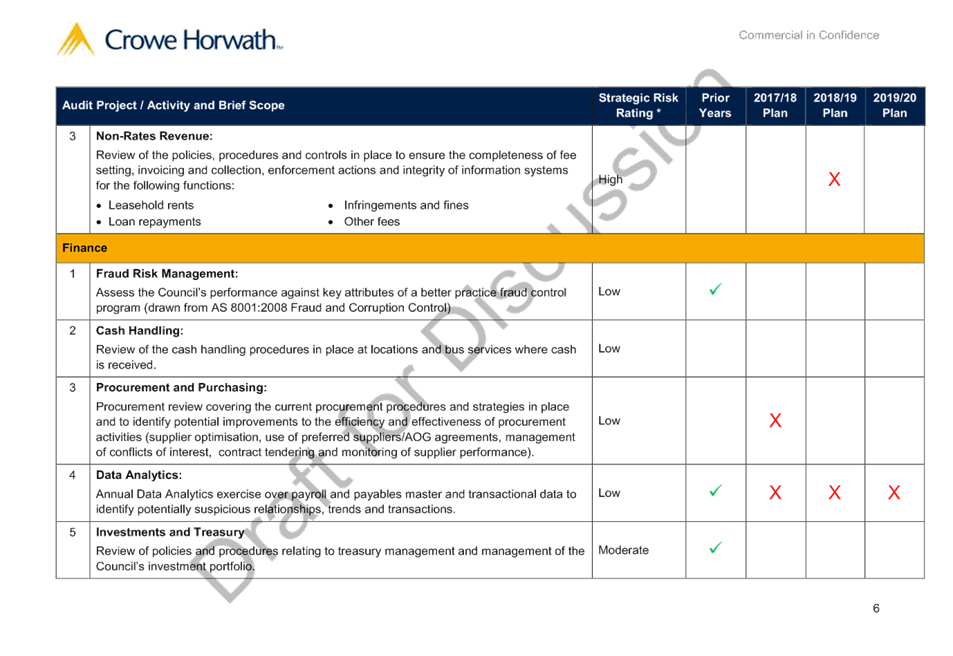

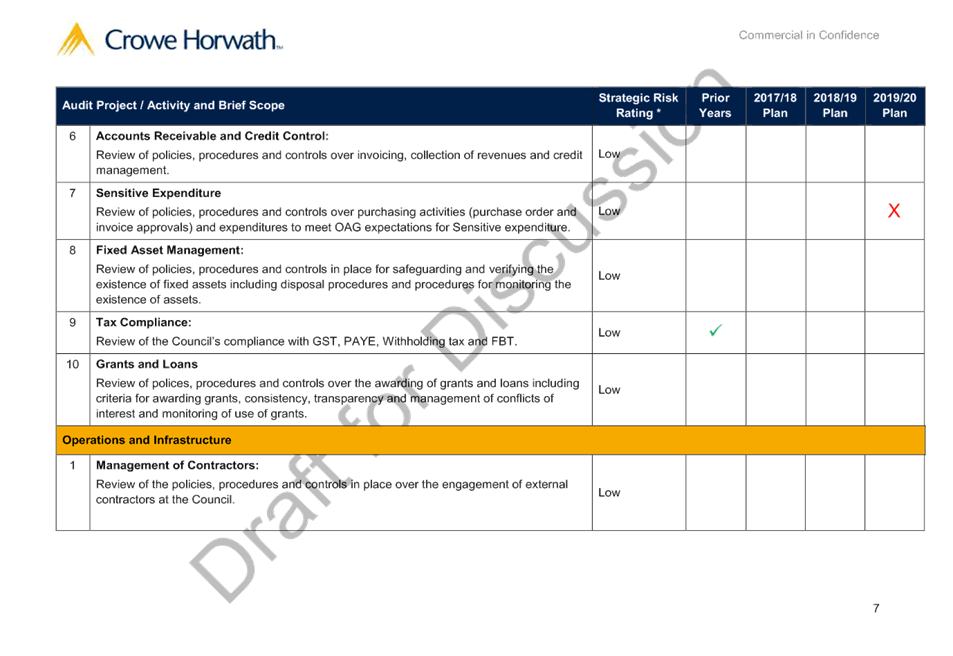

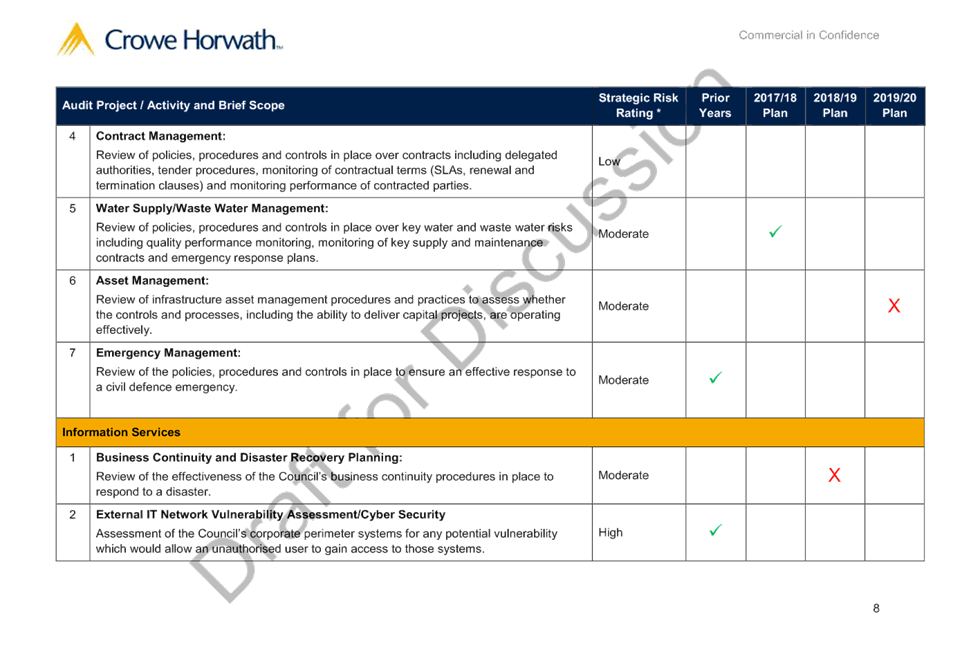

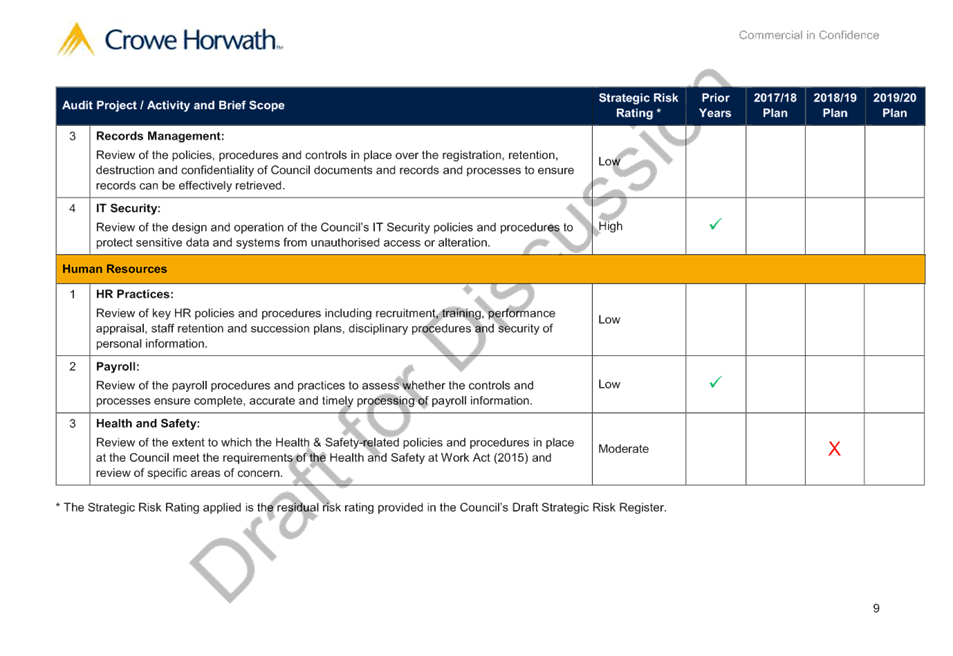

Proposed Internal Audit Programme

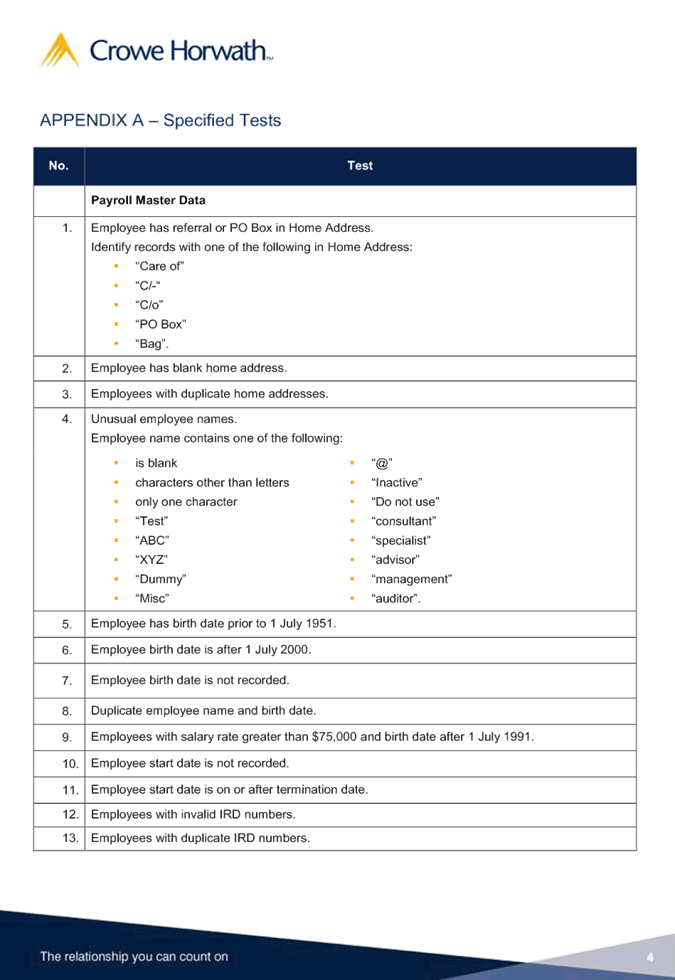

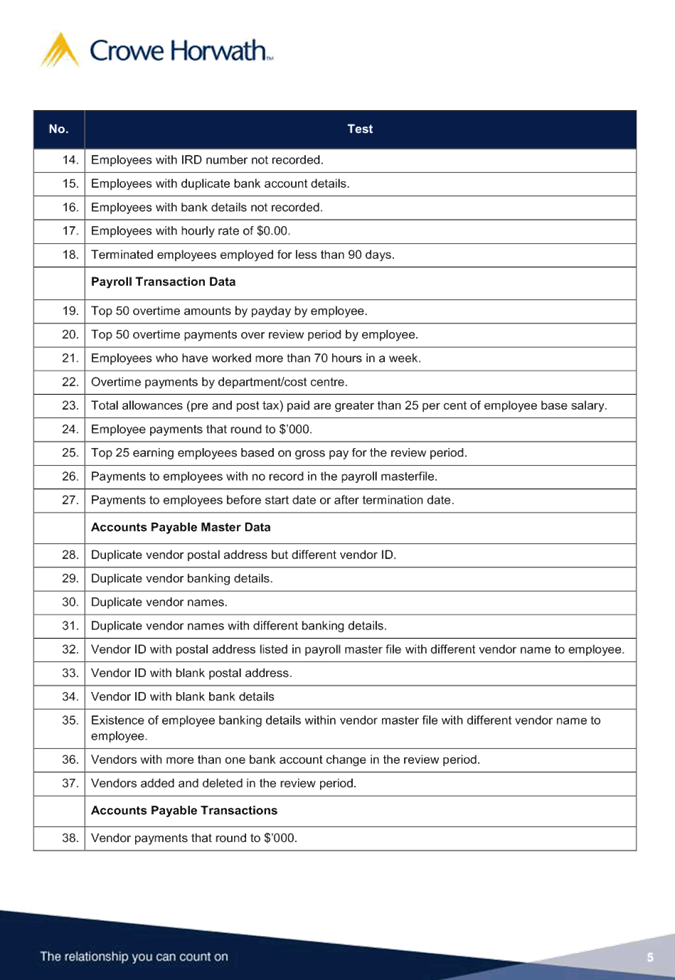

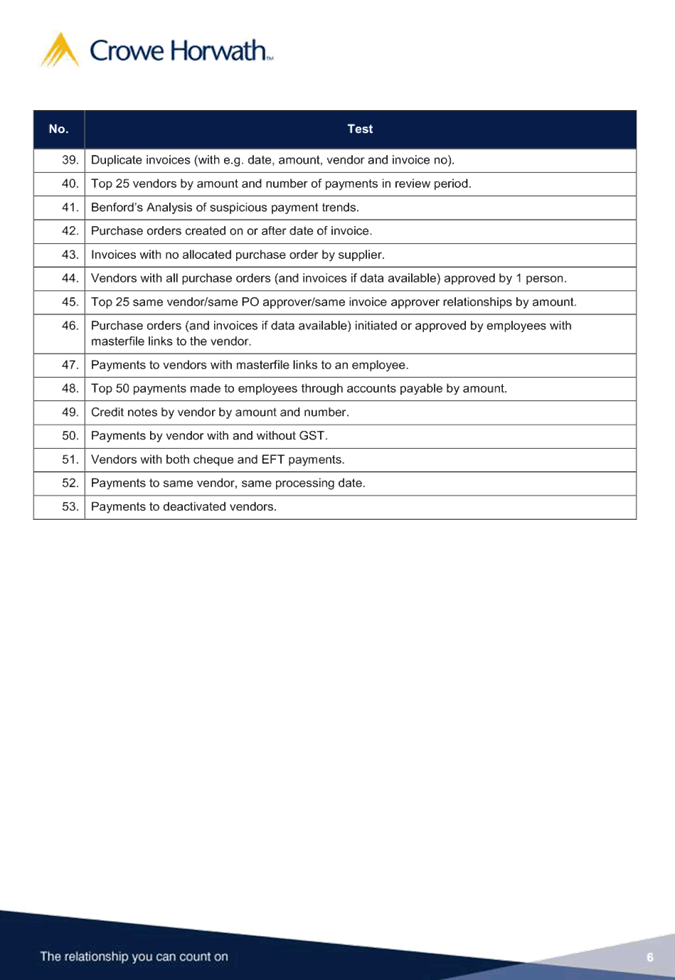

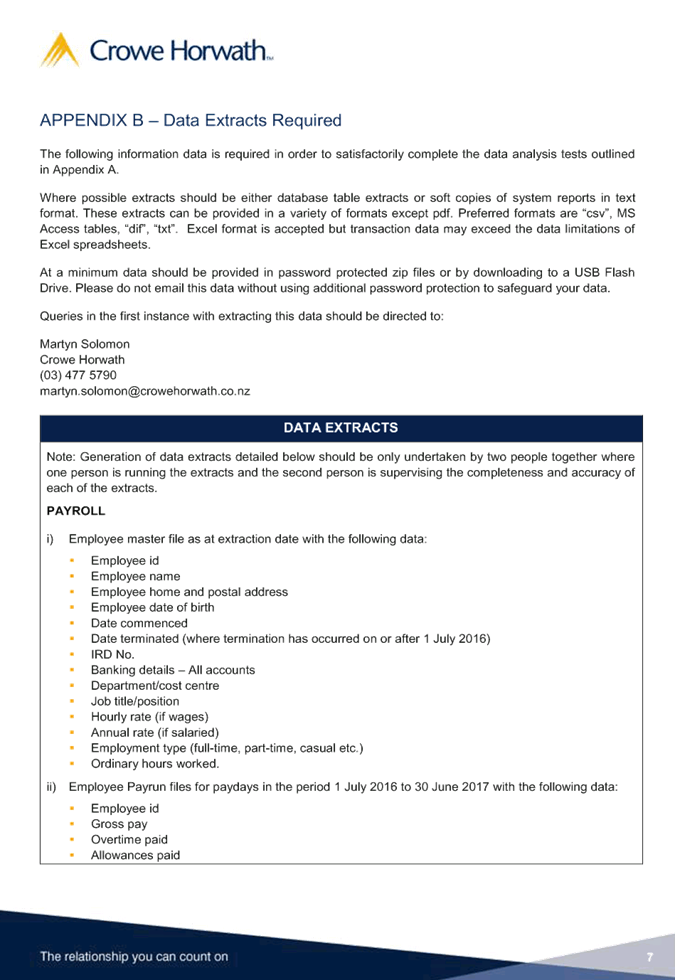

10. In consultation with Crowe

Horwath and internal staff, based on current risk register, emerging issues,

and areas of focus, the areas of internal audit proposed for the current

financial year are:

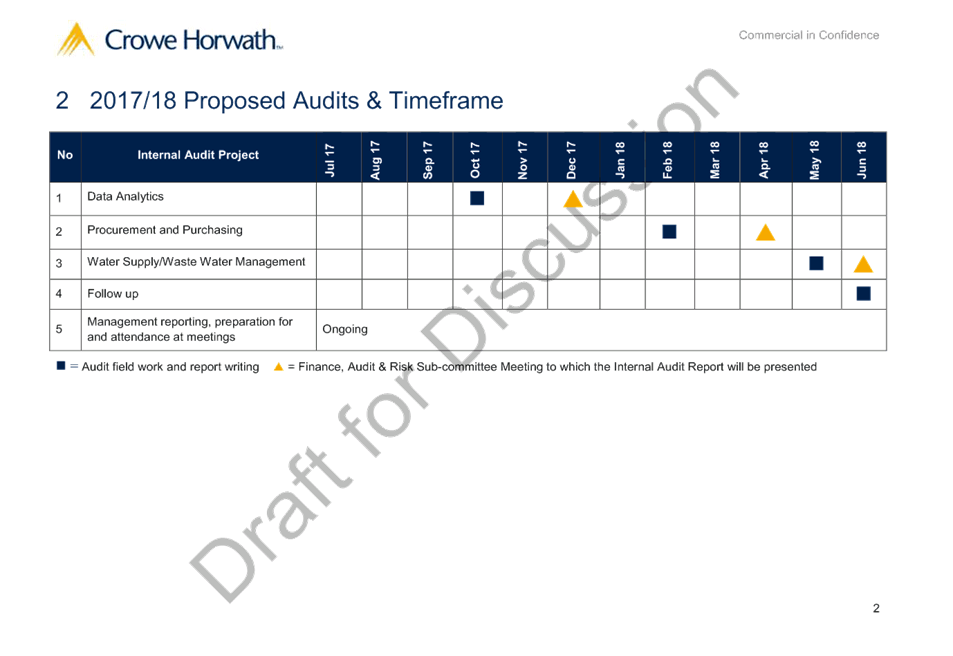

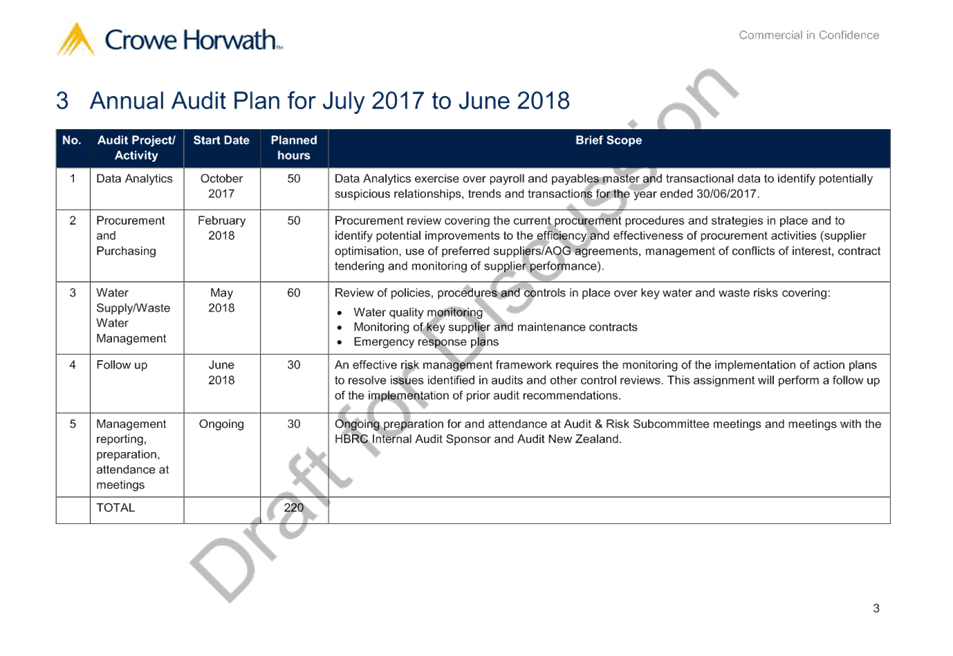

10.1. Data Analytics

10.2. Procurement and

Purchasing

10.3. Water Supply/Wastewater

Management.

11. It is proposed that the

Data Analytics internal audit be completed initially, with intention to provide

the audit report at the 4 December Finance, Audit and Risk

Sub-committee meeting. Scoping document for this is appended as Attachment

One. The second and third audit reports would be presented at the first and

second Sub-committee meetings respectively in 2018 (dates to be confirmed).

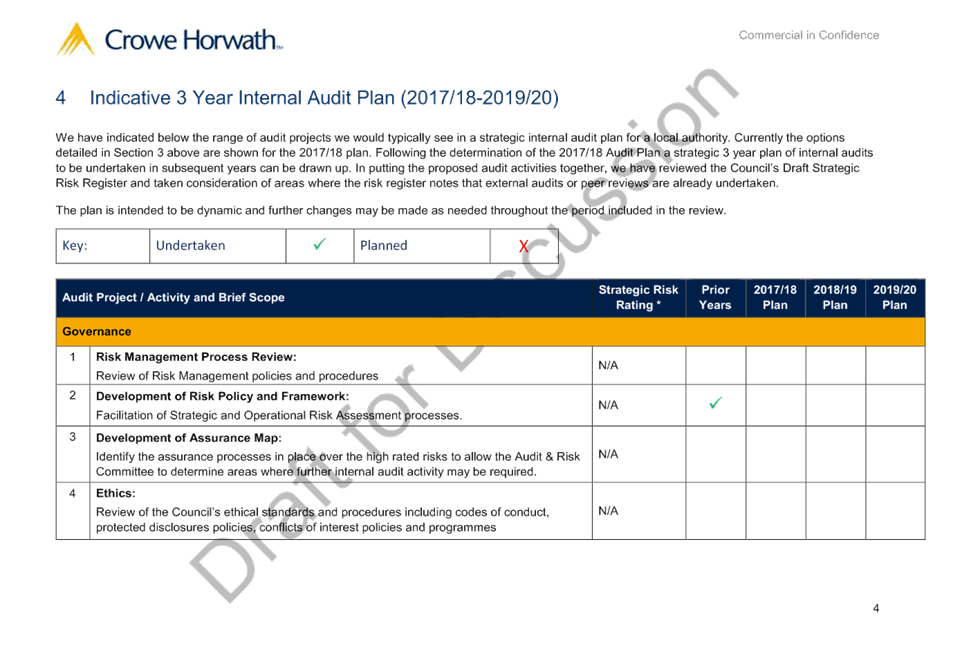

12. Further areas discussed

that may require the attention of an internal audit in future years are also

provided in the Proposed Internal Audit Plan appended as Attachment Two.

A decision on these areas is not required immediately.

Decision Making

Process

13. Staff have assessed the

requirements of the Local Government Act 2002 in relation to this item and have

concluded that, as this report is for information only, the decision making

provisions do not apply.

|

Recommendations

That the

Finance, Audit and Risk Sub-committee:

1. Receives and

notes the “Introduction to the Internal Audit Service Provider”

staff report

2. Agrees to the

schedule of Internal Audits to be carried out during the 2017-18 year, being:

2.1. Data Analytics

2.2. Procurement and Purchasing

2.3. Water Supply/Wastewater

Management

3. Notes that

the cost of the internal audits carried out in 2017-18 will be funded from

the financial provisions set aside for such audits in the Annual Plan.

|

Authored by:

|

Melissa des

Landes

Management Accountant

|

|

Approved by:

|

Jessica

Ellerm

Group Manager

Corporate Services

|

|

Attachment/s

|

⇩1

|

Crowe Horwath

Data Analysis Scoping Document

|

|

|

|

⇩2

|

Proposed

Internal Audit Plan 2017-18

|

|

|

|

Crowe

Horwath Data Analysis Scoping Document

|

Attachment 1

|

|

Proposed Internal Audit

Plan 2017-18

|

Attachment 2

|

|

Proposed

Internal Audit Plan 2017-18

|

Attachment 2

|

|

Proposed

Internal Audit Plan 2017-18

|

Attachment 2

|

HAWKE’S BAY REGIONAL COUNCIL

Finance

Audit & Risk Sub-committee

Tuesday 19 September 2017

Subject: Internal Audit Report -

Event Response Review

Reason for Report

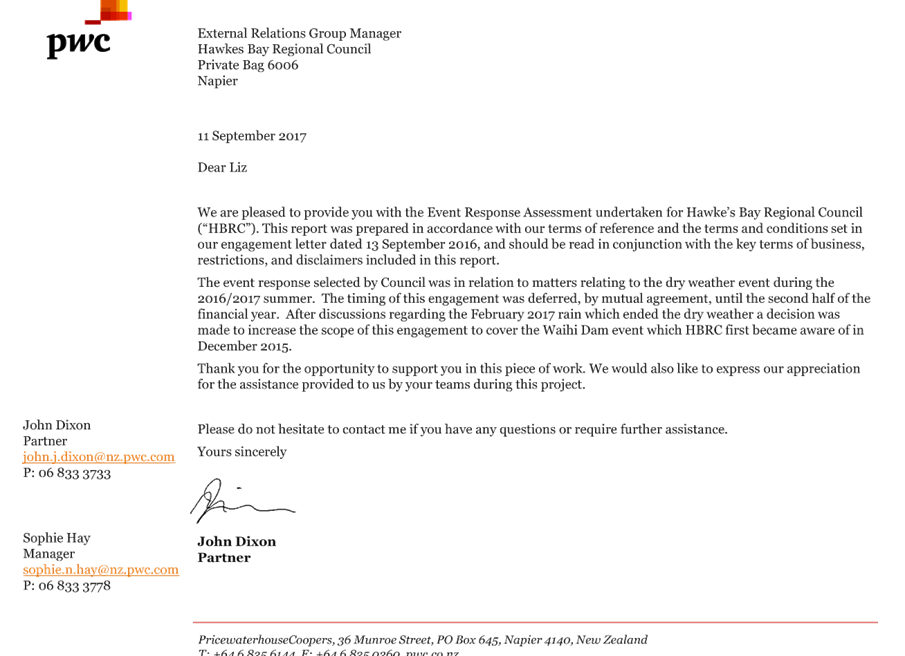

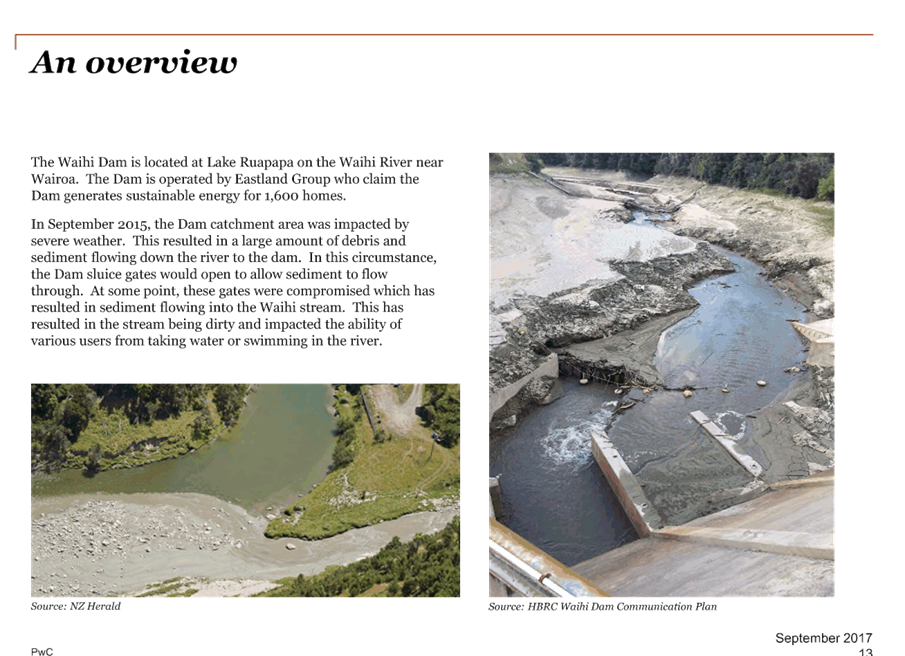

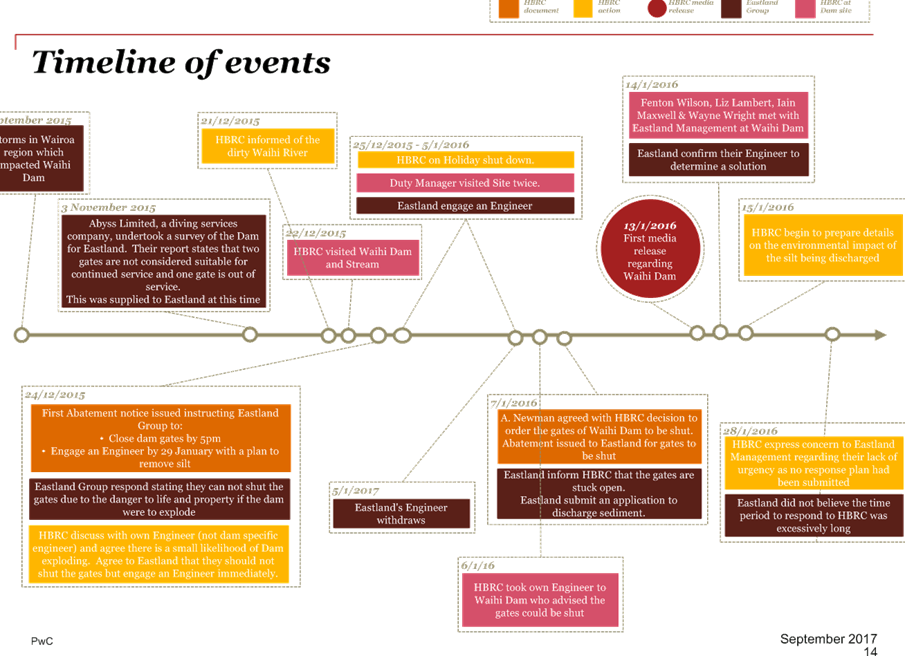

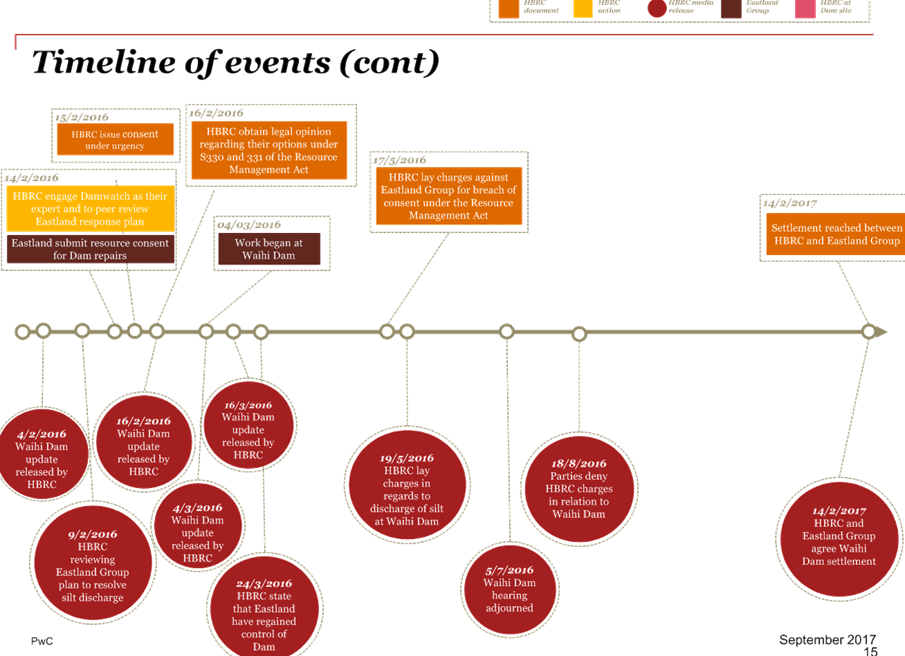

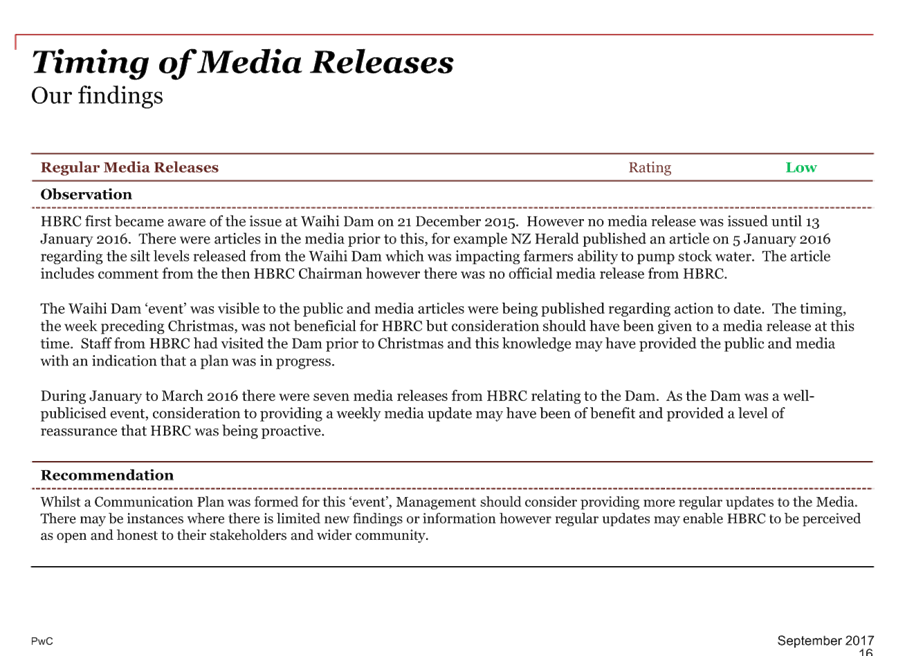

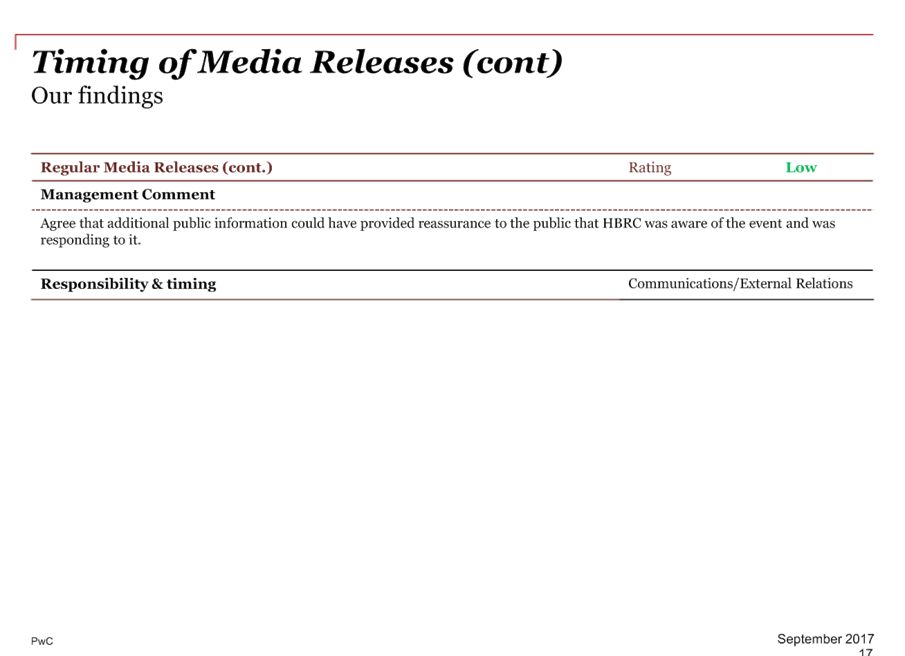

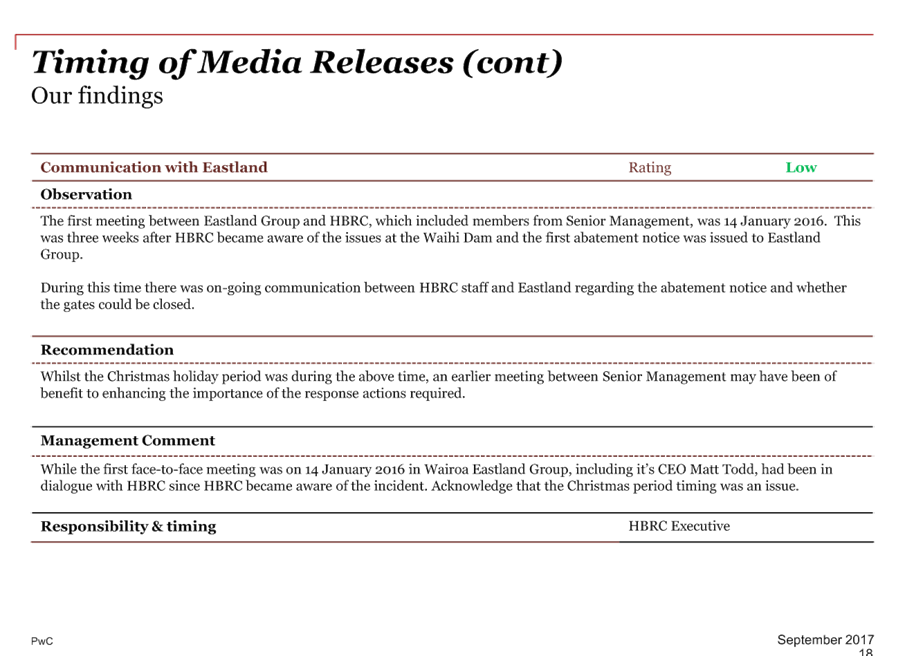

1. PricewaterhouseCoopers

(PWC) has completed the internal audit for Event Response, and their report is

attached for review by the Sub-committee.

Background

2. The Finance,

Audit & Risk Sub-committee agreed at its meeting on 20 September 2016, as

part of the internal audit work programme to engage PWC to conduct an internal

audit on Event Response with a focus on communications.

3. Prior to

commencement, PWC agreed, with the Group Manager – External Relations, to

proceed with the 2016-17 ‘Summer Dry’ event. It was subsequently

decided to increase the scope of the agreement to include the ‘Waihi

Dam’ event in addition.

Decision Making Process

4. Staff have

assessed the requirements of the Local Government Act 2002 in relation to this

item and have concluded that, as this report is for information only, the

decision making provisions do not apply.

|

Recommendations

That the

Finance, Audit and Risk Sub-committee receives and notes the “Internal

Audit Report - Event Response Review” report.

|

Authored by:

|

Melissa des

Landes

Management Accountant

|

|

Approved by:

|

Jessica

Ellerm

Group Manager

Corporate Services

|

Liz Lambert

Group Manager

External Relations

|

Attachment/s

|

⇩1

|

Event

Response Internal Audit Report

|

|

|

|

Event

Response Internal Audit Report

|

Attachment 1

|

HAWKE’S BAY REGIONAL COUNCIL

Finance

Audit & Risk Sub-committee

Tuesday 19 September 2017

Subject: Resource Management

Information System Implementation Update

Reason for Report

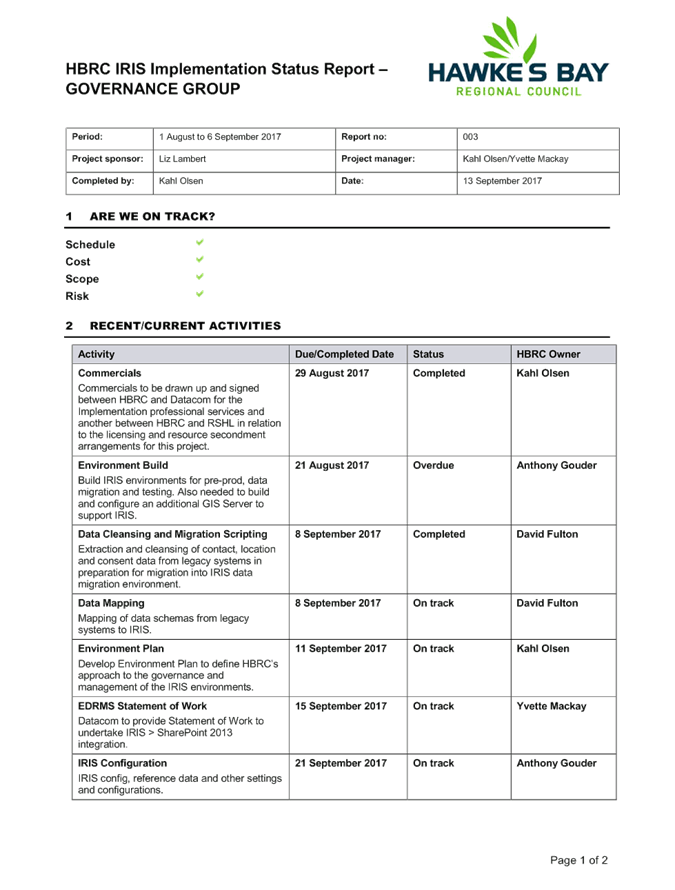

1. At its meeting on 28 June 2017 the Council confirmed

the expenditure of $1,100,000 as included in the 2017-18 Annual Plan for the

implementation of the resource management information system software and

related mobile technology, and confirmed the selection

of the Integrated Regional Information System (IRIS) as the resource management

information system to be implemented.

2. Staff have undertaken to provide an update on progress of the

implementation of the new software on a regular basis to the Finance, Audit and

Risk sub-committee. This report is the first of these updates.

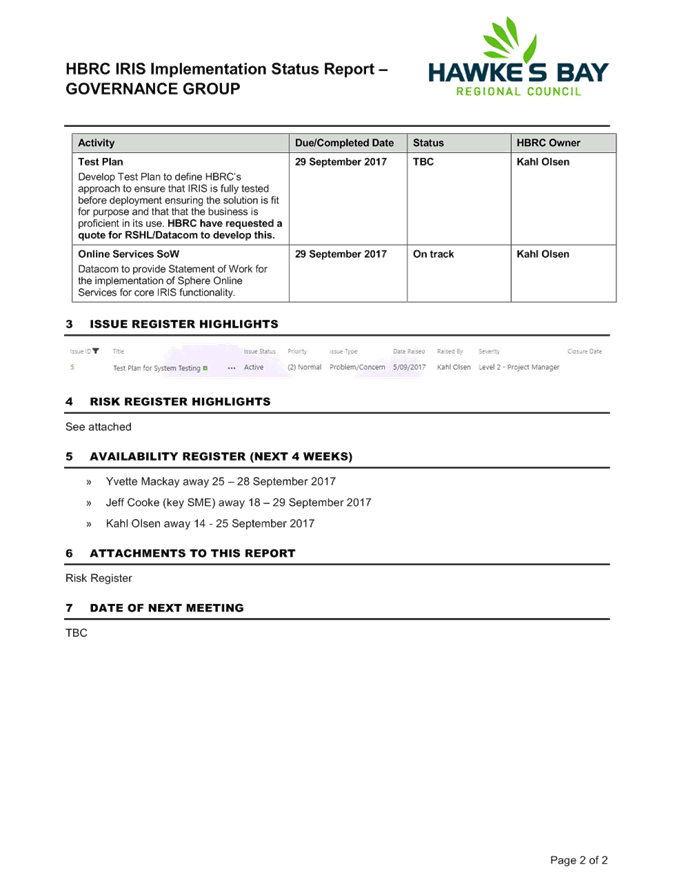

3. Attachment 1 to this paper presents the

status report for this project as presented to the IRIS Governance Group

meeting on 13 September 2017.

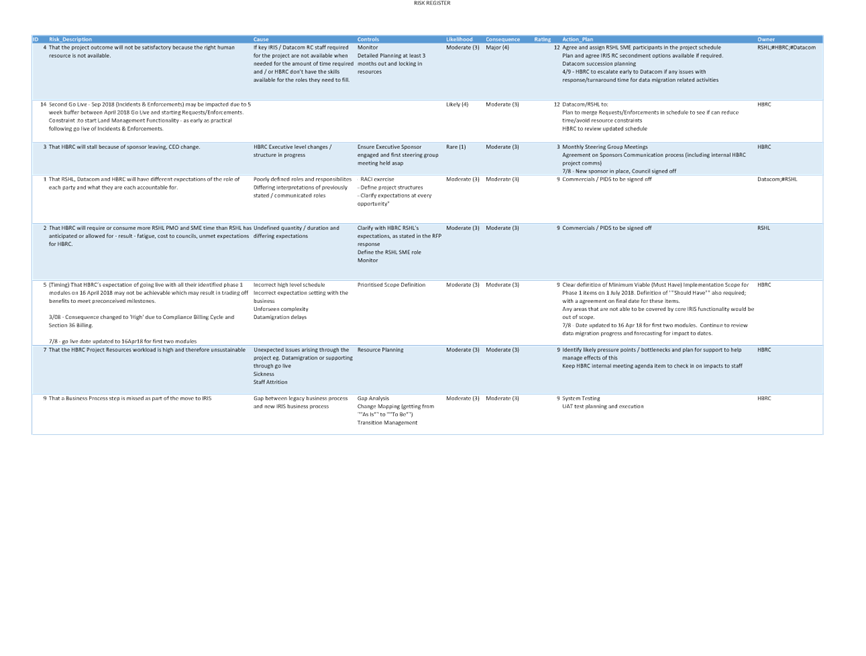

4. Attachment 2 is the risk register for

the project which is reviewed at each governance group meeting.

Decision Making

Process

5. Staff have

assessed the requirements of the Local Government Act 2002 in relation to this

item and have concluded that, as this report is for information only, the

decision making provisions do not apply.

|

Recommendation

That the Finance, Audit & Risk

Sub-committee receives and notes the “Resource Management Information

System Implementation Update” report.

|

Authored by:

|

Kahl Olsen

Information and Communications Technology

Manager

|

|

Approved by:

|

Liz Lambert

Group Manager

External Relations

|

|

Attachment/s

|

⇩1

|

IRIS Project

Status Report

|

|

|

|

⇩2

|

IRIS Project

Risk Register

|

|

|

|

IRIS

Project Status Report

|

Attachment 1

|

|

IRIS Project Risk Register

|

Attachment 2

|

HAWKE’S BAY REGIONAL COUNCIL

Finance

Audit & Risk Sub-committee

Tuesday 19 September 2017

Subject: 2016-17 Annual Report -

Audit NZ Discussions

Reason for Report

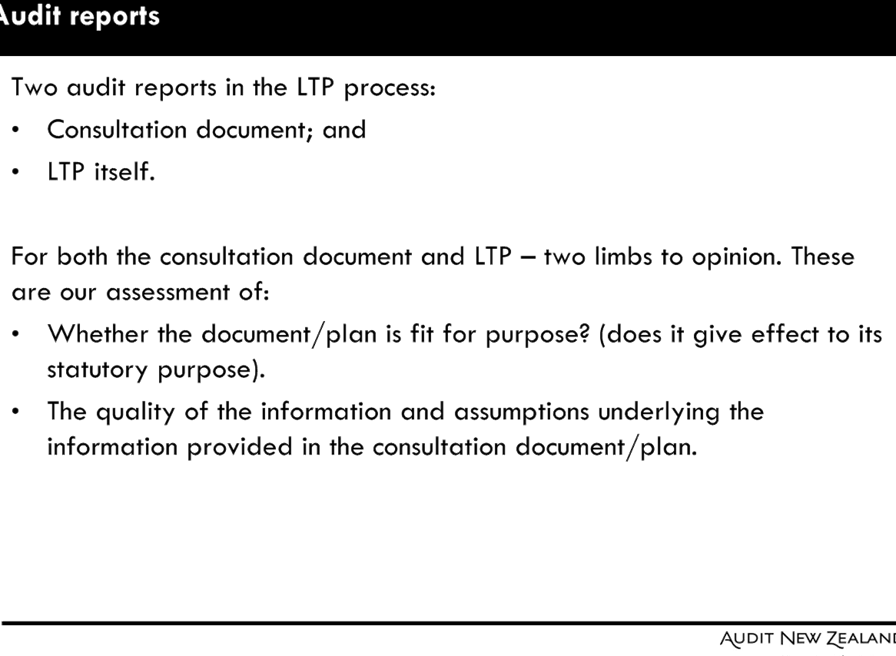

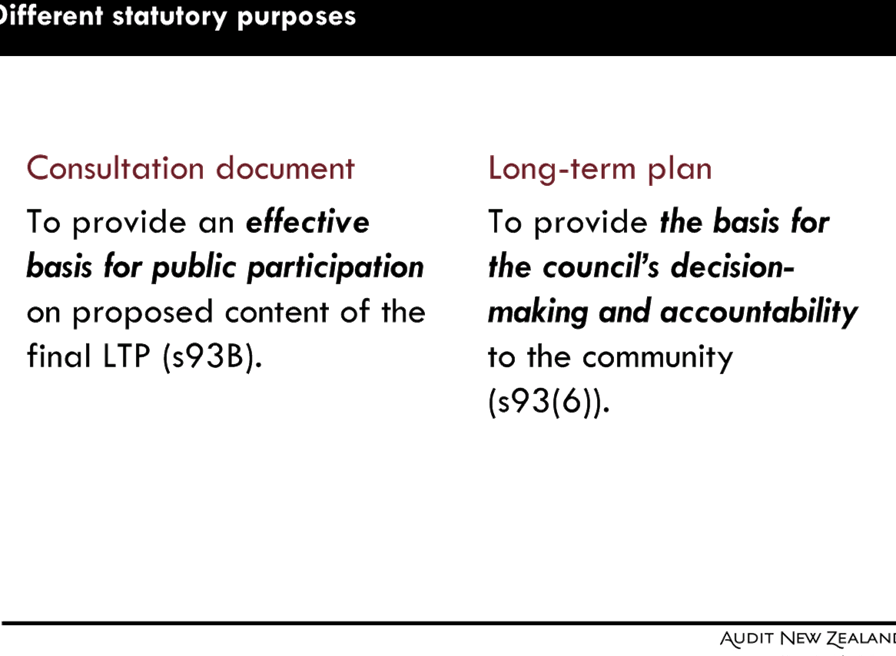

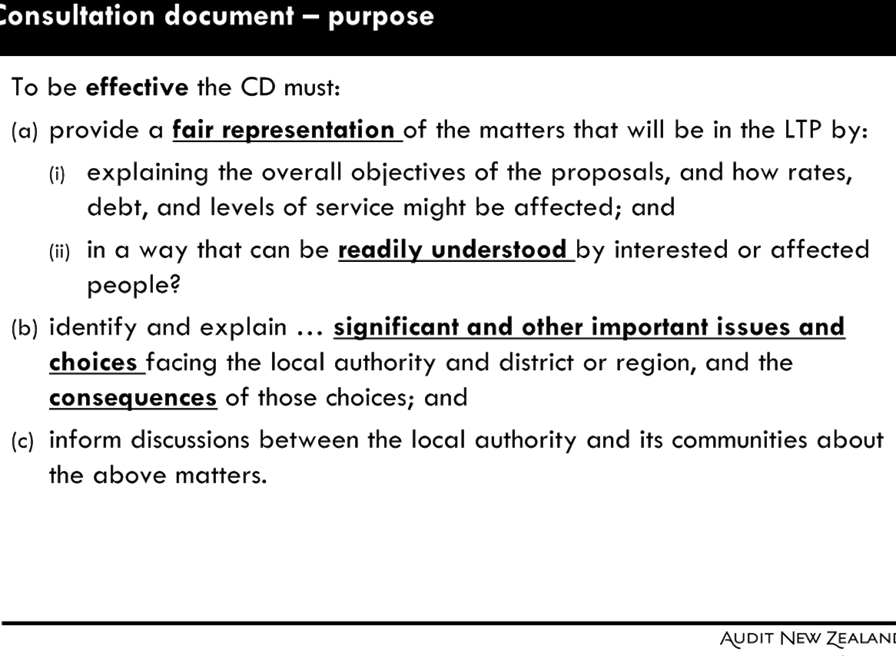

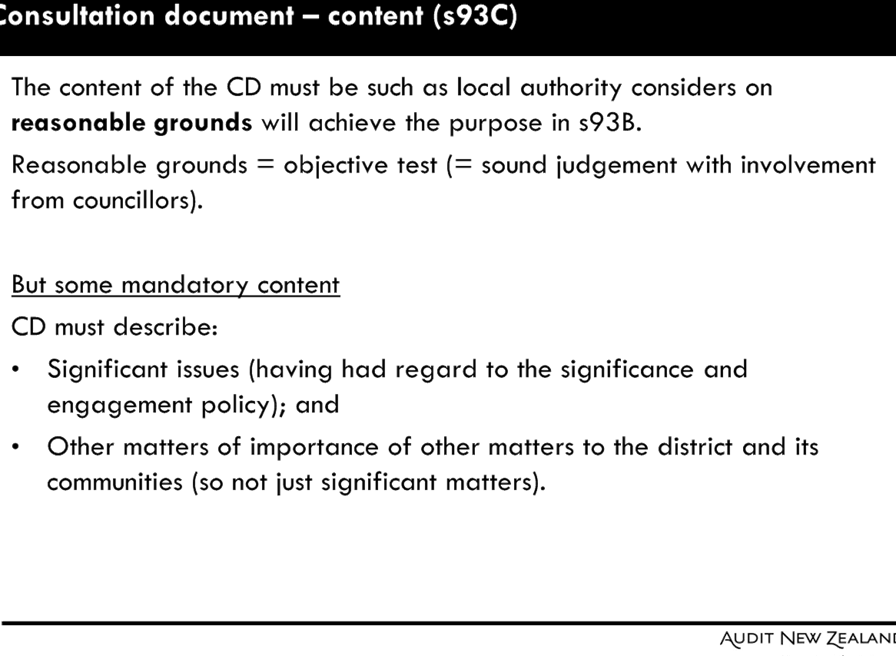

1. To provide the

sub-committee with an opportunity to discuss matters in relation to the audit

of Hawke’s Bay Regional Council’s (HBRC) and Group financial

statements for the year ending 30 June 2017 with Stephen Lucy, Director Audit

NZ.

2. Stephen Lucy

will also provide information and matters relating to the Long Term Plan for

the sub-committee’s consideration.

Comment

3. At the time of

writing this paper the audit work for HBRC has been completed and Audit NZ is

awaiting the final HBRIC Ltd financial statements so that the consolidated

group financial statements can be confirmed.

4. To enable

discussions, attached are:

4.1. the current

Draft 2016-17 Annual Report (included under separate cover for Sub-committee

members only in accordance with LGOIMA section 2(b)(ii) the withholding of the

information is necessary to protect information where the making available of

the information would be likely unreasonably to prejudice the commercial

position of the person who supplied or who is the subject (HBRIC Ltd) of the

information)

4.2. Stephen

Lucy’s comments on the HBRC financial statements for the year ending 30

June 2017

4.3. areas

relating to the HBRC 2018-28 LTP that that Stephen Lucy proposes to discuss.

5. The final

audited Annual Report will be presented to Council for adoption at its meeting

on 25 October 2017.

6. If required,

there will be an opportunity for Sub‑committee member only discussions

with Stephen at the conclusion of these discussions.

Decision Making

Process

7. As this report

is for information only and no decision is to be made, the decision making

provisions of the Local Government Act 2002 do not apply.

|

Recommendations

That the Finance Audit and Risk Sub-committee receives and notes

the issues raised by Stephen Lucy, Director Audit NZ, for discussion on

HBRC’s Annual Report for Year Ending 30 June 2017 and the 2018-28 Long

Term Plan.

|

Authored by:

|

Manton

Collings

Corporate Accountant

|

Jessica

Ellerm

Group Manager

Corporate Services

|

Approved by:

|

James Palmer

Chief Executive

|

|

Attachment/s

|

⇩1

|

Audit NZ

Comments on 2016-17 Annual Report

|

|

|

|

⇩2

|

Audit NZ

Comments on Long Term Plan Development

|

|

|

|

Audit

NZ Comments on 2016-17 Annual Report

|

Attachment 1

|

|

Audit NZ Comments on Long

Term Plan Development

|

Attachment 2

|

HAWKE’S BAY REGIONAL COUNCIL

Finance

Audit & Risk Sub-committee

Tuesday 19 September 2017

Subject: September 2017 Update

on the Sub-committee Work Programmes

Reason for Report

1. In order to ensure the sub-committee’s ability to effectively

and efficiently fulfill its role and responsibilities, an overall update on its

work programme is provided following.

|

Task

|

Item

|

Scheduled / Status

|

|

Internal Audits

|

Fraud

Detection and Prevention Review Report

|

Completed

2016

|

|

Taxation

Review

|

Completed

& presented to May 2017 FA&R meeting

|

|

Event

Response Review

|

Completed

– to be presented to September 2017 FA&R meeting

|

|

Agree and

schedule Internal Audit Programme for the remainder of 2017-18. Proposed are:

1. Data Analytics

2. Procurement and Purchasing

3. Water Supply/Wastewater Management

|

19 September

FA&R meeting

|

|

Risk Assessment & Management

|

Reporting on

risks (6-monthly) affecting Council

|

January

& September FA&R meetings

|

|

|

Review

previous 6-month Risk Assessment to note changes / improvements / areas that

require attention

|

|

|

Sub-committee

to carry out detailed review of individual Groups’ Risk Management (as

part of the programmed reviews of activities)

|

|

Insurance

|

Council’s

proposed 2017-18 Insurance programme

|

Insurance

Broker presented at May 2017 FA&R meeting

|

|

Annual Report

|

Discussion

on the major issues (if any) in the audit report on the Annual Report.

|

Auditor to

attend September 2017 FA&R meeting

|

|

Discussion

on Audit Management Letter

|

Auditor

scheduled to attend December 2017 FA&R meeting

|

|

Reviews

|

Review of

Council expenditure on delivery of functions with a view to ensuring and/or

enhancing efficiency

|

Completed

and findings reported to 31 May 2017 Council meeting, which resolved: Refers

the recommendations made by the Operational Efficiency Review report to the

incoming Chief Executive for consideration and reporting back to Council,

where appropriate, on initiatives for implementation. This work is

ongoing and forms part of the LTP process.

|

|

Review of

the Council’s capital structure, taking into account the values of

dividends in supporting Council operations

|

The panel

has met three times, and on 15 September received a presentation from

Flagstaff on potential Capital Ownership options for PONL. A report writer

has been appointed to collate background information on each of the three

organisations involved, and is in contact with staff and panel members to

ensure the views of the panel will be synthesized. Draft report of the review

findings to be presented in to the 11 October Council LTP workshop.

|

|

Comprehensive

review of the HBRC Risk Assessment and Management process to ensure major

strategic risks to the public and environment are appropriately managed

|

Review

completed and updated report presented to 19 September 2017 FA&R meeting

|

|

LTP Process

|

Update on

Process

External

Funding

Rates Review

|

Feedback

from Audit NZ from 2015 LTP audits included on 19Sept agenda

Assessment

of External Funding options and Rates Review is currently underway.

Full LTP

development update on 20 Sept Corporate & Strategic Committee agenda

|

Decision Making Process

2. As this report

is for information only and no decision is to be made, the decision making

provisions of the Local Government Act 2002 do not apply.

|

Recommendation

That the Finance, Audit and Risk

Sub-committee receives and notes the “September 2017 Update on

Sub-committee Work Programmes” staff report.

|

Authored by:

|

Manton

Collings

Corporate Accountant

|

Melissa des

Landes

Management Accountant

|

Approved by:

|

Jessica

Ellerm

Group Manager

Corporate Services

|

|

Attachment/s

There are no

attachments for this report.

HAWKE’S BAY REGIONAL COUNCIL

Finance

Audit & Risk Sub-committee

Tuesday 19 September 2017

Subject: Risk Assessment and

Management

That Council excludes the public

from this section of the meeting, being Agenda Item 10 Risk Assessment and

Management with the general subject of the item to be considered while the

public is excluded; the reasons for passing the resolution and the specific

grounds under Section 48 (1) of the Local Government Official Information and

Meetings Act 1987 for the passing of this resolution being:

|

GENERAL SUBJECT OF THE ITEM TO BE

CONSIDERED

|

REASON FOR PASSING THIS RESOLUTION

|

GROUNDS UNDER SECTION 48(1) FOR THE

PASSING OF THE RESOLUTION

|

|

Risk Assessment and Management

|

7(2)(b)(ii) That the public conduct of this agenda item

would be likely to result in the disclosure of information where the

withholding of that information is necessary to protect information which

otherwise would be likely unreasonably to prejudice the commercial position

of the person who supplied or who is the subject of the information.

7(2)(i) That the public conduct of this agenda item would

be likely to result in the disclosure of information where the withholding of

the information is necessary to enable the local authority holding the

information to carry out, without prejudice or disadvantage, negotiations

(including commercial and industrial negotiations).

|

The Council is specified, in the First Schedule to this

Act, as a body to which the Act applies.

|

Authored by:

|

Melissa des

Landes

Management Accountant

|

|

Approved by:

|

Jessica

Ellerm

Group Manager

Corporate Services

|

|